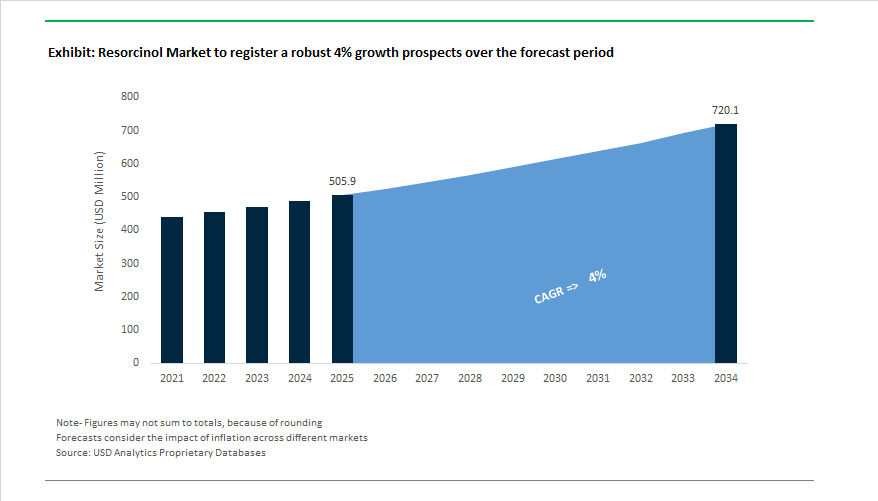

The Global Resorcinol Market is forecast to expand from $505.9 million in 2025 to $720.1 million by 2034, registering a CAGR of 4%. Resorcinol’s role as a critical raw material in Resorcinol–Formaldehyde Latex (RFL) adhesive systems for tire manufacturing, coupled with its use in UV stabilizers, wood adhesives, and pharmaceutical intermediates, continues to anchor its industrial importance. The compound’s versatility and high bonding strength position it as a fundamental specialty intermediate across the automotive, construction, chemical, and healthcare sectors.

Majority of global resorcinol volume is consumed by the tire and rubber industry, primarily in RFL adhesive applications for bonding rubber to polyester, nylon, and steel cords. This strong dependence ties the resorcinol market closely to global automotive production cycles. Furthermore, the 99% purity segment dominates specialty applications such as UV absorbers, flame retardants, and dermatological active ingredients, underscoring the growing need for stringent quality control and advanced synthesis processes among leading producers.

Regionally, over 60% of global resorcinol capacity is concentrated in Asia-Pacific, particularly in China, Japan, and South Korea, forming the backbone of global supply. This concentration introduces a strategic supply chain risk for Western buyers, pushing North American and European players toward domestic capacity expansions to secure stable feedstock access. On the downstream front, the RFL adhesive market, valued at $1.29 billion in 2024, demonstrates resorcinol’s industrial influence extends beyond base chemicals into performance adhesive ecosystems that sustain high-strength bonding and heat resistance.

The global resorcinol industry is navigating a dynamic period of structural reorganization, characterized by raw material price volatility, regional consolidation, and a growing emphasis on bio-based derivatives and digital manufacturing efficiency. The market’s resilience is increasingly tied to the ability of producers to secure feedstocks such as benzene and sulfuric acid, manage supply chain disruptions, and diversify application portfolios across industrial and pharmaceutical segments.

In June 2024, the market experienced a price surge warning following escalating feedstock costs and logistical constraints at major Asian chemical export ports. This volatility highlighted the vulnerability of global resorcinol pricing to disruptions in the Asia-Pacific supply chain, particularly as over 60% of production capacity is regionally concentrated. In response, INDSPEC Chemical Corporation (U.S.) completed its $10 million capacity expansion in March 2023, increasing North American output by 50% to improve local supply resilience and reduce dependency on Asian imports for the tire, wood, and specialty adhesive sectors.

