Packaging Wax Market to Grow to $3.7 Billion by 2034 Driven by Sustainability and Functional Coatings

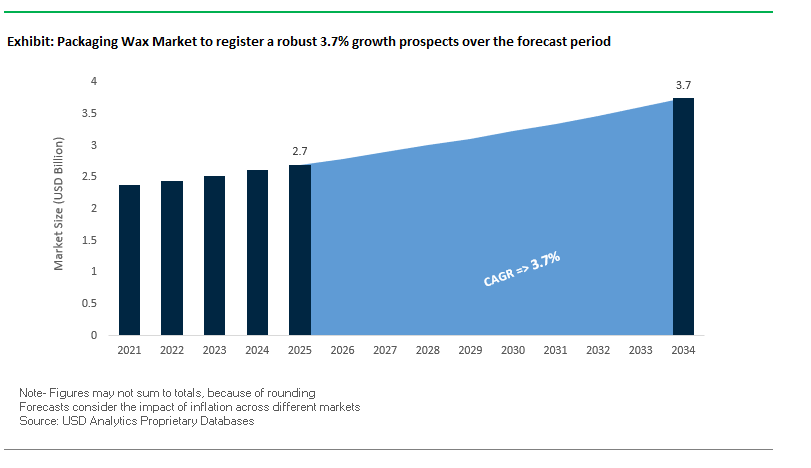

The Global Packaging Wax Market is projected to increase from $2.7 billion in 2025 to $3.7 billion by 2034, at a CAGR of 3.7%. The market provides essential waxes and wax blends that enhance moisture resistance, grease resistance, and surface gloss, crucial for food, beverage, and paper-based packaging. The industry plays a pivotal role in preserving product integrity, supporting sustainability initiatives, and enabling high-quality printing on coated surfaces.

Key Insights for Packaging Professionals:

- Barrier Performance Remains a Priority: Wax coatings are critical for moisture and grease protection, particularly in milk cartons, frozen foods, and fast-food packaging.

- Shift Toward Bio-Based Waxes: Demand is growing for soy, beeswax, and carnauba wax as alternatives to petroleum-based paraffin waxes, aligning with corporate sustainability goals.

- Food-Safe and Low-Migration Formulations: Increasing regulations and consumer awareness are driving adoption of non-migratory, safe wax coatings.

- Printability Enhancements: Wax formulations are being engineered to support high-quality printing, maintaining brand aesthetics on coated surfaces.

- Sustainable Packaging Integration: Wax coatings are increasingly applied to recyclable, compostable, and paper-based packaging materials.

Recent Strategic Developments in Packaging Wax Reflect Consolidation, Sustainability, and Advanced Functionalities

The Global Packaging Wax Industry continues to evolve with major acquisitions, sustainability initiatives, and technological advancements. In August 2025, LyondellBasell’s joint venture GXLYB received an FDA No Objection Letter for its recycled PP and HDPE resins, enabling broader adoption in food-contact packaging, including wax-coated paper applications. In July 2025, the all-stock combination of Amcor and Berry Global Group closed, creating a global packaging leader, which is expected to boost demand and innovation in wax-coated packaging.

May 2025 witnessed Durst Group acquiring callas software, enabling more integrated digital printing capabilities for wax-coated packaging. Strategic acquisitions continued with International Paper completing its $9.9 billion acquisition of DS Smith in April 2025, strengthening its European footprint in sustainable paper packaging, a major end-user of wax coatings.

Sustainability-driven innovation also surged, with Billerud launching heat-sealable, fossil-free papers in March 2025 that rely on wax coatings for functional barriers. January 2025 marked Ahlstrom’s launch of MasterTape® Cristal, a recyclable paper-based tape backing, highlighting a broader trend toward paper-based innovations. Key industry consolidations include Smurfit Kappa acquiring WestRock in October 2024, creating a corrugated packaging giant. Finally, ExxonMobil launched Prowaxx™ in April 2024, signaling strategic product differentiation and innovation in the wax segment.

