Market Overview: Structural Lightweighting and Multi-Material Design Elevate Metal Bonding Adhesives in Industrial Manufacturing

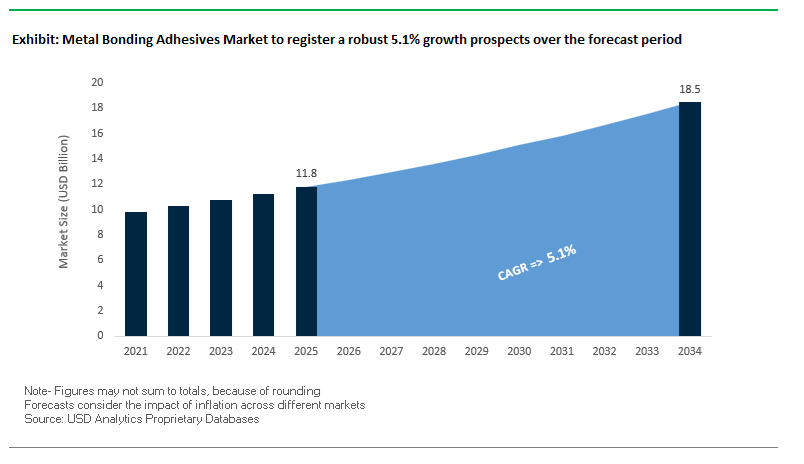

The Global Metal Bonding Adhesives Market is projected to grow from USD 11.8 billion in 2025 to USD 18.5 billion by 2034, advancing at a CAGR of 5.1%, as metal joining strategies across transportation and industrial manufacturing undergo a structural shift. Growth is driven by substitution and by OEM-led redesign of load paths, joining architectures, and material stacks, particularly in automotive, aerospace, and industrial equipment. Adhesive bonding is increasingly specified at the platform design stage, reflecting its role in enabling lightweight structures, fatigue resistance, and compatibility with dissimilar materials that mechanical fastening cannot achieve without penalties.

In automotive and aerospace manufacturing, lightweighting mandates and electrification targets are accelerating the transition away from spot welding, riveting, and bolting toward structural epoxy, polyurethane, and acrylic adhesives. Vehicle OEMs report up to 15% weight reduction in body structures when adhesive-based joining is integrated across body-in-white architectures, directly supporting fuel efficiency, extended EV range, and improved crash energy management. Manufacturers such as Henkel (LOCTITE structural epoxies), Sika, and 3M have expanded metal bonding portfolios engineered for high lap shear strength, controlled ductility, and thermal stability, enabling reliable joining of aluminum, high-strength steel, and carbon fiber-reinforced composites within a single assembly.

Process and surface engineering is becoming as critical as adhesive chemistry. The adoption of advanced surface preparation techniques—such as atmospheric plasma treatment, laser ablation, and nano-scale conversion coatings—is gaining importance, as OEMs seek to maximize bond durability while reducing primer usage and process variability. These surface innovations can increase lap shear strength by more than 300%, allowing thinner gauges, fewer fasteners, and simplified joint designs without compromising structural performance. In parallel, aerospace manufacturers continue to favor epoxy systems for their chemical resistance and thermal stability, particularly in fuselage panels, nacelle components, and bonded stiffeners exposed to cyclic loading and temperature extremes.

Beyond transportation, industrial machinery and equipment manufacturing represents a substantial and resilient demand base. Adhesives are increasingly selected to manage vibration damping, load distribution, and corrosion isolation in heavy equipment, enclosures, and fabricated assemblies where welding introduces distortion or stress concentrations. At the same time, bio-based and low-VOC formulations are gaining traction, reflecting tightening EU and North American regulatory frameworks and OEM sustainability commitments.

The metal bonding adhesives industry is undergoing a dynamic phase of technological transformation and business consolidation, with recent developments underscoring the sector’s response to sustainability pressures, regional manufacturing growth, and electrification trends.

In February 2025, Henkel AG & Co. KGaA expanded its adhesive technology portfolio with medical-grade cyanoacrylate-based adhesives under the Loctite brand, certified to ISO 10993 biocompatibility standards. This marks a major step toward diversifying metal-to-metal bonding solutions into healthcare and precision device manufacturing. Similarly, in January 2025, a major North American adhesives manufacturer inaugurated a South Carolina facility dedicated to high-performance adhesives—an investment reinforcing regional supply chain security and faster OEM integration in the automotive and industrial domains.

