Recycled Paper Packaging Market Size, Overview, and Growth Outlook (2025–2034)

Recycled Paper Packaging Market to Nearly Double by 2034 as Sustainable Practices Gain Traction

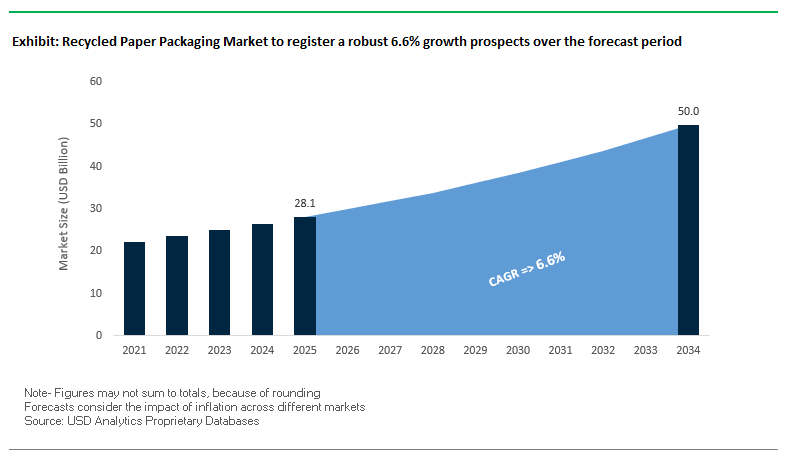

The global recycled paper packaging market is projected to grow from $28.1 billion in 2025 to $49.9 billion by 2034, registering a CAGR of 6.6%. Industry growth is driven by the combination of well-established recycling infrastructure, the rising demand for circular economy solutions, and increasing consumer awareness regarding eco-friendly packaging alternatives. Corrugated cardboard, a cornerstone of the industry, continues to dominate due to high recovery rates and proven recyclability.

Key Insights for industry professionals and buyers:

- Robust Recycling Infrastructure: Mature global collection and processing networks ensure a steady supply of recovered fiber.

- Corrugated Boxes Lead Market Demand: High recovery rates make them the preferred choice for brands seeking sustainable packaging.

- Increasing PCR Content in Products: Premium recycled paper packaging, especially in e-commerce, has seen a 25% rise in demand due to higher post-consumer recycled fiber content.

- E-commerce Drives Innovation: Lightweight, durable, and customizable packaging solutions, such as high-purity recycled corrugated mailer boxes, enhance brand recognition and consumer experience.

- Cost-Efficient Sustainability: Improved recycling technologies make recycled paper packaging increasingly competitive versus virgin materials.

- Customization and Brand Differentiation: Digital printing and design innovations allow brands to tailor recycled packaging to meet consumer expectations.

Market Analysis: Strategic Investments and Product Innovations Are Shaping the Recycled Paper Packaging Industry

The recycled paper packaging market continues to expand due to strong investments, mergers, and a growing focus on product innovation. In August 2025, International Paper announced the $1.5 billion sale of its Global Cellulose Fibers business while investing $250 million to convert its Riverdale mill into containerboard production. The same month, Smurfit Kappa Group reported sustained growth in corrugated box volumes across Europe and the Americas, indicating robust demand for recycled paper solutions.

Innovations in e-commerce and sustainable packaging are notable drivers of market growth. In June 2025, DS Smith launched a fiber-based e-commerce bag for Matas Group, offering a sustainable alternative to plastic. Earlier in March 2025, Cascades Inc. introduced produce baskets made from 100% recycled fibers, demonstrating commitment to providing eco-friendly alternatives for agricultural packaging. In January 2025, DS Smith unveiled its TapeBack solution, eliminating plastic tear strips in e-commerce packaging, alongside the TailorTemp® temperature-controlled solution, a fully recyclable packaging for the pharmaceutical sector.

Regulatory compliance and strategic mergers are shaping competitive positioning. The September 2024 merger of Smurfit Kappa Group and WestRock established Smurfit WestRock, enhancing global footprint and product diversity. In November 2024, Smurfit Kappa introduced innovations for Bag-in-Box customers to meet evolving regulations, highlighting proactive adaptation to market standards.

