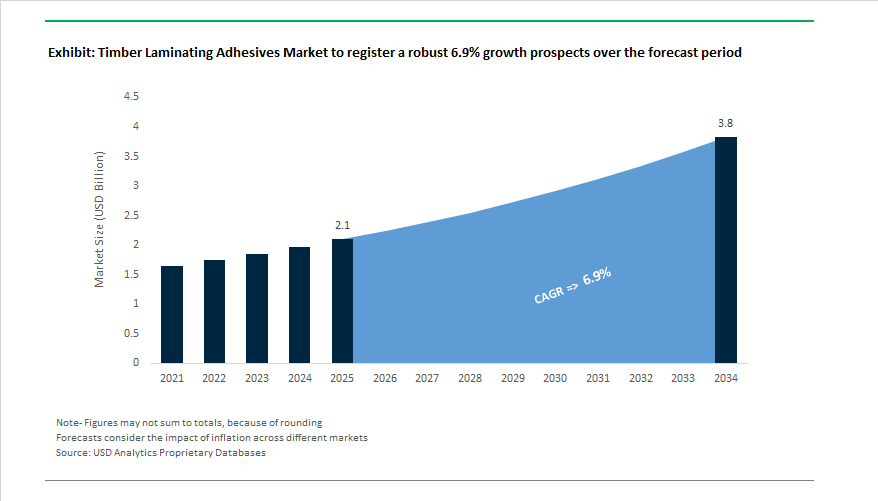

The Global Timber Laminating Adhesives Market is projected to expand from USD 2.1 billion in 2025 to USD 3.8 billion by 2034, advancing at a CAGR of 6.9%, as engineered wood transitions from a niche structural option to a mainstream alternative to steel and concrete. Growth is being driven less by incremental panel volumes and more by the system-level adoption of mass timber architectures, particularly glulam, CLT, and LVL, across mid-rise and high-rise construction.

Timber laminating adhesives are emerging as structural load-path components whose performance directly determines certification, insurance acceptance, and service life of mass timber buildings. As a result, demand is concentrating around high-reliability polyurethane (PUR), melamine-urea-formaldehyde (MUF), and emerging zero-formaldehyde systems, each selected based on structural class, exposure conditions, and fire-performance requirements. Manufacturers such as Henkel, Hexion, AkzoNobel, Sika, and Jowat have significantly re-engineered portfolios to meet EN 14080, ANSI A190.1, and PRG 320 standards that govern structural timber in Europe and North America.

A decisive structural shift is underway toward 1K and 2K PUR laminating adhesives, particularly in CLT and glulam production. These systems offer high green strength, gap-filling tolerance, and moisture resistance while eliminating formaldehyde emissions—a critical requirement as builders align with EPD declarations, LEED, BREEAM, and regional embodied-carbon regulations. Several leading PUR systems now deliver press times under 60 minutes at ambient conditions, materially improving press utilization and throughput for industrial timber fabricators.

At the same time, zero-added-formaldehyde (ZAF) technologies are moving from pilot to commercial scale. Bio-modified MUF systems, lignin-enhanced resins, and hybrid PUR formulations are being introduced to balance structural performance, fire behavior, and long-term creep resistance, particularly for large-span beams and load-critical elements. This transition is being accelerated by public procurement rules in Europe and North America, where formaldehyde emissions and lifecycle carbon accounting increasingly influence material approval.

Key Industry Insights

- Structural growth linkage: The Glulam market directly supports timber adhesive demand, driven by the surge in mass timber construction and sustainable architecture.

- Green chemistry transition: Rapid move toward zero-formaldehyde, low-VOC polyurethane adhesives, aligning with EU Green Building certification and Ecodesign regulations.

- Construction macro tailwind: Global construction spending surpassing USD 11 trillion annually, about 13% of global GDP, ensures multi-year adhesive demand stability.

- Supply chain sensitivity: Isocyanate price volatility remains a cost risk; manufacturers are emphasizing supply diversification and long-term sourcing agreements.

- High-demand applications: Window and door headers remain a top revenue contributor, requiring moisture- and heat-resistant adhesive systems capable of maintaining mechanical stability under thermal cycling.

