Market Overview: Strong Demand for BSK and BHK Pulp Drives Global Expansion

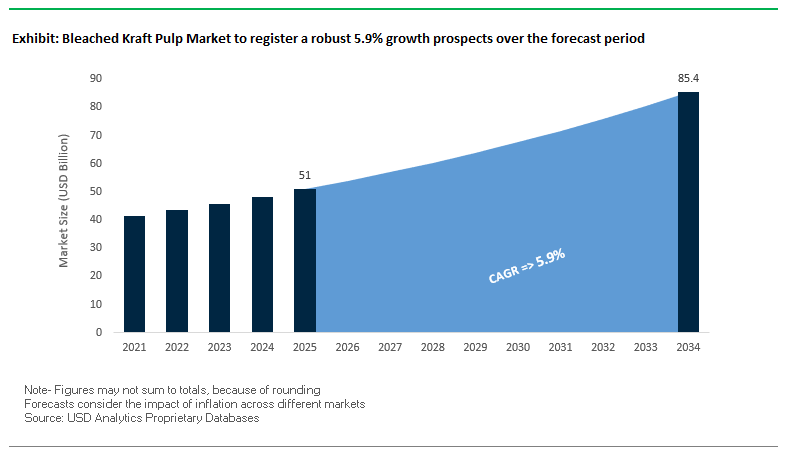

The global bleached kraft pulp market is projected to grow from USD 51 billion in 2025 to USD 85.4 billion by 2034, reflecting a steady CAGR of 5.9%. This growth trajectory is fueled by the rising demand for both bleached softwood kraft (BSK) pulp and bleached hardwood kraft (BHK) pulp, which serve distinct yet complementary roles across paper, packaging, tissue, and specialty applications. For industry professionals, the critical questions revolve around China’s role as the largest consumer, the shift toward dissolving pulp for textiles, and the increasing energy efficiency of modern bioproduct mills.

BSK pulp, derived from long softwood fibers, is essential for high-strength applications such as packaging papers and specialty grades requiring durability. In contrast, BHK pulp, largely sourced from eucalyptus, offers superior smoothness and printability, making it the preferred choice for printing, writing, and tissue papers. A notable trend reshaping the market is the rise of dissolving pulp, which supports growth in the textile and rayon industries, expanding the scope of pulp beyond traditional paper products. The industry is also witnessing a transformation toward bioenergy and carbon capture, with cutting-edge mills like Metsä Group’s Kemi facility demonstrating 250% energy self-sufficiency and full fossil-free operations.

Key Insights for Industry Leaders:

- BSK pulp dominates strength-based applications, while BHK pulp leads in smoothness and printability.

- China accounts for more consumption than Europe, North America, and Latin America combined.

- Dissolving pulp is an emerging high-growth segment linked to the global textile industry.

- Next-generation bioproduct mills are reshaping sustainability standards with high energy self-sufficiency and fossil-free operations.

Market Analysis: Recent Industry Developments Reshaping Supply and Profitability

The global bleached kraft pulp industry is experiencing a dynamic phase marked by portfolio restructuring, mill closures, expansions, and price adjustments. In August 2025, International Paper announced the sale of its Global Cellulose Fibers business for USD 1.5 billion, signaling its pivot toward core sustainable packaging operations. In the same month, Metsä Board launched a profitability program targeting an annual EBITDA uplift of €200 million by 2027, supported by efficiency gains and a stronger commercial focus.

Major consolidation has also influenced the broader pulp and materials sector. In July 2025, the USD 13.4 billion acquisition of Nova Chemicals by Borouge Group International marked a significant milestone in chemicals and packaging integration, indirectly impacting pulp supply chains. Metsä Board continued reshaping its footprint with a €60 million modernization at its Simpele mill in July 2025, even as it closed its Tako board mill in Finland in June 2025 to enhance competitiveness. Earlier, in April 2025, European pulp producers announced price hikes for both BEK and NBSK pulp, underlining inflationary pressures and tightening supply.

A strong emphasis on sustainability and operational efficiency also emerged in 2024. Metsä Group’s Kemi bioproduct mill completed its first year of production in September 2024, producing 1.5 million tonnes annually while operating on fossil-free energy. Meanwhile, industry forecasts in March 2025 highlighted the critical role of strategic downtime in balancing pulp markets, particularly as new hardwood capacity entered the supply chain.