Recycled Paper Packaging Market: Trends and Opportunities Reshaping Sustainable Packaging

Strategic Shift to 100% Recycled Content for Retail-Ready and E-Commerce Packaging

One of the strongest trends in the recycled paper packaging market is the accelerated adoption of 100% recycled content across retail-ready and e-commerce packaging formats. E-commerce platforms are taking the lead, with major online retailers collaborating with packaging suppliers to roll out fully recycled solutions such as the EarthKraft™ mailer, which replaces non-recyclable poly-based alternatives. This shift is closely tied to broader corporate strategies where retailers pledge to ensure curbside recyclability and reduce environmental impact across their logistics operations. Beyond e-commerce, multinational consumer goods giants like Unilever and Nestlé have committed to integrating at least 1 million tons of recycled materials annually into their packaging portfolios by 2025. These commitments are directly influencing demand for recycled fiberboard, cartons, and shipping boxes at scale. As online retail continues to surge, the expectation for fully recyclable, high-volume packaging formats is creating both pressure and opportunity for paper mills, converters, and brand owners to secure consistent supplies of post-consumer recycled (PCR) fiber to meet procurement targets.

Innovation in Performance-Enhanced Recycled Fiber for Demanding Applications

Recycled paper packaging is no longer limited to basic corrugated boxes; innovations are elevating its role in premium and high-performance segments. Leading paperboard producers have introduced coated recycled paperboard grades designed for high-resolution graphics, embossing, and foil stamping, enabling luxury goods and electronics brands to maintain premium aesthetics without virgin fiber dependency. On the performance side, containerboard producers are leveraging advanced refining and additive technologies to strengthen recycled corrugated packaging. For instance, a major mill achieved a 15% increase in burst strength in its recycled containerboard by optimizing a blend of old corrugated containers (OCC) with targeted strength enhancers. These improvements are allowing recycled-based solutions to enter heavy-duty shipping applications that require durability, stacking strength, and moisture resistance. Together, these advancements prove that recycled paper packaging can not only meet but often exceed performance benchmarks, positioning it as a sustainable and versatile solution for industries beyond basic consumer packaging.

Development of Advanced Deinking and Decontamination Processes for Mixed Paper Streams

The recovery of mixed paper streams has long been a bottleneck for the recycled paper packaging industry due to contamination challenges. However, advanced deinking and decontamination technologies are creating new value opportunities. Companies like TOMRA are pioneering AI-powered sensor sorting systems capable of identifying and removing contaminants such as plastic films, foils, and even food-stained pizza boxes from mixed paper bales. This innovation ensures cleaner inputs for mills, improving yields and reducing quality risks in finished packaging products. On the regulatory and food-safety front, advancements in super-clean washing and high-temperature dispersion are enabling recycled fiber to achieve compliance with food-contact standards. Research shows that these methods allow recycled pulp to be repurposed into packaging for cereals, dry foods, and other grocery staples, unlocking a high-value application segment traditionally dominated by virgin fiber.

Expansion of Recycled Fiber-Based Molds and Pulp Forms for Protective Packaging

Another significant opportunity lies in the expansion of molded pulp and thermoformed fiber solutions, which are increasingly replacing non-recyclable expanded polystyrene (EPS) foam. A case study revealed that a global electronics manufacturer successfully switched to 100% recycled molded pulp end caps for laptops, significantly reducing plastic waste while ensuring recyclability and biodegradability. Beyond electronics, thermoformed pulp offers remarkable versatility, with applications spanning cosmetics, medical devices, and fragile consumer goods. The ability to design custom-fit, shock-absorbing protective packaging through thermoforming gives brands both sustainability and functional advantages. These solutions align with growing global regulations targeting EPS bans and cater to consumer demand for eco-friendly packaging formats. With scalable applications across multiple industries, molded pulp is expected to emerge as one of the fastest-growing segments within the recycled paper packaging market.

