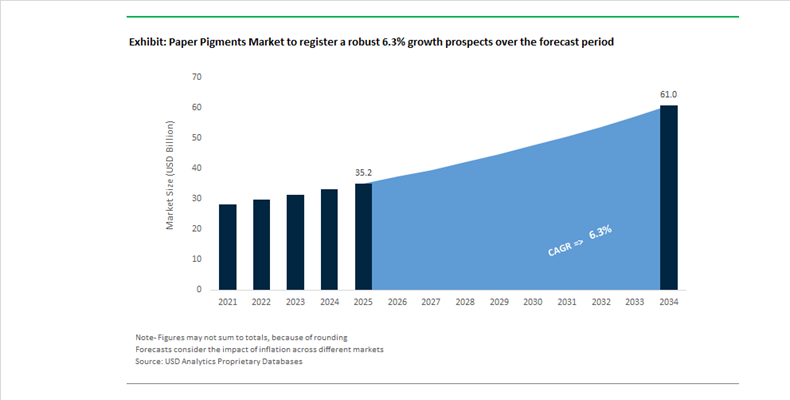

Paper Pigments Market Valued at $35.2 Billion in 2025 with 6.3% CAGR Driven by Integrated Satellite Plants and Sustainable Mineral Inputs

The Paper Pigments Market is valued at $35.2 billion in 2025 and is projected to reach $61 billion by 2034, expanding at a CAGR of 6.3%. Market acceleration is closely tied to structural growth in coated paperboard, high-brightness printing substrates, and premium packaging applications. Paper pigments—primarily ground calcium carbonate (GCC), precipitated calcium carbonate (PCC), kaolin clay, titanium dioxide, and specialty effect pigments—play a central role in brightness enhancement, opacity, smoothness, ink receptivity, and surface gloss. As plastic packaging substitution intensifies globally, coated fiber-based materials are witnessing renewed capital inflows, directly increasing pigment consumption intensity per ton of paper. The market is simultaneously undergoing structural transformation driven by mill-integrated satellite plants, mineral portfolio rationalization, and stricter environmental and occupational regulations.

A defining competitive development is the rapid expansion of satellite PCC plants by Minerals Technologies Inc. (MTI). In 2025, MTI successfully started up three new satellite plants in Asia—two in China and one in India—while doubling capacity at an existing Indian facility. An additional Chinese satellite plant is scheduled for commissioning in early 2026. These integrated facilities are built directly within customer paper mills, reducing logistics costs, ensuring consistent slurry quality, and optimizing particle morphology for high-speed coating lines. This localized, “inside-the-fence” model is becoming the industry benchmark for calcium carbonate supply in Asia’s expanding packaging ecosystem.

Portfolio realignment among mineral majors has reshaped competitive dynamics. In July 2024, Imerys completed the disposal of its paper-focused assets, exiting the kaolin and calcium carbonate segments to refocus on battery-grade graphite and carbon materials. The divestment has opened market share opportunities for regional carbonate suppliers in Europe and North America. Meanwhile, in 2024–2025, Kemira finalized the sale of its colorants business to ChromaScape, streamlining its portfolio toward strength chemicals and wet-end solutions. At the same time, BASF expanded high-performance dispersion production at its Mangalore site in February 2026, launching Basonal® PLUS grades designed to work synergistically with mineral pigments in low-Product Carbon Footprint (PCF) packaging coatings.

Sustainability metrics and regulatory oversight are becoming decisive procurement criteria. In February 2025, Imerys achieved a CDP “A List” rating for climate leadership, reinforcing the importance of verified low-carbon mineral sourcing in paper pigment contracts. In January 2026, the United States Environmental Protection Agency advanced new risk management rules for selected pigment particulates, including Pigment Violet 29, formally recognizing batch-processing risk mitigation protocols. These updates will influence worker safety investments and emissions monitoring across pigment manufacturing facilities. Upstream pulp expansion is also shaping pigment demand: in July 2024, Suzano commissioned its Cerrado Project, adding 2.55 million tons of annual eucalyptus pulp capacity, catalyzing downstream investments in coating and PCC infrastructure. Collectively, the market is transitioning toward integrated supply models, ESG-verified mineral inputs, advanced surface-effect pigments for luxury packaging, and tighter regulatory alignment across North America and Asia-Pacific.