Trends and Opportunities Redefining the Bleached Kraft Pulp Market

Strategic Capacity Expansion in South America Focused on Sustainable Hardwood Pulp

The bleached kraft pulp (BKP) market is witnessing a decisive wave of capacity expansion in South America, particularly in Brazil, as global producers target cost competitiveness and sustainable supply. Brazil has emerged as the epicenter of this growth due to its favorable climate for fast-growing eucalyptus plantations and established forestry expertise. CMPC’s “Project Natureza,” a proposed 2.5 million tonnes/year mill slated for board approval in 2026, illustrates this trend, aiming to strengthen the company’s position in the global bleached hardwood kraft pulp (BHKP) market. Beyond volume growth, these investments prioritize sustainability by incorporating practices such as reduced water consumption, enhanced carbon sequestration, and compliance with global eco-certifications. As demand for tissue, packaging, and specialty paper rises across Asia and other emerging markets, South America’s new capacity will play a critical role in supplying cost-competitive pulp while meeting strict sustainability requirements. This regional expansion underscores the shift toward geographically concentrated, large-scale, and environmentally responsible pulp production hubs.

Accelerated Adoption of Biomass Energy Systems and Carbon Capture Readiness

A parallel trend shaping the BKP market is the integration of advanced energy and carbon management systems into pulp mills. Modern kraft pulp operations are increasingly energy self-sufficient, deriving most of their energy from biomass by-products such as black liquor combusted in recovery boilers. The next step is biorefinery integration, where mills produce not just pulp but also biofuels, bio-based chemicals, and energy, increasing carbon conversion efficiency from 48% to as high as 67%. This positions pulp mills as multi-output industrial hubs capable of serving the bioeconomy while lowering operational costs. In addition, mills are preparing for carbon-constrained futures by investing in carbon capture and utilization (CCU) technologies. Research suggests that kraft pulp mills hold significant potential for biogenic CO₂ capture, which, when paired with carbon storage, could transform these facilities into net-negative emission sites. These investments not only secure compliance with tightening carbon regulations but also open pathways for new revenue streams through carbon credits and renewable energy products.

Development of Pulp-Based Bioproducts for Plastic Replacement

The bleached kraft pulp industry is uniquely positioned to contribute to the global bioeconomy by developing bioproducts that directly replace petroleum-based plastics. Specialty cellulose derived from BKP, particularly dissolving pulp, can be transformed into regenerated cellulose films with exceptional oxygen barrier properties, making them ideal for sustainable packaging. Molded pulp, created from renewable lignocellulosic fibers, is also gaining ground as an alternative to expanded polystyrene (EPS) in protective and food packaging. Its biodegradability, recyclability, and performance attributes are attracting consumer goods companies eager to align with plastic reduction mandates. Beyond packaging, dissolving pulp is being applied to the textile industry, producing bio-based fibers that reduce microplastic pollution from synthetic fabrics. By diversifying into these high-growth verticals, BKP producers can expand their role beyond traditional paper applications, positioning themselves as core suppliers to industries driving the global transition to sustainable materials.

Supply Chain Localization and Nearshoring of Critical Packaging Materials

The BKP market is also benefiting from a shift toward localized and regionalized supply chains in response to geopolitical risks, logistics disruptions, and consumer sustainability demands. North American and European manufacturers are actively pursuing nearshoring strategies to secure stable supplies of critical packaging pulp, reducing reliance on distant and geopolitically sensitive regions. Europe, in particular, has become increasingly dependent on hardwood pulp imports due to slower tree growth rates and stricter local forestry regulations. Since 2020, South American exports of hardwood pulp to Europe have grown by 19%, reinforcing the importance of regional partnerships. At the same time, consumer-facing brands are under pressure to reduce the carbon footprint of their sourcing practices and enhance supply chain transparency. By sourcing pulp closer to end markets, companies can deliver on both resilience and sustainability commitments, while suppliers in North and South America stand to benefit from their favorable resource bases and political stability.

Competitive Landscape: Leading Global Players in Bleached Kraft Pulp

The competitive environment in the bleached kraft pulp industry is shaped by global pulp leaders with vertically integrated operations, advanced sustainability strategies, and strong market diversification.

Suzano S.A.: Global Leader in BEK Pulp with Regenerative Practices

Suzano is the world’s largest producer of bleached eucalyptus kraft (BEK) pulp, supplying tissue, printing, and packaging industries. Its vertically integrated model, built on vast eucalyptus plantations, provides supply chain stability and low carbon intensity. Suzano’s “Renewing Life” strategy aligns with 15 UN SDGs, while its forest restoration programs in Brazil reinforce its regenerative economy leadership.