Competitive Landscape: Leading Recycled Paper Packaging Companies Focus on Circular Economy and Innovation to Strengthen Market Leadership

The competitive landscape of recycled paper packaging is shaped by companies that emphasize sustainability, recycling, and technological innovation. Market leaders are enhancing recycling capabilities, investing in product R&D, and implementing circular business models to meet the growing demand for eco-friendly packaging solutions.

Smurfit Kappa Group (Smurfit WestRock): Creating a Global Leader in Sustainable Packaging Through Merger and Innovation

Smurfit Kappa provides paper-based packaging solutions, including corrugated, folding carton, and bag-in-box products. The September 2024 merger with WestRock created a global sustainable packaging leader with expanded geographic reach. Smurfit Kappa’s closed-loop recycling model ensures efficient collection, recycling, and reuse of paper and corrugated materials. Key offerings like the TopClip system, a paper-based alternative to plastic shrink wrap, exemplify innovation that helps clients achieve sustainability targets.

International Paper Company: Investing in Containerboard and State-of-the-Art Facilities to Strengthen Recycled Packaging Portfolio

International Paper is a leader in fiber-based packaging, pulp, and paper products. In August 2025, it sold its Global Cellulose Fibers business for $1.5 billion while investing $250 million to convert its Riverdale mill to containerboard production. In May 2025, the company broke ground on a new packaging facility in Waterloo, Iowa, to meet rising regional demand. International Paper is recognized for its forest stewardship, recycling expertise, and commitment to high PCR content in packaging materials.

DS Smith Plc: Championing Circular Design Principles With Innovative, Fully Recyclable Packaging Solutions

DS Smith offers retail, shelf-ready, and transit packaging designed for recyclability. The company’s closed-loop recycling system ensures paper and corrugated materials are reused efficiently. In January 2025, DS Smith launched the TapeBack solution and TailorTemp® packaging, showcasing its commitment to plastic-free, fully recyclable solutions. Designers trained in Circular Design Principles enable clients to evaluate packaging performance in terms of recyclability, PCR content, and supply chain waste.

Mondi Group: Advancing Sustainable High-Barrier Paper Packaging for Diverse Industries

Mondi produces a broad range of innovative paper-based packaging, including corrugated and stand-up pouches. Recent innovations include FunctionalBarrier Paper Ultimate, a high-performance sustainable alternative. The company’s MAP2030 plan aims to increase recycled and renewable material use. In August 2025, Mondi advanced energy self-sufficiency to 90% at its Slovakian pulp and paper mill with a biomass power plant, demonstrating a focus on sustainability and operational efficiency.

Cascades Inc.: Leading Eco-Friendly Packaging Innovation With 100% Recycled Fiber Solutions

Cascades specializes in eco-friendly packaging and tissue products, offering corrugated solutions with high recycled fiber content. Its strategy emphasizes green innovation and performance-driven designs. In March 2025, Cascades launched produce baskets made from 100% recycled fibers, alongside insulated boxes for e-commerce and food service, highlighting sustainable alternatives to plastic and difficult-to-recycle packaging.

Recycled Paper Packaging Market Share Insights, 2025-2034

Corrugated Cardboard dominates Market Share by Product Type in Recycled Paper Packaging

Corrugated cardboard accounts for the largest share at 55%, cementing its role as the backbone of the recycled paper packaging industry. Its dominance stems from its universal use in e-commerce, logistics, and retail supply chains, where strength, durability, and recyclability are equally critical. Most corrugated structures are composed of 70–100% recycled fiber, with fluting almost entirely sourced from recovered material. The rapid growth of online shopping and global shipping networks has fueled corrugated’s expansion, making it the most standardized and scalable recycled paper format worldwide. Folding carton board, with around 20% share, remains the face of consumer retail packaging, balancing recycled inner plies with virgin outer layers for high-quality graphics. Kraft papers hold 10%, widely adopted for grocery bags and shipping sacks, benefiting from pulping technologies that enhance durability using recycled fibers. Molded pulp at 8% is the fastest-growing niche, providing a sustainable substitute for plastic clamshells and cushioning in electronics, foodservice, and wine packaging. The remaining 7%, including specialty paperboards such as tube board and chipboard, maximizes the closed-loop use of lower-grade recycled fibers. Collectively, these categories highlight how recycled paperboard remains the most circular and commercially mature packaging substrate, with corrugated setting the performance and sustainability benchmark.