Structural Trends and High-Value Opportunities Reshaping the Paper Pigments Market

Titanium Dioxide Substitution Accelerates Through Engineered Calcium Carbonate and Kaolin

The global paper pigments market is undergoing a decisive structural shift as paper producers actively reduce dependence on titanium dioxide. While TiO2 remains a benchmark pigment for brightness and opacity, its cost volatility, regulatory uncertainty, and trade-related risks have made it increasingly unattractive for large-scale paper applications. Even after the August 2025 ruling by the European Court of Justice that annulled the carcinogenic classification of TiO2, the industry’s strategic pivot toward extender pigments has become permanent.

Paper mills across Europe and Asia are now adopting engineered ground calcium carbonate, precipitated calcium carbonate, and calcined kaolin as primary opacity and brightness enhancers. Performance benchmarks published by Imerys in 2025 confirm that modern mineral pigments can replace up to 30% of titanium dioxide in standard paper coatings and as much as 100% in high pigment volume concentration matt grades without sacrificing optical performance. These results are achieved through advanced particle engineering that maximizes light scattering efficiency while reducing pigment overcrowding.

Cost pressures are further reinforcing this transition. The European Union’s anti-dumping duties on Chinese titanium dioxide imports, effective January 2025 and ranging from $0.28 to $0.83 per kilogram, have materially increased input costs for European paper producers. In contrast, domestically sourced calcium carbonate and kaolin offer predictable pricing and supply security. As a result, extender pigments are no longer viewed as secondary fillers but as core cost-optimization tools within paper coating formulations.

High-Filler-Content Paper Gains Momentum as Fiber Reduction Becomes a Climate Strategy

Sustainability targets and rising fiber costs are accelerating the adoption of high-filler-content paper across packaging and graphic paper segments. Mineral pigments are increasingly used not only for optical performance but also as a strategic lever to reduce wood fiber consumption, lower energy use, and cut carbon emissions across the paper manufacturing value chain.

Major producers in Europe are leading this transition. Stora Enso has expanded its lightweight paperboard portfolio by increasing filler ratios while maintaining mechanical strength, enabling lower basis weights without compromising performance. Similar strategies are being pursued by UPM, where high-filler technologies are aligned with long-term climate roadmaps targeting substantial emissions reductions by 2030.

From an operational standpoint, mineral fillers deliver a clear decarbonization return on investment. Minerals retain significantly less water than wood fibers, reducing drying energy requirements during paper production. Supply chain optimization initiatives reported by Imerys during 2023–2024 demonstrated a 24% absolute reduction in greenhouse gas emissions, reinforcing the economic case for filler-rich paper grades. Industry consolidation is also supporting scale efficiencies. In December 2025, UPM and Sappi announced plans to explore a joint venture in graphic paper, with high-performance mineral fillers positioned as a central pillar for cost control in a structurally declining market.

Functional and Conductive Pigments Enable Smart Packaging and Interactive Paper

One of the most attractive growth opportunities in the paper pigments market lies in the emergence of functional pigments that transform paper from a passive substrate into an active, value-adding medium. As e-commerce, logistics, and brand protection requirements intensify, demand is rising for pigments that deliver conductivity, anti-static behavior, and digital compatibility.

A major breakthrough occurred in December 2025 when UPM launched Circular Renewable Black, the world’s first carbon-negative, bio-based black pigment derived from lignin. Unlike conventional carbon black, which disrupts near-infrared sorting in recycling plants, this pigment is fully detectable, enabling the circular use of premium black paper packaging. This innovation addresses a long-standing sustainability bottleneck in colored paper recycling.