A major corporate transformation unfolded in May 2025, when Mitsui Chemicals Group announced a strategic portfolio split, divesting parts of its Basic & Green Materials division to accelerate its shift toward high-margin specialty products, including resorcinol-based performance resins. Complementing this move, Sumitomo Chemical (June 2025) launched its “DX NEXT empowered by AI” initiative, integrating digitalization into its production systems to enhance process efficiency, cost optimization, and product traceability—factors increasingly critical in the specialty resorcinol market.

In September 2025, Mitsui Chemicals, Idemitsu Kosan, and Sumitomo Chemical signed an MOU to consolidate polyolefin businesses, reinforcing a broader national trend of Japanese petrochemical consolidation. This strategy aims to free capital for investment in advanced materials and resorcinol-related performance chemicals, aligning with Japan’s push toward specialty production and carbon efficiency. On the sustainability front, bio-based resorcinol derivatives have gained momentum since 2024, driven by the automotive and construction industries’ shift toward eco-friendly adhesives and renewable chemistry platforms.

Meanwhile, SABIC’s 2024 Annual Report highlighted a major portfolio optimization program, involving divestitures from non-core sectors to reallocate capital toward its Advanced Materials and Specialties divisions, where resorcinol derivatives for electrical and electronics applications represent an emerging focus.

Market Trend 1: Supply Chain Consolidation and Vertical Integration to Secure Raw Material Stability

A defining transformation in the global Resorcinol market is the strategic consolidation of production networks and backward integration among leading manufacturers. The structural shift is designed to insulate producers from supply disruptions and volatile benzene feedstock costs, which surged notably through 2023. With Resorcinol’s production heavily dependent on benzene and specialized catalysts, producers are focusing on self-sufficiency, long-term raw material contracts, and domestic capacity expansion to maintain supply security.

In 2023, a major U.S.-based Resorcinol producer announced a $10 million investment to expand its manufacturing capacity by 50%, ensuring a stable domestic supply chain for the rubber, tire, and wood adhesives sectors. The expansion aligns with the increasing demand from the automotive tire industry, which relies heavily on Resorcinol-Formaldehyde-Latex (RFL) adhesion systems—an indispensable component for bonding steel cords and polyester reinforcements in high-performance and electric vehicle (EV) tires.

The EV segment, in particular, is driving a new wave of demand for advanced RFL systems due to their superior durability, fatigue resistance, and low rolling resistance properties—key for improving battery efficiency. Regional analysis confirms that Asia-Pacific accounts for nearly 70% of global Resorcinol consumption, highlighting its dominance as a production hub and a critical link in the global tire manufacturing value chain. As major players vertically integrate and secure domestic sourcing, Resorcinol supply stability and cost optimization are emerging as competitive differentiators.

Market Trend 2: Rapid R&D Acceleration Toward Bio-Based Resorcinol for Low-Carbon Adhesive and Resin Applications

The Resorcinol industry is witnessing a surge in R&D focused on decarbonizing production pathways through bio-based Resorcinol synthesis, targeting the automotive, construction, and composite sectors. As industries move toward non-petroleum-derived phenolic compounds, academic and industrial partnerships are developing renewable aromatic intermediates to replace fossil-based feedstocks.

Recent research demonstrates the successful synthesis of bio-derived aromatic polyesters utilizing Resorcinol as a core monomer, positioning it as a sustainable alternative for coatings, adhesives, and packaging materials. Further, national bioeconomy strategies—such as the India BioEconomy Report 2024—are prioritizing investments in biomanufacturing hubs and pilot facilities for producing bio-based aromatics, including Resorcinol.

In material science, Resorcinol-derived monomers are being employed in the creation of bio-based epoxy systems and green adhesives. These next-generation materials demonstrate exceptional tensile strength and ductility, outperforming conventional epoxy resins by up to threefold in carbon fiber-reinforced composites. As global sustainability commitments strengthen across automotive and construction industries, bio-based Resorcinol is poised to become a cornerstone of low-VOC, renewable adhesive chemistry, directly supporting the decarbonization of industrial value chains.