The timber laminating adhesives market is evolving rapidly, marked by strategic realignments, sustainability investments, and product innovations focused on low-emission polyurethane systems and high-performance engineered bonding. In March 2025, Henkel AG & Co. KGaA reported a 2.4% organic sales growth in its Adhesive Technologies business for FY2024, underscoring the growing profitability of engineered wood adhesives within its high-margin construction portfolio. Around the same time, Henkel’s LOCTITE® HB X PUR adhesive—designed for enhanced fire resistance (60+ minutes) in CLT and Glulam structures—was spotlighted as a next-generation solution meeting European fire classification standards.

H.B. Fuller continued its operational optimization in January 2025, finalizing a plan to enhance cost efficiency across its supply chain, particularly targeting the structural wood adhesives portfolio. This streamlining followed its FY2024 initiative to focus on high-margin construction chemicals and reduce exposure to volatile raw materials. The company reinforced its sustainability leadership in June 2025, highlighting its ECO2 Driven™ technology, which leverages naturally occurring atmospheric gases to reduce Global Warming Potential (GWP) in adhesive curing—an innovation extendable to mass timber production lines.

The industry’s regulatory and market environment also strengthened in 2025, as governments, particularly across Europe and North America, doubled down on carbon neutrality policies and material traceability. In October 2025, a new industry report projected the Glulam market to reach USD 10.9 billion by 2030, reinforcing long-term demand visibility for certified, durable structural adhesives. Meanwhile, Q3 2025 saw growing emphasis on formaldehyde-free PUR systems as global specifiers increasingly mandate low-emission materials in CLT and hybrid timber constructions. Chemical suppliers simultaneously focused on de-risking supply chains for critical components like isocyanates and polyols, mitigating inflationary pressure from petrochemical volatility.

Furthermore, Q4 2025 saw a push toward digitalization and automation in engineered wood manufacturing. Advanced automated laminating lines require adhesives that can support precise metering, rapid cure kinetics, and clean application profiles. Concurrently, regional construction booms in South Asia and Sub-Saharan Africa—driven by urbanization and infrastructure development—are stimulating demand for cost-effective yet durable bonding solutions, ensuring the timber laminating adhesive market remains a cornerstone of sustainable construction innovation globally.

Market Trend 1: Accelerated Adoption of Fast-Press, Room-Temperature Curing Adhesives for CLT Production

The rapid growth of Cross-Laminated Timber (CLT) as a sustainable building material is driving a paradigm shift in adhesive technology toward fast-press, cold-setting polyurethane (PUR) and silicone-based systems. The industry’s focus is on increasing line efficiency and reducing energy usage to meet the demands of large-scale automated mass timber production.

Recent academic studies confirm that one-component polyurethane structural adhesives can achieve the required bond integrity for CLT panels within one hour, significantly outperforming conventional phenolic systems that require more than four hours of pressing. The results in up to a 75% reduction in press time, directly improving production throughput and enabling high-volume CLT manufacturing lines to operate more sustainably.

Global producers have already established strong precedents for the transition. European CLT facilities, which rely heavily on fast-setting PUR systems, report substantial energy savings per cubic meter of timber produced, thanks to the elimination of thermal curing. The introduction of primerless silicone adhesives that achieve bond strength in under five minutes further drives the R&D direction toward rapid room-temperature curing systems, setting new standards for cycle time efficiency in engineered timber bonding.

The environmental benefits are equally compelling. Using low-energy adhesives aligns directly with sustainable construction targets, as the total energy consumption and CO₂ emissions of mass timber buildings can be reduced by over 40% compared to traditional steel and concrete structures.

Market Trend 2: Reformulation to Eliminate Formaldehyde and Isocyanates in Non-Structural Applications

Growing regulatory scrutiny under frameworks like CARB, REACH, and EPA TSCA Title VI is accelerating the industry’s shift toward formaldehyde-free and isocyanate-free adhesive formulations in interior wood applications such as furniture, cabinetry, and wall panels.

The California Air Resources Board (CARB) emission standards, which limit formaldehyde emissions to 0.05 ppm for hardwood plywood, are among the strictest globally. These standards have effectively phased out urea-formaldehyde (UF) and melamine-urea-formaldehyde (MUF) resins in favor of biomass-derived, non-toxic alternatives. Academic studies have confirmed the viability of lignin- and soy protein-based adhesives, where modified lignosulfonate blended with small quantities of pMDI achieved the mechanical strength required for EN 312-certified panels, while drastically reducing formaldehyde release.