E-commerce & Retail drive Market Share by End-Use in Recycled Paper Packaging

The E-commerce & retail sector (35%) is the largest consumer of recycled paper packaging, propelled by the explosive rise of direct-to-consumer shipping. Corrugated cardboard boxes have become the standard, and brands increasingly leverage recycled content as a marketing tool, positioning sustainable packaging as part of the “unboxing experience.” The food & beverages industry (25%) is another major driver, requiring recycled paperboard enhanced with functional coatings that provide grease, moisture, and freezer resistance without contaminating recycling streams. Logistics & shipping (15%) represents a large B2B user, focused on high-strength corrugated and kraft papers for bulk industrial use. Consumer goods (12%) employ folding cartons and rigid paperboard not only for protection but also as a visible sustainability signal that boosts brand image. Industrial goods (8%) rely on corrugated and kraft primarily for durability and cost efficiency, while healthcare & pharmaceuticals (5%) remain cautious due to strict sterility and purity requirements—limiting recycled content mainly to secondary cartons. The concentration of demand in e-commerce and food underscores how recycled paper packaging is driven simultaneously by logistics efficiency and consumer-facing sustainability.

European Union: PPWR and Ecodesign Regulations Driving Recycled Paper Adoption

The European Union is leading the transformation of the recycled paper packaging market through the Packaging and Packaging Waste Regulation (PPWR), which came into force in February 2025. This landmark regulation replaces the earlier directive and introduces comprehensive rules governing the full lifecycle of packaging, with the ultimate goal of achieving a circular economy. By 2030, all packaging must achieve 70% recyclability (Grade C), and by 2038, packaging must meet Grade A (95%) or Grade B (80%), creating significant pressure on manufacturers to redesign packaging formats for recyclability. The ban on single-use plastic packaging for fruits and vegetables below 1.5 kg from 2030 is also accelerating the shift toward recycled and fiber-based alternatives.

Europe already demonstrates strong recycling performance, with a 79.3% recycling rate in 2023, surpassing its 76% target for 2030, as set out in the European Declaration on Paper Recycling 2021–2030. Supporting regulations such as the Ecodesign for Sustainable Products Regulation (ESPR), effective since mid-2024, require transparency through Digital Product Passports and enforce stricter design criteria for sustainability. From 2028, a harmonized recycling label will be mandatory, standardizing consumer communication across all member states. Additionally, restrictions on hazardous substances like PFAS in food-contact packaging from August 2026 are shaping the material choices of paper converters and recyclers. These combined measures are positioning the EU as a global benchmark for sustainable and compliant recycled paper packaging solutions.

United States: EPR Legislation and Corrugated Packaging Innovation Driving Growth

The United States recycled paper packaging market is being propelled by both federal initiatives and state-level mandates. The U.S. Environmental Protection Agency (EPA), in collaboration with the U.S. Plastics Pact, is pushing for a circular economy model, driving companies to adopt recyclable substrates and expand fiber-based alternatives. A major trend is the shift toward mono-material packaging, which simplifies sorting and reduces contamination in recycling streams. At the state level, Extended Producer Responsibility (EPR) laws have been passed in seven states, including California, with compliance requirements that will have nationwide implications for packaging supply chains.

The Infrastructure Investment and Jobs Act is funding advanced recycling facilities, enhancing domestic paper recycling infrastructure and strengthening local supply chains. On the product development front, brands are rapidly adopting lightweight corrugated formats to replace rigid plastics in produce and grocery packaging, balancing cost efficiency with sustainability goals. The adoption of advanced digital printing technologies—including UV-curable and eco-solvent inks—is allowing manufacturers to create high-definition, fade-resistant branding on recycled paper substrates, adding value to packaging without compromising recyclability. With increasing consumer demand for eco-friendly grocery packaging and e-commerce boxes, the U.S. is emerging as one of the fastest-growing markets for recycled corrugated and paperboard solutions.