Market Opportunity 1: Expansion into High-Purity Pharmaceutical-Grade Resorcinol for Dermatological and Antimicrobial Innovation

The pharmaceutical-grade Resorcinol market represents a rapidly emerging high-margin niche driven by advances in dermatological and antimicrobial formulations. Resorcinol’s pharmacological relevance is being re-evaluated for modern medical and cosmetic applications, particularly due to its keratolytic, antibacterial, and antioxidant properties.

The compound already holds regulatory approval under U.S. FDA guidelines, where it is listed for over-the-counter topical use at ≤2% concentration for acne and skin disorder treatments. However, current innovation is focused on developing ultra-high purity Resorcinol suitable for prescription-grade and nanomaterial-based biomedical applications.

Recent research highlights Resorcinol’s role in the in situ synthesis of silver nanoparticles (AgNPs) to produce agar-based films exhibiting strong antimicrobial and antioxidant activity. These materials have demonstrated high efficacy against common pathogens like E. coli and S. aureus, opening doors for their use in advanced wound dressings and antimicrobial coatings.

With stringent purity specifications required for pharmaceutical-grade production—preventing oxidation, discoloration, and degradation—the segment demands specialized purification and controlled environment manufacturing. The evolution from traditional OTC uses toward clinical-grade applications positions Resorcinol as a strategic ingredient in next-generation healthcare formulations, bridging pharmaceuticals, biomaterials, and active medical coatings.

Market Opportunity 2: Engineering of Resorcinol-Formaldehyde Gels for Geothermal Energy and Advanced Carbon Materials

Resorcinol-Formaldehyde (RF) chemistry is unlocking transformative opportunities in energy storage and advanced materials engineering, particularly through its ability to form highly porous, thermally stable gels and aerogels. These RF gels serve as essential precursors for carbon aerogels, foams, and xerogels—materials with exceptional electrical conductivity, low density, and tunable porosity.

In Engineered Geothermal Systems (EGS), RF gels are emerging as temperature-resistant sealing and insulating agents, essential for subsurface stability and pressure control under extreme thermal and mechanical stress. The ability to fine-tune pore size (from 2–200 nm) by adjusting synthesis parameters such as pH, catalyst concentration, and reaction time allows for customized performance across geothermal and carbon capture technologies.

Additionally, carbon xerogels derived from RF polymers are attracting growing interest in energy storage systems, including supercapacitors and hydrogen fuel cells, due to their high specific surface area and conductivity. Their structural uniformity and thermal endurance make them ideal for next-generation high-capacity electrodes and catalyst supports.

Resorcinol Market Share Insights, 2025-2034

Market Share by Grade

Technical Grade Resorcinol holds a commanding 74.1% share of the global resorcinol market in 2025, driven by its widespread use across industrial and manufacturing applications where cost-efficiency and performance outweigh the need for ultra-high purity. This grade is indispensable in rubber adhesives, tire manufacturing, wood bonding resins, and UV stabilizers, forming the backbone of resorcinol’s industrial consumption. Its dominance is supported by large-scale demand from automotive, construction, and electronics sectors, where resorcinol-based compounds are crucial for enhancing material performance under thermal and mechanical stress. The compound’s superior bonding strength and chemical compatibility make it the adhesive of choice in rubber-to-metal and wood-to-wood laminations, ensuring durability in dynamic environments.

Conversely, Pure/Pharmaceutical Grade Resorcinol occupies a smaller but rapidly expanding share, characterized by its use in pharmaceutical formulations, dermatological treatments, and specialty chemical synthesis. The pharmaceutical and high-purity segment demands exceptional quality standards, particularly for applications in antiseptics, acne medications, and pharmaceutical intermediates. Despite its limited volume share, the segment carries a high value margin due to stringent purity requirements and controlled manufacturing processes. Growing investment in pharmaceutical R&D, coupled with the rising demand for dermatological and antiseptic formulations in developing economies, is expected to accelerate the growth of this grade. The clear market divide illustrates a balance between high-volume, cost-sensitive industrial uses and low-volume, premium pharmaceutical applications, positioning resorcinol as a versatile compound across multiple industries.