At the same time, conductive pigments are increasingly being integrated into paperboard to support NFC-enabled packaging, anti-static protection, and invisible tracking features. These applications allow brands to embed intelligence directly into fiber-based packaging without relying on plastic components. Strategic industry consolidation is accelerating this shift. In March 2025, Sudarshan Chemical Industries completed its acquisition of Heubach Group, creating a global platform focused on specialty and functional pigment applications across paper, coatings, and electronics-related markets.

Sustainable Opacifiers for Paints and Polymer Composites Create Cross-Industry Growth

Advances in paper pigment technology are unlocking significant cross-industry opportunities, particularly as coatings and plastics manufacturers seek lower-carbon alternatives to titanium dioxide. Calcined kaolin and high-brightness calcium carbonate developed for paper applications are now being actively marketed as sustainable extender pigments for paints and polymer composites.

Technical evaluations conducted in 2025 show that calcined aluminum silicate can replace between 5% and 20% of titanium dioxide in waterborne paints without negatively affecting gloss, viscosity, or scrub resistance. This opens a sizeable adjacent opportunity, given the scale of the global TiO2 market. Polymer processors are also evaluating paper-grade pigments in construction applications such as window profiles and siding, where dry hiding power and UV stability are critical performance parameters.

Regional dynamics are strengthening this opportunity. In late 2025, India’s paint industry began shifting toward locally sourced kaolin and calcium carbonate blends in response to margin pressure from imported raw materials. These mineral composites offer a cost-effective, lower-carbon alternative while maintaining acceptable visual performance. As sustainability, affordability, and supply resilience converge, paper pigments are increasingly positioned as multi-industry materials with relevance far beyond traditional paper manufacturing.

Paper Pigments Market Share and Segmentation Insights

Inorganic Pigments Dominate Paper Pigment Consumption with Calcium Carbonate Leading High-Volume Paper Production

Inorganic pigments accounted for 72.80% of the Paper Pigments Market by pigment type in 2025, reflecting their extensive use in papermaking processes that require high opacity, brightness, and printability at competitive costs. Key inorganic pigments including calcium carbonate, kaolin clay, talc, and titanium dioxide serve as essential components in paper coating and filler formulations used in packaging paper, printing grades, and specialty papers. Calcium carbonate remains the most widely used pigment due to its brightness performance and compatibility with alkaline papermaking systems. In 2025, the industry is witnessing increased adoption of ground calcium carbonate production at paper mills, enabling cost reduction, improved pigment consistency, and efficient integration into high-volume papermaking operations.

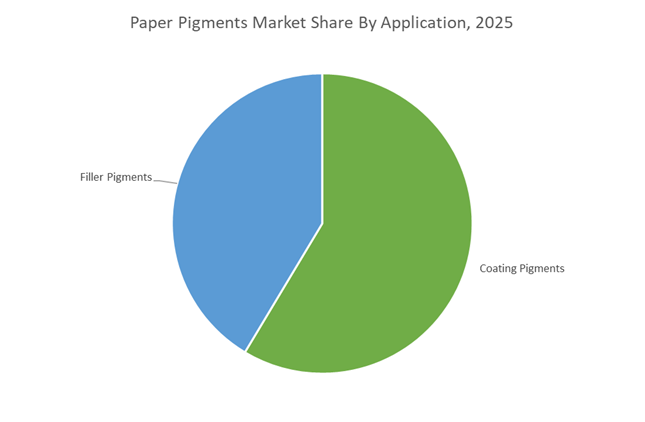

Coating Pigments Lead Paper Pigment Applications in Premium Print and Packaging Grades

Coating pigments represented 58.60% of the Paper Pigments Market by application in 2025, making them the dominant pigment category used in coated paper manufacturing. Paper coating formulations utilize high pigment loadings to enhance surface smoothness, brightness, opacity, and print quality required in packaging boards, high-end printing papers, and specialty paper products. The demand for premium packaging and graphic printing grades continues to support high coating pigment consumption. In 2025, papermakers are focusing on lightweight coating optimization, where advanced pigment blends with engineered particle size distributions enable thinner coating layers while maintaining coverage, opacity, and print performance in lightweight paper grades.

