Automotive Ceramics Market Overview: High-Temperature Performance, EV Power Electronics Reliability & Sensor Precision Driving Material Demand

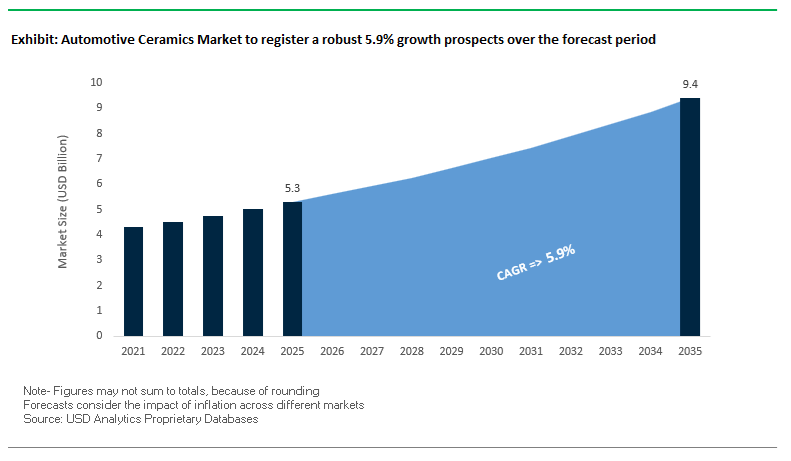

The Automotive Ceramics Market, valued at USD 5.3 billion in 2025 and projected to reach USD 9.4 billion by 2035 at a steady CAGR of 5.9%, is becoming a mission-critical technology pillar for next-generation EV platforms, 800V power electronics, emissions control systems, and high-reliability drivetrain components. As OEMs and Tier-1 suppliers shift toward electrification and advanced thermal management, demand is accelerating for SiC power module substrates, ultra-high thermal conductivity AlN ceramics, high-precision zirconia/alumina sensors, and long-life Si₃N₄ ceramic bearings that can withstand extreme electrical, thermal, and mechanical stresses.

For procurement teams, power-electronics engineers, and automotive OEMs, the strategic value of advanced ceramics is tied to Thermal performance—materials capable of supporting >200°C junction temperatures and >170 W/m·K thermal conductivity to reduce cooling-system mass, Sensor precision—zirconia-based oxygen and NOx sensor elements that maintain ±0.02 lambda accuracy at 900°C under demanding Euro 7/CAFE conditions, and Mechanical durability—ceramic bearings and DPF substrates engineered for multi-year operating life and >98% soot capture efficiency, supporting hybrid and diesel fleet reliability.

The convergence of higher allowable junction temperatures, improved heat dissipation, and multi-fold bearing life extension demonstrates a clear pathway for OEMs to shrink inverter size, improve system reliability, lower total cost of ownership (TCO), and accelerate EV platform adoption. As EV architectures evolve toward more compact, higher-density designs, automotive ceramics become essential for achieving the durability, efficiency, and sensor fidelity demanded by global vehicle programs.

Potential advantages driving the automotive ceramics sales include-

- SiC power module substrates support Tj >200°C, enabling reduced cooling mass and more compact inverter designs for 800V EV platforms;

- Zirconia lambda sensors achieve ±0.02 lambda accuracy at 900°C, meeting the stringent requirements of Euro 7 and CAFE standards.

- Cordierite and SiC DPF substrates deliver >98% soot filtration, ensuring compliance for diesel and hybrid fleets.

- AlN substrates provide thermal conductivity >170 W/m·K, supporting high-voltage battery, onboard charger, and power-control thermal management.

- Si₃N₄ ceramic bearings extend service life up to 5× longer than steel, dramatically improving high-speed motor efficiency and reducing maintenance costs.

Market Analysis: Recent Capacity, Additive Manufacturing & Product Launches Shaping Automotive Ceramics

The Automotive Ceramics market has seen targeted capacity moves and material launches that accelerate ceramic adoption across EV power electronics, sensors and wear components. In November 2025, Sintokogio Group announced the agreement to acquire Bosch Advanced Ceramics (Germany), strengthening access to European technical ceramics know-how and additive manufacturing capabilities - a strategic consolidation that will expand supply options for automotive OEMs seeking localized, high-precision ceramic components. In October 2025, KYOCERA Fineceramics Medical GmbH opened a production site in Waiblingen, Germany; while framed as medical capacity, the investment signals Kyocera’s broader commitment to expanding fine-ceramic throughput in Europe, which supports its automotive ceramics supply chain.

