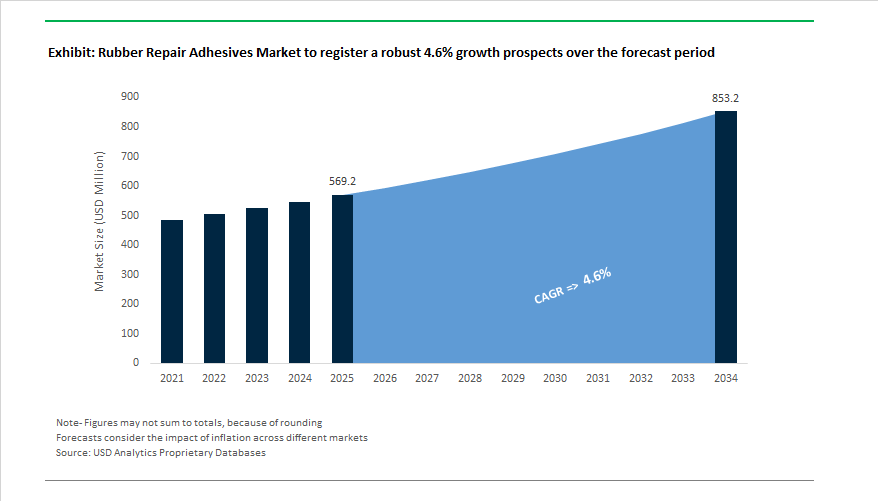

The Global Rubber Repair Adhesives Market is projected to grow from $569.2 million in 2025 to $853.2 million by 2034, registering a CAGR of 4.6%. The market is anchored in industries such as mining, material handling, automotive, and power generation, where rubber-based systems (belts, linings, seals, and hoses) form the backbone of operational infrastructure. These adhesives are indispensable for extending the service life of critical components by enabling rapid, durable, and cost-effective repairs that reduce downtime and optimize productivity.

In the industrial MRO (Maintenance, Repair, and Operations) segment, cold bond adhesives are emerging as the dominant solution. These adhesives allow faster repairs without the need for heat curing, reducing equipment downtime and enhancing safety in field conditions. Simultaneously, the push for sustainable adhesive chemistry—particularly low-VOC and solvent-free systems—is reshaping the market landscape. Major European producers report up to 40% CO₂ emission reductions in adhesive production over the last two years, aligning with the broader shift toward green industrial chemicals and compliance with EU and U.S. environmental mandates.

A crucial demand driver lies in the mining sector, where conveyor belts and processing equipment face continuous wear from abrasive materials. The Mining and Quarrying segment is expected to increase spending on rubber repair kits, cements, and patch compounds, primarily to combat wear-induced losses in mineral extraction and logistics. Meanwhile, high-heat and high-friction environments—notably in tire retreading and heavy-duty manufacturing—are sustaining demand for neoprene-based adhesives that maintain integrity under temperatures up to 300°F (148°C).

At the regional level, Asia-Pacific dominates production, supported by expanding industrial bases in China, India, and Indonesia, where rapid industrialization fuels the need for quick-bonding rubber repair materials in mining and infrastructure sectors. In contrast, North America and Europe are seeing strong adoption of eco-friendly formulations compliant with OSHA, REACH, and VOC emission standards, creating a two-tiered global demand dynamic between sustainability and performance-driven markets.

The rubber repair adhesives industry is undergoing a technological and strategic transformation, driven by innovation, sustainability, and supply chain consolidation. Major global players are increasingly integrating sustainable adhesive chemistry, digital monitoring systems, and localized production to meet the evolving demands of mining, automotive, and heavy industrial customers.

In July 2025, H.B. Fuller introduced its ECO2 Technology, designed initially for commercial roofing adhesives but with broad implications for industrial adhesive sustainability. By leveraging naturally occurring atmospheric gases as propellants rather than synthetic blowing agents, this innovation signals a paradigm shift toward low-GWP adhesive systems. Such technologies are being adapted for rubber repair applications, where solvent-free formulations reduce site hazards and environmental footprint.

