Market Overview: Cold Chain and Sustainability as Core Growth Drivers

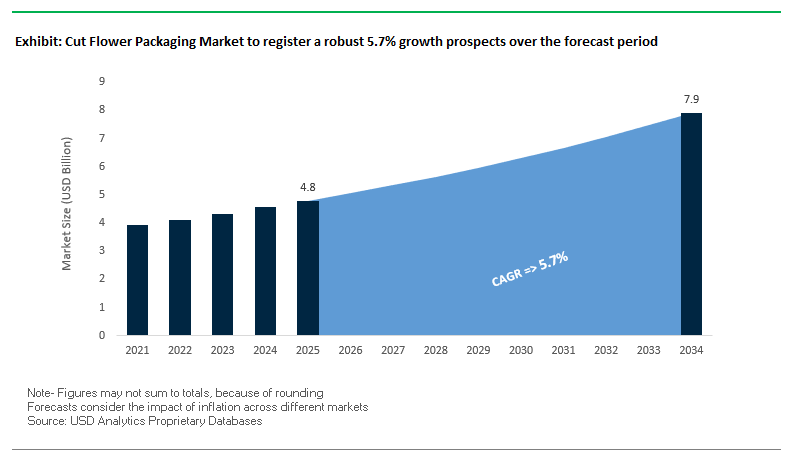

The Global Cut Flower Packaging Market is projected to expand from USD 4.8 billion in 2025 to USD 7.9 billion by 2034, growing at a CAGR of 5.7%. As a highly specialized segment of the broader packaging industry, it addresses the unique challenges of protecting one of the most perishable consumer products—fresh-cut flowers. The sector is at the intersection of aesthetics, cold chain logistics, and sustainability, making packaging a critical determinant of quality and consumer satisfaction.

The cold chain remains a primary priority, with cut flowers requiring a strict temperature range of 33°F to 35°F to maintain freshness and extend vase life. This has fueled demand for packaging formats that offer both insulation and atmosphere control, including Modified Atmosphere Packaging (MAP) and anti-ethylene solutions. At the same time, the rise of e-commerce floral delivery services is driving demand for durable, lightweight, and visually appealing packaging that ensures safe transit while delivering a premium unboxing experience.

Sustainability has become a central theme, with brands increasingly adopting biodegradable plastics, recycled paper, and natural alternatives like burlap to appeal to eco-conscious consumers. Fiber-based and paperboard packaging are gaining momentum as substitutes for plastics, particularly in premium bouquets and online gifting segments. Meanwhile, digital printing technologies and the use of QR codes or NFC tags are elevating brand engagement, transforming floral packaging from a protective medium into a communication and marketing channel.

Key Insights for professionals and Buyers:

- Cold chain packaging ensures flowers remain at 33°F–35°F, preventing wilting.

- E-commerce floral sales are pushing demand for durable and premium unboxing formats.

- Sustainable packaging materials such as recycled paper, bioplastics, and burlap are gaining traction.

- MAP technology and anti-ethylene agents are vital for extending shelf life during transit.

- Smart packaging integration is emerging, offering traceability and interactive consumer experiences.

Market Analysis: Recent Developments in the Cut Flower Packaging Industry

The global cut flower packaging industry has seen a wave of innovation, sustainability initiatives, and strategic consolidation in 2025. In August 2025, Smurfit Kappa unveiled a dedicated portfolio of e-commerce flower boxes, including designs like bouquet and letterbox formats, engineered to improve cold chain logistics and enhance the consumer unboxing experience. That same month, Mondi highlighted its paper-based e-commerce packaging portfolio at a UK trade show, positioning itself as a leader in plastic-free floral packaging solutions.

Technology integration is reshaping the industry. In July 2025, a U.S.-based consumer goods company introduced smart packaging with QR codes and NFC tags, a model now being tested in premium flower bouquets to improve traceability and consumer interaction. In June 2025, industry reports highlighted an increase in M&A activity in the paper and corrugated packaging segments, signaling that floral packaging is attracting investment due to its e-commerce alignment.