Metsä Group: Driving Bioenergy and Carbon Capture through Bioproduct Mills

Metsä Group, through Metsä Fibre, is a key producer of softwood and hardwood pulp. Its Kemi bioproduct mill, a €2.02 billion investment, produces 1.5 million tonnes annually while achieving 250% electricity self-sufficiency. Metsä is advancing carbon capture projects with ANDRITZ, targeting millions of tonnes of CO₂ annually, positioning itself as a sustainability frontrunner.

International Paper Company: Portfolio Restructuring Toward Sustainable Packaging

International Paper remains a leading producer of pulp for diapers, hygiene, and specialty applications. In August 2025, it sold its GCF business for USD 1.5 billion, redirecting focus to fiber-based packaging. With its 2025 merger with DS Smith, IP strengthened its positions in North America and EMEA, while a USD 250 million investment at Riverdale Mill supports its containerboard conversion strategy.

Paper Excellence Group: Rapid Expansion via Strategic Acquisitions

Paper Excellence has emerged as one of North America’s largest pulp producers through acquisitions, including Catalyst Paper in 2019, Domtar in 2021 (USD 3 billion), and Resolute Forest Products in 2023 (USD 2.7 billion). Its diversified portfolio supports printing, packaging, and specialty pulp applications, backed by a broad manufacturing footprint and strong market presence in Canada and the U.S.

Canfor Corporation: Supplier of High-Strength NBSK Pulp

Canfor, through Canfor Pulp, is a significant producer of northern bleached softwood kraft (NBSK) pulp, prized for strength-based paper and packaging products. Its vertically integrated model ensures secure supply from sustainably managed forests. In mid-2025, Canfor announced the closure of two sawmills in South Carolina to optimize efficiency, while strengthening its European footprint with increased ownership of Vida AB in Sweden.

Bleached Kraft Pulp Market Share Insights

Packaging Paper Dominates Bleached Kraft Pulp Market Share by Application

Packaging paper leads the bleached kraft pulp (BKP) market by application with 48% share in 2025, reflecting the global boom in e-commerce and consumer demand for sustainable, recyclable paper-based packaging. BKP’s long, strong softwood fibers are critical for containerboard and cartonboard production, providing the strength, crush resistance, and durability essential for logistics-intensive supply chains. Tissue paper follows with 35% share, anchored by steady demand for hygiene products such as toilet paper, napkins, and paper towels, particularly in emerging economies where hygiene standards are rapidly rising. Graphic paper, once a cornerstone of BKP consumption, now reflects a structural decline due to digitization, with its presence limited to high-brightness, premium printing papers. Specialty papers, including filters, labels, and security papers, form a small but high-value niche where purity and performance characteristics make BKP indispensable. Newsprint, accounting for a negligible fraction, underscores the shift away from low-value applications as BKP is increasingly reserved for premium, high-strength, and hygienic paper products.

Food & Beverages Drive MDO PE Films Market Share by End-Use Industry

Food and beverages represent the largest share of the MDO PE films market by end-use industry in 2025, cementing their position as the core growth driver for mono-material packaging solutions. MDO (machine-direction orientation) technology enhances the stiffness, clarity, and barrier properties of polyethylene films, enabling their use in pouches, bags, and wraps that meet both consumer convenience needs and regulatory requirements for recyclability. This makes them particularly attractive for snack packaging, fresh produce, and dairy products. Pharmaceuticals and healthcare are another significant growth driver, leveraging MDO PE films for sterile blister overwraps and high-barrier medical packaging, while cosmetics and personal care adopt these films for lightweight, sustainable pouches that align with premium eco-friendly branding. Homecare and industrial applications round out the market, reflecting steady adoption in cleaning products and specialty packaging formats. The overarching driver across industries is the push for recyclable mono-material packaging structures that comply with global EPR regulations, positioning MDO PE films as a central innovation pathway in the shift away from multilayer, non-recyclable plastics.

United States: Driving Sustainable Packaging Demand Through Advanced Bleached Kraft Pulp

The U.S. bleached kraft pulp market is witnessing robust growth, driven by evolving consumer and corporate preferences for sustainable and recyclable packaging solutions. Demand is particularly strong in sectors such as hygiene products, corrugated boxes, and food packaging, where high-quality fiber is critical. Technological advancements are reshaping production, with the American Forest & Paper Association (AF&PA) reporting over $4.5 million in investments from 2019 to 2025 toward building new mills, modernizing equipment, and enhancing pulping technologies.