In September 2025, Henkel AG (Loctite) reinforced its leadership in industrial bonding with its LED-curable adhesives campaign under “Bonded for Life,” showcasing innovations in high-speed precision curing—a technology that can be leveraged for rubber-to-metal and elastomeric bonding applications in MRO environments. This reflects a broader industrial trend toward faster-curing adhesives to minimize downtime in critical manufacturing and mining operations.

Meanwhile, Meridian Adhesives Group expanded aggressively with the acquisition of Bondloc UK Ltd. (December 2024), bolstering its portfolio of industrial adhesives for the European MRO sector, particularly in rubber bonding and repair systems. Following this, in January 2025, Meridian launched a unified global platform to enhance accessibility to its product portfolio, underscoring the growing importance of customer-centric digital integration in industrial adhesives markets.

A notable development came in June 2024, when a specialty chemicals manufacturer launched a two-part polyurethane elastomer repair system tailored for on-site conveyor belt maintenance. This formulation offers high abrasion resistance, rapid curing, and enhanced mechanical strength, directly addressing challenges in the mining and material handling sectors where downtime costs are critical.

The digitalization of asset management also plays a pivotal role: according to a 2025 EY global industry report, predictive maintenance and sensor-driven monitoring of rubber assets like conveyor belts could yield up to $70 billion in annual savings for the global mining sector. This evolution amplifies demand for fast-response rubber repair adhesives compatible with digital maintenance workflows.

Simultaneously, Rema Tip Top (April 2024) continues promoting REMAFIX 111, a corrosion-resistant repair paste for metallic surfaces under rubber linings, used in chemical and mining industries. This innovation reflects the growing need for corrosion and abrasion-resistant adhesive systems capable of restoring mechanical integrity in high-stress environments.

Market Trend 1: Advancement in Fast-Curing and Low-Temperature Rubber Repair Adhesives for Extreme Conditions

The market is witnessing an accelerated shift toward fast-curing rubber repair adhesives designed to operate under cold-weather, underwater, and high-humidity conditions, particularly in offshore energy, marine shipping, and cold-region mining. Traditional vulcanization systems required elevated temperatures—often 120°C to 220°C—and multi-day cure cycles, creating costly maintenance downtime.

Recent chemical breakthroughs in low-temperature vulcanization accelerators are transforming these performance constraints. Emerging ultra-fast accelerators enable rubber compound curing at temperatures as low as 70°C within 20 to 60 minutes, vastly improving repair cycle times for critical components such as conveyor belts, seals, and flexible joints. Studies focusing on cold-curing epoxy adhesive analogs confirm similar advancements—achieving structural-grade mechanical properties with curing times reduced from days to a few hours at 5°C–10°C.

The innovation directly addresses the operational realities of industries where repairs must occur without removing equipment from service or without heat-assisted curing. For example, subsea and offshore platforms utilize two-component polyurethane-based cold-curing rubber adhesives that adhere to wet substrates and cure within hours even at low ambient temperatures. These developments underscore a growing emphasis on ambient-temperature vulcanization (ATV) and rapid-set repair systems engineered for harsh, time-sensitive environments.

Market Trend 2: Integration of Bio-Based Raw Materials and Solvent-Free Chemistries Under ESG and REACH Compliance Pressure

A defining trend in the rubber adhesives industry is the integration of sustainable and bio-based raw materials, driven by corporate ESG mandates and regulatory frameworks such as the EU REACH Regulation and U.S. EPA HAPs standards. The pressure to decarbonize industrial maintenance, repair, and operations (MRO) supply chains is catalyzing a shift from traditional petroleum-based, solvent-heavy adhesives to bio-circular and solvent-free alternatives.