Strategic consolidations also shaped the sector. In April 2025, the Amcor–Berry Global merger created a mega entity in consumer packaging, potentially reshaping supply chains for floral packaging materials. Around the same time, a DS Smith survey revealed that U.S. consumers were willing to pay premiums for sustainable and intelligent packaging, a critical insight for the luxury and gifting segment of the floral industry.

Earlier, in March 2025, digital printing emerged as a critical innovation, offering flexible, small-batch customization for floral branding. In February 2025, the International Paper–DS Smith merger was finalized, creating a global fiber-based packaging leader with expanded capacity to serve the North American and European flower trade markets. Collectively, these moves underscore how sustainability, digital engagement, and supply chain efficiency are redefining competitive dynamics in cut flower packaging.

Emerging Trends Reshaping the Cut Flower Packaging Market

Strategic Shift Towards Brand-Differentiating, Shelf-Ready Packaging

One of the most transformative trends in the cut flower packaging market is the move away from plain, utilitarian packaging toward brand-differentiating, retail-optimized formats. With the rise of mass-market retail channels, growers and distributors are prioritizing packaging that communicates sustainability credentials, enhances shelf visibility, and reduces in-store labor. Shelf Ready Packaging (SRP) solutions can cut restocking time by up to 40%, creating major cost savings for retailers and a stronger incentive for adoption. Packaging suppliers are leveraging advanced printing, bold logo placement, and consistent brand messaging to help flowers stand out on crowded retail shelves. For growers, this trend translates into premium pricing and stronger brand recognition, while for packaging manufacturers, it evolves the supplier role from a commodity provider to a strategic partner in brand differentiation. Ultimately, this trend is redefining the value chain by shifting cut flowers from a bulk, utilitarian product to a branded, consumer-centric experience.

Rapid Adoption of Hydration-Forward, Life-Extending Technologies

Another critical trend driving innovation in the cut flower packaging industry is the widespread adoption of hydration-forward technologies that actively extend vase life. Freshness preservation is the single biggest challenge in floral logistics, and new packaging formats now go far beyond basic water tubes to incorporate absorbent substrates and antimicrobial wraps. Scientific studies highlight that paper-based antimicrobial packaging has significantly extended rose shelf life, proving that R&D is directly addressing perishability challenges. Industry innovators are introducing solutions like proprietary “Bouquet Wraps,” which lock in hydration during transit and keep flowers fresher for longer. For growers and distributors, this technology reduces shrink and spoilage, while for retailers, it increases consumer satisfaction and loyalty by ensuring flowers last longer at home. With vase-life extension tied directly to repeat purchases and reduced returns, this trend is creating measurable value across the floral supply chain, making it one of the most commercially impactful innovations in cut flower packaging.

Development of Integrated Smart & Connected Packaging for Traceability

The digitalization of packaging presents a major growth opportunity for the cut flower packaging market. Embedding RFID tags or QR codes directly into sleeves and boxes enables farm-to-vase traceability, giving retailers real-time visibility into inventory and consumers proof of product origin. Case studies from Europe demonstrate how RFID systems can track flowers across logistics stages, monitoring temperature and humidity to preserve freshness and reduce waste. For suppliers, this opens a new high-margin segment that goes beyond protection to deliver data-driven value-added services. Smart packaging also combats counterfeiting, curbs gray-market diversion, and builds consumer trust through transparency—making it an invaluable differentiator for premium floral brands. To realize this opportunity, packaging converters and technology providers must form strategic collaborations that integrate digital identifiers seamlessly into protective packaging, thereby creating a more resilient, connected floral supply chain.

