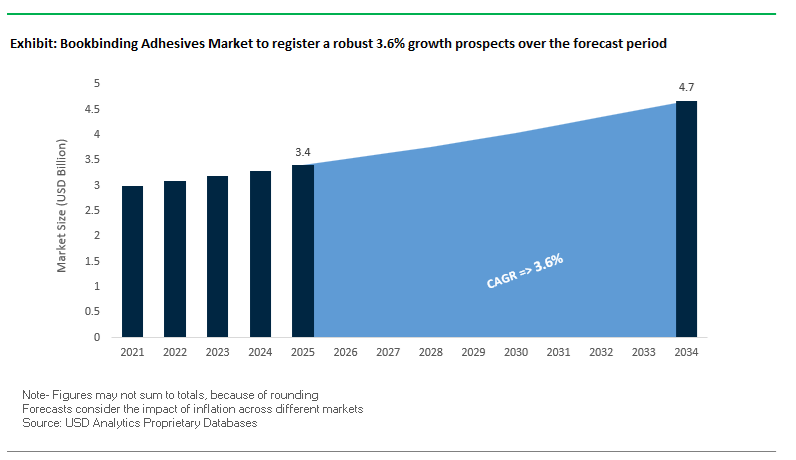

The global bookbinding adhesives market has become strategically relevant as print manufacturers, publishers, and graphic arts converters modernize production to meet durability, sustainability, and automation requirements simultaneously. Valued at USD 3.4 billion in 2025 and projected to reach USD 4.7 billion by 2034 at a CAGR of 3.6%, the market’s growth is anchored in the shift toward high-performance binding solutions that can support shorter print runs, export-grade durability, and increasingly automated finishing lines. Adhesives are no longer a consumable afterthought in book production; they are a structural component directly influencing product lifespan, rejection rates, and throughput economics.

The core structural shift reshaping demand is the transition from legacy EVA hot melts and solvent-borne systems to polyurethane reactive (PUR) hot melts and low-VOC water-based dispersion adhesives. PUR technology has become the benchmark for premium and demanding applications due to its ability to chemically react with ambient moisture and form crosslinked polymer networks after application. Manufacturer-qualified PUR bookbinding adhesives deliver bonding strengths exceeding 1,000 lbs and maintain adhesion across a wide service window from −30°C to 150°C, enabling reliable spine integrity for hardcovers, academic volumes, and export-oriented print jobs exposed to varied climate conditions. In parallel, water-based dispersion adhesives have become essential on sustainability-driven production lines, offering near-zero VOC emissions while maintaining compatibility with REACH and U.S. EPA workplace exposure limits. Emerging polyolefin-based hot melts are also gaining traction in high-speed perfect binding, where consistent viscosity, clean machining, and broad substrate tolerance—from 60 gsm uncoated text stock to 250 gsm coated covers—support higher line speeds and reduced waste.

These material substitutions deliver direct business outcomes for printers and publishers: longer book life cycles, fewer spine failures, reduced rework, and improved compliance without sacrificing productivity. PUR’s thermal flexibility and superior fiber tear translate into lower warranty claims and stronger brand reputation for publishers, while water-based systems improve operator safety and simplify environmental audits. Looking forward, competitive advantage in the bookbinding adhesives market will increasingly depend on formulation stability, supply consistency, and seamless integration with automated dispensing and monitoring platforms. The adoption of smart dispensing and condition-monitoring systems—such as AI-enabled maintenance tools integrated into adhesive application equipment—signals a market moving toward tighter process control, predictable uptime, and compliance-ready manufacturing aligned with the evolving expectations of professional print buyers and global publishers.

The bookbinding adhesives industry is undergoing a pivotal transition driven by performance optimization and sustainability-focused innovation. Market leaders are investing in renewable raw materials, smart application systems, and formaldehyde-free formulations to align with the evolving environmental and production standards of the global printing industry.

In August 2025, Super Bond Adhesives launched its Super Melt Galaxy 12, a polyolefin-based hot melt adhesive that delivers superior thermal stability and pull strength, positioning itself as a sustainable alternative to PUR in high-speed perfect binding lines. In the same month, the company announced that the Galaxy 12 formulation incorporates over 30% plant-derived polymers, underscoring the sector’s growing commitment to bio-based adhesives and circular material sourcing. Similarly, Henkel Adhesive Technologies (July 2025) introduced its “Debond-on-demand” adhesives—an innovation allowing reversible bonding for recycling and reusability, enabling circular production models within graphic arts and packaging sectors.

