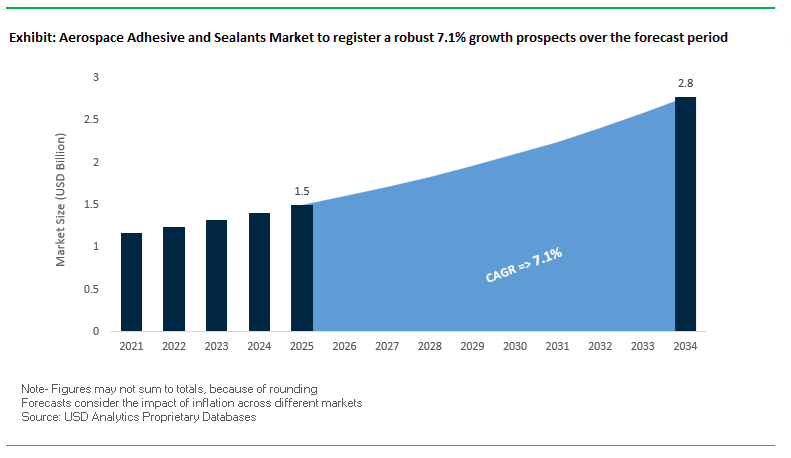

The global aerospace adhesive and sealants market is poised to grow from USD 1.5 billion in 2025 to USD 2.8 billion by 2034 at a 7.1% CAGR, driven by the industry’s shift toward composite-intensive airframes, structural bonding solutions, and advanced maintenance, repair and overhaul (MRO) practices. Unlike commodity adhesives, aerospace-grade formulations — such as structural epoxies, high-temperature silicones, and engineered polysulfide sealants — are engineered to meet the extreme performance, regulatory, and safety standards required by leading OEMs and tier suppliers.

Manufacturers such as Henkel, H.B. Fuller, and 3M emphasize adhesives and sealants designed for high-load structural assembly, critical interface bonding, and long-life sealing performance under thermal, vibration, and environmental stress. Henkel’s aerospace portfolio, for example, includes specialized epoxies and sealants formulated for rapid fixture and reliable integrity in aircraft assembly, underscoring the technical rigor needed for primary and secondary structure bonding. Similarly, H.B. Fuller highlights its comprehensive range of adhesive and sealant chemistries tailored for both commercial and defense aviation applications, supported by global technical service networks that ensure process consistency and on-time delivery.

Beyond structural bonding, aerospace sealants such as polysulfide-based systems engineered for fuel, hydraulic fluid resistance and UV stability withstand the demanding operational environments of aircraft fuselages and control surfaces, ensuring durable joints that maintain seal integrity over long service intervals. Meanwhile, 3M’s broad catalog of adhesion promoters, flexible adhesives, and repair sealants underscores the diversity of aerospace bonding needs — from interior panels and access doors to critical structural interfaces requiring consistent, validated performance.

The market’s evolution is also shaped by regulatory and process imperatives: suppliers are scaling low-VOC, solvent-free and water-based technologies where feasible, balancing environmental compliance with the reliability demands of FAA and EASA certification pathways. Material innovation is further enabling OEMs to replace mechanical fasteners with bonded joints that increase fuel efficiency, reduce weight, and integrate seamlessly into automated assembly platforms — solidifying adhesives and sealants as indispensable elements of aerospace manufacturing and asset longevity

The aerospace adhesives and sealants industry is undergoing a period of intense transformation, defined by sustainability mandates, high-rate production demands, and the integration of advanced composite systems. The sector is witnessing strong capital investments, collaborative R&D programs, and technology rollouts aimed at lightweighting, automation, and eco-compliance.