Trends and Opportunities Reshaping the Packaging Wax Market

Accelerated Regulatory Phase-Out of Paraffin Wax in Food-Contact Applications

The packaging wax market is undergoing a rapid shift due to regulatory, environmental, and recycling challenges associated with paraffin wax. The EU’s Packaging and Packaging Waste Regulation (PPWR), which came into effect in February 2025, has reinforced the industry’s transition by restricting substances of concern (SoC) and emphasizing recyclable and renewable inputs. Although paraffin wax is not directly banned, its petroleum-derived origin and incompatibility with paper recycling streams have made it a target for replacement.

Major foodservice and retail brands are actively phasing out paraffin wax from their supply chains to meet ESG commitments and sustainability targets. A 2024 non-profit industry report noted that brands like McDonald’s and Restaurant Brands International pledged to remove PFAS and hazardous coatings from food packaging by 2025, a commitment that indirectly accelerates the phase-out of paraffin wax. Recycling efficiency is another driver: paraffin-coated papers contaminate the pulping process, reducing the value of recovered fibers. As a result, converters are pivoting to bio-based waxes and alternative coatings that meet recyclability and safety requirements.

Strategic Shift to Bio-Based and Synthetic Barrier Coatings

The second major trend in the packaging wax industry is the rapid commercialization of bio-based waxes and hybrid coatings that combine sustainability with performance. Rice bran wax, a byproduct of rice milling, is emerging as a high-potential alternative, with companies like Clariant reporting renewable carbon indices above 98% and up to 80% lower carbon footprints compared to fossil-based waxes.

Hybrid polymer-mineral blends are also gaining traction. For example, Smart Planet Technologies has developed coatings using PLA resins combined with mineral fillers, which cut plastic content by up to 51% and ensure recyclability in premium fiber streams. Additionally, degradable synthetic waxes and polymeric coatings are being engineered for oil and moisture resistance, rivaling paraffin in food-contact applications while ensuring compostability and recyclability. These materials deliver thermal sealing capabilities, high melting points, and reduced environmental impact, positioning them as the next generation of barrier coatings.

Development of High-Performance Hybrid Waxes for Industrial Applications

A promising growth avenue lies in industrial-grade hybrid waxes that deliver durability, corrosion resistance, and weather-proofing for metal packaging, agricultural sacks, and heavy-duty industrial applications. Modified vegetable waxes, treated through hydrogenation and interesterification, are being developed to achieve higher melting points and mechanical strength, making them suitable for high-performance protective coatings.

Academic research supports this direction, showing that wax-impregnated papers treated with hybrid formulations exhibit enhanced hydrophobicity, thermal stability, and mechanical resistance, outperforming conventional wax solutions. Moreover, advances in flow-through synthesis have cut reaction times from 12 hours to just 30 minutes, enabling scalable, cost-efficient production. This industrialization potential gives hybrid waxes a strong pathway for commercialization in industrial and logistics packaging segments.

Bio-Wax Coatings for Home-Compostable Flexible Packaging

The second key opportunity is the development of bio-wax coatings tailored for home-compostable paper packaging. With consumer demand surging for certified home-compostable solutions, waxes derived from natural sources such as taro leaves, soy, or other plant-based feedstocks are being engineered to provide moisture resistance and barrier protection for food and dry goods packaging.

Unlike industrial composting standards (ASTM D6400), home compostability requires degradation under ambient, low-temperature conditions, which is now a central innovation focus. Companies are commercializing wax-coated pouches and wraps that are moisture-proof, biodegradable, and align with zero-waste goals for fresh produce, bakery items, and organic-certified products. Early adopters in the retail and foodservice sectors are leveraging these coatings to differentiate their brands, reduce landfill waste, and offer consumers an eco-friendly end-of-life option for everyday packaging.

Competitive Landscape in Packaging Wax Shows a Shift Toward Sustainability, Customization, and High-Performance Solutions

The global packaging wax market is driven by players leveraging expertise in wax formulations, petroleum refining, and sustainability to serve food, paper, and industrial packaging applications. Leading companies focus on high-performance coatings, bio-based alternatives, and custom blends to meet evolving regulatory and consumer demands.