China: Dual Circulation Strategy and E-Commerce Growth Boosting Paper Recycling

China’s recycled paper packaging market is being shaped by comprehensive government reforms under the 14th Five-Year Plan, which emphasizes the development of a robust domestic recycling system. Agencies such as the National Development and Reform Commission (NDRC) and the Ministry of Ecology and Environment (MEE) are enforcing stricter controls on plastic pollution, fueling demand for paper-based alternatives. New national standards for edible agricultural products restrict excessive packaging, setting limits on interspace ratios, packaging layers, and cost proportions, which are forcing manufacturers to streamline packaging designs.

A critical milestone was the ban on waste paper imports, which reshaped global recycling flows and compelled China to develop self-sufficient domestic recycling systems. Under the Dual Circulation strategy, domestic demand is the priority growth driver, with the booming e-commerce industry acting as a catalyst for paper-based packaging solutions. At the same time, the government is offering tax incentives for companies investing in remanufacturing and green technologies, accelerating innovation in corrugated cartons, recycled kraft paper, and molded fiber packaging. These combined policies are reinforcing China’s role as both a major consumer and supplier of recycled paper packaging in global markets.

India: EPR Mandates and Rising Food Packaging Demand Accelerating Adoption

The Indian recycled paper packaging market is undergoing rapid transformation due to the Plastic Waste Management (Amendment) Rules, 2024, which place significant emphasis on Extended Producer Responsibility (EPR). New Environment Protection Rules, 2024, extend EPR obligations to paper, glass, and metal packaging, mandating recycled content across all obligated packaging. For paper, targets have been set at 40% recycled content by 2026–27, increasing to 70% by 2029–30, pushing manufacturers toward large-scale adoption of recycled fibers. Every recycled paper packaging product must now carry a label disclosing the percentage of recycled content and conform to Indian Standard IS 14534:2023, enhancing compliance transparency.

India is also seeing significant innovation in bioplastic and hybrid solutions, including patents for biodegradable materials derived from agricultural and dairy waste, such as ghee residue-based bioplastic. These eco-friendly materials complement recycled paper packaging and align with corporate sustainability goals. The country’s increasing consumption of processed foods, dairy, and ready-to-eat meals is a major driver, with recycled cartons and trays playing a crucial role in preserving freshness and ensuring food safety. Supported by the government’s strong regulatory stance and the rising demand from food, retail, and e-commerce, India is positioning itself as a key growth market for recycled paper packaging in Asia.

Japan: Advanced Paper-Based Materials and Bio-PP Integration in Packaging

Japan’s recycled paper packaging market is characterized by technological innovation and high sustainability standards. Companies like Nippon Paper Industries are leading the way with products such as SHIELDPLUS, a recyclable paper with advanced barrier properties against oxygen and odors, offering a viable replacement for plastic laminates in food and cosmetic packaging. The government is simultaneously promoting bio-polypropylene (bio-PP) integration, with a goal to introduce 2 million tons of bio-PP annually by 2030, leading to new paper-plastic hybrid solutions.

The market is also benefiting from strong government advocacy for a circular economy, encouraging investments in materials that are both recyclable and compostable. Strategic collaborations, such as LyondellBasell and Shiseido’s integration of bio-PP in cosmetics packaging, showcase how Japanese companies are blending renewable materials with paper packaging to meet both performance and environmental goals. Oversight by organizations such as the Japan Vinyl Industry Association (JVIA) ensures that new packaging formats comply with rigorous safety and quality standards. Japan’s strong consumer preference for high-quality and aesthetically refined packaging further accelerates the adoption of premium recycled paperboard and corrugated solutions.