In June 2025, a scientific advancement showcased the use of polymeric nanoparticles (PNPs) containing anion-π functional groups to significantly enhance ink binder adhesion and dispersion stability, improving print durability in digital publishing. Earlier in February 2025, research on nano-Al₂O₃ dispersion additives demonstrated a 66% increase in scratch resistance for coated papers, a breakthrough supporting next-generation varnish and adhesive compatibility for print finishing.

From an industry collaboration perspective, Henkel and Celanese (November 2024) advanced their sustainability portfolio by co-developing CO₂-based waterborne adhesives, minimizing the carbon footprint across packaging and graphic material bonding. Additionally, H.B. Fuller’s acquisition of Sanglier Ltd. (September 2024) expanded its UK and European presence, enhancing its access to sprayable and flexible industrial adhesive technologies applicable to bookbinding. Henkel’s launch of its Easyflow® system (April 2024) marked a major milestone for process automation, offering reduced stringing, cleaner application, and faster melt flow, boosting operational efficiency across high-volume book production facilities.

The global bookbinding adhesives market is witnessing a decisive transition toward Reactive Polyurethane (PUR) and Low-VOC Hot Melt Adhesives, driven by performance, sustainability, and regulatory compliance factors. Studies have consistently demonstrated that PUR adhesives deliver 40–60% higher page-pull strength compared to traditional Ethylene-Vinyl Acetate (EVA) hot melts—an engineering advantage that makes them indispensable for long-life publications, including textbooks, high-use reference materials, and premium commercial prints. The substantial performance differential directly translates to superior mechanical durability, ensuring that bindings remain intact under repetitive use and challenging environmental conditions.

Beyond strength, PUR adhesives excel in adhesion versatility—a factor that is redefining quality benchmarks in the printing industry. Their unique chemical structure enables bonding to non-porous, coated, and digitally printed substrates, including UV-coated papers where EVA formulations traditionally fail due to ink migration and weak substrate penetration. As digital printing and specialty coatings dominate modern publishing, the property positions PUR as the adhesive of choice for next-generation printing and binding operations.

The industry’s pivot is further accelerated by tightening environmental regulations under frameworks like the European Union’s REACH directive, which mandates the reduction of hazardous chemical use in manufacturing processes. Adhesive producers are responding by developing low-VOC, water-based, and bio-based formulations that maintain high bonding performance while ensuring compliance with global emission standards. The regulatory momentum aligns with consumer preferences for sustainable materials, especially in eco-certified publishing and educational sectors.

From a performance standpoint, PUR also demonstrates unmatched temperature resistance, retaining flexibility and structural integrity across a wide operational range—from −40°F to 248°F (−40°C to 120°C)—compared to EVA’s limited thermal resilience. The property is essential for books exposed to varying climates and logistical environments, including global shipping and storage conditions. As a result, PUR-based bookbinding adhesives are not just enhancing mechanical longevity but are also setting new standards for thermal stability, environmental performance, and multi-substrate adhesion versatility—the three pillars defining the future of high-performance bookbinding.

As digital printing technologies dominate short-run and print-on-demand publishing, the need for adhesives compatible with digital inks and coatings has become one of the most influential product development drivers in the bookbinding adhesives market. Unlike conventional offset printing, digital printing often utilizes oil-based or toner-based ink systems that can migrate or interfere with the adhesive’s bonding interface, leading to delamination or discoloration over time. In response, specialized PUR formulations have been engineered with enhanced chemical resistance to prevent oil migration, maintaining consistent bond strength and avoiding the yellowing or brittleness observed in legacy adhesive systems.

A crucial innovation trend in the domain is production efficiency. While traditional PUR adhesives require up to 24 hours for complete chemical curing, new fast-set reactive formulations can achieve an initial tack in as little as 15 seconds, enabling immediate post-binding operations such as trimming, stacking, or packaging. The advancement dramatically enhances print-on-demand production speed, making it ideal for small-batch or customized book runs—a rapidly expanding market segment as global e-commerce and self-publishing platforms grow.

