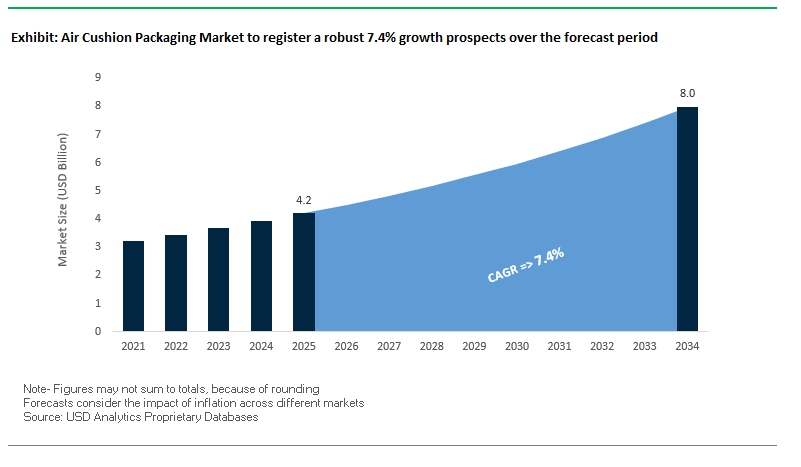

Market overview: e-commerce fulfillment, on-demand inflatables, and lightweighting propel the market from $4.2B (2025) to $8.0B (2034) at 7.4% CAGR

Executive overview for packaging, logistics, and sustainability leaders. The global air cushion packaging market is scaling with the expansion of e-commerce and omnichannel parcel shipping, where void-fill reliability, cube efficiency, and total landed cost dominate buying criteria. Operators are standardizing on on-site inflatable systems to produce packaging on demand, cutting warehouse space and inventory risk. Lightweighting remains a structural advantage air pillows lower freight mass and emissions versus molded or paper-heavy alternatives while material innovation (bio-based resins, PCR blends) aligns with evolving regulatory and brand ESG targets. Performance choices increasingly hinge on automation readiness, ISTA-compliant protection, and recyclability without sacrificing pack-out speed.

Key Insights for professionals

- Demand engine: U.S. e-commerce sales grew 7.5% in Q4-2023, reinforcing the secular need for protective, lightweight void-fill across parcel networks.

- Cost & carbon: Air pillows reduce shipping weight, lowering transportation cost and Scope 3 emissions while maintaining shock/void control.

- Operational model: On-demand inflators eliminate bulky dunnage inventories and improve dock-to-pack agility in high-mix fulfillment.

- Materials roadmap: Shift from conventional PE/PP toward bio-based and PCR content to satisfy sustainability mandates.

- Specification focus: Match film gauge/barrier to product risk, verify automation compatibility, and ensure end-of-life claims align with local recovery streams.

Market Analysis: automation deals, capacity adds, and AI toolchains reshape protection economics (2024–2025)

Strategic collaborations underscore a pivot to automation and AI-assisted pack-out. In August 2025, Ranpak and Walmart announced a multi-year rollout of AutoFill™ across Next-Gen Fulfillment Centers, pairing machine vision with precise dunnage dosing to trim material overuse and labor variance. The same month, Ranpak expanded its AI footprint via a partnership with Rabot (February 2025) and showcased AI/automation at ProMat (March 2025), including on-demand printing for line personalization signals that retailers will increasingly expect closed-loop, data-driven pack optimization.

Supply capacity and materials advanced in parallel. Sealed Air reported Q2-2025 volume growth in protective packaging its first since Q4-2021 while executing on CTO2Grow to tighten conversion costs and service levels. Pregis added blown-film capacity in May 2025 (Anderson, SC) including EVOH barrier options to broaden high-performance films and expanded sustainable paper portfolios (e.g., EasyPack®/GeoTerra®). Ecosystem moves continued: Stratasys ( July 2025 ) acquired assets from Nexa3D to accelerate high-speed polymer AM applicable to pack fixture/prototype tooling, and Harpak-ULMA (April 2025) launched a 3D-printing service for tray prototyping, compressing design-to-trial from weeks to hours. Consolidators also deepened regional reach Macfarlane Group acquired Allpack Packaging Supplies (March 2024) to enhance protective offerings in East Anglia.