Leading adhesive manufacturers are incorporating renewable feedstocks such as castor oil derivatives and starch-based polyols, achieving up to 60% bio-based content in select industrial repair adhesives. A major global producer, for example, confirmed the application of its bio-based polyurethane adhesive line—originally designed for consumer-grade repair—into its industrial MRO product range, targeting carbon footprint reduction while maintaining performance parity with conventional materials.

In addition, REACH and global chemical safety initiatives continue to restrict or phase out over 200 conventional substances, directly impacting legacy rubber adhesive formulations. The regulatory momentum is forcing formulators to adopt low-VOC, non-hazardous, and isocyanate-free chemistries to ensure supply chain continuity and sustainability alignment.

Market Opportunity 1: Development of Conductive and Static-Dissipative Rubber Repair Adhesives for Electronics Manufacturing

The convergence of automation and precision electronics manufacturing presents a lucrative growth opportunity for conductive and static-dissipative rubber repair adhesives, vital for maintaining electrostatic discharge (ESD) control and electrical continuity in cleanroom and semiconductor production environments.

Specialized silver- or carbon-filled conductive epoxy systems used for rubber repairs exhibit ultra-low volume resistivity (<0.001 Ω·cm), ensuring effective restoration of conductive rubber components such as conveyor belts, ESD mats, and roller surfaces. The capability is critical for preventing static buildup that can damage sensitive microchips or disrupt automated equipment calibration.

Leading manufacturers are also investing in next-generation functional filler technologies, combining silver, nickel, and carbon nanotube (CNT) materials to enhance conductivity while maintaining flexibility and mechanical resilience. These materials are being tailored for low-temperature and fast-curing formulations, allowing for rapid repairs without thermal degradation of adjacent components.

Additionally, the rise of sensor-integrated rubber components in advanced assembly lines is driving demand for adhesives that enable seamless electronics-to-elastomer integration. These specialized adhesives ensure mechanical bonding and electrical conduction without compromising elasticity, marking a key enabler for smart manufacturing and Industry 4.0 infrastructure.

Market Opportunity 2: Ceramic-Filled Adhesives Enabling Abrasion-Resistant Rubber Repairs in Mining and Mineral Processing

The mining and mineral processing sectors represent one of the most profitable and performance-critical application areas for ceramic-filled rubber repair adhesives, which are engineered to withstand abrasion, impact, and chemical exposure in extreme industrial environments.

Mining operations face continuous wear on rubber-based components such as slurry discharge elbows, pump liners, conveyor belts, and hydrocyclones, where downtime can lead to revenue losses exceeding tens of thousands of dollars per hour. In response, manufacturers are deploying two-component, ceramic bead-filled epoxy systems offering up to 4X greater abrasion resistance compared to standard polyurethane or rubber-based repair products.

Additionally, certain advanced formulations demonstrate 7X higher drop impact strength than traditional ceramic tile liners, making them ideal for dynamic systems subjected to high particle velocity and impact stress. The latest generation of these adhesives cures within 2–3 hours, enabling rapid equipment return to service—a crucial advantage in continuous mining operations.

The ongoing adoption of these high-performance repair solutions aligns with the mining sector’s focus on total lifecycle cost reduction and predictive maintenance, reducing the frequency of component replacement and extending operational uptime. The ability to engineer ceramic-reinforced elastomeric matrices for hybrid mechanical and chemical resistance positions these adhesives as essential for sustainable mining MRO strategies.

Rubber Repair Adhesives Market Share Insights, 2025-2034

Market Share by Type/Chemistry

Polyurethane-based rubber repair adhesives dominate the global market, accounting for an estimated 24.9% share in 2025, owing to their exceptional elasticity, impact resistance, and chemical compatibility with diverse rubber materials. These adhesives are the industry standard for conveyor belt splicing, patching, and high-wear rubber component repair, where durability under dynamic loading and harsh environments is critical. Their ability to bond effectively to both natural and synthetic rubbers, combined with resistance to oils, abrasion, and vibration, makes PU formulations indispensable in sectors such as mining, construction, and automotive maintenance. Furthermore, advancements in moisture-curing and two-component PU systems have enhanced workability and curing control, improving on-site repair efficiency for industrial maintenance teams.