Additive manufacturing and materials innovation advanced in July 2025, when Kyocera Fineceramics Europe enabled 3D printing of SiSiC geometries at Selb, Germany - allowing complex thermal and wear-resistant geometries for EV thermal management and turbocharger components that were previously difficult or costly to machine. Also in July 2025, Kyocera showcased its integrated portfolio of semiconductor, fine ceramic and automotive components at The Advanced Ceramics Show, reinforcing cross-sector material synergies for power electronics and sensors. In June 2025, CeramTec launched Sinalit, a custom material targeted at high-performance power modules - a direct response to EV inverter requirements for higher thermal conductivity, dielectric strength and reliability under high junction temperatures.

Earlier in January 2025, Kyocera expanded manufacturing technologies (multi-wire sawing capability) and joined the Mannheim Energy Efficiency and Sustainability Network, indicating supplier focus on precision substrate slicing and reduced process energy intensity - both relevant to automotive OEMs seeking low-carbon supply chains. Going back to May 2024, Kyocera exhibited next-generation in-car sensor and road communication ceramics, signaling a multi-year R&D push into piezoelectric and functional ceramics for ADAS and autonomous driving systems.

Key Trends Reshaping the Automotive Ceramics Market

Trend 1: Silicon Nitride Becomes a Qualified Mass-Production Material for Electrified Powertrain Bearings and High-Stress Components

Silicon Nitride (Si₃N₄) is undergoing rapid qualification across global EV and hybrid platforms as OEMs confront unprecedented mechanical, thermal, and electrical challenges in modern powertrains. Unlike steel, Si₃N₄ ceramic bearings offer complete electrical insulation, preventing shaft voltage-induced arcing that commonly leads to premature pitting and catastrophic bearing failure in traction motors with variable speed drives. This insulation advantage alone is accelerating the transition to ceramic bearings in high-speed e-propulsion systems.

Si₃N₄’s lightweight nature—approximately 58% lighter than steel alloys—enhances rotational acceleration in hybrid bearings, reducing frictional losses and improving motor efficiency. At the same time, its chemical inertness and corrosion resistance significantly reduce lubrication requirements. This characteristic is particularly valuable in EVs, where extreme temperatures, inconsistent lubrication patterns, and contamination risks degrade steel components more rapidly than in traditional ICE drivetrains. Si₃N₄’s combination of durability, thermal stability, and electrical insulation is establishing it as a cornerstone ceramic material for both high-performance and mainstream electric powertrain architectures.

As OEMs intensify lightweighting initiatives and increase motor speeds to 20,000 rpm and beyond, the automotive ceramics market will see accelerated adoption of Si₃N₄ bearings, seals, and thermal components across mass-production models.

Trend 2: Ceramic-Based Exhaust Gas Sensors Surge in Demand Under Real-Driving Emissions (RDE) Enforcement

Global emissions legislation—driven by Euro 7, China 6b, and tightening U.S. real-world compliance protocols—is dramatically increasing the sophistication and volume of exhaust gas sensors required per vehicle. Modern vehicles must now operate under Real-Driving Emissions (RDE) conditions, where dynamic temperature changes, transient loads, and real-time monitoring necessitate highly durable, fast-response ceramic sensor systems.

Zirconia-based planar oxygen (λ) sensors remain the industry standard due to their solid-state electrolyte functionality at high temperatures, providing unmatched accuracy in controlling the air–fuel ratio and optimizing combustion. As Euro 6 and China 6 frameworks require multiple oxygen and particulate matter sensors throughout the aftertreatment chain, the total ceramic sensor content per vehicle has expanded significantly. Wider adoption of wideband O₂ sensors, particulate matter sensors, and NOx sensors is creating a sustained high-volume demand for automotive-grade zirconia ceramics.

The transition toward multi-sensor arrays reflects not only regulatory mandates but also OEM strategies to avoid compliance penalties and improve long-term engine durability. As Euro 7 further tightens limits on NOx, PM, and ammonia slip, ceramic sensor manufacturers will remain central suppliers in the vehicle emissions ecosystem.