In October 2025, PPG Industries announced a $380 million investment in a new manufacturing facility in Shelby, North Carolina, specifically dedicated to aerospace coatings and sealants. This expansion marks one of the largest capacity enhancements in North America and aims to strengthen PPG’s supply capabilities for aircraft manufacturers and MRO service providers. Similarly, in September 2025, Hexcel Corporation launched a Type IV carbon overwrap pressure vessel in collaboration with HyPerComp, targeting space and defense composite applications. The same month, Huntsman Advanced Materials unveiled a reformulated range of ARALDITE® epoxy adhesives in Europe—free from BPA and CMR substances—underscoring its commitment to worker safety and sustainability in aerospace materials.

July and June 2025 were landmark months for Hexcel’s strategic partnerships. The company collaborated with A&P Technology and NIAR to develop an FAA certification framework for overbraided structures, streamlining next-generation composite adoption. At the Paris Air Show in June 2025, Hexcel showcased its HexPly® M51 prepreg, known for rapid-curing performance and high-rate structural manufacturing efficiency. In a major sustainability milestone, Hexcel also partnered with FLYING WHALES in June 2025 to supply lightweight composite materials for the LCA60T low-carbon airship, advancing eco-friendly cargo transport solutions. Earlier, in April 2025, Hexcel joined hands with JetZero under the FAA’s FAST program to qualify materials for an “all-wing” demonstrator aircraft—a breakthrough in advanced aerospace design.

Beyond materials innovation, strategic corporate focus has intensified. During 3M’s Investor Day in February 2025, aerospace was highlighted as a core vertical, with the company leveraging its deep material science expertise to advance structural and MRO adhesive solutions. Across the value chain, the trend points toward automation-driven production, bio-based reformulations, and multi-material bonding solutions that meet next-gen aviation sustainability and safety benchmarks.

The transition toward fuel-efficient turbine engines, Sustainable Aviation Fuel (SAF) compatibility, and hydrogen propulsion systems is driving an urgent need for next-generation high-temperature aerospace adhesives and sealants. As aircraft components are increasingly exposed to extreme heat, cryogenic conditions, and aggressive chemical environments, polymer innovation is reshaping bonding technologies used across engine compartments, nacelles, and fuselage interfaces.

Modern epoxy and silicone-based adhesives are engineered to sustain continuous performance beyond 200°C (392°F), addressing the thermal challenges posed by next-generation high-thrust engines. According to Incure’s High-Temperature Adhesives Guide, specialized polymer systems maintain structural integrity even above the range, ensuring durability for both OEM production and aftermarket repair operations.

Further advances are visible in polyimide-based adhesives, which demonstrate continuous stability at 350°C and peak resilience up to 500°C. These materials are increasingly applied in avionics, propulsion assemblies, and composite engine cowling systems, where traditional epoxy systems would degrade. The leap in thermal endurance supports not only jet engines but also emerging hydrogen fuel cell aircraft, which operate at cryogenic temperatures as low as −253°C, demanding adhesives that can withstand rapid thermal cycling without delamination or embrittlement.

Major OEMs such as Airbus—through its ZEROe initiative—are redefining aircraft design around liquid hydrogen propulsion and electric fuel cells, requiring advanced adhesives and sealants that combine cryogenic flexibility, chemical resistance, and electrical insulation. Simultaneously, manufacturers like Incure are developing silicone-based adhesives optimized for a temperature range of −50°C to +250°C, balancing flexibility and vibration damping to ensure reliability in demanding engine and MRO applications.

The continued shift toward composite-intensive aircraft designs is reshaping adhesive and sealant demand across the aerospace industry. With modern airframes comprising up to 50% composite materials by weight, as seen in the Boeing 787 Dreamliner, adhesives have become essential to achieving fuel efficiency, reduced assembly complexity, and superior fatigue performance.

Unlike metallic fasteners that add weight and create stress concentration points, structural epoxy adhesives distribute loads evenly across composite joints, enhancing fatigue resistance and enabling thinner, lighter structures. Research from Patsnap confirms that adhesive-bonded composites improve stress uniformity and damage tolerance, directly supporting aircraft lifespan and structural integrity under cyclic loads.