Parallel research in polyvinyl acetate (PVAc) adhesive technology is also contributing to the modernization of digital binding systems. Laboratory findings report that integrating nano-modified additives such as hydrophobic fumed silica can boost PVAc bonding strength by 10–26% while reducing strength variability by up to 71%. The improvement in bonding uniformity supports predictable adhesion quality across different paper stocks, which is essential for maintaining visual consistency and structural durability in short-run digital jobs.

As publishers and print service providers continue to invest in automation, these digitally compatible adhesive innovations—combining speed, precision, and chemical stability—are becoming indispensable to high-efficiency production environments. The trend drives the market’s evolution toward chemically engineered, hybrid adhesives designed for versatility, enabling seamless transition from traditional offset to fully digital print workflows without sacrificing quality or durability.

A niche yet rapidly expanding market opportunity exists within specialty and artisanal publishing, encompassing zines, artist books, and limited-edition print collections. The segment places a premium on aesthetic craftsmanship, flexibility, and archival stability, which creates a sustained demand for premium-grade bookbinding adhesives engineered for low-stress flexibility and material preservation. Institutions such as museums, art galleries, and national libraries are major consumers of archival adhesives that are chemically stable, reversible, and acid-free, ensuring long-term preservation without substrate degradation.

For the luxury publishing and fine-art printing sectors, adhesive flexibility and lay-flat performance are crucial design features. Artist books and exhibition catalogs often employ thick or folded paper substrates that require flexible, thin adhesive films to maintain a seamless reading experience and avoid cracking along the spine. In such applications, PUR adhesives and advanced water-based dispersion adhesives are ideal due to their ability to provide both structural durability and aesthetic uniformity.

The niche market also benefits from the convergence of sustainability and craftsmanship, where eco-friendly adhesive formulations offer an added marketing advantage. The combination of archival-grade chemical stability, tactile paper compatibility, and sustainable production credentials positions the sector as a lucrative high-margin opportunity for manufacturers developing specialty-grade and conservation-focused adhesive lines.

The global shift toward sustainable and recyclable book construction is creating a transformative opportunity for adhesive manufacturers. As publishers and printing houses align with corporate sustainability targets and extended producer responsibility (EPR) frameworks, the demand for repulpable adhesives—formulations that dissolve completely during paper recycling—has surged. These adhesives play a critical role in enabling fiber recovery and circularity within the paper value chain, ensuring minimal contamination during the repulping process and supporting the circular economy of printed materials.

Environmental legislation is intensifying the demand. Under the European Union’s packaging and recycling directives, bookbinding adhesives must comply with repulpability certification standards, ensuring that adhesives can be easily separated during the recycling process. Simultaneously, large publishers are seeking third-party certifications that validate the environmental compatibility and recyclability of their materials.

In response, adhesive producers are expanding their R&D investments in bio-based and repulpable materials, with industry reports indicating a 65% increase in R&D expenditure between 2017 and 2020 for low-VOC, water-soluble, and biodegradable adhesive innovations across paper and packaging sectors. These sustainability-driven formulations not only meet regulatory requirements but also cater to eco-conscious publishers seeking to enhance their ESG (Environmental, Social, and Governance) credentials.

Overall, the convergence of repulpability, recyclability, and regulatory compliance is redefining product design across the bookbinding adhesives industry. Manufacturers capable of developing adhesives that offer strong bonding performance while enabling post-consumer recyclability will gain a strategic edge in a market increasingly defined by sustainable material innovation and closed-loop production systems.