Implications for buyers: Expect tighter automation-film co-development, verified ISTA performance at higher line speeds, and broader availability of PCR/bio-based film SKUs. Business cases should capture material right-sizing, labor deltas from AI dosing, and freight savings from lighter pack-outs, while ensuring reverse-logistics or store-take-back programs support end-of-life claims.

Emerging Trends and Strategic Opportunities Shaping the Air Cushion Packaging Market

Strategic Shift Towards High-Performance Recycled Content and Monomaterial Films

The air cushion packaging market is experiencing a decisive shift towards sustainable, high-performance films that meet both regulatory and corporate sustainability mandates. Manufacturers are increasingly investing in air cushion films with high post-consumer recycled (PCR) content, while adopting monomaterial polyolefin structures to enhance recyclability. For instance, Sealed Air has introduced inflatable cushions with 80% recycled content, including 30% post-consumer material, achieving durability, burst strength, and creep resistance comparable to traditional materials. Companies such as Mondi and Storopack are advancing monomaterial PE and PP films, simplifying end-of-life recycling by eliminating multi-layer separation requirements. Extended Producer Responsibility (EPR) regulations are a key driver, with products like Storopack’s AIRplus® films obtaining RecyClass certification, providing brands with a verifiable path to compliance across Europe. This trend not only strengthens sustainability credentials but also aligns with consumer and regulatory pressure for recyclable packaging solutions.

Automation and On-Demand System Integration in E-Commerce Fulfillment

The rapid growth of e-commerce is fueling the integration of automated, on-demand air cushion packaging systems in fulfillment centers. Automation reduces labor costs, improves efficiency, and minimizes material waste. Stanford University studies indicate that process automation can cut labor costs by 50% and enhance operational efficiency by 30%, demonstrating the value of on-demand air cushion production directly at packing stations. Leading solutions from Storopack and Sealed Air enable packers to produce void-fill materials on-demand, drastically reducing storage space for bulky pre-inflated cushions. Furthermore, University of Cambridge research shows that precise material usage can reduce packaging costs by 40% and carbon footprint by 70%, highlighting the sustainability and economic advantages of integrating automated air cushion systems into modern e-commerce logistics.

Development and Commercialization of Certified Compostable Protective Air Cushions

The increasing focus on circular economy principles presents a significant opportunity for certified compostable air cushions. Conventional polyethylene cushions often fail to enter recycling streams due to their lightweight structure, creating end-of-life disposal challenges. Compostable alternatives, such as Storopack’s AIRplus® Bio Home Compostable film, offer a fully natural degradation pathway certified by TÜV Austria to convert into carbon dioxide, water, and biomass within 365 days. These films leverage bio-based resources like starch, contributing to renewable material use and the circular economy. The market demand is further validated by leading e-commerce brands like Amazon, which have replaced nearly 95% of single-use plastic cushions in North America, signaling a significant opportunity for cost-competitive, high-performance compostable air cushions to capture the zero-waste packaging segment.

Competitive Landscape: leaders differentiate on automation readiness, recycled/bio content, and on-demand systems uptime

A concentrated set of players is setting benchmarks in inflator reliability, film science, and closed-loop automation the core levers behind cost-per-shipment, damage rates, and sustainability KPIs.

Sealed Air Corporation On-demand inflatables and recycled content at global scale

Sealed Air anchors the category with BUBBLE WRAP® cushioning and NewAir I.B. on-demand systems that shrink warehouse footprints and boost pack-station throughput. In Q2-2025, the company posted its first protective-packaging volume growth since Q4-2021, supported by its CTO2Grow program to streamline operations. The portfolio spans air pillows, void-fill, and protective films, with increasing emphasis on recycled content and recyclable designs. For high-volume e-commerce, Sealed Air’s proposition centers on uptime, consumables consistency, and network-wide deployment/servicing that protects OEE and cost-to-serve.