ExxonMobil: Driving Differentiated Wax Products Through Global Refining Expertise

ExxonMobil leverages its extensive refining network to produce high-quality paraffin and microcrystalline waxes. In April 2024, the company launched Prowaxx™, enhancing its product differentiation in packaging waxes. ExxonMobil provides fully refined, semi-refined, and slack waxes for coatings, lamination, and paper-based packaging, emphasizing quality, reliability, and superior performance.

Sinopec Corp: Expanding Sustainable Wax Applications Across Asia

Sinopec is a leading producer of petroleum-based waxes in Asia, with strong refining capacity and a broad portfolio of paraffin grades for coatings and moisture barriers. In August 2025, Sinopec introduced bio-based PP for high-end cosmetics packaging, reflecting its commitment to sustainable packaging solutions. The company focuses on technological innovation and circular economy principles to meet evolving industry demands.

The International Group, Inc. (IGI): Custom Wax Blends for High-Performance and Eco-Conscious Packaging

IGI specializes in custom wax blends and specialty waxes, including paraffin, microcrystalline, and soy waxes. Its sustainability initiatives emphasize plant-derived and eco-friendly solutions, supporting circular economy practices. IGI’s products offer moisture barriers, high-performance coatings, and print-friendly surfaces, catering to paper and corrugated packaging industries.

Blended Waxes, Inc.: Tailoring Custom Wax Solutions for Specialized Packaging Needs

Blended Waxes provides custom wax blends and toll manufacturing, focusing on hot melt adhesives, lamination waxes, and moisture barriers. Its portfolio includes paraffin, microcrystalline, and natural waxes, designed for unique packaging applications. The company prioritizes quality, customization, and innovation to address evolving market requirements.

Shell PLC: Integrating Specialty Waxes with Sustainable Practices for Industrial Packaging

Shell produces paraffin and microcrystalline waxes, including specialty grades for coatings, hot melt adhesives, and high-performance packaging applications. The company is actively pursuing an energy transition strategy, investing in sustainable technologies and partnerships. Shell focuses on providing high-performance wax solutions while contributing to a more sustainable and low-carbon packaging ecosystem.

Packaging Wax Market Share Insights, 2025-2034

Paraffin Wax Dominates Market Share by Wax Type in the Packaging Wax Industry

Paraffin wax continues to hold the largest market share at 55% within the packaging wax industry, primarily due to its unbeatable cost-to-performance ratio. It remains the workhorse material for high-volume applications such as corrugated board coatings and case sealing, where moisture resistance and scalability are critical. The paraffin segment benefits directly from the e-commerce boom, which drives demand for moisture-protected corrugated packaging across global supply chains. Microcrystalline wax, holding around 20% share, sustains demand in premium and performance-driven applications thanks to its superior adhesion, flexibility, and high melting point, making it ideal for composite coatings and hot-melt adhesives used in demanding environments. Polyethylene wax has carved out a niche by serving as a functional additive, improving abrasion resistance and scuff protection in printed and laminated packaging. Meanwhile, natural waxes are the fastest-growing category, fueled by sustainability mandates and brand owners’ ESG commitments, despite their higher costs and supply chain limitations. The “Others” category, including Fischer-Tropsch and specialized synthetics, remains small but strategically critical in formulations requiring precise melting points, chemical stability, or niche performance enhancements, particularly in adhesives and barrier coatings.

Corrugated Board Coating Holds the Largest Market Share by Application in the Packaging Wax Industry

Corrugated board coating accounts for 40% of the packaging wax market, making it the single largest application segment. This dominance is directly tied to the growth of online retail and global logistics, where corrugated boxes treated with paraffin wax deliver essential moisture resistance, durability, and stacking strength. Flexible packaging follows with a significant share at 25%, driven by the rising consumption of frozen foods, dairy, and beverages, where wax blends create reliable barriers against vapor and gases while maintaining sealability. The food and beverage sector, while smaller in scale, represents a high-value opportunity because it demands FDA-compliant waxes for direct food contact applications such as fruit coatings, cheese preservation, and beverage cup linings. Paper and paperboard coatings add further volume by serving cups, folding cartons, and decorative wraps, where wax enhances both aesthetics (gloss finish) and functionality (barrier protection). Hot-melt adhesives represent another critical application, where wax plays a performance-modifying role in controlling viscosity and set times, particularly in automated packaging lines. Other specialized uses, such as explosives packaging, corrosion protection, and industrial coatings, although niche, are essential for safety and compliance in highly regulated industries.