To further optimize performance, R&D efforts are focused on co-curing adhesive processes, where the adhesive cures simultaneously with the composite structure. The method—used in advanced wing box manufacturing and eVTOL airframes—minimizes assembly time, improves alignment precision, and enhances interfacial bonding strength.

Hybrid joining techniques are also gaining ground, combining adhesives with selective fasteners to achieve redundancy and enhanced mechanical durability in composite-metal interfaces. According to industry research published in MDPI and ResearchGate, these hybrid approaches are becoming standard for next-generation aircraft, offering unmatched weight reduction, vibration resistance, and fuel efficiency improvements.

Market Opportunity 1: Servicing the Rapidly Scaling Commercial and Defense UAV & eVTOL Markets

The rise of Unmanned Aerial Vehicles (UAVs) and Electric Vertical Take-Off and Landing (eVTOL) platforms represents a major growth frontier for aerospace adhesives and sealants. As electric propulsion and compact aerostructures demand high-precision bonding and superior thermal management, adhesive technologies are becoming pivotal in both airworthiness certification and system performance optimization.

In Urban Air Mobility (UAM) applications, noise mitigation and aerodynamic sealing have emerged as key design imperatives. According to Omniseal Solutions, specialized sealants not only improve aerodynamic efficiency but also reduce aeroacoustic emissions, a critical factor in achieving regulatory approval for urban flight operations.

The electric propulsion systems powering UAVs and eVTOLs rely on electrically insulating and moisture-resistant polyurethane adhesives to protect battery modules and electronic control units from vibration, moisture ingress, and shock. ThreeBond India notes that these formulations extend service life and reliability in both defense drones and commercial UAM aircraft.

Manufacturers are also shifting toward fast-curing structural adhesives for modular UAV assembly, replacing traditional fasteners to reduce production time and enable automated robotic assembly lines. In addition, thermally conductive adhesives and pastes (TIMs) are being increasingly adopted to enhance battery heat dissipation and prevent thermal runaway, ensuring operational safety in high-density lithium-ion configurations.

Market Opportunity 2: Capitalizing on MRO Demand from Aging Commercial and Defense Fleets

With the average global commercial fleet age exceeding 15 years, the Maintenance, Repair, and Overhaul (MRO) sector represents a long-term, non-cyclical opportunity for certified aerospace adhesive and sealant manufacturers. As older aircraft undergo structural repairs and life-extension programs, demand for qualified, OEM-approved bonding and sealing solutions continues to surge.

According to Aviation Week Network, adhesives are increasingly replacing mechanical joints in structural repairs to restore integrity and extend component lifespan—particularly where legacy parts are no longer in production. The shift supports both cost efficiency and airworthiness compliance under modern standards.

Governments are reinforcing the trend through targeted initiatives. For instance, India’s MRO Policy 2021 promotes regional MRO hubs to reduce downtime and operational costs, directly stimulating demand for certified aerospace repair adhesives and sealants. Similar policies in the Middle East and Southeast Asia are driving regional consumption, positioning MRO centers as key distribution hubs for aerospace bonding products.

Further, the aftermarket segment—covering corrosion protection, interior reinstallation, and external sealing—remains a stable revenue driver, representing over 60% of total aviation adhesive and sealant usage in service operations. As airlines focus on fleet longevity and sustainability, advanced MRO-grade adhesives will play a central role in maintaining airframe performance and regulatory compliance.