Mergers and acquisitions continue to reshape competitive structures. In November 2024, INX Group Limited finalized its acquisition of Coatings & Adhesives Corporation, enhancing its portfolio in the packaging adhesives space, particularly for metalized flexible packaging and rigid container applications. In October 2024, H.B. Fuller demonstrated strong sustainability leadership through the introduction of bio-based polyurethane and epoxy systems, addressing global VOC emission regulations and marking a pivotal transition toward eco-friendly bonding technologies.

Strategic regional expansions are further fueling market penetration. ThreeBond’s participation at the EV India Expo in September 2024 emphasized the company’s active engagement in Asian EV component manufacturing, especially in battery pack assembly adhesives. Similarly, Dow Inc.’s R&D investment in July 2024 focused on enhancing heat resistance for EV battery module bonding, reflecting how thermal management is emerging as a key adhesive performance parameter in energy storage systems. Permabond Europe’s April 2024 launch of TA4208 Black, a new toughened acrylic adhesive, provided a breakthrough in mixed-material bonding, while Huntsman Corporation’s March 2024 debut of bio-based adhesive platforms underscored the green chemistry trend. The European Union’s February 2024 discussions on diisocyanate regulation have further accelerated innovation toward micro-emission polyurethane systems—a defining trend expected to reshape formulation strategies globally.

Market Trend 1: Adoption of Dual-Cure and Toughened Acrylic Systems for High-Throughput Mixed-Material Assembly

The global shift toward lightweight, multi-material structures in industries like automotive, aerospace, and rail is driving the widespread adoption of dual-cure and toughened acrylic adhesives that combine rapid fixture capability with structural durability. These next-generation metal bonding adhesives are engineered for dissimilar substrates, enabling high-strength bonding of metals, composites, and thermoplastics without extensive surface preparation or mechanical fasteners.

A leading adhesive manufacturer recently introduced a two-part acrylic adhesive achieving 1,000 psi overlap shear strength within just 19 minutes at room temperature—an innovation that significantly reduces fixture time compared to traditional epoxies requiring multiple hours. The rapid-curing property directly enhances high-throughput production efficiency, particularly in automotive assembly lines where cycle-time reduction is critical.

Further, dual-cure mechanisms, combining UV and anaerobic curing, are gaining popularity for bonding opaque substrates such as aluminum and steel to fiber composites. The ensures complete curing even in “shadowed areas” where UV light cannot reach, guaranteeing consistent joint strength and dimensional stability across complex assemblies. In parallel, toughened acrylic adhesives are being engineered with enhanced peel and impact resistance, critical for crash durability and vibration management in next-generation vehicles.

The materials versatility of these new acrylics also supports bonding on oily or unprepared surfaces, a significant production advantage. As automotive and aerospace manufacturers adopt multi-material bonding strategies to meet lightweighting and emission reduction targets, structural acrylic adhesives have emerged as a high-performance, process-efficient alternative to welding and mechanical fastening.

Market Trend 2: Shift Toward Low-Temperature-Cure Epoxies for Thermal Protection of Electronic Components

In applications where heat sensitivity and dimensional precision are paramount—particularly in EV battery systems, aerospace sensors, and industrial electronics—the market is shifting toward low-temperature-cure epoxy adhesives. These formulations are optimized to cure fully between 60°C and 100°C, minimizing thermal stress on delicate circuitry, printed circuit boards (PCBs), and sensor assemblies while maintaining robust mechanical properties.

A major specialty chemicals company recently unveiled a new polyurethane and epoxy adhesive portfolio designed to enhance battery integration and protection in electric vehicles. These systems deliver high mechanical strength, dimensional stability, and thermal endurance, supporting the underbody and top-cover bonding of EV battery modules. Similarly, dual-functional epoxies are being introduced that combine heat-conductive mineral fillers with electrical insulation, preventing short circuits while effectively managing heat generated by high-density power electronics.

Additionally, two-component acrylic systems for hem-flange bonding demonstrate the industry’s growing preference for low-bake manufacturing processes, eliminating high-temperature oven cycles while achieving full structural integrity. The trend drives the broader transition toward energy-efficient curing, temperature-sensitive component protection, and process simplification in modern manufacturing ecosystems.