High-Value Opportunities Emerging in the Automotive Ceramics Market

Opportunity 1: Ceramic Matrix Composites (CMCs) Enable Next-Generation Braking Systems for Heavy and High-Performance EVs

The electrification trend has exposed the limitations of traditional cast-iron braking systems, particularly in heavy EVs where mass increases and regenerative braking reduces friction brake usage. This creates a prime opportunity for Ceramic Matrix Composite (CMC) brake discs—particularly C/SiC variants—that offer transformative weight reduction, superior corrosion resistance, and unparalleled thermal stability.

CMC brake discs deliver 50%–61% lower unsprung weight than cast iron discs, significantly improving efficiency, handling dynamics, and overall driving range. Their durability is equally compelling: C/SiC discs offer service lives of up to 300,000 km, approximately four times longer than steel discs, and remain virtually unaffected by the corrosion challenges that plague conventional discs in low-use EV braking cycles.

Most importantly, ceramics maintain consistent friction coefficients even under extreme heat loads. C/SiC systems retain structural integrity and friction performance up to 2000°C, making them indispensable for high-performance EVs and heavy-duty electric trucks that require reliable braking under repeated high-energy stops. This superior performance profile positions CMC brake systems as a major commercial opportunity as performance, safety requirements, and vehicle weights continue to rise.

Opportunity 2: Ceramic Substrates and Power Electronics Packaging for High-Temperature, High-Power EV Architectures

As the automotive industry shifts to 800V+ vehicle architectures, power electronics must dissipate increasing thermal loads while remaining compact, efficient, and highly reliable. This has created a rapidly expanding opportunity for ceramic substrates—especially Aluminum Nitride (AlN)—that combine electrical insulation with exceptional thermal conductivity.

AlN substrates offer thermal conductivities of 170–180 W/m·K, which is up to 9.5× higher than alumina (Al₂O₃) and essential for heat removal in SiC and GaN power device modules. The material’s Coefficient of Thermal Expansion (CTE) of ~4.7 ppm/K is nearly identical to that of SiC and Si chips, minimizing solder joint stress during extreme thermal cycling in inverters and DC-DC converters. This significantly enhances long-term module reliability and reduces the risk of fatigue-related failures.

Multilayer AlN substrates further accelerate miniaturization. According to TDK, AlN enables 5× smaller module footprints compared to Si₃N₄ and up to 12× smaller compared to Al₂O₃ for the same thermal power, allowing OEMs to design more compact inverters and power control units critical for next-generation EV platform architecture.

As EV power density continues rising, ceramic substrates will remain central to enabling compact, thermally efficient, and highly reliable automotive power electronics.

Automotive Ceramics Market Share Analysis

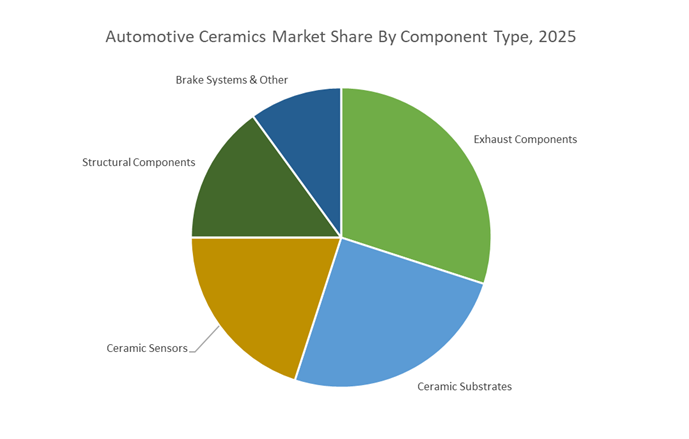

Market Share by Component Type: Exhaust Components Lead with 30.7% Share

Exhaust components—including ceramic substrates and particulate filters—hold the largest share of the Automotive Ceramics Market at 30.7% in 2025, reflecting their longstanding role as essential elements of internal combustion engine (ICE) emissions control systems. Their dominance is rooted in decades of regulatory tightening around NOx, PM, and HC emissions, which elevated ceramics such as cordierite, silicon carbide (SiC), and aluminum titanate into mission-critical materials for catalytic converters and diesel particulate filters. This entrenched demand persists because the global vehicle fleet remains heavily ICE-dependent, ensuring high replacement cycles and continued OEM adoption. However, the segment’s future trajectory is defined by a structural market transition: ceramic power electronics substrates (AlN, Si₃N₄) are rapidly emerging as the performance backbone of electric vehicle (EV) inverters and onboard chargers, ceramic sensors remain indispensable for combustion monitoring and emissions compliance, structural ceramics gain relevance for high-speed EV bearings and friction-reduction in ICE systems, and ceramic brake discs continue as a premium motorsport niche. The segmentation highlights a market in dual motion—legacy exhaust ceramics anchoring current volume while EV-ready ceramic technologies accelerate long-term value creation.