Brazil: Reverse Logistics System and Corrugated Packaging Adoption

Brazil’s recycled paper packaging market is expanding under the framework of the National Solid Waste Policy (PNRS), which mandates responsible waste management practices including reuse, recycling, and waste reduction. A cornerstone of this policy is the reverse logistics system, which places responsibility on producers for post-consumer collection and recycling of packaging. This system is encouraging companies to design packaging with recyclability in mind, spurring investments in corrugated cartons, recycled kraft paper, and molded paper trays.

The government’s strong commitment to waste reduction and recycling infrastructure investment is positioning Brazil as a leader in sustainable packaging within Latin America. The food and agriculture sector, in particular, is driving demand, with corrugated boxes and recycled trays gaining adoption for maintaining freshness and extending shelf life. These formats are increasingly used for fruits, vegetables, and meat exports, aligning with international buyer expectations for eco-friendly packaging. With the combination of regulatory pressure and global trade competitiveness, Brazil is poised to accelerate its transition toward eco-friendly recycled paper packaging solutions.

Recycled Paper Packaging Market Report Scope

Recycled Paper Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$28.1 Billion

|

|

Market Size (2034)

|

$49.9 Billion

|

|

Market Growth Rate

|

6.6%

|

|

Segments

|

By Product Type (Corrugated Cardboard, Folding Carton Board, Paperboard, Molded Pulp, Kraft Papers), By Packaging Type (Boxes & Cartons, Bags & Sacks, Wraps & Films, Tubes & Cores, Molded Pulp Products), By End-Use Industry (Food & Beverages, Consumer Goods, E-commerce & Retail, Logistics & Shipping, Healthcare & Pharmaceuticals, Industrial Goods)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

WestRock Company, International Paper Company, Smurfit Kappa Group Plc, DS Smith Plc, Mondi Group, Sonoco Products Company, Graphic Packaging Holding Company, Oji Holdings Corporation, Nippon Paper Industries Co., Ltd., Stora Enso Oyj, Pactiv Evergreen Inc., Amcor plc, Greif, Inc., Cascades Inc., Pratt Industries

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Recycled Paper Packaging Market Segmentation

By Product Type

- Corrugated Cardboard

- Folding Carton Board

- Paperboard

- Molded Pulp

- Kraft Papers

By Packaging Type

- Boxes & Cartons

- Bags & Sacks

- Wraps & Films

- Tubes & Cores

- Molded Pulp Products

By End-Use Industry

- Food & Beverages

- Consumer Goods

- E-commerce & Retail

- Logistics & Shipping

- Healthcare & Pharmaceuticals

- Industrial Goods

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Recycled Paper Packaging Market

- WestRock Company

- International Paper Company

- Smurfit Kappa Group Plc

- DS Smith Plc

- Mondi Group

- Sonoco Products Company

- Graphic Packaging Holding Company

- Oji Holdings Corporation

- Nippon Paper Industries Co., Ltd.

- Stora Enso Oyj

- Pactiv Evergreen Inc.

- Amcor plc

- Greif, Inc.

- Cascades Inc.

- Pratt Industries

* List Not Exhaustive

Methodology

USDAnalytics employs a rigorous and structured approach to analyze the global recycled paper packaging market, combining primary and secondary research with advanced data modeling to ensure accuracy and reliability. The methodology includes comprehensive assessments of industry drivers, regulatory frameworks, and technological innovations impacting market growth. Primary research consists of detailed interviews with key stakeholders such as packaging manufacturers, suppliers, distributors, and industry experts, providing insights into supply chain dynamics, product adoption, and emerging trends. Secondary research leverages authoritative sources including company annual reports, press releases, government policies, and industry publications to validate market projections and competitive positioning. Quantitative models, including CAGR forecasts, market sizing, and segmentation analysis by product type, packaging format, and end-use industry, are developed using historical data and trend extrapolation. USDAnalytics also evaluates regional and country-specific dynamics, factoring in policy impacts, sustainability mandates, and consumer behavior to provide actionable intelligence. Finally, the research integrates competitor analysis and investment patterns to present a holistic view of market opportunities, ensuring that business leaders, investors, and professionals receive actionable, evidence-based insights for strategic decision-making in the recycled paper packaging sector.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.