The emergence of hybrid adhesive systems that enhance wet adhesion strength by up to 23% without relying on isocyanates marks a significant leap in non-structural adhesive safety and sustainability. Further, chemical innovation using biomass-derived reagents like 5-hydroxymethylfurfural (HMF) offers non-toxic modifications to traditional resin systems, ensuring compliance with indoor air quality standards for residential and commercial applications.

Market Opportunity 1: Development of Bio-Based, Cold-Press Polyurethane Adhesives for Sustainable Mass Timber

The growing focus on carbon-neutral and sustainable construction presents a major commercial opportunity for bio-based polyurethane (PUR) adhesives capable of replacing petroleum-derived resins in mass timber applications such as CLT, LVL, and Glulam.

Leading adhesive manufacturers have already commercialized bio-attributed PUR systems with up to 63% renewable content, certified under the ISCC PLUS mass balance scheme, reducing CO₂-equivalent emissions by over 60% in cradle-to-gate life cycle assessments. The shift toward renewable polyols derived from technical Kraft lignin and liquefied bark exemplifies how biomass feedstocks can maintain structural adhesive strength while minimizing fossil dependency.

Cold-press processing further amplifies sustainability benefits by reducing the need for heat curing, enabling energy savings of up to 30% per production cycle. Additionally, the absence of solvents and isocyanates aligns with EU Green Deal and North American LEED requirements, offering a high-value pathway for adhesive manufacturers to secure eco-compliance certifications and tap into the premium low-carbon construction market.

The widespread adoption of these certified bio-based systems is also reshaping supply chain dynamics, allowing global manufacturers to claim sustainability credits through verifiable, traceable raw material sourcing.

Market Opportunity 2: Engineering of Fire-Retardant, Intumescent Adhesives for Exposed Mass Timber Structures

The implementation of the 2021 International Building Code (IBC), which allows for mass timber buildings up to 18 stories (Type IV-A), has catalyzed an urgent demand for fire-resistant laminating adhesives. Structural adhesives used in CLT and Glulam assemblies must meet stringent fire performance standards, including maintaining bond-line integrity under extreme heat conditions.

The fire resistance of mass timber depends heavily on the formation of a char layer that insulates the inner wood. The next generation of intumescent adhesive systems is being designed to expand and carbonize at specific trigger temperatures, actively contributing to slower char propagation and maintaining structural integrity throughout extended fire exposure.

Research drives that bond-line stability during thermal stress determines whether the wood or the adhesive fails—a critical factor for achieving required 3-hour fire ratings under the IBC. The development of high-temperature resistant adhesive formulations, capable of retaining bonding performance above 250°C, is therefore a high-value innovation area.

In addition, integrating intumescent agents directly into laminating adhesives, rather than applying surface coatings, ensures a uniform fire-retardant performance across the entire bond line—an approach increasingly preferred by structural engineers and regulatory authorities for exposed mass timber construction.

Timber Laminating Adhesives Market Share Insights, 2025-2034

Market Share by Application Type

The structural laminating adhesives segment commands the largest share of the global timber laminating adhesives industry, accounting for an estimated 58.6% of the projected 2025 market share. This dominance is directly linked to the surging demand for engineered wood products (EWPs) such as cross-laminated timber (CLT), glued laminated timber (Glulam), laminated veneer lumber (LVL), and mass timber elements, all of which rely heavily on high-strength, durable adhesive systems. Structural applications are experiencing exponential growth in both developed and emerging markets due to sustainable construction mandates, carbon reduction initiatives, and the aesthetic resurgence of exposed timber architecture in commercial and residential projects. These adhesives are engineered to deliver exceptional load-bearing capacity, heat and moisture resistance, and long-term durability, meeting stringent certification standards such as EN 301 and ASTM D2559. Moreover, as prefabricated timber construction gains momentum, the industry is witnessing a shift toward automated adhesive application systems and one-component polyurethane and melamine-based adhesives, which provide superior bond integrity and production efficiency.