Epoxy-based and acrylic-based adhesives follow closely, securing substantial shares due to their high tensile strength, excellent adhesion to metal-reinforced rubber composites, and long-term environmental resistance. Epoxy systems are favored in industrial hose, gasket, and rubber-metal joint repair, particularly where structural integrity and chemical resistance are vital. Meanwhile, acrylic and methyl methacrylate (MMA) adhesives are gaining popularity in quick-repair applications where rapid curing and high impact resistance are required. Cyanoacrylate-based adhesives occupy a niche yet growing market, particularly for emergency and small-scale rubber repairs, where instant bonding and minimal surface preparation are valued. Silyl-Modified Polymers (SMPs) are emerging as hybrid technologies combining elasticity with weather resistance, suitable for outdoor or flexible joint repairs. Neoprene, silicone, and natural rubber-based adhesives maintain specialized roles where compatibility with specific rubber formulations or thermal resistance is essential, such as in marine, HVAC, and gasket sealing applications.

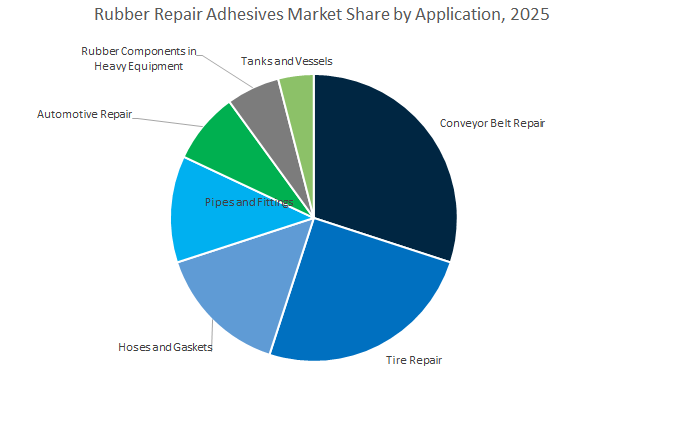

Market Share by Application

Conveyor Belt Repair is the leading application, capturing approximately 32.6% of the global rubber repair adhesives market in 2025, driven by the massive installed base of conveyor systems across mining, cement, power generation, and manufacturing industries. These belts experience constant mechanical stress, abrasion, and environmental exposure, necessitating frequent repair and splicing operations. Rubber repair adhesives, particularly polyurethane and epoxy formulations, are preferred for their high peel strength, flexibility, and ability to withstand dynamic loads and thermal cycling. The rise in automation and predictive maintenance practices has increased the use of fast-curing and sprayable adhesives, reducing downtime and enhancing operational efficiency. The dominance of this segment underscores the critical role of reliable adhesive bonding in maintaining material handling infrastructure globally.

The Tire Repair segment maintains strong momentum, supported by the global automotive and transportation industries where both passenger and commercial vehicle tires require periodic repair and retreading. Rubber repair adhesives are integral in patching, tread bonding, and vulcanization applications, where strong adhesion under high temperature and pressure conditions is crucial. Hoses, gaskets, and piping repairs represent another significant area, especially within industrial plants and fluid transport systems, where adhesives provide long-lasting seals and resistance to chemicals, oils, and thermal expansion. Automotive and heavy equipment repair applications are also expanding due to the growing need for bonding weather seals, mounts, and vibration isolators, contributing to improved noise and vibration control. Tank and vessel repair, though smaller in market size, serves critical containment applications in chemical processing, oil & gas, and marine sectors, where high chemical resistance and adhesion to elastomer linings are required.