Aerospace Adhesive and Sealants Market Share Insights, 2025-2034

The epoxy adhesives segment dominates the global aerospace adhesives and sealants industry, commanding approximately 45% of the total market share in 2025. Epoxies are the undisputed cornerstone of aerospace bonding due to their exceptional mechanical strength, chemical resistance, and superior adhesion to both metals and advanced composites. They are widely used in primary and secondary structural applications, including fuselage panels, wings, nacelles, and engine components, where performance consistency and durability under extreme temperature and pressure conditions are non-negotiable. Their resistance to jet fuels, hydraulic fluids, and de-icing chemicals makes them ideal for long-term reliability in flight environments. With the increasing adoption of carbon-fiber-reinforced polymer (CFRP) structures in next-generation aircraft such as the Boeing 787 and Airbus A350, epoxy-based structural adhesives have become even more critical, enabling lightweighting without compromising strength. Epoxy adhesives are also favored for their certification pedigree and proven track record with aerospace regulatory bodies (FAA, EASA), which ensures continued dominance. As aerospace manufacturing transitions toward automation, sustainability, and composite-intensive architectures, epoxy systems will remain the core bonding chemistry defining the performance standards of the global aerospace adhesives market.

The film adhesives segment, holding around 20% market share, represents the high-value, precision-driven backbone of advanced aerospace manufacturing. Film adhesives—primarily epoxy-based—are supplied as pre-catalyzed B-staged films, allowing for precise control, minimal waste, and superior bond uniformity in large-scale composite assembly. Their key role lies in wing skin bonding, fuselage assembly, and honeycomb core bonding, where consistent adhesion and void-free bonds are critical for both structural integrity and safety certification. Film adhesives have become essential for automated production processes, particularly in the manufacturing of composite wings, tail sections, and control surfaces. The demand for film adhesives is rising in parallel with the automation of aerospace manufacturing, as they are fully compatible with robotic layup systems and autoclave curing processes. Furthermore, ongoing innovation in out-of-autoclave (OOA) curing and low-temperature film systems is expanding their use into business jets, UAVs, and satellite structures. Their combination of precision application, thermal stability, and structural performance positions film adhesives as the go-to solution for aerospace OEMs seeking both reliability and efficiency in advanced composite fabrication.

, 2025.png)

The polyurethane, silicone, acrylic, and cyanoacrylate adhesives segments represent the specialized and application-specific tier of the aerospace adhesives and sealants market. Polyurethanes are valued for their flexibility, toughness, and compatibility with diverse substrates, making them ideal for interior cabin assemblies, sound-damping panels, and bonding of dissimilar materials. Silicones are indispensable for high-temperature gasketing, sealing, and vibration-damping applications, particularly in engine compartments, fuel tanks, and thermal protection systems. Their ability to maintain elasticity from –60°C to +250°C makes them critical for both commercial aircraft and spacecraft applications. Acrylic adhesives are used for non-structural bonding where fast curing and impact resistance are required, while cyanoacrylates—though limited due to brittleness—are used for quick repairs and small electronic assemblies within avionic systems. While these materials account for smaller volume shares, their high functional diversity and targeted performance advantages make them indispensable in specialized aerospace operations.

The OEM (Original Equipment Manufacturer) segment leads the global aerospace adhesives and sealants industry, holding approximately 60% of the total market share in 2025. This dominance is underpinned by the expanding global aircraft production and the integration of advanced composite structures in both commercial and military platforms. Adhesives and sealants are critical to OEM processes, where they replace traditional fasteners to reduce weight, enhance fuel efficiency, and enable next-generation aerodynamic designs. Major aircraft manufacturers—such as Boeing, Airbus, Lockheed Martin, and Bombardier—are increasingly adopting automated adhesive application and curing systems for precision bonding during fuselage, wing, and engine nacelle assembly. The use of film adhesives, epoxy pastes, and structural sealants in composite bonding and corrosion protection applications continues to rise alongside demand for lightweight and high-durability materials. The OEM segment is also the primary innovation driver in the industry, pushing the development of low-density, flame-retardant, and high-temperature adhesives that meet evolving certification and sustainability standards. With global air travel rebounding and commercial aircraft order backlogs extending into the next decade, the OEM sector will remain the engine of volume growth and technological advancement in the aerospace adhesives and sealants market.