As the electrification of transport and automation in industrial electronics accelerate, low-temperature-curing metal bonding epoxies are becoming indispensable in achieving strong, thermally stable, and lightweight assemblies without compromising product reliability or throughput.

Market Opportunity 1: Driving Lightweight Multi-Material Design for Electric Vehicle Battery Enclosures

The evolution of electric vehicle (EV) architecture has created an expansive, long-term growth avenue for metal bonding adhesives in the assembly of battery enclosures (“skateboards”). These critical components require high-strength, vibration-resistant bonds that also act as hermetic seals to prevent moisture intrusion and thermal runaway risks. Adhesives are replacing traditional welding and mechanical fastening methods to join aluminum, steel, and composites, providing greater design flexibility while reducing total system weight.

Studies indicate that structural adhesives used in conjunction with self-piercing rivets or spot welds can match or exceed the stiffness and crash resistance of traditional welded assemblies. The combination not only improves vehicle safety but also enhances manufacturing efficiency and corrosion resistance. In addition, metal bonding adhesives serve as critical enablers for thermal management, bonding battery cells to heat-dissipating cold plates to facilitate efficient heat transfer and temperature regulation during charging and operation.

As automakers aim to extend EV range through lightweight materials and improved energy efficiency, thermally conductive structural adhesives are playing a pivotal role. These adhesives support multi-material bonding within battery packs, improve electromagnetic shielding, and ensure dimensional stability under dynamic conditions. Given the rising production of EVs globally, the application segment represents one of the most substantial revenue opportunities in the metal bonding adhesives market, with demand expected to accelerate as automakers adopt next-generation adhesive integration strategies for structural and thermal optimization.

Market Opportunity 2: Infrastructure Rehabilitation and Structural Reinforcement Using High-Performance Metal Bonding Adhesives

Aging civil infrastructure presents another major, long-term opportunity for the metal bonding adhesives market, supported by national infrastructure investment programs and the global focus on sustainable rehabilitation. Governments worldwide, including the U.S., have launched multi-billion-dollar infrastructure renewal plans targeting bridge repairs, water systems, and transportation assets—many of which require high-strength metal bonding epoxies for structural reinforcement.

Studies from the U.S. National Institute of Standards and Technology (NIST) emphasize that modern infrastructure repair requires durable, fatigue-resistant bonding technologies rather than short-term patching. Advanced epoxy adhesives and structural resins are being deployed for bonding Fiber-Reinforced Polymer (FRP) composites to steel girders, concrete decks, and pipelines, significantly extending service life and structural capacity.

These high-performance adhesives deliver exceptional tensile strength, chemical resistance, and weather durability, making them ideal for bridges, tunnels, and offshore platforms. Additionally, the integration of Structural Health Monitoring (SHM) sensors directly onto bonded structures requires stable, long-life adhesive systems that maintain integrity under thermal cycling and environmental exposure for decades.

With global infrastructure repair demand rising and governments prioritizing sustainable construction materials, the use of structural metal bonding adhesives in retrofitting and reinforcement applications represents a rapidly expanding and technically advanced segment of the market. Manufacturers who develop corrosion-resistant, fatigue-proof adhesive formulations are positioned to benefit from the wave of infrastructure modernization and safety-driven maintenance.

