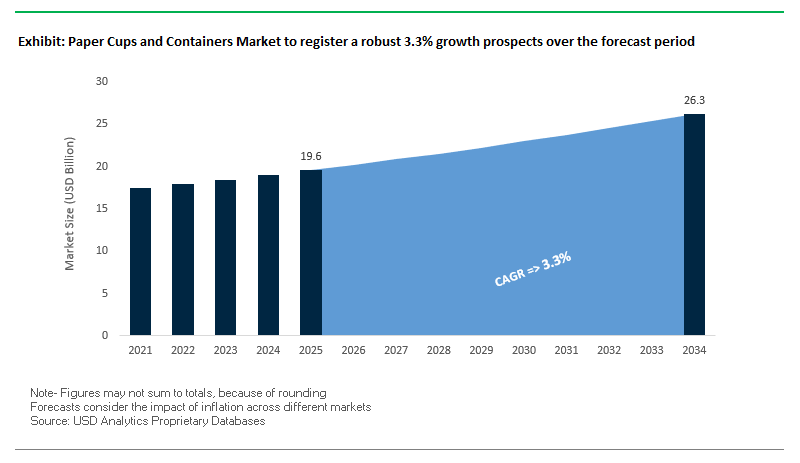

Paper Cups and Containers Market to Grow from $19.6 Billion in 2025 to $26.3 Billion by 2034 Driven by On-the-Go Consumption and Sustainability Demands

The Global Paper Cups and Containers Market is projected to reach $26.3 billion by 2034, up from $19.6 billion in 2025, at a CAGR of 3.3%, driven by the surging demand from quick-service restaurants (QSRs), specialty coffee chains, and takeaway food services. These fiber-based, single-use products are central to hygiene, convenience, and brand differentiation, forming a core part of the modern foodservice and on-the-go lifestyle ecosystem.

Key Insights for Industry Professionals:

- QSR and Specialty Coffee Expansion Fuels Demand: The proliferation of global food chains and increasing on-the-go consumption trends are boosting demand for high-quality, durable, and brand-enhancing paper cups and containers.

- Sustainability Shaping Material Innovation: Industry is transitioning to plant-based linings and reduced polymer content, driven by government regulations and consumer preference for eco-friendly solutions.

- Enhanced Functional Performance Is Critical: Containers are engineered to provide heat, moisture, and grease resistance, ensuring product integrity and positive consumer experience.

- Optimized Designs for Recycling and Composting: Companies are adopting easily separable coatings to improve fiber recovery and recycling efficiency.

- Strategic Role in Circular Economy Initiatives: The sector is contributing to plastic reduction targets and enhancing eco-conscious supply chain operations globally.

Strategic Developments Highlighting Sustainability and Innovation in Paper Cups and Containers

The Global Paper Cups and Containers Industry has seen a surge of strategic initiatives and product innovations, signaling a strong emphasis on sustainability, functional performance, and market consolidation. In August 2025, Graphic Packaging International introduced its PaperSeal® Pressed MAP Tray, expanding its fiber-based alternatives to plastic trays, and achieved child-resistant certification for CleanClose™ detergent pod packaging, demonstrating innovation in safety-focused paperboard solutions.

In the same month, International Paper committed $250 million to convert a Riverdale, Alabama machine for containerboard production, increasing its capacity for a key raw material in paper containers. Mondi plc launched its FunctionalBarrier Paper Ultimate, a high-performance food packaging solution with superior moisture and grease protection, reflecting the industry's move toward functionalized, sustainable coatings.

Other key milestones include July 2025, when the Recycled Materials Association (ReMA) added paper cups to its recycled materials classifications, marking a recycling milestone. June 2025 saw Mondi Group launch re/cycle PaperPlus Bag Advanced, targeting humidity-sensitive products, and in February 2025, Huhtamaki introduced recyclable single-coated paper cups with less than 10% plastic for European markets. Strategic consolidation includes April 2025, when International Paper completed its $9.9 billion acquisition of DS Smith, strengthening its European footprint in sustainable packaging.