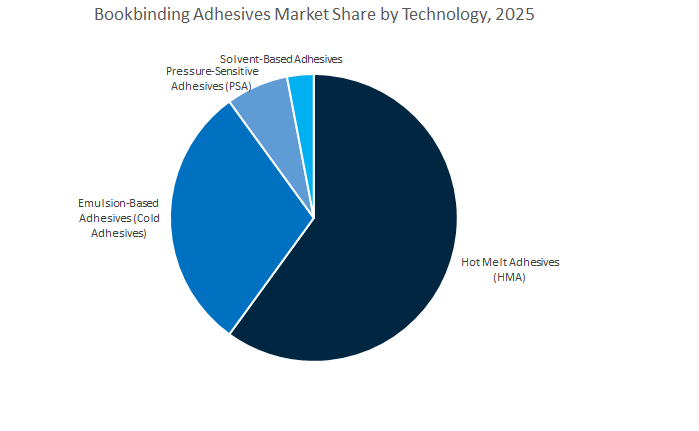

Bookbinding Adhesives Market Share Insights, 2025-2034

The Hot Melt Adhesives (HMA) segment dominates the global bookbinding adhesives industry, capturing nearly 60.8% of the total market share in 2025, primarily due to its unmatched efficiency, speed, and cost-effectiveness in large-scale, automated book production. HMAs, particularly Ethylene-Vinyl Acetate (EVA) and Polyolefin-based formulations, are indispensable in perfect binding and saddle stitching operations where rapid setting and immediate trimming capability are essential for productivity. Their ability to provide fast curing, minimal equipment downtime, and strong adhesion to coated and uncoated paper substrates makes them the default choice for mass-market paperback and magazine production lines. Additionally, reactive hot melts (PUR-based) are gaining ground within this segment, offering enhanced flexibility, superior page pull strength, and heat and cold resistance—key for high-quality publications and long-lasting binding. The growing adoption of HMAs aligns with the global trend toward energy-efficient, solvent-free adhesive systems, further reinforcing their dominant market position.

The Emulsion-Based Adhesives (Cold Adhesives) segment, holding around 30.6% of the market, plays a crucial role in applications requiring flexibility, precision, and long-term durability, such as hardcover and premium print products. Predominantly Polyvinyl Acetate (PVA) and Polyvinyl Alcohol (PVOH) emulsions, these adhesives offer excellent wet tack, superior aging properties, and an unmatched lay-flat capability that makes them ideal for case binding and endpaper attachment. The flexibility of these waterborne adhesives ensures that books can open and close repeatedly without cracking or delamination, extending product life—a key consideration for archival publications, textbooks, and library editions. In high-end publishing, dual adhesive systems (combining HMA for spine binding and emulsion for side gluing) have become standard to balance speed with aesthetic quality. Furthermore, the eco-friendly profile of emulsions—low VOCs, easy cleanup, and compatibility with paper recycling streams—supports their growing adoption in regions with stringent environmental standards, particularly across Europe and North America.

On the other hand, Pressure-Sensitive Adhesives (PSAs) and Solvent-Based systems account for a minimal share but serve specialized niches within the global bookbinding adhesives market. PSAs are primarily used for repositionable tabs, sticky notes, removable labels, and magazine inserts, where flexibility and user reusability are key. They are also gaining relevance in digital and custom publishing, where modular or interactive features are increasingly common. Solvent-Based adhesives, once widespread for their strong and instant bonds, have been largely phased out due to volatile organic compound (VOC) restrictions and occupational safety regulations, confining their use to specific industrial environments and high-strength specialty applications.

The Softcover Books (Paperbacks) segment leads the global bookbinding adhesives market, accounting for approximately 45% of total demand in 2025, reflecting the massive production volumes of educational, trade, and mass-market fiction books. This segment is highly cost-driven and dominated by EVA-based hot melt adhesives, which provide rapid setting and good adhesion even at high processing speeds. As global literacy initiatives, educational publishing, and the affordability of printed books continue to expand in emerging economies, paperback production remains a key volume contributor. Publishers and printers favor hot melt technologies for their high throughput, automation compatibility, and efficient energy use, allowing them to meet tight deadlines and competitive cost structures. Furthermore, the rise of perfect binding systems in both traditional and digital printing environments continues to anchor the dominance of hot melts in this segment.

The Magazines and Catalogs segment, while showing moderate growth, remains an important pillar of the market, driven by ongoing demand for advertising-driven print products, lifestyle publications, and corporate communications. This segment heavily relies on fast-curing hot melts for spine binding and pressure-sensitive adhesives for inserts and promotional attachments. Although digital media continues to erode market share, high-quality print catalogs and niche magazines are experiencing a resurgence as premium branding tools, supporting stable adhesive demand. The Hardcover Books (Case Binding) segment, On the other hand, represents the high-value end of the market, focusing on long life, durability, and superior aesthetics. This segment primarily uses PVA-based emulsion adhesives for casing-in and endpaper attachment, ensuring flexibility and resilience for premium publications like coffee-table books, corporate editions, and art collections. Publishers in this segment prioritize bond strength and long-term integrity over production speed, which keeps emulsion adhesives as the technology of choice.