Market Share by Vehicle Type: Passenger Vehicles (ICE & Hybrid) Lead with 48.1% Share

Passenger Vehicles (ICE & Hybrid) command the largest share at 48.1% in 2025, driven by the sheer scale of the global internal combustion fleet and the continued demand for ceramic-enabled components in emissions control, sensing, thermal insulation, and efficiency improvement systems. Despite the rapid growth of battery electric vehicles (BEVs), ICE and hybrid platforms still dominate global production volumes—sustaining robust demand for ceramic substrates, oxygen sensors, DPF/SCR filters, spark-plug insulators, and high-strength structural ceramics. The segment’s leadership is reinforced by regulatory pressure in emerging economies, where emissions standards increasingly mandate ceramic-based filtration and catalyst technologies. Meanwhile, the broader vehicle mix signals a profound technological shift: BEVs represent the fastest-growing ceramic demand center, particularly for power electronics substrates, high-voltage insulation, battery system ceramics, and advanced thermal management components; commercial vehicles remain the volume backbone for diesel exhaust ceramics due to long duty cycles and heavy-load operations; and high-performance vehicles continue to push the frontier of ceramic brakes and ultra-lightweight structural components. Overall, the market reflects a dual-phase adoption cycle—ICE-driven ceramic demand sustaining short- to mid-term volume, while EV-driven ceramics unlock the next wave of high-margin, performance-critical growth.

Country Analysis: Global Automotive Ceramics Market Innovation Hubs

Germany (Europe): Advancing E-Mobility Through High-Voltage Ceramic Substrates and Digital Manufacturing Integration

Germany continues to anchor Europe’s leadership in automotive ceramics, leveraging its engineering excellence, EV transition momentum, and deep expertise in high-precision manufacturing. German automotive suppliers are intensifying development of metallized ceramic substrates and ceramic heat sinks designed to dissipate the extreme thermal loads of 800V SiC and GaN power modules used in next-generation EV drivetrains. These thermally conductive substrates enable superior heat spreading, electrical insulation, and long-term reliability—critical requirements for high-performance electric vehicles.

Government programs have accelerated this transformation. Germany’s historic €1.5 billion automotive support programme (through 2024) has strengthened industry-wide digitalization and environmentally aligned production investments, directly benefitting ceramic component suppliers across the EV value chain. The country is also pushing boundaries in additive manufacturing for technical ceramics, with the “Germany Makes” initiative driving calls for dedicated AM mega-projects in 2026—essential for producing complex, customized ceramic automotive parts at industrial scale. Companies like CeramTec continue to dominate high-temperature ceramic component engineering, including zirconium oxide–based bearing bushes capable of stable performance at ~500°C. CeramTec’s partnership with the Fraunhofer IISB further strengthens Germany's position in ceramic-based thermal interface solutions supporting advanced E-Mobility cooling architectures.

Japan: Global Leader in Functional Ceramics for Automotive Sensors, Bearings, and Precision Engineered Components

Japan holds an unrivaled position in functional automotive ceramics, driven by decades of materials excellence in sensors, ignition components, and high-speed rotating systems. Japanese manufacturers such as NGK Spark Plug and Kyocera dominate global volumes of zirconium oxide–based Lambda sensors, particulate matter sensors, and NOx sensors—technologies that remain indispensable for meeting increasingly stringent global emissions regulations. These ceramic sensors provide high sensitivity, chemical resistance, and accuracy across extreme temperature ranges.

Japan is also advancing high-performance silicon nitride (Si₃N₄) ceramics, particularly for bearing rollers in turbochargers and electric motor systems where low friction, high strength, and high-speed reliability are essential. To support expanding global demand, Kyocera secured land for a new fine ceramics plant in Nagasaki (April 2023), reinforcing long-term manufacturing capacity for advanced ceramic components used in EVs, ADAS sensors, and smart mobility platforms. Japan’s functional ceramics leadership is consistently showcased at events such as CES Mobility, where Kyocera presents innovations in autonomous driving optics, LiDAR components, and robust sensor housings designed for harsh automotive environments. With continuous advancement across sensing, actuation, and lightweight ceramic engineering, Japan remains at the forefront of next-generation automotive ceramics.