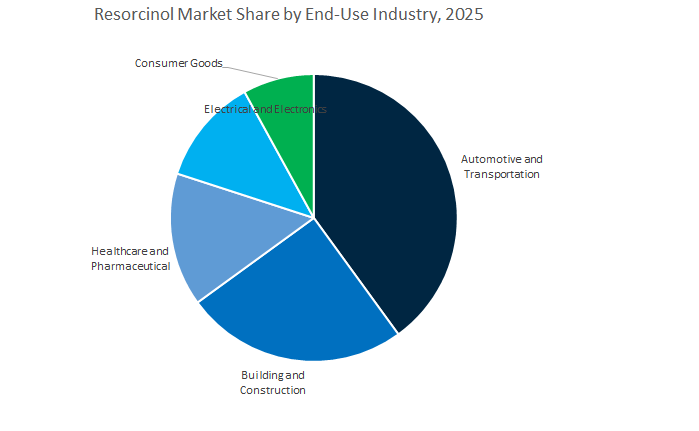

Market Share by End-Use Industry

Automotive and Transportation remains the largest consumer of resorcinol, accounting for an estimated 42.3% share of the global market by 2025, primarily due to its indispensable role in rubber-to-metal bonding adhesives used for tire cord and steel belting applications. The compound’s ability to form strong, heat-resistant bonds between metal and rubber materials makes it vital for tire reinforcement, brake pads, gaskets, belts, and vibration damping components. With increasing global vehicle production, particularly in emerging markets, and the rise of electric vehicles (EVs) requiring advanced tire and vibration control systems, the automotive sector continues to anchor resorcinol demand. The compound’s performance advantages over traditional phenolic adhesives further consolidate its market dominance in this segment.

The Building and Construction sector represents another major application area, utilizing resorcinol-based adhesives for structural wood bonding, marine-grade plywood, laminated beams, and weather-resistant panels. Its durability under moisture, temperature variation, and UV exposure makes it essential for high-performance architectural and infrastructure projects. Meanwhile, the Healthcare and Pharmaceutical industry is emerging as a high-growth segment, leveraging resorcinol’s antibacterial, antiseptic, and keratolytic properties for medicinal and dermatological formulations. The Electrical and Electronics segment increasingly utilizes resorcinol in UV stabilizers, epoxy resins, and flame-retardant materials, especially for heat-resistant and insulating components in modern electronic devices.

The Consumer Goods sector adds further diversity to the market, with resorcinol integrated into cosmetic formulations (such as hair dyes and skin treatments) and furniture adhesives. However, this segment is experiencing mild substitution pressure from greener alternatives due to regulatory scrutiny in cosmetics and consumer applications.

The Global Resorcinol Market is led by vertically integrated chemical companies such as Sumitomo Chemical, Mitsui Chemicals, INDSPEC (OxyChem), Sinopec Shanghai Petrochemical, and Atul Ltd.. These players are diversifying into advanced formulations, improving energy efficiency, and implementing digitalized manufacturing systems to sustain profitability amid rising compliance and sustainability costs.

Sumitomo Chemical is strengthening its leadership in Essential & Green Materials, with resorcinol as a core product line serving the automotive, tire, and agrochemical industries. Through its 2025–2027 Business Plan, the company has prioritized digital transformation (DX NEXT empowered by AI) to enhance operational efficiency and predictive maintenance in its production facilities. Sumitomo’s integrated chemical complexes ensure consistent supply of high-purity resorcinol, a crucial input for RFL adhesives and structural composites. Its long-standing presence in East Asia’s tire cord and adhesive chain positions it as a strategic partner for global automotive manufacturers.