Trends and Opportunities Shaping the Paper Cups and Containers Market

Accelerated Regulatory Phase-Out of Plastic-Lined Cups Mandating New Barriers

The global paper cups and containers market is being directly reshaped by regulatory mandates that target plastic-lined beverage cups. In Europe, the Single-Use Plastics Directive (SUPD) has classified plastic-lined paper cups as “plastic products,” making them subject to strict reduction measures, fees, and extended producer responsibility obligations. This regulation has forced packaging converters and brands to develop new paper cups with non-plastic barrier coatings to avoid penalties and remain compliant in one of the world’s largest consumer markets. In the United States, a growing number of cities and states are following a similar trajectory, with Seattle pioneering comprehensive food packaging rules that require recyclable or commercially compostable packaging for foodservice operators. Quick-service restaurants and cafes across the region are now switching from conventional polyethylene (PE)-lined cups to certified alternatives. The pressure is compounded by the incompatibility of traditional plastic-lined cups with curbside recycling infrastructure, as PE liners are nearly impossible to separate from paper fibers in standard pulping systems. This has made plastic-lined cups a contaminant stream in many municipalities, further intensifying the urgency for next-generation, recyclable, and compostable barrier solutions.

Strategic Expansion of Reusable Cup Infrastructure and Systems

Beyond material innovation, a structural trend is emerging in the form of reusable cup systems. Quick-service restaurant (QSR) leaders are driving this shift through pilot projects and nationwide rollouts. Starbucks, for instance, announced in January 2024 that customers in the U.S. and Canada can now bring their own cups for all transactions, including drive-thru and mobile orders—a first-of-its-kind industry move to normalize reusables at scale. Meanwhile, deposit return schemes (DRS) are gaining traction as system-wide solutions. Germany’s “Refill It!” program, where consumers borrow reusable cups for a small deposit refundable upon return at any participating cafe, is reducing the staggering figure of over 320,000 disposable cups discarded every hour in the country. These models highlight a broader trend: the paper cups and containers industry is not only innovating materials but also transforming business models and consumer behavior. Reusables and deposit-based systems are emerging as credible, scalable pathways to reduce waste and meet corporate sustainability pledges.

Development and Scaling of Polylactic Acid (PLA) and Other Bio-Based Liners

The replacement of plastic liners with bio-based alternatives represents one of the most promising opportunities for the paper cups and containers market. PLA (polylactic acid), derived from renewable feedstocks, is gaining traction as a compostable liner option. While PLA has historically faced challenges with heat resistance, recent academic research shows that increasing PLA concentration enhances water resistance, tensile strength, and heat-sealing capacity, making it suitable for both hot and cold beverages. Industrial composting standards such as EN13432 are accelerating PLA’s commercialization, especially in regions where composting infrastructure is expanding. Innovations in raw material sourcing are further strengthening PLA’s sustainability credentials. Companies are developing PLA from agricultural by-products like rice husks and other residues, reducing dependence on cornstarch and improving cost-efficiency. These developments position PLA as a scalable, plant-based alternative that can help brands comply with regulatory bans on plastics while enhancing their eco-friendly packaging portfolios.

Integration of Digital Watermarking for Advanced Sorting and Recycling

Digital watermarking is emerging as a transformative opportunity for solving the recycling challenges associated with paper cups. The HolyGrail 2.0 initiative—a consortium of over 130 companies—demonstrated in 2024 industrial trials in Germany that digital watermarking enables high-speed sorting equipment to achieve over 90% detection accuracy. For paper cups, this technology can be applied to distinguish between different liner types such as PE, PLA, or other bio-based coatings. This granular sorting capability ensures that cups are routed to the correct end-of-life pathway: recyclable cups to paper mills and compostable cups to industrial composting facilities. By reducing cross-contamination and enhancing the purity of recycled fiber, digital watermarking creates a genuine pathway toward a circular economy for paper cups and containers. Its ability to combine material recovery with compliance tracking positions it as a disruptive innovation with long-term potential to align with both regulatory mandates and sustainability commitments.

Leading Companies Are Shaping Sustainability and Innovation in Paper Cups and Containers

The competitive landscape is dominated by companies leveraging materials science, manufacturing scale, and sustainable design to provide high-performance, fiber-based packaging solutions. These leaders differentiate through innovative coatings, plant-based materials, and strategic global expansions, driving functional, eco-friendly, and consumer-centric solutions.

Huhtamaki Oyj Drives Sustainability with Recyclable and Plant-Based Paper Cups

Huhtamaki is a global leader in sustainable food packaging, with expertise in paperboard converting and material innovation. In February 2025, it launched recyclable single-coated paper cups for dairy, emphasizing lower-polymer solutions and food safety compliance, and in January 2024, introduced AI-driven cup forming machines for enhanced production efficiency. Its portfolio includes hot and cold beverage cups, lids, and Future Smart cups made from 100% renewable materials, positioning the company as a pioneer in sustainable foodservice packaging.