The non-structural or secondary adhesives segment remains a vital and stable component of the market ecosystem. These adhesives are predominantly used in furniture manufacturing, cabinetry, veneer lamination, and plywood production, where cost-effectiveness, surface aesthetics, and curing speed are prioritized. Demand in this segment is closely correlated with consumer spending, home renovation activity, and the furniture export market, making it more sensitive to macroeconomic cycles. However, innovation in low-formaldehyde and bio-based adhesive systems is reshaping product portfolios as manufacturers align with indoor air quality regulations and sustainability goals. Non-structural applications also benefit from the increasing popularity of modular furniture and lightweight engineered panels, ensuring a consistent demand trajectory.

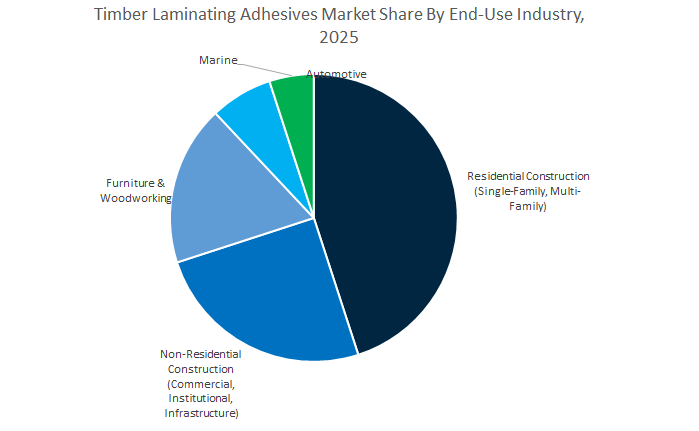

Market Share by End-Use Industry

The residential construction sector leads the global timber laminating adhesives market, holding a projected 44.9% share by 2025, reflecting the pivotal role of wood-based materials in modern housing. The rising adoption of mass timber systems for single- and multi-family homes, combined with a sustained global housing demand, underpins this segment’s dominance. Adhesives play a crucial role in ensuring dimensional stability, weather resistance, and load-bearing strength in glued structural elements used in walls, floors, and roof assemblies. Additionally, increased interest in eco-certified and low-emission homes is accelerating the use of formaldehyde-free and bio-based adhesive systems. Government incentives supporting green building certifications (LEED, BREEAM) further enhance adoption, positioning residential construction as both the largest and most influential market driver for timber adhesives.

Meanwhile, non-residential construction—including commercial, institutional, and public infrastructure projects—represents the fastest-growing sector, fueled by the rapid globalization of timber architecture. The growing construction of mass timber offices, schools, civic buildings, and mixed-use developments in North America, Europe, and Asia-Pacific reflects a fundamental shift toward sustainable urban infrastructure. These large-scale projects require adhesives that deliver superior mechanical performance, fire resistance, and long-term weatherability, often under extreme environmental conditions. Beyond construction, the furniture and woodworking industry forms a mature but steady revenue base, supporting interior fit-outs, joinery, and decorative paneling across residential and commercial spaces. Smaller yet critical niches such as automotive and marine applications rely on specialty timber laminating adhesives designed to withstand moisture, vibration, and thermal cycling, serving high-specification markets.

The competitive landscape of the timber laminating adhesives industry is defined by polyurethane leadership, low-VOC formulation innovation, and integration with mass timber production technologies such as CLT, Glulam, and LVL. Companies are differentiating through fire-rated adhesives, digital dispensing compatibility, and carbon-reduced manufacturing.

Henkel remains at the forefront of engineered wood adhesives with its LOCTITE® HB X PUR product line, engineered for fire-rated structural applications in CLT and Glulam manufacturing. Its zero-formaldehyde polyurethane technology addresses both emission compliance and mechanical reliability. Henkel’s Adhesive Technologies division reported a 20.9% increase in adjusted EBIT for FY2024, driven by its sustainability-led product portfolio. The company’s long-term strategic vision is anchored in net-zero manufacturing, bio-based formulations, and circular innovation partnerships, reinforcing its dominance in the mass timber bonding sector.