Sustainability initiatives are further supported by the U.S. Environmental Protection Agency (EPA), which has launched three new programs aimed at waste prevention, reuse, and recycling, under the Infrastructure Investment and Jobs Act. The boom in e-commerce has also fueled the use of fiber-based packaging, helping companies meet ESG (Environmental, Social, and Governance) standards. Major corporations like International Paper and WestRock are actively promoting sustainable forestry and production practices, aligning corporate strategies with environmental responsibility and boosting demand for bleached kraft pulp across multiple applications.

Germany: Regulatory Leadership and Circular Economy Driving High-Quality Pulp Adoption

Germany’s bleached kraft pulp industry is governed by a stringent regulatory framework, including the EU Packaging and Packaging Waste Regulation (PPWR) 2025, which mandates the use of eco-friendly and highly recyclable materials. The market benefits from Germany’s leadership in the circular economy, with extensive collaboration between manufacturers and end-users, making the country one of the top collectors and processors of waste paper for recycled pulp production.

Technological innovation is a key growth driver. Automated recycling facilities and advanced fiber recovery systems enable the production of high-quality bleached kraft pulp suitable for food and beverage packaging. Government mandates, alongside studies on waste utilization in sectors like textiles, demonstrate that companies are repurposing byproducts to create value-added products, reinforcing Germany’s position as a leader in sustainable pulp production.

China: Dual Carbon Goals and Technological Integration Fuel Bleached Kraft Pulp Growth

China’s bleached kraft pulp market is strongly influenced by the government’s dual carbon objectives, aiming to achieve carbon peak and carbon neutrality, which is accelerating the green transformation of the paper and packaging industry. Investments in automation, AI, and the “5G plus industrial internet” are optimizing production efficiency and enabling flexible pulp manufacturing processes.

The rise of e-commerce in Tier 2 and 3 cities has increased demand for secure and tamper-proof packaging, boosting the consumption of bleached kraft pulp. Additionally, the ban on unsorted solid waste imports has forced domestic mills to source recycled paper locally, improving collection and processing infrastructure. Sustainability is further reinforced by China’s national carbon trading market, where companies are incentivized to monetize eco-friendly performance, positioning the market for long-term environmentally conscious growth.

India: Government Initiatives and Industrial Investments Strengthen Pulp Market

India’s bleached kraft pulp market is benefiting from government programs like Make in India and Zero Effect Zero Defect, which encourage high-quality domestic production and provide regulatory support. Infrastructure development, including the creation of seven mega textile parks under the PM MITRA scheme, is enhancing manufacturing capabilities and boosting pulp production.

Growth in food processing and e-commerce sectors is driving demand for affordable, protective, and eco-friendly packaging. Sustainability is prioritized through GST reforms that reduce the tax on paper pulp molded trays to 5%, promoting cost-effective solutions for businesses. Companies are investing in advanced machinery and alternative raw materials like rice husk and bagasse to improve efficiency and product quality. These initiatives, combined with rising industrial demand, are positioning India as a key emerging market for bleached kraft pulp.

Brazil: Strategic Investments and Regulatory Support Foster Sustainable Pulp Growth

Brazil’s bleached kraft pulp market is strongly supported by the National Solid Waste Policy, which encourages reusable and durable alternatives. Technological advancements, including robotics and AI, are enhancing efficiency, quality control, and production sophistication in pulp manufacturing.

Significant investments, such as Suzano’s $4 billion fossil-free pulp plant with an annual capacity of 2.55 million tons, are ensuring a sustainable supply of raw materials. The solid waste import ban of January 2025 encourages domestic collection and processing, strengthening the circular economy. These developments collectively boost the adoption of high-quality bleached kraft pulp for packaging and industrial applications.

Japan: Innovation in Functionality and Bio-based Materials Leading Pulp Market

Japan’s bleached kraft pulp industry is supported by advanced recycling systems, enforced through the Containers and Packaging Recycling Law, ensuring efficient collection and reuse of waste materials. The market is also embracing bio-based materials, exemplified by innovations like Spiber’s Brewed Protein™, which offers sustainable alternatives for packaging applications.

Continuous innovation focuses on enhancing pulp functionality, including high dimensional stability and resistance to deformation, meeting the demands of high-performance applications in electronics and premium goods. Japan’s strong focus on sustainability, technological advancement, and high-quality production establishes it as a global leader in bleached kraft pulp manufacturing.