Paper Pigments Market Competitive Landscape

The Paper Pigments Market is evolving toward low-carbon mineral slurries, circular-economy pigments, and functional barrier coatings. Industry leaders are expanding regional capacity, integrating satellite manufacturing, and developing GCC and PCC-based solutions that enhance recyclability, reduce fiber usage, and enable plastic-free packaging applications.

MTI scales satellite PCC plants to dominate packaging-grade pigment supply in Asia

Minerals Technologies Inc. (MTI) is leading the paper pigments market through its satellite plant model, enabling on-site PCC production at paper mills for seamless supply and cost optimization. The company expanded aggressively in Asia with three new satellite plants in 2025 and an additional unit planned for 2026, alongside capacity doubling in India. Approximately 50% of these expansions target packaging applications, where demand for high-performance pigments is surging. MTI’s proprietary crystal engineering technology enhances brightness and opacity while reducing wood fiber consumption in uncoated paper. With 56 satellite plants globally and $2.1 billion in sales, MTI maintains strong operational scale. This integration of localized production and advanced mineral engineering reinforces its market leadership.

Imerys optimizes engineered kaolin portfolio for recyclable barrier paper packaging

Imerys S.A. is repositioning its paper pigments portfolio toward high-value engineered minerals aligned with green economy applications. Through Project Horizon, the company is targeting €50–€60 million in annual savings by 2027, improving efficiency and competitiveness. Its engineered kaolin and calcium carbonate pigments enhance barrier properties in paper packaging, enabling substitution of plastic laminates. Despite currency challenges, Imerys delivered €546 million EBITDA in 2025, supported by disciplined pricing and operational optimization. Strategic investment in the EMILI lithium project strengthens capital flexibility and cross-sector mineral expertise. This focus on engineered pigments and sustainability positions Imerys strongly in recyclable packaging solutions.

Omya advances calcium carbonate pigments for high-speed, recyclable food packaging

Omya AG is strengthening its leadership in calcium carbonate pigments by focusing on high-performance coatings and sustainable packaging applications. Its pigments are optimized for high-solids formulations, enabling faster paper machine speeds and reduced energy consumption during drying. The company’s water-based barrier coatings provide oil and grease resistance for food packaging while maintaining full recyclability and compostability. Through its R&D collaboration with IFG, Omya is advancing low-carbon mineral solutions for fiber-based materials. Its ability to replace wood fiber with calcium carbonate improves opacity, brightness, and fiber yield in paperboard products. This combination of performance and sustainability enhances Omya’s competitive positioning.

Kemira integrates pigment chemistry and renewable coatings for circular packaging systems

Kemira Oyj is leveraging its expertise in water and paper chemistry to optimize pigment performance across the papermaking value chain. Its investment in expanding strength chemical capacity in Thailand supports growing demand for high-quality packaging board driven by e-commerce. Kemira’s Renewable Coatings strategy focuses on developing sustainable barrier systems that work synergistically with pigments to enable plastic-free packaging. With an EBITDA margin of 19.1% in 2025, the company demonstrates strong financial resilience. Its portfolio of dispersants, biocides, and defoamers ensures efficient handling of pigment slurries such as kaolin and TiO2. This integrated chemistry approach strengthens Kemira’s role in circular paper production.

Sudarshan expands global pigment footprint through Heubach acquisition and clean colorant focus

Sudarshan Chemical Industries Limited (SCIL) has emerged as a global pigment leader following its acquisition of the Heubach Group, integrating 19 manufacturing sites worldwide. This expansion enhances its ability to supply high-performance pigment dispersions and powders to the paper and printing industries across Europe and North America. The company is focusing on non-toxic, chemical-free pigments to meet demand for safer stationery and child-friendly paper products. Post-acquisition, SCIL is optimizing its global supply chain to ensure stable and localized pigment availability. Leveraging Heubach’s advanced technical capabilities, it is strengthening its position in specialty colorants. This strategic integration positions SCIL as a competitive force in high-purity paper pigments.