The Print-on-Demand (POD) segment has emerged as the fastest-growing niche, reflecting the transformation of the publishing industry toward digital short-run and custom printing. POD manufacturers require adhesives that offer extended open time, strong adhesion to diverse substrates, and compatibility with compact, on-demand binding systems. Reactive PUR-based hot melts are gaining traction in this space for their superior adhesion to coated and digital print papers. Additionally, hybrid adhesive systems that combine the precision of emulsions with the speed of hot melts are increasingly adopted in short-run printing and self-publishing ecosystems, where flexibility and reliability are crucial.

The competitive landscape of the Global Bookbinding Adhesives Market is led by key multinational players such as Henkel AG & Co. KGaA, H.B. Fuller, Sika AG, DIC Corporation, and Bostik (Arkema Group). These companies dominate through continuous polymer innovation, high-speed process optimization, and eco-sustainable formulations designed for global publishing, packaging, and print finishing markets.

Henkel remains a pioneer in PUR and EVA-based adhesives optimized for both standard and digitally printed paper substrates. Its RE range, “Designed for Recycling,” reinforces its leadership in circular economy adhesives. The company’s Easyflow® system redefines process efficiency, minimizing application waste and thermal degradation. Henkel’s LOCTITE® Pulse technology brings predictive analytics to adhesive application systems, ensuring consistent performance in high-volume binding operations.

H.B. Fuller provides a comprehensive range of PUR, EVA, PSA, and waterborne adhesives for bookbinding applications including hardcover, softcover, and tipping. Its DM 20000 PSA formulation is renowned for low peel and stain resistance in direct mail and removable tipping. The company’s high-performance hot melts support high-speed production lines with excellent thermal stability and glue wheel compatibility.

Sika AG leverages its world-class polyurethane (PUR) chemistry expertise to develop adhesives offering superior flexibility, cohesion, and cold resistance for globally distributed publications. Its systems are designed for lay-flat binding and premium photobooks, maintaining durability in varying humidity and temperature conditions.

By integrating adhesive material and dispensing equipment systems, Sika ensures optimized bond performance and machine runnability. The company’s commitment to low-VOC, sustainable PUR innovations reflects a growing synergy between sustainability and performance in bookbinding.

DIC Corporation leads in reactive hot melt PUR technology, offering the TYFORCE H Series for durable, solvent-free bookbinding. Products such as TYFORCE FH-100 and FH-400 deliver high-speed processing and long open times suited for diverse machines and paper grades. DIC’s formulations combine low-temperature handling with superior moisture and heat resistance, meeting the evolving needs of high-performance industrial printing lines.

Bostik, part of Arkema Group, continues to strengthen its position in hot melt and water-based adhesive systems for perfect binding, casing-in, and spine gluing. Leveraging Arkema’s advanced polymer technologies, Bostik develops metallocene-based polyolefin adhesives known for thermal stability, reduced stringing, and superior page pull strength.

The company’s global focus on lay-flat durability and clean application caters to premium publishing, while its alignment with Arkema’s sustainability goals supports bio-based formulation expansion.

Country Analysis: Global Bookbinding Adhesives Industry

Germany continues to dominate the European bookbinding adhesives market through its advanced polymer technology innovation and regulatory compliance initiatives. Henkel AG & Co. KGaA, one of the world’s leading adhesive producers, has expanded its Technomelt portfolio, introducing next-generation hot melt adhesives designed for high-speed, energy-efficient bookbinding. The formulations are tailored to enhance process efficiency and ensure excellent adhesion across coated, uncoated, and recycled paper substrates — a growing demand in the eco-conscious European printing sector.

Jowat SE, another German adhesive leader, is setting new benchmarks in performance and sustainability. The company introduced unfilled Polyurethane (PUR) hot melt adhesives for premium-quality bookbinding, delivering high initial strength, superior flexibility, and seamless spine finishes—key for hardcover and perfect binding applications. In parallel, Jowat is spearheading bio-based innovation through its Jowacoll® GROW line, offering dispersion adhesives with 30% bio-based content, aligning with EU Green Deal targets.

Responding to occupational safety regulations, German manufacturers are also prioritizing monomer-reduced PUR hot melt adhesives such as Jowatherm-Reaktant® MR, minimizing isocyanate exposure and enhancing operator health and compliance with REACH standards. The advancements underscore Germany’s position as a global hub for sustainable, high-efficiency bookbinding adhesive technologies.