The global competitive landscape is dominated by multinational players integrating sustainability, advanced polymer chemistry, and digital asset management into their product strategies. Companies such as Rema Tip Top AG, Henkel AG & Co. KGaA, 3M Company, ELANTAS (ALTANA), and Trelleborg AB are setting new benchmarks through green chemistry initiatives, high-temperature bonding technologies, and service-based maintenance solutions for industrial customers.

Rema Tip Top AG (REMA) remains the leading specialist in rubber repair systems and tire retreading, with a vast global network of over 150 subsidiaries and service centers. Its REMABOND Adhesive Systems are engineered for extreme industrial stress, providing solvent-based and solvent-free cements that deliver superior adhesion for rubber splicing and patching. The company reported a 40% reduction in CO₂ emissions at its adhesive manufacturing facilities in 2024, underscoring its commitment to sustainable operations. Its ESKANOL VE-L SF resin technology introduces a styrene- and solvent-free vinyl ester laminate offering enhanced chemical resistance for corrosive environments. Further, Rema Tip Top is integrating predictive maintenance tools into its service offerings, positioning itself as a digitalized MRO partner for global mining clients.

Henkel’s Loctite brand continues to dominate the industrial repair adhesives market, renowned for its durability and fast-curing performance. Its rubber and belt repair kits feature self-leveling, flexible compounds designed for rapid maintenance of conveyor systems. Henkel’s integration of digital dispensing solutions and technical support services enhances user precision and efficiency. Under its “Bonded for Life” campaign (September 2025), Henkel showcased LED-curable systems and next-generation hybrid adhesives targeting industrial and mobility sectors. The company’s strategy emphasizes Mines & Quarries and Power Generation, reducing mechanical failures in heavy equipment, while its ongoing investments in eMobility adhesives expand its reach into next-generation polymer bonding.

3M’s Industrial Adhesives & Tapes Division offers one of the most diverse portfolios for rubber bonding and repair applications, led by the 3M™ Neoprene High-Performance Adhesive 1300—a benchmark product offering instant bonding strength, moisture resistance, and heat durability up to 300°F (148°C). Widely used for rubber sheeting, gasket repair, and industrial sealing, 3M’s products are available in brushable, spray, and flowable forms, ensuring application flexibility. Many of its rubber adhesive products contribute toward LEED® certification and comply with CARB and REACH regulations, reinforcing 3M’s commitment to environmental compliance and low-emission adhesive systems for industrial users worldwide.

ELANTAS, part of ALTANA AG, focuses on protective materials and electrical insulation systems with overlap in rubber-based repair compounds and protective coatings. In May 2024, the company announced a CHF 12.5 million investment to convert its Breitenbach site (Switzerland) into a sustainable technology hub focused on high-voltage insulation materials and eMobility protection solutions. Following its 2023 acquisition of Von Roll Holding AG, ELANTAS significantly expanded its expertise in rubber-polymer insulation and repair technologies. Its R&D expenditure continues to rise annually, underlining its commitment to next-generation elastomeric and polymer adhesives for harsh environmental conditions.

Trelleborg AB, a global leader in engineered polymer solutions, leverages its internal and external expertise in rubber bonding and repair adhesives for mining, offshore, and industrial applications. The company’s high-performance rubber sheeting (ARMURITE®, BLACKROCK+) requires specialized repair adhesives to maintain durability under abrasion, impact, and chemical exposure. Trelleborg’s focus on proactive maintenance, onsite condition monitoring, and emergency repair support has positioned it as a system-level solution provider rather than a product supplier. Its adhesive systems are designed for EPDM, NBR, and NR/SBR rubbers, maintaining reliable performance even in high-load and vibration-intensive environments.