Ranpak Holdings Corp. AI-driven paper automation with blue-chip retail adoption

Ranpak specializes in paper-based cushioning and void-fill plus automation that minimizes material use without compromising protection. AutoFill™, now rolling out with Walmart (August 2025), uses AI + vision to meter dunnage precisely, normalizing pack quality across shifts. New AI/automation unveiled at ProMat (March 2025) and the Rabot collaboration (February 2025) extend Ranpak’s software layer. The value proposition: material right-sizing, labor efficiency, and lower plastic reliance a compelling route for retailers prioritizing fiber-first sustainability narratives.

Pregis LLC High-performance films and scalable on-demand inflators

Pregis offers a broad mix of air cushioning systems (AirSpeed), paper-based void-fill, and flexible packaging. The May 2025 expansion of EVOH barrier film capacity (Anderson, SC) strengthens performance options for moisture/oxygen-sensitive shipments, while the EasyPack® line (including GeoTerra®) broadens sustainable paper SKUs. Strategically, Pregis focuses on smart, sustainable solutions pairing on-demand inflators that reduce labor and storage with a film portfolio increasingly oriented to recycled content and curbside-ready end-of-life where infrastructure permits.

3M Company Performance adhesives and tapes that stabilize pack integrity

3M underpins protective workflows with tapes, adhesives, and materials used to seal, reinforce, and integrate air-cushion systems into cartonization. Through its OMX operating model transformation, 3M is targeting organic growth and operational efficiency to improve margins and resource allocation. In air-cushion contexts, the company’s role is enabling secure seals, label adhesion, and structural reinforcement so that void-fill performance translates into real-world drop/stack protection and fewer transit exceptions.

Air Cushion Packaging Market Share Insights

Air Bubble Packaging Dominates Market Share by Product Type in the Air Cushion Packaging Industry

Air bubble packaging leads with 40% of the market, supported by its unrivaled durability, cushioning performance, and brand recognition, making it the default choice for fragile, high-value goods such as electronics, glassware, and medical instruments. Air pillows hold 35% share, establishing themselves as the efficiency-driven solution for e-commerce void-fill applications, where lightweight films reduce shipping costs and high-speed inflation systems drive operational efficiency. Inflatable air bags, while smaller in volume, are critical in pallet-level logistics, protecting heavy or irregular loads during freight transport and reducing in-transit damage. Air column bags represent the premium cushioning segment, gaining traction as all-in-one protective mailers for cosmetics, pharmaceuticals, and small electronics, where branding and a professional appearance are as important as protection. The segmentation reflects a balance between high-volume commodity applications like air pillows and specialized, value-added solutions like air columns.

E-commerce and Retail Drive Market Share by End-Use in the Air Cushion Packaging Industry

E-commerce and retail hold a commanding 55% share, cementing their position as the undisputed growth engine of the air cushion packaging market. The exponential rise of online shopping and direct-to-consumer shipments drives demand for lightweight, protective void-fill and cushioning solutions that reduce returns and enhance consumer satisfaction. Electronics and appliances represent 25%, forming the high-value core where damage prevention is critical to avoid costly product returns and warranty claims. Pharmaceuticals and healthcare, with 8%, rely on specialized air column bags and wraps to safeguard sensitive devices and biologics under strict shipping regulations. Food and beverages account for 7%, primarily through the protection of fragile glass bottles, premium oils, and condiments during transit. Automotive, holding 5%, represents the industrial niche where air cushions protect sensors, lighting assemblies, and precision parts in complex logistics networks. Together, these end-use insights highlight how consumer convenience, product value, and supply chain reliability dictate adoption across industries.

United States: State-Level EPR Laws and Sustainable Air Cushion Innovations Fuel Market Expansion

The U.S. air cushion packaging market is increasingly influenced by state-level Extended Producer Responsibility (EPR) regulations, which place the cost and responsibility of packaging waste management on producers. This has accelerated the adoption of sustainable materials, including air cushions made from recycled content. Technological advancements are driving innovation, with companies like Pregis introducing high-pressure air cushioning films containing 80% post-consumer recycled (PCR) material, reflecting the market’s shift toward high-performance sustainable solutions.

Corporate initiatives by major e-commerce players, such as Amazon, are also reshaping the market. By replacing plastic air pillows with recycled paper in North American fulfillment centers, Amazon is expected to save millions of pounds of plastic and influence industry-wide packaging standards. The explosive growth of e-commerce continues to drive demand for lightweight, on-demand, and protective void-fill solutions, while investments in advanced on-site inflation systems and automated packaging lines streamline operations, save storage space, and reduce shipping costs. Consumer demand for eco-friendly options, including biodegradable and compostable air cushions, is at an all-time high, further reinforcing the sustainability trend in the U.S. market.