The MRO (Maintenance, Repair, and Overhaul) segment, accounting for about 40% of market share, represents the lifeline of long-term adhesive demand across the aerospace value chain. Unlike OEM manufacturing, which is cyclical and tied to aircraft production rates, MRO activities are driven by the expanding in-service aircraft fleet and mandatory maintenance schedules. This segment encompasses line maintenance, structural repairs, cabin refurbishments, and component overhauls, all of which rely on adhesives and sealants that are certified, compatible, and approved under OEM and aviation authority standards. Products such as silicone sealants, polysulfide fuel tank sealants, and epoxy repair adhesives are essential for extending aircraft lifespan and maintaining safety compliance. As global fleets age and new aircraft platforms introduce more composite-intensive structures, the MRO segment is witnessing increasing demand for composite repair kits, low-VOC adhesives, and rapid-curing systems that minimize aircraft downtime. Additionally, the growth of regional MRO hubs across Asia-Pacific and the Middle East is expanding distribution networks, creating opportunities for local suppliers to offer certified adhesive solutions. With the global fleet expected to exceed 40,000 aircraft by 2035, the MRO market’s steady, service-driven nature ensures its position as the stabilizing and recurring revenue stream of the aerospace adhesives and sealants industry.

The global aerospace adhesives and sealants competitive landscape is anchored by leading innovators including PPG Industries, Hexcel Corporation, Huntsman Advanced Materials, 3M Company, and Solvay (Syensqo). These players are driving the market forward through targeted investments, sustainability initiatives, and technological advancements in epoxy systems, composite adhesives, and thermoplastic bonding. Their strategies reflect a collective industry push toward sustainable manufacturing, lightweight materials, and automation in aerospace assembly.

In October 2025, PPG Industries announced a $380 million investment to establish a new aerospace coatings and sealants facility in the U.S., significantly enhancing its North American capacity. The company’s strength lies in its Aerospace Sealants and Aero-coatings, known for corrosion protection, durability, and fire resistance. PPG’s aerospace division works closely with OEMs and MROs through globally recognized brands such as DESOTHANE® and PR-C®. Ongoing R&D efforts target chromate-free and low-VOC formulations, aligning with aviation industry goals for eco-friendly sealant technologies and emission reduction.

Hexcel Corporation remains a pioneer in advanced composite systems and structural adhesives. The company’s partnership with JetZero in April 2025 exemplifies its role in developing qualified materials for disruptive “all-wing” aircraft architectures. With the HexPly® M51 rapid-curing prepreg introduced in June 2025, Hexcel enables high-rate aerospace manufacturing with reduced cycle times. The firm’s vertically integrated operations—from HexTow® carbon fiber to prepregs and adhesives—ensure precision and quality for both primary and secondary aerospace structures. Hexcel also maintains a strong defense footprint, supporting major U.S. military programs such as the MQ-25 Stingray UAV.

Huntsman Advanced Materials leads innovation in epoxy adhesive systems through its ARALDITE® brand, which has been trusted for over eight decades. In September 2025, Huntsman introduced a reformulated ARALDITE® epoxy adhesive range free of intentionally added CMR substances, ensuring compliance and worker safety. The brand’s sustainable initiatives include the use of post-consumer recycled (PCR) plastic cartridges, reducing carbon emissions by 36%. The company’s solutions help manufacturers replace mechanical fasteners, achieving 75% weight savings and up to 80% process efficiency improvement, aligning with the aerospace industry’s drive for sustainability and cost efficiency.

In February 2025, 3M Company identified aerospace as a strategic growth vertical, channeling R&D resources toward structural bonding, aircraft maintenance, and sealing solutions. Its broad product range extends beyond adhesives to polyurethane protection tapes, thermal acoustics, and films for integrated aircraft systems. Leveraging its material science expertise, 3M addresses challenges like bonding difficult aerospace thermoplastics and improving durability under extreme conditions. The company continues to invest in supply chain resilience and manufacturing efficiency, ensuring reliable deliveries for OEM and MRO customers worldwide.