Country Analysis: Regional Growth Dynamics and Innovation in the Global Rubber Repair Adhesives Industry

United States: Infrastructure Investments and Technological Innovation in Industrial Rubber Adhesives

The United States rubber repair adhesives market is experiencing strong momentum, driven by massive infrastructure upgrades, industrial maintenance, and sustainability-focused innovation. The Infrastructure Investment and Jobs Act (IIJA)—allocating more than $550 billion for modernization projects—is significantly boosting the use of industrial-grade rubber adhesives in bridge construction, transportation systems, and structural sealing applications. The adhesives play a vital role in the maintenance of expansion joints, vibration dampers, and structural rubber components used across public works and private sector industries.

Technological advancements are transforming the market landscape, with more than 20 major investment announcements in 2024 alone focused on developing solvent-free and low-VOC rubber adhesive formulations. The shift aligns with EPA emission compliance and the nation’s increasing adoption of sustainable polymer technologies. Heavy industries, especially mining and aggregate operations, rely heavily on two-part polyurethane (PU) and epoxy-based repair systems for conveyor belts, enabling rapid on-site restoration that reduces downtime.

Furthermore, the automotive aftermarket, with an estimated 280 million registered vehicles, remains a major end-use segment. Demand for high-strength bonding agents and flexible sealants in engine mounts, weather seals, and bushings is accelerating. The defense and aerospace sectors also represent niche but growing markets, utilizing rubber-to-metal bonding compounds for high-stress, high-temperature repairs in aircraft systems. The combination of infrastructure funding and next-generation chemistry innovation ensures the U.S. retains its dominance as a high-value market for industrial rubber repair adhesives.

China: Expanding Industrial Base and Sustainable Adhesive Transition

China remains the largest global producer and consumer of rubber repair adhesives, underpinned by its manufacturing leadership, massive construction investments, and environmental regulation upgrades. The nation produces over 40% of global resorcinol-based rubber bonding systems, with industrial expansion in Tier-2 and Tier-3 cities fueling steady consumption across factory maintenance, materials handling, and transport infrastructure.

China’s mining and materials handling industries, utilizing extensive conveyor systems for coal, iron ore, and cement, accounted for roughly 17 million kilograms of rubber repair adhesive consumption in 2024. Major state-backed industrial projects continue to rely on polyurethane and epoxy bonding agents for conveyor and rubber component repair. Additionally, the government's New Energy Vehicle (NEV) initiative is driving the adoption of lightweight structural adhesives that enhance bonding strength while reducing vehicle weight, a crucial element for EV performance and range efficiency.

In line with national decarbonization goals, the country is pushing a large-scale shift toward water-based, hot-melt, and low-solvent rubber adhesive technologies to comply with stringent VOC emission standards. As major domestic manufacturers invest in localized R&D and sustainable chemical synthesis, China is positioning itself as the center of innovation and volume production for rubber repair and bonding adhesives globally.

Germany: Engineering Excellence and Sustainable Rubber Repair Systems

Germany is a global leader in advanced rubber adhesive engineering, combining its industrial automation ecosystem and sustainability-driven policy environment to pioneer premium bonding technologies. Major chemical producers in Germany are expanding capacity for hot-bond and epoxy-based rubber repair compounds, used in industrial machinery maintenance, tire re-treading, and automotive sealing applications. The high-performance formulations are designed to endure extreme dynamic stress, making them ideal for precision engineering and heavy machinery repairs.

Germany’s E-Mobility boom further strengthens market demand. The nation’s growing EV manufacturing capacity drives the adoption of specialized silicone and polyurethane (PU) sealants for rubber gaskets, cable harnesses, and high-voltage battery systems requiring thermal and vibration resistance. In addition, industrial automation is generating demand for fast-curing adhesives suitable for bonding rubber grips and elastomeric components in robotic grippers and automated assembly systems.

With strong R&D investment from European adhesive manufacturers and regulatory alignment under REACH for environmentally safe production, Germany continues to set global benchmarks for durable, sustainable, and precision-grade rubber repair adhesives.