United States: Driving CMC Adoption and Ceramic Safety Solutions for High-Density EV Battery Platforms

The United States is emerging as a high-growth innovation hub for Ceramic Matrix Composites (CMCs), high-temperature structural ceramics, and EV battery safety materials. U.S. companies remain leading suppliers of ceramic monolith carriers—typically cordierite or alumina—which enable catalytic converter efficiency and form the structural backbone of Diesel Particulate Filters (DPFs). These ceramic substrates are engineered for high surface area, thermal shock resistance, and durability under rapid heating cycles.

As EV adoption accelerates, American ceramic manufacturers and global suppliers with US operations are intensifying efforts in ceramic-based battery safety components, including ceramic separators, thermal barriers, insulating sleeves, and ceramic-coated plates designed to mitigate thermal runaway risks. These advanced ceramics play critical roles in preventing internal short circuits, improving heat spreading, and enhancing crash resilience in high-energy battery packs. Research into CMC brake disks, turbine parts, and lightweight ceramic structural components continues at national laboratories and aerospace–automotive collaborative programs, positioning the U.S. as a key player in ultra-high-temperature and performance-critical automotive ceramic solutions.

South Korea: Innovating Ceramic Substrates and Battery Safety Materials for High-Voltage EV Architectures

South Korea’s dominance in batteries and electronics is fueling rapid innovation in automotive ceramic substrates, insulators, and ceramic-based heater technologies. With Korean automakers and battery manufacturers shifting aggressively toward 800V EV powertrains, the demand for highly reliable ceramic insulators, bushings, and dielectric components has surged. These ceramics must withstand intense electrical loads, fast charging cycles, and elevated thermal stress—making advanced alumina and silicon nitride ceramics integral to Korean EV drivetrain systems.

South Korea is also a global innovation leader in PTC (Positive Temperature Coefficient) ceramic heaters, which serve as efficient, self-regulating heating solutions for electric vehicles. As EVs lack combustion-based waste heat, PTC ceramic heaters provide precise cabin heating, battery warm-up functionality, and thermal conditioning for electronics. This makes them essential components in cold-weather EV performance and occupant comfort. With its strong electronics ecosystem and world-leading battery manufacturers, South Korea continues to scale advanced ceramic materials as core enablers of next-generation electric mobility.

Competitive Landscape: Supplier Differentiation by Thermal, Sensor and Wear Expertise

The competitive field in Automotive Ceramics is led by companies combining high-purity powder metallurgy, precision forming, additive manufacturing and strong automotive qualification track records. Leaders differentiate on substrate thermal conductivity, sensor ceramic purity, ceramic bearing composition, and AM-enabled complex geometry production, each critical to OEM adoption in EV, ICE-hybrid and high-reliability applications.

Kyocera Corporation - Fine-ceramic breadth enabling SiC substrates, sensors and AM production

Kyocera is a global leader in fine ceramics with product lines spanning Si₃N₄ bearings, AlN/SiN ceramic substrates and advanced sensor ceramics for ADAS and exhaust systems. Recent European investments (Waiblingen production site, Selb SiSiC 3D printing capability, and Erfurt technology expansion) strengthen Kyocera’s local supply for automotive customers and enable complex geometry components for thermal management and turbocharger applications. Kyocera’s strategy to bridge medical, semiconductor and automotive ceramics delivers cross-industry process maturity and scale for OEM qualification.

CeramTec GmbH - Specialist in high-performance alumina/zirconia and bespoke power-module materials (Sinalit)

CeramTec focuses on engineered alumina, zirconia and SiC solutions for wear, insulation and power electronics. The June 2025 launch of Sinalit positions CeramTec as a preferred supplier for custom EV power modules requiring high dielectric strength and thermal handling at elevated junction temperatures. CeramTec leverages additive manufacturing and near-net-shape forming to reduce finishing time and cost for complex automotive wear parts, accelerating design-for-manufacture cycles for OEMs.