Solvay (Syensqo) holds a leadership position in high-performance thermoplastic composites and aerospace adhesives, backed by extensive Boeing TPC qualifications for PEKK and PEEK resins. Its integrated product line spans toughened epoxy resin systems, polyimide adhesives, and structural bonding solutions for both primary and secondary aircraft components. Solvay’s global operations across North America, Europe, and Asia ensure proximity to major OEMs, supporting high-volume production of next-generation aircraft. Its materials are engineered for lightweighting, design flexibility, and fuel efficiency, reinforcing its role in the transition toward sustainable and high-performance aerospace materials.

The United States aerospace adhesives and sealants market remains the global benchmark for innovation, with strong investment in lightweight composite bonding, advanced sealant chemistry, and next-generation structural adhesives. In late 2023, Park Aerospace Corp. launched the Aeroadhere FAE-350-1 structural film adhesive, tailored for primary and secondary aerospace assemblies, reinforcing the industry’s ongoing lightweighting and fuel efficiency initiatives. Complementing The innovation, Solvay’s partnership with Wichita State University’s National Institute for Aviation Research (NIAR) is driving R&D into advanced composite bonding and testing technologies, vital for improving material performance in commercial and defense aviation.

Manufacturing capacity is also scaling to meet rising aircraft production rates. In May 2025, PPG Industries announced a $380 million investment to build a state-of-the-art coatings and sealants facility in Shelby, North Carolina, a strategic move aligned with surging demand from Boeing, Lockheed Martin, and other OEMs. With the U.S. defense sector accounting for nearly 40% of global military aviation spending, continuous innovation in high-temperature, stress-resistant adhesives and corrosion-protective sealants is strengthening the country’s leadership in military, commercial, and MRO aerospace applications.

Germany remains the core of Europe’s aerospace adhesive and sealant ecosystem, combining its engineering precision and sustainability-driven chemistry to meet evolving EU standards. Henkel AG, headquartered in Düsseldorf, leads R&D for epoxy and polyurethane adhesives designed for European aerospace programs such as Airbus A320, A350, and Eurofighter platforms. German manufacturers are pioneering chrome-free pretreatment chemicals and low-VOC sealant formulations, aligning with EU REACH and REACH Annex XVII regulations — a critical step toward sustainable aerospace manufacturing and maintenance.

Germany’s integration in the Airbus supply chain is another strategic advantage. The country supports high-volume composite bonding operations, producing advanced gap-filling sealants and lightweight adhesive systems optimized for automated assembly lines. With continued public-private partnerships emphasizing energy-efficient materials and circular manufacturing, Germany is consolidating its reputation as Europe’s hub for advanced aerospace adhesives and sealants that balance mechanical strength, low emissions, and long-term durability.

The United Kingdom aerospace adhesives and sealants industry is advancing through high-value investments in component manufacturing, lightweighting, and Urban Air Mobility (UAM). GE Aerospace announced a €3.3 million investment in 2025 to expand its UK facilities with new machining and production setups, incorporating advanced materials and structural adhesives for critical engine components. The investment enhances the local Tier-1 supplier ecosystem, directly benefiting adhesive formulators catering to metal-to-composite bonding and high-thermal-resistance sealants.

The Future Flight Challenge, backed by UK government innovation funding, continues to drive demand for fast-curing, low-weight adhesives suitable for electric aircraft, drones, and hybrid propulsion platforms. The country’s commitment to aerospace decarbonization and UAM integration is encouraging material suppliers to focus on epoxy, methyl methacrylate (MMA), and polyurethane adhesives that enable multi-material bonding for the next generation of sustainable flight vehicles. The positions the UK as a strategic European hub for advanced adhesive solutions in electric and hybrid aerospace platforms.