Graphic Packaging International Pioneers Fiber-Based Packaging Solutions for Foodservice

Graphic Packaging excels in fiber-based consumer packaging with a focus on functionality and aesthetics. In August 2025, it released its 2024 Impact Report, highlighting replacement of 1 billion plastic packages with paperboard alternatives, and launched Cold&Go insulated paper cups for frozen desserts. Its ecotainer line features plant-based, compostable materials, reinforcing Vision 2030 goals for circularity and sustainability.

Smurfit Westrock plc Emerges as a Global Leader with Unmatched Scale and Integrated Operations

Smurfit Westrock, formed from the Smurfit Kappa and WestRock merger, operates 62 mills and 500+ converting operations across 40 countries. In August 2025, the company reported Q2 results while implementing capacity optimizations in the U.S. and Germany. Its portfolio includes corrugated containers, folding cartons, and specialty packaging, designed for foodservice and retail applications, with a strategic emphasis on circular economy principles and renewable materials.

International Paper Company Strengthens Sustainable Packaging Footprint through Strategic Acquisitions

International Paper is a global leader in fiber-based packaging and pulp, emphasizing vertical integration and containerboard expertise. In August 2025, it divested its Global Cellulose Fibers business and completed the $9.9 billion acquisition of DS Smith in April 2025, expanding European operations. Its offerings include paperboard stock and finished paper-based packaging, supporting foodservice, industrial, and consumer applications with a focus on operational efficiency and customer value.

Stora Enso Oyj Invests in Renewable Production and Circular Economy Leadership

Stora Enso provides renewable packaging, biomaterials, and wooden construction solutions, leveraging an integrated forest-to-product model. In August 2025, it inaugurated Europe’s most modern consumer board production line in Finland and achieved a 53% reduction in Scope 1 and 2 emissions by 2024, surpassing 2030 targets. Its portfolio includes folding boxboard and liquid packaging board used in paper cups, cartons, and food containers, with the Performa Nova board enhancing consumer packaging sustainability and performance.

Paper Cups and Containers Market Share Insights, 2025-2034

Hot Cups Dominate Market Share by Product Type in the Paper Cups and Containers Industry

Hot cups account for 40% of the paper cups and containers market, reflecting their entrenched role in global coffee consumption and foodservice operations. Their dominance stems from the ubiquity of single-wall and double-wall PE-lined cups, which provide insulation and barrier protection for hot beverages. However, this segment is undergoing rapid transformation due to regulatory bans on non-recyclable plastic linings, pushing the industry toward compostable PLA coatings, aqueous dispersions, and mono-material fiber-based designs. Cold cups are growing in share, supported by the surging popularity of iced beverages, bubble tea, and specialty drinks, often requiring condensation-resistant or clear PLA-based alternatives. Food containers, including bowls, trays, and clamshells, represent the fastest-growing category, benefiting from the global phaseout of polystyrene and plastic containers in quick-service restaurants (QSRs) and delivery platforms. Paperboard trays and leak-proof barriers are becoming the preferred solutions for sustainable food packaging. Bottles, tubes, and other specialized formats hold smaller shares but are strategically important, particularly where branding, vending system compatibility, or grease resistance are decisive. The product segmentation illustrates how hot cups maintain volume leadership, while food containers and cold cups are the innovation hotspots driving the next wave of sustainable paper packaging adoption.

Quick-Service Restaurants (QSRs) Lead Market Share by Application in the Paper Cups and Containers Industry

Quick-service restaurants dominate the market with 35% share, reflecting their unparalleled consumption of hot cups, cold cups, and takeaway food containers. QSRs operate at the highest volume scale, demanding cost-efficient, durable, and regulatory-compliant packaging that can accommodate diverse menus while aligning with sustainability commitments. Their role as early adopters of compostable linings, fiber-based lids, and recyclable designs makes them the single largest driver of industry innovation. Coffee shops and cafes form the second pillar of demand, acting as the brand showcase for premium cup designs, high-quality printability, and eco-friendly solutions. The institutional sector—including offices, schools, and hospitals—favors bulk purchasing of functional, cost-effective packaging, often shaped by municipal sustainability mandates. Catering and foodservice operators demand robust containers with secure lids for transport and delivery, while the retail and consumer goods segment is transitioning to paper-based yogurt cups, oatmeal packs, and frozen food tubs as part of the global plastic replacement drive. Vending machines, though niche, sustain steady demand through highly standardized formats. Collectively, the application segmentation underscores how QSRs and coffee chains dictate the scale and direction of the market, while retail and food delivery are accelerating the shift toward fiber-based, recyclable, and compostable paper packaging solutions.