INDSPEC Chemical Corporation, a subsidiary of Occidental Chemical (OxyChem), remains the only major resorcinol producer in North America, ensuring a critical domestic supply for tire and engineered wood manufacturing. The company’s $10 million expansion (completed late 2023) boosted production by 50%, addressing regional demand surges and reducing import reliance. INDSPEC’s proprietary Resorcinol-based RFL adhesive formulations enable superior rubber-to-metal bonding in high-performance tires and industrial belts. Its focus on VOC compliance, reliability, and local sourcing makes it the cornerstone of the U.S. resorcinol supply network.

Mitsui Chemicals is actively transitioning toward a global specialty materials leader, with resorcinol-based performance resins playing a vital role in its high-value product mix. Its May 2025 portfolio restructuring marked a strategic divestment of non-core assets in favor of advanced materials R&D. The company’s Omuta Works facility (Japan), which resumed operations in September 2025 after a temporary disruption, remains a key node in Asia-Pacific’s specialty chemicals network. With its ongoing initiatives in chemically recycled and bio-mass balanced materials, Mitsui is aligning resorcinol production with circular economy principles and next-generation polymer compatibility.

Sinopec Shanghai Petrochemical, a subsidiary of China Petrochemical Corporation (Sinopec), commands a leading position in the Asia-Pacific resorcinol supply chain. Utilizing the Hydroperoxidation of Meta-Diisopropylbenzene process, the company achieves high-volume and cost-efficient production that anchors global pricing dynamics. Its resorcinol output primarily supports domestic tire and rubber industries, which account for a major share of the world’s vehicle manufacturing. Aligned with China’s five-year plan for chemical sustainability, Sinopec continues to invest in process optimization and emissions reduction, ensuring long-term competitiveness in basic and performance chemicals.

Atul Ltd., one of India’s most diversified chemical manufacturers, maintains a significant presence in the resorcinol and derivative markets. Its product line includes Resorcinol Dimethyl Ether, a critical intermediate for UV stabilizers and agrochemical compounds, supporting India’s expanding specialty chemicals sector. With growing domestic demand from tire and construction industries, Atul leverages its integrated operations to cater to both bulk and specialty chemical markets. The company’s adherence to high manufacturing standards and emphasis on pharmaceutical-grade resorcinol intermediates underscore its reputation for precision, purity, and reliability in global supply chains.

Country Analysis: Key Regional Developments and Strategic Shifts in the Global Resorcinol Industry

China: Global Resorcinol Production Powerhouse Undergoing Regulatory Transformation

China remains the world’s largest producer and exporter of Resorcinol, accounting for over 40% of global output and playing a pivotal role in the supply of rubber-to-textile adhesives, UV stabilizers, and fine chemical intermediates. However, the sector is currently undergoing a structural transformation due to stringent environmental and safety audits initiated by the government in late 2024, leading to temporary capacity constraints among key producers in East China. The compliance checks are reshaping the production ecosystem, forcing major manufacturers to upgrade emission control technologies and adopt greener production methodologies aligned with China’s “Green Chemical Industry Modernization” initiative.

China’s Resorcinol production base continues to expand in sophistication, with companies investing in automated, energy-efficient reactors and improved purification systems to reduce waste. The country’s strong domestic automotive and construction sectors sustain massive demand for Resorcinol-derived resins and coatings, while export volumes support global supply chains across rubber manufacturing, textile bonding, and UV-curable materials. With China’s strategic pivot toward supply chain resilience and environmental compliance, the nation’s Resorcinol market outlook remains robust, though characterized by short-term volatility due to regulatory realignment and potential price corrections in early 2025.