Commercialization of Home-Compostable and Plant-Based Protective Wraps

With mounting regulations on single-use plastics and rising consumer demand for eco-friendly products, the cut flower packaging market has a major opportunity to scale home-compostable and plant-based bouquet wraps. Traditional plastic film, still widely used in the industry, is increasingly viewed as unsustainable. By commercializing compostable cellulose-based or plant-derived protective wraps, manufacturers can offer solutions that align with circular economy goals and resonate with environmentally conscious buyers. Leading companies are already launching compostable films certified for industrial composting, but the frontier lies in creating true home-compostable wraps that decompose naturally in household settings. This would not only reduce landfill waste and microplastic pollution but also position brands as leaders in sustainable packaging. For packaging suppliers, the commercialization of compostable wraps represents a premium growth avenue, allowing them to capture share in the rapidly expanding sustainable consumer goods market.

Competitive Landscape: Leading Companies in Cut Flower Packaging

The global cut flower packaging market is shaped by a combination of fiber-based packaging leaders, e-commerce-focused innovators, and global packaging giants.

Smurfit Kappa drives e-commerce-ready floral packaging innovation

Smurfit Kappa, now part of the Smurfit WestRock entity, is a leader in paper-based solutions tailored for cold chain and e-commerce logistics. In August 2025, it launched its Bouquet Box and Letterboxable formats, designed to reduce transit damage while elevating customer experience. With proven case studies showing 300% sales growth for floral clients, Smurfit Kappa combines durability, branding, and sustainability. Its strategy is focused on premium unboxing and reduced material usage, aligning with global e-commerce trends.

Mondi advances plastic-free paper packaging for flowers

Mondi plc is recognized for its sustainable paper-based solutions that replace plastics in the floral supply chain. Its portfolio includes corrugated boxes, paper bags, and mailers optimized for online flower delivery. In 2025, its acquisition of Schumacher Packaging’s Western European assets expanded its corrugated production capacity. With a corporate target of making all packaging reusable, recyclable, or compostable by 2025, Mondi positions itself as a pioneer of sustainable floral packaging design aligned with the circular economy.

International Paper expands containerboard focus for flower logistics

International Paper, following its 2025 restructuring and DS Smith acquisition, reinforced its dominance in fiber-based packaging. In August 2025, it announced a USD 250 million investment to convert a paper machine to containerboard production, directly supporting corrugated floral packaging growth. With its vast manufacturing and distribution network, the company provides reliable, sustainable corrugated solutions critical for cold chain floral transport. Its focus remains on streamlining operations and improving sustainability across packaging formats.

WestRock develops insulated solutions for cut flowers

WestRock, now part of Smurfit WestRock, has been a key innovator in temperature-controlled packaging. Its InsulShield™ system for plant and flower shipments highlights its expertise in balancing thermal regulation and durability. With a diversified portfolio spanning retail-ready and e-commerce packaging, WestRock emphasizes design-driven solutions that reduce waste and improve cold chain performance. Its strategy is rooted in circular packaging innovation powered by advanced material science.

Cut Flower Packaging Market Share Insights

Boxes & Cartons Dominate Market Share by Product Type in Cut Flower Packaging

Boxes and cartons hold the largest share at 35% of the cut flower packaging market, a position strengthened by the rapid expansion of e-commerce and direct-to-consumer flower delivery platforms. These packaging solutions provide robust protection for delicate stems during air freight and last-mile delivery, ensuring product integrity and reducing waste from damaged goods. Beyond protection, they enable branding opportunities through printed designs that enhance the consumer unboxing experience, a critical differentiator in online floral retail. Their leadership is further reinforced by the shift toward recyclable fiber-based materials, aligning with sustainability expectations from both consumers and corporate buyers in the floral supply chain.

Bunch & Bouquet Packaging Dominates Market Share by Flower Type in Cut Flowers

Bunch and bouquet formats represent an overwhelming 85% share of the cut flower packaging market, highlighting the consolidation of consumer preferences around pre-arranged, ready-to-gift floral units. The dominance of bouquets is tied directly to e-commerce growth, supermarket sales, and gifting occasions, where convenience and presentation drive value. This segment requires integrated packaging solutions such as sleeves, cartons, and wrapping sheets designed to support multiple stems while maintaining hydration and visual appeal. By contrast, single-stem packaging remains a high-value niche for exotic or luxury flowers but cannot match the scale of bouquet sales. The 85/15 split illustrates how modern retail dynamics have transformed packaging into a critical enabler of bouquet-based sales, solidifying its dominant market position.