Sika AG delivers an expansive range of timber bonding solutions through SikaBond® and SikaForce® brands, addressing high-strength structural wood applications and industrial laminations. The introduction of Purform® technology marked a breakthrough in low-monomer polyurethane adhesives, enhancing worker safety and ensuring REACH compliance. As part of its integrated building systems, Sika offers complete solutions—adhesives, waterproofing membranes, and sealants—to streamline project execution. Financially, Sika achieved a record CHF 1.25 billion net profit in 2024, underlining its resilience and growing foothold in sustainable structural adhesives.

H.B. Fuller is redefining the performance-to-sustainability ratio with high-strength timber laminating adhesives and adjacent eco-efficient bonding technologies. Its ECO2 Driven™ systems offer reduced GWP without compromising curing strength or durability, aligning with global carbon-reduction initiatives. The company’s FY2024 EBITDA margin (16.6%) highlights its strategic focus on value capture and cost efficiency. After divesting its Flooring business, H.B. Fuller sharpened its focus on engineered wood and construction adhesives, positioning itself as a global leader in sustainable building materials chemistry.

Huntsman Corporation leverages decades of polyurethane and epoxy chemistry expertise to deliver structural-grade adhesives for Glulam and CLT beams. Its systems are optimized for large bonding surfaces and thick joints, ensuring load-bearing stability under thermal and environmental stress. Through its global technical centers, Huntsman continues to refine its PUR formulations to meet international safety and fire certification standards. The company’s 2024 Sustainability Report reaffirmed its focus on safe and reliable production aligned with ESG performance metrics across all product verticals.

Ashland offers specialized acrylic-polyurethane hybrid adhesives such as Purethane™ A-1090, delivering excellent moisture resistance and thermal stability in freezer and exterior wood applications. Its expertise in water-based polymer chemistry allows Ashland to provide low-VOC systems that meet evolving regulatory standards and architectural sustainability targets. Leveraging cross-sector innovation from packaging and coatings, Ashland integrates binder chemistry advancements into its timber laminating adhesive portfolio, appealing to manufacturers prioritizing eco-compliance and application versatility.

Country Analysis: Advancing Global Timber Laminating Adhesives Industry through Sustainable and Structural Innovation

Germany – European Timber Construction Pioneer and Bio-Based Adhesives R&D Powerhouse

Germany stands as the epicenter of technological innovation and sustainability in the European timber laminating adhesives industry, supported by the country’s strong regulatory framework and leadership in engineered wood manufacturing. In February 2024, Henkel and Covestro AG announced a landmark collaboration to develop bio-based polyurethane (PU) adhesives for load-bearing timber construction, integrating ISCC PLUS-certified, bio-attributed raw materials into high-strength bonding formulations. The move aligns with Germany’s Circular Economy Action Plan and the European Union’s Green Deal objectives, emphasizing the shift from fossil-based to renewable adhesive chemistries.

At Ligna 2025 in Hanover, Henkel unveiled its micro-emission hot-melt wood adhesive range, featuring ultra-low diisocyanate emissions (<0.1%), ensuring compliance with the EU REACH standard for occupational safety in adhesive manufacturing. Further reinforcing its leadership, Henkel launched the Loctite HB XE Line in March 2025, designed explicitly for Cross-Laminated Timber (CLT) and Glued Laminated Timber (GLT) bonding. The adhesives are engineered to deliver superior shear strength, long-term weather stability, and Eurocode 5 fire protection compliance, making them ideal for sustainable architectural timber construction. Germany’s strong alignment between chemical innovation, structural engineering, and environmental policy continues to shape the future of green construction adhesives across Europe.

United States – Global Leader in Mass Timber Adoption and Formaldehyde-Free Adhesive Innovation

The United States timber laminating adhesives market is rapidly advancing, fueled by regulatory evolution, sustainability commitments, and mass timber construction growth. The 2021 update of the International Building Code (IBC)—widely adopted by multiple U.S. states—permits mass timber structures up to 18 stories, directly increasing demand for Phenol Resorcinol Formaldehyde (PRF) and Polyurethane (PU) structural adhesives. The formulations are now critical for the growing wave of Cross-Laminated Timber (CLT) and Laminated Veneer Lumber (LVL) construction projects across commercial, educational, and multi-family housing developments.