India: Emerging Regional Hub Backed by Trade Policy and Pharmaceutical Demand

India’s Resorcinol market is evolving rapidly as the country positions itself as a supply chain diversification hub amid tightening global supply conditions. The Directorate General of Trade Remedies (DGTR) launched an anti-dumping investigation in late 2024 targeting imports from other Asian producers, creating temporary pricing uncertainty but boosting the prospects of Atul Ltd., India’s only major domestic producer. Supported by the “Make in India” and Production Linked Incentive (PLI) schemes, Indian specialty chemical manufacturers are increasingly investing in indigenous feedstock production, aiming to reduce dependency on imports while aligning with national self-reliance goals.

Demand remains strong across automotive and pharmaceutical applications, with Pharmaceutical Grade Resorcinol being a critical raw material in dermatological and antiseptic formulations. The expansion of healthcare infrastructure and generics manufacturing continues to stimulate demand for high-purity Resorcinol intermediates. Simultaneously, the rubber processing sector—driven by the growth in tire manufacturing—provides consistent consumption momentum. India’s strategic focus on sustainability, domestic capability building, and high-value derivatives positions it as one of the fastest-growing Resorcinol markets in Asia-Pacific, offering long-term potential for both local and global investors.

Japan: High-Performance Innovation in EV Tires and Electronics Applications

Japan continues to be a technological pioneer in the Resorcinol industry, leveraging its advanced manufacturing infrastructure and world-class research institutions to develop high-purity and application-specific derivatives. Sumitomo Chemical Co., Ltd. has been at the forefront of R&D into next-generation RFL (Resorcinol-Formaldehyde-Latex) systems, tailored for electric vehicle (EV) tire manufacturing, where enhanced adhesion, lower rolling resistance, and improved thermal durability are paramount. The innovations reflect Japan’s broader commitment to sustainable mobility solutions and high-efficiency polymer bonding systems.

Japanese producers also lead in ultra-high-purity Resorcinol production, catering to niche markets in electronics, semiconductors, and UV light stabilization. Ongoing trade collaborations with Southeast Asia and North America ensure that Japan maintains a strategic export foothold in premium-grade Resorcinol applications. The nation’s precision chemical manufacturing culture and continued investments in eco-efficient synthesis technologies reinforce its position as a global innovation hub for advanced Resorcinol derivatives, particularly for high-end industrial and electronic use cases.

Germany: Sustainability Leadership and Advanced Rubber Chemical Innovation

Germany stands at the forefront of sustainable Resorcinol innovation, aligning industrial development with the EU’s REACH and Green Deal frameworks. As a European hub for chemical refinement and conversion, Germany focuses on creating safer handling and environmentally compliant synthesis processes for Resorcinol and its downstream derivatives. LANXESS AG, among others, is spearheading low-emission and renewable-based production models, incorporating greener reagents and advanced purification systems that reduce environmental impact without compromising quality.

The German automotive and rubber industries—long known for their engineering excellence—remain key consumers of Resorcinol-based adhesion systems, particularly in high-performance tire manufacturing. With European tire makers transitioning toward sustainable and recyclable rubber composites, demand for innovative RFL bonding agents continues to grow. Concurrently, Germany’s supply chain de-risking strategy, prompted by logistics disruptions and energy market volatility in 2024, has led to increased investments in domestic and intra-EU sourcing strategies for critical chemicals like Resorcinol. The proactive shift strengthens the region’s chemical independence and reinforces its leadership in performance and sustainability-focused chemical manufacturing.

United States: Specialized Applications and Transition Toward High-Performance, Sustainable Solutions

The U.S. Resorcinol market is defined by specialized demand and limited domestic production capacity, primarily served by INDSPEC Chemical Corporation and complemented by imports from Asia. The market’s strongest growth sectors include wood adhesives used in structural and engineered wood products such as glulam beams, where Resorcinol’s superior waterproofing and heat resistance make it indispensable for construction applications. Additionally, the U.S. remains a major innovation hub for flame retardant development, with chemical companies expanding R&D into Resorcinol-based non-halogenated systems for use in electronics, coatings, and aerospace composites.