United States Paper Cups and Containers Market Shaped by EPA, FDA Regulations and Smart Packaging Innovation

The United States paper cups and containers market is evolving rapidly due to strong regulatory action and corporate sustainability initiatives. The U.S. Environmental Protection Agency (EPA) has designated paper products under its Comprehensive Procurement Guidelines (CPG) program, prioritizing the use of recycled content in federal procurement. This is driving large-scale adoption of paper cups made with post-consumer recycled (PCR) fiber. Furthermore, the U.S. Food and Drug Administration (FDA) ban on per- and polyfluoroalkyl substances (PFAS) in food contact materials has accelerated the industry’s shift to fluorine-free and biodegradable barrier coatings, setting new benchmarks for food safety.

Market leaders are investing strategically to expand capabilities. For example, WinCup’s acquisition of ConverPack Inc. in July 2025 has strengthened its product offerings across both traditional and sustainable cup formats. Similarly, Starbucks introduced redesigned cold cups in April 2024 that use less plastic and streamline operations for baristas, demonstrating how major foodservice chains are pushing innovation in packaging. A defining trend in the U.S. is the adoption of “smart cups” with QR codes and NFC chips, enabling interactive marketing and consumer engagement. Combined with the growth of the on-the-go and e-commerce-driven food service sector, the U.S. is positioning itself as a global leader in digitally enabled, eco-friendly paper packaging solutions.

China Paper Cups and Containers Market Expands with E-Commerce Growth and Fast-Food Demand

The China paper cups and containers market is experiencing robust growth, underpinned by the government’s National Clean Air Programme and stringent plastic waste reduction policies. These initiatives are positioning paper-based packaging as the primary sustainable alternative. Explosive growth in e-commerce and food delivery services is fueling high-volume demand for corrugated paper containers, folding cartons, and takeaway cups, especially in urban centers.

Domestic manufacturers are scaling production capacity and investing in new coating technologies to improve cost efficiency, grease resistance, and performance. At the same time, multinational fast-food chains such as McDonald’s, which plans 1,000 new outlets in 2025, are fueling significant demand for disposable cups and containers. With both domestic innovation and foreign investment, China remains the largest global hub for high-volume, cost-efficient, and sustainable paper packaging solutions, especially in the food and beverage takeaway sector.

India Paper Cups and Containers Market Driven by Plastic Ban and Food Delivery Growth

The India paper cups and containers market is being transformed by strong government intervention and consumer demand for sustainability. The nationwide ban on single-use plastics has accelerated the adoption of compostable and biodegradable paper cups, creating opportunities for domestic producers. The food delivery boom, led by platforms like Zomato and Swiggy, has sharply increased the need for durable, spill-proof, and eco-friendly paper containers.

The Make in India initiative is further encouraging domestic manufacturing, with policy support in the form of MSME loans, subsidies, and EPR mandates. Major producers such as Andhra Paper and Satia Industries have announced substantial investments to expand production capacity and improve packaging-grade paper quality. India’s Ministry of Environment, Forest and Climate Change (MoEFCC) is pushing industry-wide adoption of biodegradable and recyclable materials, aligning manufacturers with national sustainability goals. Coupled with the rapid rise of organized retail and affordable housing-driven urbanization, India is positioned to become one of the fastest-growing markets for eco-friendly paper cups and containers.

Germany Paper Cups and Containers Market Driven by EU PPWR and Aqueous Coating Innovation

The Germany paper cups and containers market is strongly influenced by the European Union’s Packaging and Packaging Waste Regulation (PPWR), which mandates recyclability and reuse by 2030. German manufacturers are actively developing fully recyclable and compostable cup solutions, focusing on aqueous (water-based) coatings that replace traditional polyethylene linings and allow recycling in conventional paper mills.

The Blue Angel ecolabel sets additional sustainability standards, making certified eco-friendly paper cups a strong driver in the market. With Germany’s thriving café culture and high per capita coffee consumption, demand for insulated and premium paper cups continues to grow. Local companies are investing heavily in R&D to align with circular economy principles, ensuring paper-based packaging meets both consumer expectations and stringent EU sustainability directives.

United Kingdom Paper Cups and Containers Market Boosted by Plastic Packaging Tax and Recycling Initiatives

The United Kingdom paper cups and containers market is benefiting from regulatory and industry-driven efforts to phase out plastics. The UK Plastic Packaging Tax, which applies to packaging with less than 30% recycled plastic, has accelerated the shift toward paper and paperboard alternatives. The country’s strong recycling infrastructure supports this transition, with initiatives like the Paper Cup Recovery & Recycling Group (PCRRG) working to establish scalable recycling solutions across industries.