United States Packaging Wax Market Driven by EPR Laws and Sustainable Investments

The United States packaging wax market is evolving rapidly under the influence of Extended Producer Responsibility (EPR) laws. By 2025, one in five Americans live in states with active EPR regulations such as Maine, Maryland, and Washington, compelling companies to use recyclable and post-consumer recycled (PCR) waxes for packaging. This legislative environment is pushing demand for waxes that support sustainability while maintaining protective and barrier properties.

Corporate investments are also reshaping the sector. In August 2025, top players including General Mills, Mars, and PepsiCo launched the US Flexible Film Initiative (USFFI), a non-profit targeting scalable recycling solutions for flexible packaging, directly impacting packaging wax applications. At the same time, innovation is centered on mono-material paper-based structures with recyclable wax coatings, which mimic the barrier properties of multi-material plastics. Key applications remain concentrated in corrugated boxes, e-commerce shipping solutions, and food and beverage packaging, where FDA compliance on direct and indirect food-contact resins and waxes is critical.

Germany Packaging Wax Market Strengthened by PPWR and Circular Economy Mandates

The Germany packaging wax market operates under the European Union’s Packaging and Packaging Waste Regulation (PPWR), effective from February 2025, which sets mandatory targets for recyclability and reuse. This regulation, alongside the German Packaging Act (VerpackG), drives companies to adopt sustainable and recyclable wax-based coatings that align with EU sustainability objectives.

German manufacturers are recognized for technological innovation in bio-based waxes, including coatings derived from PLA, PHA, cellulose, and vegetable oils. Additionally, the industry is preparing for the EU Deforestation Regulation (EUDR), requiring paper-based packaging coated with wax to be deforestation-free by December 2025. Applications remain strong across food, beverage, and cosmetics packaging, where waxes enhance shelf life, product presentation, and compliance with safety standards, reinforcing Germany’s leadership in eco-friendly packaging innovation.

China Packaging Wax Market Expanding Under Dual-Carbon Goals and Smart Standards

The China packaging wax market is expanding quickly, fueled by the government’s dual-carbon goals to peak emissions by 2030 and achieve neutrality by 2060. Policies such as the June 2025 express delivery regulations encourage the adoption of eco-friendly and reusable wax-coated packaging materials, crucial for a nation handling 175 billion parcels annually in 2024.

The State Administration for Market Regulation has also announced nine new recycled plastics standards effective from February 2026, which include guidance for wax-coated packaging. These standards demand recyclability-focused design, reduced adhesives, and efficient material separation. Chinese manufacturers are increasingly investing in AI-driven production and automation, enhancing both efficiency and traceability. With booming demand in consumer goods, electronics, and food sectors, China is set to remain a global hub for high-quality and sustainable packaging waxes.

India Packaging Wax Market Supported by Make in India and Manufacturing Expansions

The India packaging wax market is witnessing accelerated growth under government-backed initiatives like Make in India and the Production Linked Incentive (PLI) scheme, which emphasize domestic manufacturing and self-reliance. New EPR mandates requiring 30% recycled content in rigid plastics by April 2025 directly influence packaging wax adoption across industries.

Corporate expansions highlight strong momentum. In March 2023, Payal Group doubled its chlorinated paraffin wax capacity to 70 kilotons at its Gujarat facility, positioning itself as a key supplier to packaging and industrial sectors. Indian manufacturers are also investing in automation and robotics integration for efficient wax processing and application. Key end-use markets include food and beverage packaging, e-commerce logistics, and FMCG industries, where wax coatings are essential for moisture resistance, product safety, and branding customization.

Japan Packaging Wax Market Driven by Positive List System and Bio-Based Innovation

The Japan packaging wax market is adapting to the positive list system for food-contact materials, effective June 1, 2025, which strictly defines substances permissible in wax coatings and adhesives for packaging. This regulation ensures higher compliance in food and beverage applications, reinforcing safety standards across the supply chain. At the same time, QR code-enabled e-labeling is expanding, requiring printable and adaptable wax-coated surfaces.