Metal Bonding Adhesives Market Share Insights, 2025-2034

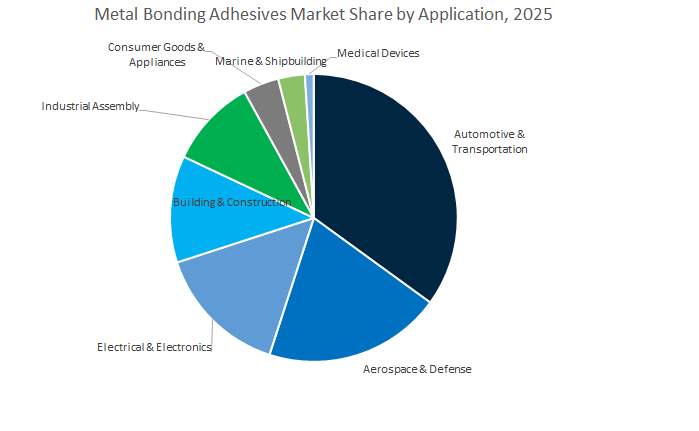

Market Share by Application

The automotive and transportation segment dominates the global metal bonding adhesives market, accounting for a projected 37.5% share in 2025, driven by the automotive industry’s transition toward lightweight, mixed-material vehicle design. Adhesives are integral to bonding aluminum, steel, and composite substrates in critical vehicle assemblies such as body-in-white structures, closure panels, chassis, and battery enclosures. The replacement of traditional welding and riveting methods with structural epoxy and polyurethane adhesives offers key advantages including weight reduction, improved crash energy absorption, and enhanced corrosion resistance, aligning with global fuel efficiency and electric vehicle (EV) mandates. The segment’s dominance is reinforced by major automakers adopting automation-compatible, heat-resistant adhesive formulations optimized for e-coat and paint bake cycles.

The aerospace and defense industry represents a high-value segment, characterized by demand for high-strength, fatigue-resistant adhesives used in composite-to-metal bonding, honeycomb panel assembly, and primary structural repairs. Adhesive systems in this segment must meet stringent performance and certification standards under extreme temperature, vibration, and chemical exposure conditions. Similarly, the electrical and electronics sector is witnessing robust growth, driven by miniaturization trends and the need for thermal management, encapsulation, and conductive bonding solutions in power systems and printed circuit boards. Building and construction, along with industrial assembly, continue to provide substantial market volumes through applications in cladding, HVAC systems, and heavy equipment manufacturing, where epoxy and acrylic-based metal bonding adhesives ensure durability and weather resistance.

Market Share by Technology/Formulation

The reactive adhesives segment leads the global metal bonding adhesives market, projected to hold 46.9% of the share in 2025, owing to its unmatched combination of mechanical strength, environmental durability, and adhesion versatility. Reactive systems—including epoxies, acrylics, and polyurethanes—dominate structural bonding applications across automotive, aerospace, and heavy machinery manufacturing. These adhesives form chemical crosslinks during curing, delivering exceptional resistance to thermal shock, vibration, and corrosion, making them ideal for high-load and fatigue-prone assemblies. With the continued shift toward lightweight vehicles and composite-metal hybrid assemblies, reactive adhesives are increasingly being formulated with enhanced thermal conductivity, faster curing cycles, and compatibility with automated dispensing systems.

Water-based adhesives maintain a strong position, supported by regulatory pressures to reduce VOC emissions and the industry’s growing preference for eco-friendly manufacturing processes. These formulations are favored in non-structural metal bonding applications, such as surface lamination, coatings, and assembly lines, particularly in regions enforcing strict EPA and REACH compliance. Hot-melt adhesives are gaining traction for their fast processing speeds, immediate bond strength, and recyclability, especially in automotive trim and consumer appliance assembly. Meanwhile, film and tape adhesives are expanding in aerospace, electronics, and industrial sectors for precisely controlled bondline thickness and uniform stress distribution, crucial in composite lamination and surface finishing.

The metal bonding adhesives market is moderately consolidated, led by Henkel, 3M, H.B. Fuller, Sika, Arkema (Bostik), and Dow Chemical Company, all of which emphasize R&D-driven differentiation. Competitive success depends on technological innovation, sustainability adaptation, and integration within OEM and Tier 1 manufacturing ecosystems. These players dominate through diversified product portfolios, regional expansion, and active partnerships with automotive, aerospace, and industrial manufacturers.

Henkel remains the global leader in structural metal bonding adhesives, leveraging its Loctite and Technomelt brands. The company’s expertise in epoxy and acrylic systems supports crash-durable automotive applications and high-reliability industrial assemblies. In February 2025, Henkel launched its medical-grade cyanoacrylate adhesives, further extending its innovation footprint into healthcare. The company’s strategic focus centers on electrification trends, particularly EV battery bonding, underpinned by a strong global OEM integration network and automated application capabilities.

3M continues to advance acrylic and epoxy adhesive technologies with a focus on difficult-to-bond metals like stainless steel and aluminum. Its latest R&D investments target adhesion promoters and pre-treatment solutions to enhance reliability in aerospace-grade joints. As a key supplier to the aerospace and defense industries, 3M’s solutions offer exceptional fatigue and environmental resistance. The company also emphasizes customizable adhesive film formats, facilitating lightweight and multi-material design flexibility for modern manufacturing.