China’s aerospace adhesives and sealants market is expanding rapidly in line with its indigenous aircraft production and MRO modernization. The country’s flagship manufacturer, COMAC (Commercial Aircraft Corporation of China), is ramping up output for the C919 and ARJ21 programs, boosting demand for qualified structural adhesives, fuel tank sealants, and composite bonding systems. Local suppliers are scaling capacity to meet stringent aviation-grade material certifications, particularly in fire-retardant epoxy and high-temperature silicone formulations.

The government’s focus on self-reliance in aerospace materials under its “Made in China 2025” initiative has spurred investment in domestic R&D for non-corrosive and flame-resistant sealants. The growing MRO industry, supported by the expansion of facilities in Shanghai, Chengdu, and Xi’an, is increasing consumption of cabin sealants, polysulfide-based fuel tank sealants, and pressure-resistant bonding agents. As local players strengthen technology partnerships with Western OEMs, China is emerging as a key aerospace adhesives production base and a critical link in the global supply chain.

Singapore continues to solidify its position as a global MRO (Maintenance, Repair, and Overhaul) hub, directly influencing the demand for advanced aerospace adhesives and sealants. In September 2025, GE Aerospace announced a major multi-year investment at its Seletar Aerospace Park facility, focusing on transforming it into a repair technology research and automation hub. The initiative includes robotic application systems and additive manufacturing integration, necessitating fast-curing, high-adhesion sealants and bonding agents to meet MRO throughput requirements.

The investment aligns with Singapore’s national ambition to lead in digitalized and sustainable aerospace operations, fostering local partnerships to co-develop repair-optimized adhesives capable of maintaining performance under variable stress, temperature, and vibration. The convergence of automation, precision repair, and material science is positioning Singapore as a technological epicenter for aerospace adhesive applications in the Asia-Pacific MRO ecosystem.

India’s aerospace adhesives and sealants industry is growing rapidly due to its twin focus on defense modernization and commercial aviation expansion. The ‘Make in India’ initiative, led by the Ministry of Defence, is propelling indigenous aircraft manufacturing through Hindustan Aeronautics Limited (HAL) and related defense programs, stimulating the need for certified aerospace adhesives for aircraft assembly, rotorcraft, and avionics. The specialized formulations are used in composite structures, canopy bonding, and fuel system sealing, meeting stringent defense-grade requirements.

In the commercial sector, a surge in aircraft orders by carriers such as Indigo and Air India is driving long-term OEM and MRO demand for structural and sealing adhesives. International materials suppliers like Hexcel Corporation are expanding operations to meet the rising adoption of carbon fiber composites that require structural epoxy adhesives for bonding and assembly. India’s strategic emphasis on self-reliant aerospace production, coupled with a growing civil aviation market, is establishing it as a future hub for aerospace-grade adhesives and composite bonding materials in South Asia.

Poland’s aerospace sector is gaining global relevance through engine component manufacturing and aerospace cluster expansion, directly influencing demand for high-specification adhesives and sealants. In 2025, GE Aerospace announced a €11.6 million investment in new machinery and infrastructure in Poland to expand production for military rotorcraft and commercial aircraft engines. The investment boosts consumption of structural epoxy adhesives, polyurethane sealants, and precision bonding materials for critical aerospace assemblies.

The Polish Aviation Valley, home to a growing cluster of OEMs, Tier-1 suppliers, and MRO providers, continues to attract foreign investment, driving technology transfer and innovation in advanced bonding processes. With an emphasis on composite manufacturing and engine maintenance, Poland is emerging as a strategic European hub for aerospace adhesives, contributing to the continent’s resilient supply chain for high-performance materials.