The United States bookbinding adhesives industry is experiencing substantial momentum as commercial printing and packaging sectors accelerate sustainability adoption. Franklin International, Inc., one of North America’s leading adhesive producers, has announced major capacity expansions to meet rising demand for specialized bookbinding and graphic arts adhesives, particularly in perfect binding and case binding applications for textbooks, manuals, and corporate publishing.

Simultaneously, 3M Company continues to push material innovation boundaries with the launch of a new reactive hot melt adhesive in 2025, initially developed for electronics but adaptable for durable hardcover book assembly due to its enhanced thermal stability and moisture resistance. The cross-sectoral material transfer illustrates how high-performance adhesive technologies are being repurposed to modernize print finishing and bookbinding operations.

Additionally, Diversified Chemical Technologies, Inc. is seeing strong market uptake for its low-VOC synthetic bookbinding adhesives, driven by increasingly stringent EPA and state-level emission standards. The innovations not only support cleaner production environments but also align with major U.S. publishers’ goals to meet sustainable printing certifications.

China’s position as the largest publishing and printing base globally makes it a critical growth driver in the bookbinding adhesives market. Domestic manufacturers like Hubei Huitian Adhesive Enterprise Co. Ltd. are scaling their hot melt and PUR adhesive portfolios to cater to the enormous education, magazine, and catalog printing sectors. The products are specifically engineered for high-speed, automated binding lines, ensuring strong adhesion, flexibility, and reduced curing time across diverse paper grades.

Global players including Henkel and H.B. Fuller are strategically localizing adhesive production in Shanghai and Suzhou, investing in Asia-Pacific technical centers to meet demand for advanced polymer formulations tailored to China’s expanding print-on-demand market. Concurrently, EVA-based adhesives remain in heavy use across lower-cost, high-volume applications, favored for their excellent machinability and cost efficiency.

Policy-driven sustainability targets are further accelerating the transition to low-VOC and solvent-free adhesive chemistries, making China a rapidly advancing hub for eco-efficient bookbinding adhesive manufacturing.

France’s bookbinding adhesives industry is aligning with the European Union’s circular economy initiatives, emphasizing sustainable, recyclable, and non-toxic adhesive formulations. Bostik SA, a subsidiary of Arkema Group, is leading The transformation by developing new lines of environmentally friendly, water-based adhesives specifically for high-speed perfect binding and case binding applications. The adhesives deliver excellent adhesion while enabling recyclability and easy re-pulping — essential under EU packaging sustainability frameworks.

The EU Packaging and Packaging Waste Regulation (PPWR), which mandates the gradual elimination of PFAS and hazardous chemicals, is reshaping adhesive chemistry standards across France’s printing and binding industries. Consequently, Bostik’s R&D teams are innovating solvent-free, low-odor systems optimized for large-scale bookbinding production lines. France’s leadership in green formulation development is reinforcing its reputation as a key contributor to Europe’s sustainable printing material ecosystem.

Switzerland’s Sika AG is leveraging its expertise in construction and industrial adhesives to innovate cross-application solutions for technical and specialty bookbinding. The company’s SikaMelt hot melt adhesives, initially designed for demanding construction and automotive applications, are being adapted for high-durability bookbinding—particularly for heavy-use environments like libraries, archives, and educational publishing.

By integrating heat-resistant polymer backbones and moisture-resistant formulations, Sika’s adhesive technologies ensure long-term structural integrity and superior binding strength in complex binding processes. The Swiss adhesives sector’s emphasis on cross-industry technology transfer and performance optimization places it among the most advanced hubs for industrial-grade binding innovation globally.

India’s bookbinding adhesives market is rapidly expanding, driven by massive textbook production and a surge in digital printing adoption. Pidilite Industries Limited, a dominant player in India’s adhesives sector, is broadening its PVA and VAE dispersion adhesives portfolio to cater to the growing educational publishing segment, which demands cost-effective, fast-drying, and strong adhesion systems. The company’s expansion strategy includes increased manufacturing capacity and localized raw material sourcing to support India’s high-volume print cycles.

The rise of digital and print-on-demand printing centers across metro cities has also driven demand for low-temperature PUR and EVA hot melt adhesives, enabling efficient binding across various coated paper types. Additionally, India’s focus on sustainability through green manufacturing and eco-label certifications is boosting market preference for low-VOC, solvent-free formulations suitable for export-oriented printing operations.