H.B. Fuller has strengthened its market presence with bio-based polyurethane and epoxy innovations aligned with regulatory expectations in Europe and North America. Its deep expertise in custom formulations makes it a preferred partner in industrial equipment, renewable energy, and construction applications. The company’s late 2024 launch of low-VOC adhesive chemistries positioned it as a frontrunner in sustainable bonding, while its regional expansion strategies target emerging manufacturing hubs in Asia and Latin America.

Sika AG maintains a stronghold in construction and automotive structural bonding. The company has prioritized high-performance polyurethane and epoxy systems for bonding steel and metal elements in infrastructure modernization projects. With a growing presence in automotive aftermarket and chassis bonding, Sika continues to emphasize system integration, offering adhesive materials alongside application and dispensing systems, ensuring high throughput for large-scale industrial users.

Under the Bostik brand, Arkema has refined Methyl Methacrylate (MMA) and hybrid epoxy-acrylic adhesives for rapid-setting and high-strength applications. Its focus on the electronics and consumer appliance industries positions it at the forefront of miniaturized and thermally demanding applications. The company’s strategic emphasis on R&D collaboration across its global network enhances its ability to develop next-generation adhesives that merge high performance with process speed—an essential requirement for automated assembly lines.

Dow Chemical has deep expertise in epoxy and polyurethane adhesive technologies, catering to aerospace, defense, and electric vehicle sectors. In 2024, Dow expanded its R&D investment to improve thermal and fatigue resistance in adhesive lines used for EV battery modules and high-heat industrial applications. Its strategy revolves around simulation-driven product development, enabling precise prediction of joint performance and long-term durability—critical in high-stress environments such as aerospace and defense.

Country Analysis: Global Metal Bonding Adhesives Industry

China: Dominance in EV Manufacturing Drives High-Strength Metal Adhesive Demand

China is a global powerhouse in electric vehicle (EV) battery pack assembly, construction, and general industrial applications—all major demand centers for high-performance metal bonding adhesives. Multinational adhesive giants are rapidly expanding their production and R&D capacity in China to meet the surging requirements of the EV and electronics supply chain, particularly for battery module-to-pack bonding and thermal interface management.

Domestic adhesive manufacturers are also prioritizing R&D into next-generation conductive and thermally stable epoxy and polyurethane formulations designed for power electronics and energy storage systems. The government’s ongoing urbanization and infrastructure projects, coupled with the Made in China 2025 initiative, are sustaining demand for industrial-grade metal adhesives used in railways, bridges, and construction machinery.

With VOC reduction policies and stricter environmental oversight, the Chinese market is transitioning toward solvent-free, high-solids adhesives, while AI-integrated smart factories enhance local production of advanced reactive bonding agents tailored for metal-to-metal and composite-metal joints.

United States: Aerospace and Additive Manufacturing Fuel Structural Adhesive Innovation

The United States continues to lead in high-performance metal bonding adhesive applications across aerospace, defense, and automotive sectors, emphasizing multi-material joining and durability. Aerospace manufacturers increasingly employ epoxy and methacrylate (MMA) adhesives for bonding aluminum and composite structures, ensuring lightweight strength and crash resistance in critical applications.

Recent investments in additive manufacturing (3D printing) have opened a new niche for heat-resistant, post-process compatible metal adhesives, enabling precision bonding in complex metallic geometries. Concurrently, the Department of Defense (DoD) and NASA-backed initiatives are driving qualification programs for high-temperature epoxy and hybrid adhesives suitable for extreme environments, including hypersonic and defense-grade systems.

Domestic adhesive producers are also responding to supply chain resilience goals under the Biden Administration’s manufacturing policies, securing domestic sourcing for epoxy resins, curing agents, and reactive systems. Furthermore, the booming EV sector and renewable energy infrastructure projects are catalyzing the use of low-VOC and bio-based structural adhesives, positioning the U.S. as a global benchmark in advanced adhesive engineering for metallic substrates.