United States – Infrastructure-Led Scale-Up and Regulatory-Driven Reformulation

The U.S. paper pigments industry is undergoing a structurally important expansion phase, anchored in capacity investment and regulatory realignment toward safer, mineral-based chemistries. In May 2025, Solenis announced an additional USD 76 million investment at its Suffolk, Virginia site, raising the total project value to USD 269 million. The expansion includes a new production facility and dedicated rail spur, materially strengthening logistics efficiency and supporting higher-volume production of mineral-based polymers and pigment additives for the global containerboard and folding carton markets. This infrastructure scaling reflects sustained demand for functional paper pigments that enhance stiffness, opacity, and surface smoothness in lightweight packaging grades.

Regulation is accelerating formulation change. Effective January 2026, the U.S. market has largely completed its transition to fluorine-free barrier technologies, replacing intentionally added PFAS with mineral-blend coatings such as Contour SM for grease resistance in molded pulp and food service applications. Parallel to this, January 2025 updates to the Toxic Substances Control Act enabled faster EPA review for new pigments assessed under hazard-based models, favoring inorganic minerals with low bioaccumulation profiles. Strategic raw material security has also moved into focus. In December 2025, Tronox Holdings secured USD 600 million in financing support to integrate high-purity titanium dioxide production with rare earth extraction, reinforcing domestic pigment resilience. Innovation is extending into circularity, with Smart Planet Technologies commercializing a biopolymer EarthCoating in late 2025 that combines PLA with mineral pigments engineered for easier removal during paper recycling.

China – Pigment Asset Consolidation and Low-Carbon Mandates

China remains a pivotal force in global paper pigments, combining asset acquisition with policy-driven efficiency targets. In October 2025, LB Group signed an agreement to acquire Venator Materials’ Greatham site and associated TiO2 pigment assets in the UK. This transaction strengthens China’s control over high-performance sulfate-process titanium dioxide while supporting downstream paper and board applications requiring high brightness and opacity. Domestically, pigment performance is being reinforced through chemistry infrastructure. BASF inaugurated a high-performance dispersant production line in Nanjing in late 2025, using Controlled Free Radical Polymerization to stabilize pigment slurries for high-speed paper machines, particularly in packaging and decor paper grades.

Regulatory pressure is reshaping operating economics. In October 2025, China introduced stricter import purity standards for recycled “dry pulp,” rejecting shipments with impurity levels of 0.5% or higher. This has forced pigment suppliers to develop clean-wash additives that support recycled fiber brightness without contamination risks. At the same time, the Ministry of Industry and Information Technology enforced its 2025 Low-Carbon Chemical Roadmap, requiring pigment manufacturers to cut energy intensity by 15% by late 2026 or face curtailments in industrial clusters. Together, these measures are pushing the market toward fewer, more technologically advanced producers with strong process control capabilities.

Germany – Circular Mineral Innovation and Portfolio Rebalancing

Germany’s paper pigments industry is increasingly defined by circular economy alignment and decarbonized mineral production. At K 2025 in Düsseldorf, Omya launched Omya Performance Polymers Distribution, integrating mineral pigments with circular polymer additives to help packaging converters meet EU Green Deal targets. This integration reflects a shift away from standalone fillers toward multifunctional pigment systems that improve recyclability, barrier performance, and process efficiency in one formulation.

Energy transition commitments are materially influencing pigment cost structures. In October 2025, Imerys announced a 10-year Corporate Power Purchase Agreement securing 200 GWh of renewable electricity annually to decarbonize European mineral pigment processing. Portfolio restructuring is also underway. In December 2025, Mutares SE & Co. KGaA submitted an irrevocable offer to acquire Venator’s Ultramarine Blue Pigments business, consolidating specialty color pigments under infrastructure-focused ownership. Product innovation continues with the launch of Omyaloop FC in 2025, a food-contact approved, pre-consumer recycled calcium carbonate grade that cuts carbon emissions by up to two-thirds versus virgin mineral inputs.