Germany: Circular Economy Leadership and Eco-Friendly Air Cushion Development

Germany’s air cushion packaging market is shaped by stringent regulations, including the EU Packaging and Packaging Waste Regulation (PPWR) effective February 2025, which mandates that all packaging must be fully recyclable or reusable by 2030. The country’s Packaging Act (VerpackG) ensures producers are responsible for the entire lifecycle of their packaging, encouraging the creation of highly recyclable mono-material air cushions and the adoption of robust recycling systems.

Technological innovation is thriving, with companies like Storopack leading the market through home-compostable air cushion films and products with up to 100% recycled content. Governmental mandates under the EU PPWR emphasize waste reduction and reuse targets, significantly influencing the air cushion packaging industry. Key applications are prevalent in the electronics and automotive sectors, where protective void-fill solutions are critical for fragile or high-value components, highlighting Germany’s role as a pioneer in sustainable and technologically advanced air cushion packaging.

China: Dual Carbon Goals and E-Commerce Expansion Accelerate Sustainable Packaging Adoption

China’s air cushion packaging market is driven by the government’s “dual carbon” initiative, targeting carbon peak and neutrality. Policies promoting eco-friendly and reusable materials are reshaping the design and production of air cushions. Technological advancements, including AI and “5G plus industrial internet” integration, optimize production processes and enhance flexible manufacturing capacity, reducing material waste and improving efficiency.

Sustainability is a central focus, with new policies restricting non-degradable plastics and promoting paper-based alternatives. Companies like Dow and Procter & Gamble China have launched mono-PE air capsules designed for recyclability and material reduction. The rapid expansion of domestic e-commerce platforms fuels demand for customizable, protective air cushions across diverse industries, from food to chemicals. Strategic investments in local manufacturing and vertically integrated supply chains, particularly in Guangdong province, are positioning the region as a critical hub for high-volume air cushion production and logistics efficiency.

India: PLI Scheme and Biodegradable Innovations Drive Market Growth

India’s air cushion packaging market is benefiting from the Production Linked Incentive (PLI) Scheme, which boosts demand for protective and efficient packaging in the electronics sector. Government initiatives like the Swachh Bharat Mission promote plastic waste management through Plastic Waste Management Units (PWMUs), influencing the packaging supply chain. Regulatory policies, including the Plastic Waste Management (Amendment) Rules, are driving the adoption of eco-friendly alternatives.

Technological advancements, such as on-demand automated air cushion systems, are improving operational efficiency and reducing storage requirements. The focus on biodegradable and compostable materials is growing, with companies like Mumbai-based WOL3D pioneering protective packaging solutions using advanced manufacturing methods. This convergence of regulatory support, sustainability initiatives, and technological adoption is rapidly advancing India’s air cushion packaging market.

Brazil: Circular Economy Policies and AI-Enhanced Manufacturing Promote Sustainable Packaging

Brazil’s air cushion packaging market is strongly influenced by the National Solid Waste Policy, which encourages a circular economy through reusable and durable packaging solutions. Technological advancements, including AI and robotics, are enhancing operational efficiency and quality control, enabling automated sorting, defect detection, and sophisticated production capabilities.

Sustainability is a key driver, especially following the January 2025 ban on imported solid waste, including plastics, fostering eco-friendly material adoption. Strategic investments in factory expansions, reverse logistics, and recycling technologies are anticipated to reach R10.5bn/yr ($1.8bn/yr), bolstering local production capabilities. The growing e-commerce sector, particularly for fragile goods like electronics and glassware, is fueling demand for air cushions designed for superior protection, positioning Brazil as a significant market for sustainable and high-performance air cushion packaging.

Japan: Bio-Based Materials and Precision Manufacturing Reinforce High-Performance Air Cushion Solutions

Japan’s air cushion packaging market is supported by advanced precision manufacturing and AI-driven design processes that enhance efficiency and product accuracy. Regulatory updates from May 2025 by the Ministry of Health, Labour and Welfare (MHLW) revise the “Specifications and Standards for Foods, Additives, etc.,” enforcing stricter food-contact packaging standards.