Germany: Advancing Automated and Lightweight Bonding Solutions for E-Mobility

Germany stands at the forefront of automotive electrification and industrial automation, fueling its dominance in high-performance metal bonding adhesives. The government’s “Lightweighting Initiative” underpins extensive collaboration between Tier 1 suppliers, OEMs, and adhesive manufacturers, fostering the creation of bi-component polyurethane (PU) and epoxy adhesives that enable rapid curing and automated body-in-white (BIW) assembly.

German automotive manufacturers such as Volkswagen, BMW, and Mercedes-Benz are adopting hybrid metal-to-composite bonding systems to reduce vehicle weight while improving crash durability and corrosion resistance. The technological shift aligns with Industry 4.0 principles, incorporating robotic dispensing systems and real-time adhesive performance monitoring within production lines.

Additionally, silicone and silane-modified adhesives are gaining prominence for industrial machinery, HVAC, and renewable energy components, providing long-term flexibility and vibration damping. Germany’s emphasis on sustainability, precision engineering, and REACH-compliant chemical formulations reinforces its position as a European innovation hub for advanced metal bonding adhesives that meet both structural and environmental performance criteria.

India: Government-Led Manufacturing Expansion Fuels Adhesive Market Growth

India’s rapidly industrializing economy and government-backed infrastructure programs are propelling strong growth in the metal bonding adhesives market, particularly across transportation, construction, and automotive manufacturing. The Production Linked Incentive (PLI) Scheme for Automobiles and Auto Components, with a financial outlay of ₹25,938 crore, is catalyzing investments in Advanced Automotive Technology (AAT), including lightweight vehicle manufacturing that relies heavily on structural metal adhesives.

As India scales up its railway, bridge, and metro rail networks, the demand for high-durability, weather-resistant polyurethane and epoxy adhesives is increasing across civil engineering and heavy infrastructure projects. Global adhesive leaders such as Henkel, Sika, and H.B. Fuller have established or expanded local R&D and technical centers to address India’s high-temperature, high-humidity environmental conditions, developing customized metal bonding formulations for local use.

The nation’s focus on ‘Make in India’ manufacturing self-reliance, coupled with rising foreign direct investment (FDI) in automotive and industrial sectors, positions India as a strategic growth market for structural metal bonding adhesives with an emphasis on cost efficiency, sustainability, and global export compliance.

Japan: Innovation in Thermally Conductive and Miniaturized Adhesive Technologies

Japan’s metal bonding adhesives market is driven by precision manufacturing in automotive, electronics, and semiconductor packaging industries, emphasizing miniaturization and high thermal conductivity. Japanese materials science companies like Nitto Denko and Toray Industries are developing ultra-thin pressure-sensitive adhesives (PSAs) and conductive epoxies optimized for thermal management in compact electronic devices.

Ongoing academic R&D collaborations focus on hybrid bio-based and solvent-free adhesive chemistries, responding to stringent VOC and environmental safety regulations. The automotive sector continues to adopt toughened epoxy and hybrid adhesive systems offering high fatigue resistance under cyclical mechanical loads—critical for electric powertrains and advanced lightweight vehicle structures.

Japan’s manufacturing excellence in precision robotics, optics, and medical devices further drives the use of high-flexibility, low-shrink epoxy adhesives, ensuring reliability and long-term performance in metallic assemblies exposed to both vibration and thermal cycling. The technological depth cements Japan’s role as a global leader in advanced adhesive solutions for electronics and high-value manufacturing.

South Korea: Electrification and Consumer Electronics Driving Metal Bonding Adhesive Growth

South Korea’s metal bonding adhesive market is expanding rapidly on the back of its electric vehicle (EV) battery manufacturing and consumer electronics sectors. Automotive OEMs are aggressively replacing traditional spot welding with structural adhesives in body-in-white (BIW) applications, improving crash energy absorption, NVH performance, and corrosion protection for next-generation EV platforms.

In parallel, South Korea’s dominance in smartphone, display, and semiconductor production drives massive demand for fast-curing cyanoacrylate and UV-curable metal adhesives used in micro-assembly of sensors, frames, and connectors. Adhesive suppliers are forming strategic partnerships with consumer electronics giants such as Samsung and LG to deliver high-temperature-resistant, non-yellowing bonding solutions compatible with miniaturized devices.