Japanese companies are at the forefront of bio-based wax innovation, developing eco-friendly wax coatings for paper-based barrier materials designed for fragile and temperature-sensitive packaging. The government’s commitment to cut GHG emissions by 46% by 2030 and achieve net-zero by 2050 has accelerated investment in recyclable and compostable waxes. Demand is particularly strong in ready-to-drink beverages, snacks, and premium consumer goods, where design quality, durability, and sustainability converge to drive innovation in wax-coated packaging.

Brazil Packaging Wax Market Driven by ANVISA Regulation and Food Industry Demand

The Brazil packaging wax market is evolving under Anvisa’s RDC No. 983/2025, which updates food-contact packaging standards and enforces a phase-out of certain unsafe materials. Coupled with the National Solid Waste Policy (PNRS), this regulation pushes manufacturers toward safer and recyclable waxes that meet both domestic and international compliance standards.

Technological progress is evident in the adoption of sustainable wax manufacturing techniques aligned with global food safety benchmarks. The food and beverage sector remains the largest consumer of packaging wax in Brazil, particularly for canned goods, processed foods, and export packaging. Corporate investment trends show companies enhancing facilities and complying with Conasq’s updated chemical safety register, which mandates safer raw materials in plastics and coatings. This regulatory and technological environment positions Brazil as a growing hub for sustainable packaging wax innovation in Latin America.

Packaging Wax Market Report Scope

Packaging Wax Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.7 Billion

|

|

Market Size (2034)

|

$3.7 Billion

|

|

Market Growth Rate

|

3.7%

|

|

Segments

|

By Wax Type (Paraffin, Microcrystalline, Polyethylene, Natural, Others), By Application (Corrugated Board Coating, Flexible Packaging, Paper & Paperboard Coating, Hot-Melt Adhesives, Food & Beverage, Others), By End-Use Industry (Food & Beverage, Personal Care & Cosmetics, Industrial, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

China Petrochemical Corporation (Sinopec), ExxonMobil Corporation, Sasol Limited, Royal Dutch Shell plc, Nippon Seiro Co., Ltd., BP p.l.c., The International Group, Inc., SABIC, Mitsui Chemicals, Inc., Petrobras, Honeywell International Inc., BASF SE, Dow Inc., Braskem S.A., Numaligarh Refinery Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Packaging Wax Market Segmentation

By Wax Type

- Paraffin

- Microcrystalline

- Polyethylene

- Natural

- Others

By Application

- Corrugated Board Coating

- Flexible Packaging

- Paper & Paperboard Coating

- Hot-Melt Adhesives

- Food & Beverage

- Others

By End-Use Industry

- Food & Beverage

- Personal Care & Cosmetics

- Industrial

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Packaging Wax Market

- China Petrochemical Corporation (Sinopec)

- ExxonMobil Corporation

- Sasol Limited

- Royal Dutch Shell plc

- Nippon Seiro Co., Ltd.

- BP p.l.c.

- The International Group, Inc.

- SABIC

- Mitsui Chemicals, Inc.

- Petrobras

- Honeywell International Inc.

- BASF SE

- Dow Inc.

- Braskem S.A.

- Numaligarh Refinery Limited

* List Not Exhaustive

Methodology

USDAnalytics employs a robust and integrated research methodology to provide precise insights into the global Packaging Wax Market. Our approach combines primary research, including consultations with key stakeholders such as wax manufacturers, packaging converters, regulatory authorities, and end-use industry leaders, with secondary research from corporate reports, trade publications, government documents, and industry databases. We analyze market trends, technological innovations, and sustainability initiatives across wax types, applications, and end-use industries to forecast growth opportunities accurately. Regional analysis spans major markets including the United States, Germany, China, India, Japan, and Brazil, considering regulatory frameworks, e-commerce expansion, bio-based wax adoption, and automation in packaging processes. Quantitative modeling, coupled with qualitative insights, allows USDAnalytics to evaluate market dynamics such as paraffin wax phase-out, hybrid and bio-wax innovations, functional barrier coatings, and performance-driven industrial applications, delivering actionable intelligence for decision-makers focused on sustainability, efficiency, and competitive positioning.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.