Bleached Kraft Pulp Market Report Scope

Bleached Kraft Pulp Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$51 Billion

|

|

Market Size (2034)

|

$85.4 Billion

|

|

Market Growth Rate

|

5.9%

|

|

Segments

|

By Pulping Process (Chemical, Mechanical, Semi-Chemical), By Bleaching (ECF, TCF, Chlorine Bleaching), By Grades (BHKP, BSKP), By Application (Packaging Paper, Tissue Paper, Graphic Paper, Specialty Paper, Newsprint Paper)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

International Paper, Suzano S.A., WestRock, Smurfit Kappa Group, Stora Enso Oyj, Mondi Group, UPM-Kymmene Oyj, Nine Dragons Paper Holdings Limited, Oji Holdings Corporation, Nippon Paper Industries Co., Ltd., Asia Pulp & Paper (APP), Resolute Forest Products, Domtar Corporation, BillerudKorsnäs AB, Bracell S.A.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Bleached Kraft Pulp Market Segmentation

By Pulping Process

- Chemical

- Mechanical

- Semi-Chemical

By Bleaching

- ECF

- TCF

- Chlorine Bleaching

By Grades

By Application

- Packaging Paper

- Tissue Paper

- Graphic Paper

- Specialty Paper

- Newsprint Paper

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Bleached Kraft Pulp Market

- International Paper

- Suzano S.A.

- WestRock

- Smurfit Kappa Group

- Stora Enso Oyj

- Mondi Group

- UPM-Kymmene Oyj

- Nine Dragons Paper Holdings Limited

- Oji Holdings Corporation

- Nippon Paper Industries Co., Ltd.

- Asia Pulp & Paper (APP)

- Resolute Forest Products

- Domtar Corporation

- BillerudKorsnäs AB

- Bracell S.A.

*List not Exhaustive

Research Coverage

This comprehensive report by USDAnalytics investigates the global bleached kraft pulp market, examining breakthroughs in both softwood and hardwood pulp production, innovations in energy-efficient mills, and emerging opportunities in sustainable bioproducts. The analysis reviews historical performance from 2021 to 2024, forecasts market trends from 2025 to 2034, and highlights critical developments across product grades, pulping processes, and regional supply dynamics. This report is an essential resource for industry professionals seeking insights on capacity expansion in South America, adoption of dissolving pulp for textiles, carbon capture readiness, and next-generation bioenergy integration in pulp mills. It emphasizes strategic investments by leading producers such as Suzano, Metsä Group, International Paper, and Canfor, while analyzing supply chain localization trends, circular economy compliance, and innovations in molded pulp and sustainable packaging. USDAnalytics also provides a detailed competitive assessment of 15+ key companies, evaluating market positioning, portfolio strategies, and sustainability initiatives, making this study indispensable for executives, procurement managers, and investors aiming to capitalize on the evolving global bleached kraft pulp landscape.

Scope Highlights:

- Segmentation: By Pulping Process (Chemical, Mechanical, Semi-Chemical), By Bleaching (ECF, TCF, Chlorine Bleaching), By Grades (BHKP, BSKP), By Application (Packaging Paper, Tissue Paper, Graphic Paper, Specialty Paper, Newsprint Paper)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa

- Historic & Forecast Data: Historic data from 2021 to 2024; forecast data from 2025 to 2034

- Companies: Analysis/profiles of 15+ leading producers including International Paper, Suzano S.A., WestRock, Smurfit Kappa Group, Stora Enso Oyj, Mondi Group, UPM-Kymmene Oyj, Nine Dragons Paper, Oji Holdings, Nippon Paper Industries, APP, Resolute Forest Products, Domtar, BillerudKorsnäs AB, and Bracell S.A.

Methodology

The research methodology combines primary and secondary data sources, leveraging direct interviews with industry stakeholders, company reports, regulatory filings, and expert insights to ensure accuracy and relevance. Secondary data include trade associations, government publications, company press releases, and sustainability reports, which are cross-verified for reliability. The analysis employs quantitative techniques such as CAGR calculation, market share analysis, and demand forecasting, alongside qualitative evaluations of technological innovations, regulatory frameworks, and supply chain dynamics. USDAnalytics integrates a bottom-up approach for production and capacity assessment, coupled with top-down market validation to ensure consistency across geographies, pulping processes, grades, and applications. Scenario analysis evaluates risks and opportunities under varying energy, sustainability, and trade conditions, while market segmentation modeling provides actionable insights for strategic planning. This methodology ensures a robust, data-driven assessment suitable for executives, investors, and market analysts seeking high-quality intelligence on the global bleached kraft pulp market.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.