In February 2025, BioBond Adhesives introduced BioAdhere, a USDA BioPreferred-certified, plant-based adhesive line featuring zero microplastics and solvent-free formulations—a significant step toward greener wood bonding solutions. Concurrently, Emulsion Polymer Isocyanate (EPI) and PU adhesives continue to dominate the structural flooring and roof panel sectors, offering high moisture resistance and bond durability under thermal stress. The Inflation Reduction Act (IRA) is further incentivizing sustainable construction materials, spurring R&D into low-VOC, formaldehyde-free adhesives for engineered wood applications. The U.S. thus emerges as a technology-driven and policy-backed leader, balancing industrial scalability, bio-innovation, and environmental compliance in the global timber adhesives landscape.

Finland – Sustainable Wood Processing and Bio-Adhesive Technology Integration

Finland, a global benchmark for sustainable forestry and engineered wood innovation, is advancing the integration of bio-based adhesives in structural timber applications. In May 2025, Koskisen Oyj introduced Zero ThinPly, a formaldehyde-free thin plywood manufactured using a bio-based adhesive co-developed with Plantics. The new adhesive technology eliminates phenolic compounds and urea while maintaining superior water and heat resistance, setting new environmental and performance standards for eco-certified plywood and laminated timber.

Complementing The, Kiilto Oy launched its Pro SW adhesive series in January 2025, a one-component polyurethane system that enhances bonding strength for CLT, glulam beams, and roof trusses by up to 30%. The innovations reflect Finland’s strong R&D emphasis on renewable, non-toxic, and high-durability adhesive systems aligned with European green building regulations. With a deep-rooted commitment to carbon neutrality and forest-based bioeconomy, Finland is shaping the next generation of timber bonding technologies that combine performance with sustainability.

China – High-Volume Infrastructure Growth and MUF Adhesive Dominance

China continues to dominate the global timber laminating adhesives market by volume, driven by its massive residential and commercial construction expansion and the nation’s extensive furniture and panel manufacturing base. Melamine-Urea-Formaldehyde (MUF) adhesives remain the market’s backbone due to their cost efficiency, bond strength, and versatility in the production of plywood, particleboard, and laminated veneer lumber (LVL). With China’s urbanization rate exceeding 65%, demand for prefabricated wooden panels and modular construction components continues to surge.

In addition to cost efficiency, rising middle-class expectations for premium interior finishes and eco-friendly products are pushing manufacturers toward low-formaldehyde or formaldehyde-free formulations. Domestic firms are also investing in advanced R&D for water-resistant and high-thermal-stability adhesives, particularly for engineered wood used in high-humidity environments. With strong policy alignment under China’s Green Building Certification Program, and the country’s commitment to reducing VOC emissions, the market for high-performance, low-emission MUF and hybrid PU adhesives is expected to expand significantly through 2030.

Japan – Seismic-Resistant Timber Adhesives and High-Performance Composite Systems

Japan is a global pioneer in high-strength, seismic-resistant timber adhesive technologies, catering to one of the world’s most demanding structural performance standards. The country’s focus on earthquake-resilient construction has led to widespread adoption of Epoxy and Phenol Resorcinol Formaldehyde (PRF) adhesives in mass timber structures, CLT panels, and glulam beams. The adhesives deliver superior load-bearing capacity, creep resistance, and moisture stability, essential for structural reliability in seismic environments.

AICA Kogyo Co., Ltd., one of Japan’s foremost engineered wood adhesive producers, continues to innovate in industrial composite bonding and formaldehyde-reduced resin systems. The company’s extensive domestic R&D emphasizes chemical durability, fast curing times, and temperature resilience, enhancing Japan’s leadership in both timber construction and high-performance composite adhesives. Japan’s integration of precision chemistry, structural engineering, and seismic safety standards solidifies its reputation as an innovation hub for advanced timber laminating adhesive technologies.

Canada – Expanding Mass Timber Commercialization and CLT Adhesive Demand

Canada’s timber laminating adhesives market is witnessing unprecedented growth, driven by the nation’s mass timber construction boom and emphasis on sustainable forestry-based manufacturing. The federal and provincial governments have introduced incentives for mass timber adoption in public infrastructure projects, leading to surging demand for industrial-scale adhesives used in CLT, GLT, and LVL production.