India – Consolidation, Trade Protection, and Domestic Demand Pivot

India’s paper pigments industry is transitioning from export dependence toward domestic market reinforcement, underpinned by consolidation and tariff protection. In March 2025, Sudarshan Chemical Industries completed its USD 138 million acquisition of the Heubach Group, positioning India as a global supplier of high-end organic and inorganic pigments for decor paper and specialty printing applications. However, external trade pressures are reshaping demand flows. Following new U.S. tariffs in late 2025, Indian pigment exports are projected to contract by 5 to 7% in FY26, prompting producers to prioritize domestic consumption in tissue, hygiene, and packaging segments where demand remains structurally resilient.

Policy intervention is providing downside protection. In June 2025, the Central Board of Indirect Taxes and Customs imposed anti-dumping duties of up to USD 542 per tonne on imported decor paper, indirectly strengthening domestic demand for locally produced titanium dioxide and kaolin pigments. This trade shield is encouraging capacity utilization and investment in higher-purity mineral grades tailored to Indian paper mills.

Saudi Arabia – Operational Efficiency and Pigment Optimization

Saudi Arabia’s role in the paper pigments landscape is increasingly linked to mill-level efficiency and optimized mineral usage rather than large-scale pigment production. In late 2024, Saudi Paper Manufacturing Company received the Solenis Sustainability Award for implementing the PerForm SP 4715 KR retention aid. The system significantly improved mineral pigment retention, reduced resin consumption, and lowered overall carbon emissions at the mill level. This achievement highlights how operational chemistry optimization is becoming a competitive lever for paper producers in regions focused on efficiency, water conservation, and energy intensity reduction.

Comparative Snapshot – Paper Pigments Industry by Country

Paper Pigments Market County Level Snapshot

|

Country

|

Strategic Focus

|

Primary Driver

|

Structural Outcome

|

|

United States

|

Capacity expansion and PFAS-free reformulation

|

TSCA updates and infrastructure investment

|

Scaled, mineral-led pigment systems

|

|

China

|

Asset consolidation and energy intensity reduction

|

MIIT low-carbon mandates

|

Fewer, technologically advanced producers

|

|

Germany

|

Circular minerals and decarbonized processing

|

EU Green Deal and renewable energy

|

Premium recycled and low-carbon grades

|

|

India

|

Industry consolidation and trade protection

|

Tariffs and domestic demand growth

|

Shift toward local tissue and packaging

|

|

Saudi Arabia

|

Mill efficiency and pigment optimization

|

Sustainability and cost reduction

|

Lower resin use and improved pigment yield

|

Paper Pigments Market Report Scope

Paper Pigments Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$35.2 Billion

|

|

Market Size (2034)

|

$61 Billion

|

|

Market Growth Rate

|

6.3%

|

|

Segments

|

By Pigment Type (Inorganic Pigments, Organic Pigments, Specialty Pigments), By Application (Coating Pigments, Filler Pigments), By Paper Grade (Packaging and Board, Printing and Writing, Tissue and Hygiene, Specialty Paper), By Processing Form (Slurry Form, Dry Powder)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Omya, Imerys, Minerals Technologies, LB Group, Tronox Holdings, Solenis, BASF, Kemira, Sudarshan Chemical Industries, Chemours, Venator Materials, KaMin, Thiele Kaolin Company, Ashland, Huber Engineered Materials

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Paper Pigments Market Segmentation

By Pigment Type

By Application

- Coating Pigments

- Filler Pigments

By Paper Grade

- Packaging and Board

- Printing and Writing

- Tissue and Hygiene

- Specialty Paper

By Processing Form

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Paper Pigments Industry

- Omya

- Imerys

- Minerals Technologies

- LB Group

- Tronox Holdings

- Solenis

- BASF

- Kemira

- Sudarshan Chemical Industries

- Chemours

- Venator Materials

- KaMin

- Thiele Kaolin Company

- Ashland

- Huber Engineered Materials

*- List not Exhaustive