United States Cut Flower Packaging Market Expands Through Sustainable Materials and Smart Packaging Innovations

The United States cut flower packaging market is shaped by a complex patchwork of state-level regulations and federal grants, with sustainability emerging as a key driver. Consumer demand for eco-friendly and reduced packaging is prompting companies to adopt biodegradable wraps, recyclable paperboard sleeves, and domestically-produced bio-based polymers. Initiatives like the Specialty Crop Block Grant Program and the federal Agriculture and Food Research Initiative are providing targeted funding to enhance floriculture competitiveness, indirectly supporting packaging innovations.

Technological advancements are transforming the U.S. market, particularly through smart packaging with QR codes that enable supply chain traceability, consumer engagement, and care instructions. Corporate investments are focusing on automation and sustainable material development to meet growing e-commerce and direct-to-consumer (DTC) demand. The rise of subscription-based flower delivery and online sales requires lightweight, durable, and visually appealing packaging that protects delicate products during transit while aligning with eco-conscious consumer preferences.

Germany Cut Flower Packaging Market Strengthens Through PPWR Regulations and Circular Economy Leadership

Germany’s cut flower packaging market is governed by stringent regulations, including the EU Packaging and Packaging Waste Regulation (PPWR) effective February 2025, mandating fully recyclable or reusable packaging by 2030 and phasing out harmful chemicals like PFAS. The country’s robust Extended Producer Responsibility (EPR) system incentivizes packaging innovation through recycling and sorting initiatives. New recyclability standards, effective January 2026, are encouraging the development of reusable transport packaging that aligns with circular economy goals.

Technological innovation is central to the German market, with companies investing in machinery capable of handling sustainable materials, digital product passports, and watermarks to enhance transparency. Key applications include retail and florist sectors, where reusable and efficient packaging is in high demand. Collaborative efforts between film producers and brand owners are driving high-performance, customized flexible packaging solutions. EU regulations setting minimum recycled content and packaging optimization requirements are pushing the market toward smarter, more sustainable designs.

China Cut Flower Packaging Market Gains Momentum With Green Transformation and E-Commerce Growth

China’s cut flower packaging market is being transformed by the government’s “dual carbon” goal and related green industrial initiatives. The 2024 Action Plan for Promoting Large-Scale Equipment Updates and Consumer Goods Replacement encourages recycling and sustainable materials, while State Post Bureau regulations prioritize eco-friendly, reusable packaging for express delivery. These initiatives are driving demand for lightweight and sustainable floral packaging solutions.

Regulatory reforms limiting excessive packaging layers and void ratios, effective September 2023, directly impact e-commerce flower shipments. Technological advancements, including AI, automation, and integration of 5G plus industrial internet, are enhancing production efficiency and flexible manufacturing capacity. Domestic production is expanding to reduce reliance on imports, meeting growing consumer demand for circular and high-quality packaging. E-commerce platforms and floriculture delivery services are key growth drivers, with sustainability and functionality at the forefront of innovation.

Brazil Cut Flower Packaging Market Accelerates With Sustainable Policies and Advanced Manufacturing

Brazil’s cut flower packaging industry is benefiting from the National Solid Waste Policy and recent regulations banning single-use disposable items, with a 2030 mandate for returnable or fully compostable packaging. The adoption of biodegradable films made from sugarcane-derived carboxymethyl cellulose (CMC) is enhancing packaging for perishable products like flowers. Robotics and AI integration are improving manufacturing efficiency and quality control.

Corporate investments are supporting new production facilities, including Wheaton’s interactive design center in São Paulo, focused on glass and sustainable packaging solutions. The fresh food and floriculture sectors are major applications driving demand, while sustainability is a central focus across the Brazilian market. Companies are leveraging eco-friendly materials and green manufacturing techniques to meet both regulatory requirements and growing consumer expectations for environmentally responsible packaging.