NGK Spark Plug Co., Ltd. (Niterra) - Sensor ceramics and ignition expertise for emissions compliance

NGK (Niterra) is a global authority in zirconia and alumina sensor elements (lambda, NOx) and igniter ceramics, with extensive OE penetration in ICE and hybrid platforms. The company is pivoting ceramic expertise into new mobility and clean-energy fields (solid-state batteries, high-precision emission sensors), ensuring continued relevance as regulatory pressure (Euro 7/CAFE) tightens and as hybrid architectures persist in the market mix.

CoorsTek, Inc. - High-purity alumina and SiC components with sustainability improvement focus

CoorsTek supplies high-purity alumina, zirconia and SiC parts used for DPF substrates, wear components and thermal protection. Its integration across powder-to-finished-part processing and active sustainability targets (scope emission reductions) make it an attractive partner for OEMs emphasizing low-carbon supply chains. CoorsTek’s diversified proprietary formulations (400+ materials) allow rapid material tailoring to specific EV inverter and sensor applications.

Morgan Advanced Materials plc - Piezoelectric ceramics and high-temperature sealing for electrification

Morgan Advanced Materials specializes in piezoelectric ceramics for sensors and ceramic-metal seals for high-voltage systems. Its strategic focus on electrification components (e.g., ceramic seals for HV battery pack interfaces) and high-reliability mechanical seals supports EV thermal management and longevity targets. Morgan’s capability to produce low-friction sealing components that withstand operating temperatures around 500°C is particularly relevant for hybrid exhaust and turbocharger assemblies.

Saint-Gobain S.A. - Powder and grain supplier powering DPF substrates and high-temperature insulation

Saint-Gobain is a major supplier of fused alumina, SiC grains and specialty powders that serve as the feedstock for DPF/GPF substrates and high-temperature insulating ceramics. The company’s emphasis on decarbonization and industrial heat-recovery aligns with OEM demands for energy-efficient manufacturing and robust filtration media; its global supply footprint supports scale for tier-1 ceramic part manufacturers.

Automotive Ceramics Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5.3 Billion

|

|

Market Size (2035)

|

$9.4 Billion

|

|

Market Growth Rate

|

5.9%

|

|

Segments

|

By Component Type (Ceramic Substrates, Ceramic Sensors, Engine Components, Exhaust Components, Brake Systems, Bearings, Seals & Valves), By Material Type (Alumina Oxide Ceramics, Zirconia Oxide Ceramics, Silicon Nitride Ceramics, Silicon Carbide Ceramics, Titanate Oxide Ceramics, Cordierite), By Vehicle Type (Passenger Vehicles, Commercial Vehicles, High-Performance Vehicles), By Application Function (Emissions Control, Thermal Management, Power Electronics, Structural/Mechanical, Safety)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Kyocera Corporation, CeramTec GmbH, NGK Spark Plug Co. Ltd., Morgan Advanced Materials plc, CoorsTek Inc., Murata Manufacturing Co. Ltd., Saint-Gobain S.A., SCHOTT AG, Bosch Group, Corning Incorporated, Denso Corporation, 3M Company, Vesuvius plc, F. X. Stöhr GmbH & Co. KG, H.C. Starck GmbH

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Automotive Ceramics Market Segmentation

By Component Type

- Ceramic Substrates

- Ceramic Sensors

- Engine Components

- Exhaust Components

- Brake Systems

- Bearings

- Seals and Valves

By Material Type

- Alumina Oxide (Al₂O₃) Ceramics

- Zirconia Oxide (ZrO₂) Ceramics

- Silicon Nitride (Si₃N₄) Ceramics

- Silicon Carbide (SiC) Ceramics

- Titanate Oxide Ceramics

- Cordierite

By Vehicle Type

- Passenger Vehicles

- Commercial Vehicles

- High-Performance Vehicles

By Application Function

- Emissions Control

- Thermal Management

- Power Electronics

- Structural / Mechanical

- Safety

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Automotive Ceramics Market

- KYOCERA Corporation

- CeramTec GmbH

- NGK Spark Plug Co., Ltd.

- Morgan Advanced Materials plc

- CoorsTek, Inc.

- Murata Manufacturing Co., Ltd.

- Saint-Gobain S.A.

- SCHOTT AG

- Bosch Group

- Corning Incorporated

- Denso Corporation

- 3M Company

- Vesuvius plc

- F. X. Stöhr GmbH & Co. KG

- H.C. Starck GmbH

*- List not Exhaustive