Trade policy continues to shape the market landscape, with recent tariff revisions on chemical imports affecting cost structures and supply reliability. The has encouraged greater domestic research investment in synthesis alternatives and process optimization for specialty applications. The combination of stringent environmental regulations, growing sustainability goals, and strong R&D momentum positions the U.S. as a strategic consumer and innovation market for high-performance, eco-compliant Resorcinol derivatives.

South Korea: High-Tech Demand from Automotive and Electronics Manufacturing

South Korea’s Resorcinol market dynamics are strongly influenced by its advanced automotive and semiconductor industries, making it one of Asia’s most specialized consumers of high-grade derivatives. The country’s premium tire manufacturers—including global brands with domestic bases—maintain consistent demand for Resorcinol-based adhesives for tire cord bonding, ensuring superior adhesion, heat resistance, and performance in EV and high-performance tire segments.

Beyond automotive applications, Resorcinol derivatives are finding expanded use in photoresists, coating materials, and specialized electronic components, critical for semiconductor lithography and display technologies. Korean manufacturers are prioritizing supply chain diversification through multi-regional sourcing agreements, reducing dependency on any single country while ensuring resilience in high-volume production. With the nation’s aggressive R&D investment in advanced materials and electronic chemicals, South Korea remains a crucial end-use driver in the global high-purity Resorcinol market, bridging the automotive, semiconductor, and electronics sectors.

Resorcinol Market Report Scope

Resorcinol Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$505.9 Million

|

|

Market Size (2034)

|

$720.1 Million

|

|

Market Growth Rate

|

4%

|

|

Segments

|

By Application (Tires and Rubber Products, Wood Adhesives and Binders, UV Products and Dyes, Flame Retardants, Pharmaceuticals and Intermediates, Others), By Grade (Technical, Pure/USP/Pharmaceutical), By Production Method (Hydroperoxidation of Meta-Diisopropylbenzene, Benzene Disulfonation, Hydrolysis of Meta-Phenylenediamine), By End-Use Industry (Automotive and Transportation, Building and Construction, Healthcare and Pharmaceutical, Electrical and Electronics, Consumer Goods

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Sumitomo Chemical Co., Ltd., Atul Ltd., LANXESS AG, INDSPEC Chemical Corporation, Koei Chemical Co., Ltd., Amino-Chem Co., Ltd., Jiangsu Zhongdan Chemical Group Company, Mitsui Chemicals, Inc., Merck KGaA, SKW Trostberg GmbH, Domo Chemicals, Ube Industries, Ltd., Panjin Haoye Chemical Co., Ltd., BASF SE, The Goodyear Tire & Rubber Company

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Application

- Tires and Rubber Products

- Wood Adhesives and Binders

- UV Products and Dyes

- Flame Retardants

- Pharmaceuticals and Intermediates

- Others

By Grade

- Technical

- Pure/USP/Pharmaceutical

By Production Method

- Hydroperoxidation of Meta-Diisopropylbenzene

- Benzene Disulfonation

- Hydrolysis of Meta-Phenylenediamine

By End-Use Industry

- Automotive and Transportation

- Building and Construction

- Healthcare and Pharmaceutical

- Electrical and Electronics

- Consumer Goods

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Resorcinol Market

- Sumitomo Chemical Co., Ltd.

- Atul Ltd.

- LANXESS AG

- INDSPEC Chemical Corporation

- Koei Chemical Co., Ltd.

- Amino-Chem Co., Ltd.

- Jiangsu Zhongdan Chemical Group Company

- Mitsui Chemicals, Inc.

- Merck KGaA

- SKW Trostberg GmbH

- Domo Chemicals

- Ube Industries, Ltd.

- Panjin Haoye Chemical Co., Ltd.

- BASF SE

- The Goodyear Tire & Rubber Company

*- List not Exhaustive

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.