The UK market is also characterized by innovation in packaging formats, including glue-free interlocking paperboard designs that enhance recyclability. Coffee chains are actively piloting reusable and recyclable cup schemes to meet consumer expectations and regulatory mandates. Combined with the UK’s on-the-go lifestyle and high consumption of premium coffee and soft drinks, the market for rigid paper containers and recyclable paper cups continues to expand, particularly in the retail and foodservice segments.

Japan Paper Cups and Containers Market Strengthened by Convenience Culture and Advanced Coating R&D

The Japan paper cups and containers market is growing under strong government support for plastic waste reduction policies, which are accelerating the adoption of biodegradable and compostable paper packaging. Japan’s foodservice industry and vending machine culture contribute significantly to demand for paper cups for hot and cold beverages, while the emphasis on hygiene and convenience strengthens their role in the consumer market.

Leading Japanese manufacturers such as Oji Holdings and Nippon Paper Industries are investing heavily in research and development of new fiber-based coatings that balance performance with sustainability. Innovations in functional coatings for grease and moisture resistance are becoming increasingly important as Japan’s food and beverage sector grows. With its focus on design, precision, and consumer safety, Japan is emerging as a global hub for high-quality, eco-friendly paper cups and containers that also meet aesthetic and performance standards.

Paper Cups and Containers Market Report Scope

Paper Cups and Containers Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$19.6 Billion

|

|

Market Size (2034)

|

$26.3 Billion

|

|

Market Growth Rate

|

3.3%

|

|

Segments

|

By Product Type (Hot Cups, Cold Cups, Food Containers, Other Containers), By Material (Virgin Paperboard, Recycled Paperboard, Specialty Paperboard), By Lining/Coating (PE Coated, PLA Coated, Aqueous Coated, Wax Coated, Other Biopolymer Coatings), By Application (QSRs, Coffee Shops & Cafes, Institutional, Food Service & Catering, Vending Machines, Retail & Consumer Goods), By Wall Type (Single Wall, Double Wall, Ripple Wall)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Huhtamäki Oyj, International Paper, Dart Container Corporation, Smurfit Kappa Group, WestRock Company, Graphic Packaging Holding Company, Sonoco Products Company, Pactiv Evergreen Inc., Nippon Paper Industries Co., Ltd., Genpak LLC, Benders Paper Cups, Go-Pak UK Ltd., WinCup, Inc., F Bender Ltd., Greif, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Paper Cups and Containers Market Segmentation

By Product Type

- Hot Cups

- Cold Cups

- Food Containers

- Other Containers

By Material

- Virgin Paperboard

- Recycled Paperboard

- Specialty Paperboard

By Lining/Coating

- PE Coated

- PLA Coated

- Aqueous Coated

- Wax Coated

- Other Biopolymer Coatings

By Application

- QSRs

- Coffee Shops & Cafes

- Institutional

- Food Service & Catering

- Vending Machines

- Retail & Consumer Goods

By Wall Type

- Single Wall

- Double Wall

- Ripple Wall

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Paper Cups and Containers Market

- Huhtamäki Oyj

- International Paper

- Dart Container Corporation

- Smurfit Kappa Group

- WestRock Company

- Graphic Packaging Holding Company

- Sonoco Products Company

- Pactiv Evergreen Inc.

- Nippon Paper Industries Co., Ltd.

- Genpak LLC

- Benders Paper Cups

- Go-Pak UK Ltd.

- WinCup, Inc.

- F Bender Ltd.

- Greif, Inc.

* List Not Exhaustive

Methodology

The research methodology for the Paper Cups and Containers Market employs a combination of primary and secondary approaches to ensure accurate, actionable insights for industry professionals. Primary research involved in-depth interviews with executives, packaging engineers, sustainability experts, and supply chain stakeholders across major regions to capture emerging trends, regulatory impact, and technological innovations such as PLA liners, aqueous coatings, and reusable cup systems. Secondary research encompassed analysis of company annual reports, regulatory frameworks, patents, sustainability disclosures, and verified industry publications. Data triangulation was applied to validate market sizing, growth forecasts, and CAGR projections, integrating macroeconomic indicators, on-the-go consumption trends, sustainability mandates, and advancements in digital watermarking and circular economy solutions. Forecasts were developed using both top-down and bottom-up approaches, while regional insights were contextualized against policies like the EU PPWR, U.S. FDA PFAS bans, India’s single-use plastic regulations, and Japan’s Green Innovation initiatives. This robust, multi-layered methodology by USDAnalytics ensures that the report delivers reliable, fact-based, and strategic insights aligned with the evolving global paper cups and containers industry.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.