The market is shifting toward bio-based materials, exemplified by LyondellBasell’s partial incorporation of bio-based polypropylene in Shiseido’s packaging. Continuous innovation in functionality focuses on high dimensional stability and resistance to deformation, enabling high-performance protective solutions. Japan’s emphasis on sustainable and technologically advanced air cushions, combined with regulatory compliance and precision manufacturing capabilities, strengthens its position as a leading market for premium and eco-friendly packaging solutions.

Air Cushion Packaging Market Report Scope

Air Cushion Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.2 Billion

|

|

Market Size (2034)

|

$8 Billion

|

|

Market Growth Rate

|

7.4%

|

|

Segments

|

By Product Type (Air Pillows, Air Bubble Packaging, Inflatable Air Bags, Air Column Bags), By Material (PE, PP, PET, Bio-based Materials), By Functionality (Void Filling, Block & Bracing, Wrapping, Corner Protection), By End-Use Industry (Electronics & Appliances, E-commerce & Retail, Food & Beverages, Pharmaceuticals & Healthcare, Automotive)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Sealed Air Corporation, Pregis Corporation, Storopack Hans Reichenecker GmbH, Smurfit Kappa Group, Intertape Polymer Group (IPG), Automated Packaging Systems Inc., Airfil Protective Packaging Ltd, Fromm Packaging Systems, Shurtape Technologies, LLC, Veritiv Corporation, Protective Packaging Company (PPC), FP International, Macfarlane Group PLC, Wenzhou Rehuo Packaging Technology Co., Ltd., Jinhua Guanfeng Packaging Materials Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Air Cushion Packaging Market Segmentation

By Product Type

- Air Pillows

- Air Bubble Packaging

- Inflatable Air Bags

- Air Column Bags

By Material

- PE

- PP

- PET

- Bio-based Materials

By Functionality

- Void Filling

- Block & Bracing

- Wrapping

- Corner Protection

By End-Use Industry

- Electronics & Appliances

- E-commerce & Retail

- Food & Beverages

- Pharmaceuticals & Healthcare

- Automotive

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Air Cushion Packaging Market

- Sealed Air Corporation

- Pregis Corporation

- Storopack Hans Reichenecker GmbH

- Smurfit Kappa Group

- Intertape Polymer Group (IPG)

- Automated Packaging Systems Inc.

- Airfil Protective Packaging Ltd

- Fromm Packaging Systems

- Shurtape Technologies, LLC

- Veritiv Corporation

- Protective Packaging Company (PPC)

- FP International

- Macfarlane Group PLC

- Wenzhou Rehuo Packaging Technology Co., Ltd.

- Jinhua Guanfeng Packaging Materials Co., Ltd.

* List Not Exhaustive

Methodology

USDAnalytics employs a rigorous, multi-source methodology to provide actionable insights into the global Air Cushion Packaging Market. Our research integrates primary interviews with packaging engineers, supply chain and e-commerce logistics managers, and sustainability officers, combined with secondary analysis of corporate reports, trade publications, regulatory filings, and government databases. Market sizing from USD 4.2 billion in 2025 to USD 8.0 billion by 2034 at a 7.4% CAGR is calculated using both bottom-up and top-down approaches, considering product types (air pillows, air bubble packaging, inflatable air bags, air column bags), materials (PE, PP, PET, bio-based resins), functionalities (void-fill, block & brace, wrapping, corner protection), and end-use industries (e-commerce & retail, electronics, healthcare, food & beverages, automotive). USDAnalytics evaluates emerging trends such as automation and on-demand systems, AI-assisted pack optimization, high PCR and monomaterial films, and certified compostable cushions, alongside regional dynamics in the U.S., Germany, China, India, Brazil, and Japan. Competitive benchmarking encompasses leaders such as Sealed Air, Pregis, Storopack, and Ranpak, with focus on automation readiness, sustainable materials, and operational efficiency. This integrated approach ensures packaging, logistics, and sustainability professionals receive precise, forward-looking intelligence to optimize protective performance, cost efficiency, and environmental compliance.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.