Aerospace Adhesive and Sealants Market Report Scope

Aerospace Adhesive and Sealants Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.5 Billion

|

|

Market Size (2034)

|

$2.8 Billion

|

|

Market Growth Rate

|

7.1%

|

|

Segments

|

By Product Type (Adhesives, Sealants), By Adhesives Chemical Type (Epoxy, Polyurethane, Film Adhesives, Cyanoacrylate, Acrylic, Others), By Sealants Chemical Type (Polysulfide, Silicone, Polyurethane, Others), By Technology (Solvent-Based, Water-Based, Hot-Melt, Reactive, Film Adhesives, UV Cured), By Aircraft Type (Commercial Aircraft, Military Aircraft, General Aviation, Spacecraft & Launch Vehicles, Unmanned Aerial Vehicles (UAVs)), By Application (Interior, Exterior, Engine, Fuel Tanks, Windshields & Windows, Electronics & Wiring, Composites Bonding, Metal Bonding, Fluid/Pressure Sealing), By End-User (OEM, MRO

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, 3M Company, PPG Industries Inc., H.B. Fuller Company, Huntsman Corporation, Solvay S.A., Dow Inc., Hexcel Corporation, DuPont de Nemours, Inc., Master Bond Inc., Permabond LLC, Scott Bader Company Ltd., Arkema S.A. (Bostik), Sika AG, L&L Products, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Product Type

By Chemical Type (Adhesives)

- Epoxy

- Polyurethane

- Film Adhesives

- Cyanoacrylate

- Acrylic

- Others

By Chemical Type (Sealants)

- Polysulfide

- Silicone

- Polyurethane

- Others

By Technology

- Solvent-Based

- Water-Based

- Hot-Melt

- Reactive

- Film Adhesives

- UV Cured

By Aircraft Type

- Commercial Aircraft

- Military Aircraft

- General Aviation

- Spacecraft & Launch Vehicles

- Unmanned Aerial Vehicles (UAVs)

By Application

- Interior

- Exterior

- Engine

- Fuel Tanks

- Windshields & Windows

- Electronics & Wiring

- Composites Bonding

- Metal Bonding

- Fluid/Pressure Sealing

By End-User

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- Henkel AG & Co. KGaA

- 3M Company

- PPG Industries Inc.

- H.B. Fuller Company

- Huntsman Corporation

- Solvay S.A.

- Dow Inc.

- Hexcel Corporation

- DuPont de Nemours, Inc.

- Master Bond Inc.

- Permabond LLC

- Scott Bader Company Ltd.

- Arkema S.A. (Bostik)

- Sika AG

- L&L Products, Inc.

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the revenue runway from $1.5 billion (2025) to $2.8 billion (2034) and the 7.1% CAGR, maps certification pathways, and quantifies how composite-intensive platforms, high-temperature polymers, and fuel-resistant chemistries are changing bill-of-materials decisions. Our analysis reviews OEM/MRO demand pivots, benchmarks cure-speed and automation fit, and distills qualification lead times that matter for program ramps. It highlights regulatory momentum (FAA/EASA), solvent-free reformulations, and the economics of switching from mechanical fastening to structural bonding. With technology scorecards, cost-in-use models, and scenario stress tests, this report is an essential resource for strategy, sourcing, engineering, and product leaders seeking airworthiness-ready, lower-mass, and longer-life bonding and sealing solutions—plus the breakthroughs most likely to pass qualification windows on time.

Scope Includes

- By Product Type: Adhesives; Sealants.

- By Chemical Type (Adhesives): Epoxy; Polyurethane; Film Adhesives; Cyanoacrylate; Acrylic; Others.

- By Chemical Type (Sealants): Polysulfide; Silicone; Polyurethane; Others.

- By Technology: Solvent-Based; Water-Based; Hot-Melt; Reactive; Film Adhesives; UV Cured.

- By Aircraft Type: Commercial; Military; General Aviation; Spacecraft & Launch Vehicles; UAVs.

- By Application: Interior; Exterior; Engine; Fuel Tanks; Windshields & Windows; Electronics & Wiring; Composites Bonding; Metal Bonding; Fluid/Pressure Sealing.

- By End-User: OEM; MRO.

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

- Timeframe: Historic 2021–2024 and Forecast 2025–2034.

Companies: 15+ company analysis/profiles.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.