India: Mining Modernization and Infrastructure Growth Driving Market Expansion

India’s rubber repair adhesives market is rapidly growing, supported by massive infrastructure modernization, mining automation, and domestic manufacturing initiatives. Coal India Ltd., the world’s largest coal producer, has committed INR 157 billion (approx. USD 1.9 billion) toward upgrading conveyor systems with long-distance belt transport, creating strong demand for on-site rubber repair kits and quick-curing bonding solutions.

The construction sector, contributing nearly 8% to India’s GDP, is another major growth driver, particularly through the Smart Cities Mission and National Infrastructure Pipeline (NIP). The programs encourage the use of high-strength adhesives and sealants for rubber components in heavy machinery, construction vehicles, and expansion joints. India’s manufacturing resurgence, under the ‘Make in India’ and PLI Schemes, is further stimulating domestic production of rubber compounds and elastomer adhesives, reducing import dependence.

With international and local players—such as Pidilite Industries and Atul Ltd.—expanding their specialty polymer facilities, India is emerging as a regional powerhouse for industrial rubber adhesives. Its diverse climate and industrial base demand temperature-resistant, UV-stable, and fast-curing repair adhesives, positioning the country as a key growth engine in the Asia-Pacific region.

Brazil: Mining and Agricultural Machinery Driving Elastomer Adhesive Demand

Brazil’s rubber repair adhesive demand is closely linked to its resource extraction and large-scale agricultural machinery sectors. As one of the top global producers of iron ore, bauxite, and copper, Brazil’s mining operations depend heavily on steel-cord conveyor systems, which require regular hot and cold bonding repairs using advanced two-part polyurethane and epoxy formulations. The materials enable rapid curing, enhanced abrasion resistance, and improved longevity for heavy-duty belts operating under extreme mechanical load.

In the agriculture and logistics industries, adhesive consumption is equally strong. Frequent maintenance of rubber tires, harvesters, and transport vehicles drives demand for cold vulcanization compounds and high-strength tire repair adhesives. Moreover, Brazil’s expanding port and marine infrastructure—particularly for grain and mineral export—creates significant opportunities for marine-grade rubber bonding systems, used in fenders, dock seals, and vibration dampers. The nation’s emphasis on sustainable resource utilization and maintenance efficiency positions it as a key Latin American hub for industrial elastomer adhesives and repair solutions.

Canada: Cold-Weather Performance and Resource Sector Maintenance Solutions

Canada’s rubber repair adhesives market is defined by its extreme environmental conditions and high dependence on resource-based industries. The nation’s vast mining and oil sands operations demand chemical-resistant, temperature-tolerant, and fast-curing elastomer adhesives for maintaining and extending the life of critical rubber components, such as conveyor belts, liners, and hoses.

With Canada ranking among the top five global producers of 13 major minerals, consistent mining operations create a steady stream of maintenance requirements. Adhesive technologies must perform under sub-zero temperatures, making two-part polyurethane and epoxy-based repair systems the preferred choice. Furthermore, Canada’s Net-Zero Emissions Plan emphasizes industrial maintenance efficiency, driving increased adoption of sustainable, long-lasting adhesive solutions that enhance operational uptime and reduce waste.

The integration of eco-friendly polymers and low-emission curing technologies across industrial maintenance practices demonstrates Canada’s commitment to innovation in cold-weather and high-durability rubber adhesive systems, securing its role as a strategic contributor to North America’s specialty adhesive landscape.