Bookbinding Adhesives Market Report Scope

Bookbinding Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.4 Billion

|

|

Market Size (2034)

|

$4.7 Billion

|

|

Market Growth Rate

|

3.6%

|

|

Segments

|

By Technology (Hot Melt Adhesives, Emulsion-Based Adhesives, Solvent-Based Adhesives, Pressure-Sensitive Adhesives), By Chemistry Type (Polyurethane, Ethylene Vinyl Acetate, Polyvinyl Acetate, Vinyl Acetate Ethylene, Styrenic Block Copolymers, Polyolefins, Bio-based Adhesives), By Application (Softcover Books, Hardcover Books, Magazines and Catalogs, Print on Demand, Specialty Applications), By End-User (Commercial Printing & Publishing, Educational Institutions, Corporate/Retail, Government/Archival), By Product Type (Spine Glue, Side Glue, Casing-in Adhesives

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, H.B. Fuller Company, Arkema S.A., Jowat SE, Sika AG, 3M Company, The Dow Chemical Company, KLEIBERIT SE & Co. KG, Pidilite Industries Limited, Franklin International, Inc., Ashland Inc., Eastman Chemical Company, Texyear Industrial Adhesives Private Limited, NANPAO RESINS CHEMICAL GROUP, Hubei Huitian Adhesive Enterprise Co. Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Technology

- Hot Melt Adhesives

- Emulsion-Based Adhesives

- Solvent-Based Adhesives

- Pressure-Sensitive Adhesives

By Chemistry/Resin Type

- Polyurethane

- Ethylene Vinyl Acetate

- Polyvinyl Acetate

- Vinyl Acetate Ethylene

- Styrenic Block Copolymers

- Polyolefins

- Bio-based Adhesives

By Application

- Softcover Books

- Hardcover Books

- Magazines and Catalogs

- Print on Demand

- Specialty Applications

By End-Use Sector

- Commercial Printing & Publishing

- Educational Institutions

- Corporate/Retail

- Government/Archival

By Product Type

- Spine Glue

- Side Glue

- Casing-in Adhesives

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- Henkel AG & Co. KGaA

- H.B. Fuller Company

- Arkema S.A.

- Jowat SE

- Sika AG

- 3M Company

- The Dow Chemical Company

- KLEIBERIT SE & Co. KG

- Pidilite Industries Limited

- Franklin International, Inc.

- Ashland Inc.

- Eastman Chemical Company

- Texyear Industrial Adhesives Private Limited

- NANPAO RESINS CHEMICAL GROUP

- Hubei Huitian Adhesive Enterprise Co. Ltd.

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates how PUR hot melt, water-based dispersions, and next-gen polyolefin systems are redefining softcover, hardcover, magazine/catalog, and print-on-demand workflows; our analysis reviews durability (page-pull, flex, thermal cycling), digital-print compatibility, recyclability/repulpability, and line-speed economics. It highlights eco-certified, low-VOC chemistries, debond-on-demand concepts, and AI-enabled application that cut waste and downtime, while benchmarking premium lay-flat and archival requirements. Capturing supplier moves, qualification hurdles, and buyer criteria across commercial printing and education, we surface material breakthroughs that raise spine strength, expand substrate latitude, and accelerate curing without sacrificing IAQ or fiber recovery—making this report an essential resource for publishers, converters, procurement, and plant engineering leaders planning 2025–2034 investments.

Scope Includes

- By Technology: Hot Melt Adhesives; Emulsion-Based Adhesives; Solvent-Based Adhesives; Pressure-Sensitive Adhesives

- By Chemistry/Resin: Polyurethane; Ethylene Vinyl Acetate; Polyvinyl Acetate; Vinyl Acetate Ethylene; Styrenic Block Copolymers; Polyolefins; Bio-based Adhesives

- By Application: Softcover Books; Hardcover Books; Magazines & Catalogs; Print on Demand; Specialty Applications

- By End-Use: Commercial Printing & Publishing; Educational Institutions; Corporate/Retail; Government/Archival

- By Product Type: Spine Glue; Side Glue; Casing-in Adhesives

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Timeframe: Historic 2021–2024; Forecast 2025–2034.

- Companies: Deep-dive analysis/profiles of 15+ companies.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.