Japan Cut Flower Packaging Market Advances Through Bio-Based Materials and High-Performance Films

Japan’s cut flower packaging market is defined by advanced manufacturing and sustainability initiatives, including the Plastic Resource Circulation Act effective April 2022. The act encourages “Design for the Environment” and aims to reduce single-use plastics, targeting 2 million tonnes per year of bio-polypropylene (bio-PP) by 2030.

Innovation in high-performance films is driving the market, with enhanced barrier properties and IoT-enabled real-time tracking to protect fragile flowers during transport. Functional advancements focus on dimensional stability and resistance to deformation. Cross-industry collaborations, such as LyondellBasell incorporating bio-based PP into Shiseido’s packaging, demonstrate opportunities for floral packaging to adopt sustainable and high-quality materials. Japan’s emphasis on precision manufacturing and technology integration positions the country as a leader in next-generation, eco-friendly cut flower packaging solutions.

Cut Flower Packaging Market Report Scope

Cut Flower Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.8 Billion

|

|

Market Size (2034)

|

$7.9 Billion

|

|

Market Growth Rate

|

5.7%

|

|

Segments

|

By Packaging Material (Paper & Paperboard, Plastic, Metal, Jute), By Product Type (Sleeves, Wrapping Sheets, Boxes & Cartons, Poles, Bags, Metal Stands), By Sales Channel (Florists, Supermarkets & Retail Stores, Online Sales), By Flower Type (Bunch/Bouquet, Single Cut)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Mondi Group, Huhtamaki Oyj, Smurfit Kappa Group plc, Sonoco Products Company, DS Smith plc, WestRock Company, Sealed Air Corporation, Berry Global Group, Inc., International Paper Company, Pactiv Evergreen Inc., Uflex Ltd., Rengo Co., Ltd., Billerud AB, Graphic Packaging Holding Company

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Cut Flower Packaging Market Segmentation

By Packaging Material

- Paper & Paperboard

- Plastic

- Metal

- Jute

By Product Type

- Sleeves

- Wrapping Sheets

- Boxes & Cartons

- Poles

- Bags

- Metal Stands

By Sales Channel

- Florists

- Supermarkets & Retail Stores

- Online Sales

By Flower Type

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Cut Flower Packaging Market

- Amcor plc

- Mondi Group

- Huhtamaki Oyj

- Smurfit Kappa Group plc

- Sonoco Products Company

- DS Smith plc

- WestRock Company

- Sealed Air Corporation

- Berry Global Group, Inc.

- International Paper Company

- Pactiv Evergreen Inc.

- Uflex Ltd.

- Rengo Co., Ltd.

- Billerud AB

- Graphic Packaging Holding Company

* List Not Exhaustive

Methodology

USDAnalytics employed a comprehensive methodology to analyze the Global Cut Flower Packaging Market, combining both primary and secondary research to deliver actionable insights for industry professionals. Primary research involved interviews and surveys with key stakeholders, including packaging manufacturers, floriculture distributors, e-commerce floral service providers, and sustainability experts, to understand market trends, technological adoption, and supply chain dynamics. Secondary research encompassed analysis of company reports, press releases, regulatory filings, trade journals, patent data, and industry publications to validate market size, growth projections, and competitive developments. Quantitative methods were applied to forecast market valuation, CAGR, and segmentation by material, product type, sales channel, and flower type, while qualitative assessment focused on cold chain innovations, sustainable materials adoption, smart packaging integration, hydration-forward technologies, and Shelf-Ready Packaging (SRP) trends. USDAnalytics also considered regional regulatory frameworks, such as the EU PPWR, U.S. sustainability grants, and Japan’s Plastic Resource Circulation Act, along with recent mergers, acquisitions, and technological advancements, producing a professional-grade, future-ready market outlook tailored for decision-makers across North America, Europe, Asia, and Latin America.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.