Additionally, white goods manufacturers are increasingly incorporating PU and hybrid adhesives in appliance assembly to enhance design flexibility and manufacturing throughput. With continued government incentives for green mobility and digital infrastructure, South Korea is set to remain a high-value market for technologically advanced metal bonding adhesives, particularly in EV, electronics, and appliance manufacturing ecosystems.

Metal Bonding Adhesives Market Report Scope

Metal Bonding Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$11.8 Billion

|

|

Market Size (2034)

|

$18.5 Billion

|

|

Market Growth Rate

|

5.1%

|

|

Segments

|

By Resin Type (Epoxy-Based, Acrylic-Based, Polyurethane-Based, Silicone-Based, Cyanoacrylate, Modified Phenolic Resin, Hybrid and Specialty), By Application (Automotive & Transportation, Aerospace & Defense, Electrical & Electronics, Building & Construction, Industrial Assembly, Marine & Shipbuilding, Consumer Goods & Appliances, Medical Devices), By Technology (Reactive Adhesives, Water-Based, Solvent-Based, Hot-Melt, Film/Tape

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, 3M Company, H.B. Fuller Company, Sika AG, Arkema Group (Bostik), The Dow Chemical Company, Huntsman Corporation, LORD Corporation (Parker Hannifin), BASF SE, Dymax Corporation, Permabond LLC, Ashland Global Holdings Inc., DuPont de Nemours, Inc., Evonik Industries AG, Jowat SE

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Resin Type

- Epoxy-Based

- Acrylic-Based

- Polyurethane-Based

- Silicone-Based

- Cyanoacrylate

- Modified Phenolic Resin

- Hybrid and Specialty

By Application/End-Use Industry

- Automotive & Transportation

- Aerospace & Defense

- Electrical & Electronics

- Building & Construction

- Industrial Assembly

- Marine & Shipbuilding

- Consumer Goods & Appliances

- Medical Devices

By Technology/Formulation

- Reactive Adhesives

- Water-Based

- Solvent-Based

- Hot-Melt

- Film/Tape

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Metal Bonding Adhesives Market

- Henkel AG & Co. KGaA

- 3M Company

- H.B. Fuller Company

- Sika AG

- Arkema Group (Bostik)

- The Dow Chemical Company

- Huntsman Corporation

- LORD Corporation (Parker Hannifin)

- BASF SE

- Dymax Corporation

- Permabond LLC

- Ashland Global Holdings Inc.

- DuPont de Nemours, Inc.

- Evonik Industries AG

- Jowat SE

*- List not Exhaustive

Research Coverage

USDAnalytics delivers an executive-grade view of the Global Metal Bonding Adhesives Market, where this report investigates the migration from mechanical fastening to structural bonding as OEMs pursue lightweight, crash-durable, and automation-ready assemblies; our expert analysis reviews demand inflections across automotive, aerospace, electronics, construction, and industrial equipment as epoxies, polyurethanes, and acrylics set new performance baselines in strength, toughness, and thermal stability; it curates breakthroughs in dual-cure/toughened acrylic systems, low-temperature-cure epoxies for EV battery and electronics thermal protection, and bio-based/low-VOC platforms aligned to evolving EU/NA regulations; and highlights how process speed, mixed-material compatibility, and sustainability credentials are redefining specifications and total cost of ownership across global manufacturing lines—making this report an essential resource for product, sourcing, manufacturing, and engineering leaders planning next-gen metal joining strategies.

Scope Highlights

Segmentation (covered in this study):

- By Resin Type: Epoxy-Based; Acrylic-Based; Polyurethane-Based; Silicone-Based; Cyanoacrylate; Modified Phenolic Resin; Hybrid & Specialty

- By Application/End-Use Industry: Automotive & Transportation; Aerospace & Defense; Electrical & Electronics; Building & Construction; Industrial Assembly; Marine & Shipbuilding; Consumer Goods & Appliances; Medical Devices

- By Technology/Formulation: Reactive Adhesives; Water-Based; Solvent-Based; Hot-Melt; Film/Tape

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Timeframe: Historic data 2021–2024 and forecast data 2025–2034.

Companies: Analysis/profiles of 15+ companies, including Henkel; 3M; H.B. Fuller; Sika; Arkema (Bostik); Dow; Huntsman; LORD (Parker Hannifin); BASF; Dymax; Permabond; Ashland; DuPont; Evonik; Jowat.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.