Rubber Repair Adhesives Market Report Scope

Rubber Repair Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$569.2 Million

|

|

Market Size (2034)

|

$853.2 Million

|

|

Market Growth Rate

|

4.6%

|

|

Segments

|

By Type (Polyurethane-based, Epoxy-based, Cyanoacrylate-based, Acrylic-based, Neoprene/Elastomer-based, Silicone-based, Silyl-Modified Polymer, Natural Rubber-based), By Technology (Cold Bond, Hot Bond, Air, UV, Pressure Sensitive), By Application (Conveyor Belt Repair, Tire Repair, Pipes and Fittings, Tanks and Vessels, Hoses and Gaskets, Rubber Components, Automotive Repair), By End-Use Industry (Mining & Quarrying, Cement & Aggregate, Automotive & Transportation, Construction & Infrastructure, Steel & Metal Processing, Marine & Offshore, Power Generation & Utilities), By Distribution Channel (Aftermarket/MRO, OEM

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, 3M Company, Sika AG, H.B. Fuller Company, Rema Tip Top AG, LORD Corporation (Parker Hannifin), DuPont de Nemours, Inc., ITW Performance Polymers, Huntsman Corporation, Bostik (Arkema Group), Belzona International Ltd., Permabond Engineering Adhesives, Dow Inc., Wacker Chemie AG, Evonik Industries AG

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Type/Chemistry

- Polyurethane-based

- Epoxy-based

- Cyanoacrylate-based

- Acrylic-based

- Neoprene/Elastomer-based

- Silicone-based

- Silyl-Modified Polymer

- Natural Rubber-based

By Technology/Curing

- Cold Bond

- Hot Bond

- Air

- UV

- Pressure Sensitive

By Application

- Conveyor Belt Repair

- Tire Repair

- Pipes and Fittings

- Tanks and Vessels

- Hoses and Gaskets

- Rubber Components

- Automotive Repair

By End-Use Industry

- Mining & Quarrying

- Cement & Aggregate

- Automotive & Transportation

- Construction & Infrastructure

- Steel & Metal Processing

- Marine & Offshore

- Power Generation & Utilities

By Distribution Channel

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Rubber Repair Adhesives Market

- Henkel AG & Co. KGaA

- 3M Company

- Sika AG

- H.B. Fuller Company

- Rema Tip Top AG

- LORD Corporation (Parker Hannifin)

- DuPont de Nemours, Inc.

- ITW Performance Polymers

- Huntsman Corporation

- Bostik (Arkema Group)

- Belzona International Ltd.

- Permabond Engineering Adhesives

- Dow Inc.

- Wacker Chemie AG

- Evonik Industries AG

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the evolving Rubber Repair Adhesives Market through decision-focused analysis reviews of demand across mining, material handling, automotive, marine/offshore, and utilities; it highlights breakthroughs in fast-curing cold-bond chemistries, solvent-free/low-VOC systems, and abrasion-resistant ceramic-filled repairs that cut downtime and extend asset life; mapping regulatory shifts (REACH, OSHA, VOC/HAPs limits), digital MRO adoption, and competitive moves in polyurethane, neoprene, epoxy, and hybrid SMP technologies, we benchmark performance, total installed cost, and reliability under heat, impact, and chemicals—this report is an essential resource for operations leaders, maintenance engineers, and procurement teams seeking lifecycle gains and sustainability alignment.

Scope Highlights

Segmentation:

- By Type/Chemistry: Polyurethane-based; Epoxy-based; Cyanoacrylate-based; Acrylic-based; Neoprene/Elastomer-based; Silicone-based; Silyl-Modified Polymer; Natural Rubber-based.

- By Technology/Curing: Cold Bond; Hot Bond; Air; UV; Pressure Sensitive.

- By Application: Conveyor Belt Repair; Tire Repair; Pipes and Fittings; Tanks and Vessels; Hoses and Gaskets; Rubber Components; Automotive Repair.

- By End-Use Industry: Mining & Quarrying; Cement & Aggregate; Automotive & Transportation; Construction & Infrastructure; Steel & Metal Processing; Marine & Offshore; Power Generation & Utilities.

- By Distribution Channel: Aftermarket/MRO; OEM.

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa).

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Horizon: Historic data 2021–2024 and forecast data 2025–2034.

Companies Covered: Analysis / profiles of 15+ companies.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.