Key players such as Canfor and Western Forest Products are investing in modern glulam production facilities that require consistent, high-bond-strength adhesive systems. Moreover, Canadian manufacturers are increasingly adopting formaldehyde-free polyurethane and EPI adhesives to align with North American environmental standards and green building certifications. With its abundant forest resources and strong focus on carbon-neutral building materials, Canada is quickly positioning itself as a North American hub for advanced timber bonding and lamination technologies.

Timber Laminating Adhesives Market Report Scope

Timber Laminating Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.1 Billion

|

|

Market Size (2034)

|

$3.8 Billion

|

|

Market Growth Rate

|

6.9%

|

|

Segments

|

By Resin Type (Melamine Formaldehyde, Phenol Resorcinol Formaldehyde, Polyurethane, EPI, Epoxy, PVA), By Application Type (Structural, Non-Structural), By Engineered Wood Product (Glulam, CLT, LVL, SIPs, Plywood), By End-Use Industry (Residential, Non-Residential, Furniture, Automotive, Marine), By Function (Interior, Exterior, Fire-Resistant), By Technology (Water-Based, Solvent-Based, Solvent-Less, Hot-Melt

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, H.B. Fuller Company, Sika AG, Arkema SA, Dow Inc., Hexion, 3M Company, Jowat SE, Franklin International, Pidilite Industries Ltd., Akzo Nobel N.V., Huntsman Corporation, BASF SE, Wanhua Chemical Group Co., Ltd., AICA Kogyo Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Resin Type

- Melamine Formaldehyde

- Phenol Resorcinol Formaldehyde

- Polyurethane

- EPI

- Epoxy

- PVA

By Application Type

- Structural

- Non-Structural

By Engineered Wood Product

- Glulam

- CLT

- LVL

- SIPs

- Plywood

By End-Use Industry

- Residential

- Non-Residential

- Furniture

- Automotive

- Marine

By Function

- Interior

- Exterior

- Fire-Resistant

By Technology

- Water-Based

- Solvent-Based

- Solvent-Less

- Hot-Melt

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Timber Laminating Adhesives Market-

- Henkel AG & Co. KGaA

- H.B. Fuller Company

- Sika AG

- Arkema SA

- Dow Inc.

- Hexion

- 3M Company

- Jowat SE

- Franklin International

- Pidilite Industries Ltd.

- Akzo Nobel N.V.

- Huntsman Corporation

- BASF SE

- Wanhua Chemical Group Co., Ltd.

- AICA Kogyo Co., Ltd.

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the Timber Laminating Adhesives Market with a decision-grade focus on mass-timber use cases (CLT, Glulam, LVL), resin advances, processing efficiency, and compliance pathways; it synthesizes breakthroughs in zero-formaldehyde chemistry, fast-press PUR lines, and intumescent/fire-resistant bonding while our analysis reviews cost drivers, supply-risk (isocyanates/polyols), and specification trends across structural and interior applications. It also highlights how evolving building codes, low-VOC mandates, and factory automation are reshaping adhesive selection, cure kinetics, and quality assurance from beam to panel, positioning qualified systems for scalable, low-carbon construction. For engineers, specifiers, and procurement leaders, this report is an essential resource for aligning bond performance, durability, and EHS objectives with throughput targets, warranty requirements, and circular-design strategies, etc……

Scope Highlights

Segmentation:

- By Resin Type: Melamine Formaldehyde; Phenol Resorcinol Formaldehyde; Polyurethane; EPI; Epoxy; PVA

- By Application Type: Structural; Non-Structural

- By Engineered Wood Product: Glulam; CLT; LVL; SIPs; Plywood

- By End-Use Industry: Residential; Non-Residential; Furniture; Automotive; Marine

- By Function: Interior; Exterior; Fire-Resistant

- By Technology: Water-Based; Solvent-Based; Solvent-Less; Hot-Melt

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Horizon: Historic data 2021–2024 and forecast data 2025–2034.

Companies Covered: Analysis/profiles of 15+ companies, including Henkel, H.B. Fuller, Sika, Arkema, Dow, Hexion, 3M, Jowat, Franklin International, Pidilite Industries, Akzo Nobel, Huntsman, BASF, Wanhua Chemical, and AICA Kogyo.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.