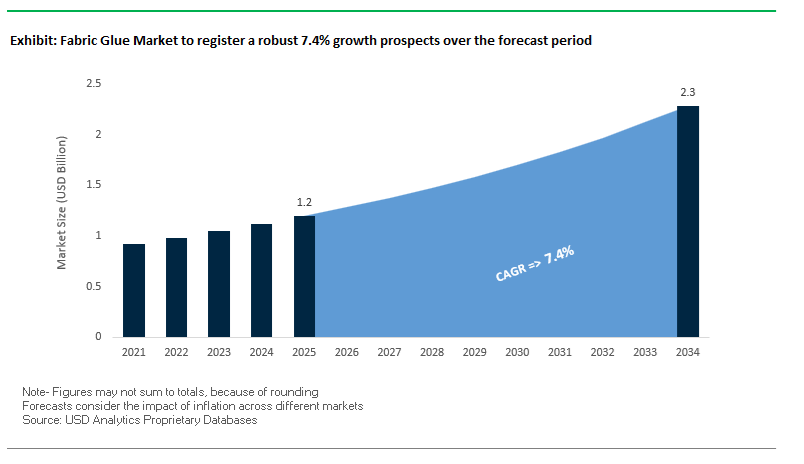

The Global Fabric Glue Market is projected to expand from USD 1.2 billion in 2025 to USD 2.3 billion by 2034, advancing at a CAGR of 7.4%, as textile manufacturing structurally shifts away from sewing-intensive assembly toward adhesive-enabled bonding. Across apparel, footwear, automotive interiors, medical textiles, and industrial fabrics, fabric glues are increasingly specified to replace stitching and mechanical fastening in order to improve design flexibility, surface aesthetics, production efficiency, and multi-layer laminate performance. Polyurethane reactive (PUR) systems, water-based fabric adhesives, hot melts, and emerging bio-based chemistries are integral to modern textile lines where stretchability, drape retention, and bond invisibility are as critical as mechanical durability.

From an OEM and converter perspective, adoption is being driven by performance reliability under real-use and post-processing conditions, rather than convenience alone. Technical textile adhesives—including cassava starch–based hot melts achieving approximately 4.93 ± 0.11 MPa dry shear strength—are enabling non-sewn structural joints in high-stress applications such as outdoor apparel, protective gear, and reinforced fabrics. In parallel, urethane-based fabric glues capable of retaining adhesion after repeated 90°C sterilization cycles have become essential in medical textiles and high-durability garments, where washability, hygiene compliance, and long service life are mandatory. Fast-curing hot melt fabric adhesives, delivering initial set times of around three minutes and full cure within 72 hours, are further supporting high-throughput garment and footwear assembly by reducing bottlenecks on global production lines.

Sustainability and regulatory compliance are reinforcing these structural shifts. Leading manufacturers, including Henkel, H.B. Fuller, Bostik, and Sika, are reformulating fabric adhesive portfolios to incorporate bio-based content, low-VOC profiles, and improved occupational safety without compromising bond performance. Examples include eco-conscious adhesive systems using up to 90% renewable raw materials validated under ASTM D6866-22, aligning textile bonding with ESG and circular manufacturing objectives. At the same time, polyurethane technologies with below 0.1% monomeric diisocyanate content, such as Purform®-based systems, are reducing REACH-related safety burdens and operator exposure in industrial environments.

The fabric glue market is experiencing a surge in sustainability-driven R&D, regional production expansion, and safer polyurethane formulation rollouts, underscoring the growing intersection of chemical innovation and textile functionality.

In July 2025, Henkel Adhesive Technologies India inaugurated a major automotive warehouse in Chakan, Pune, reinforcing its local logistics and distribution network for automotive and technical textile adhesives. This strategic move supports India’s fast-growing transportation and industrial textile sectors, signaling Henkel’s regional supply chain strengthening amid rising demand for high-performance flexible bonding materials.

In February 2025, H.B. Fuller Company showcased its new Swift®lock 6511 lamination adhesive, a low-monomer, non-hazardous formulation under EU Regulation 1272/2008, compliant with OEKO-TEX® ECO PASSPORT. The product addresses the global shift toward non-toxic, sustainable textile bonding and is especially suitable for laminated fabrics in activewear and home textiles. Around the same period, Sika AG expanded its Purform® polyurethane adhesive line, reducing occupational exposure risks and simplifying REACH regulatory compliance, a major advancement in safe industrial adhesive deployment.

In August 2025, Henkel AG & Co. KGaA announced an operating profit (EBIT) rise to EUR 1.6 billion, supporting R&D in textile and nonwoven adhesives, particularly for sportswear and medical applications. Earlier, in April 2025, Bostik (Arkema Group) published a new “No-Sew Apparel Solutions” brochure, focusing on adhesives that enable stitchless garment assembly—a key innovation for activewear and lingerie manufacturers targeting comfort and precision in high-speed production.

The academic sector also contributed to bio-adhesive innovation. In September 2024, research on cassava starch-based hot melts demonstrated a tensile strength of 3.45±0.22 MPa, proving the potential of low-cost, biodegradable glues for industrial fabric bonding. By October 2024, multiple adhesives firms pledged to incorporate recycled polymer content into packaging and formulation processes, aligning with circular economy goals.

In June 2025, Henkel India further enhanced its ESG commitments by partnering with the Navi Mumbai Municipal Corporation for a large-scale clean-up initiative. Though not product-related, such environmental actions reinforce Henkel’s sustainability branding—a key factor in procurement decisions for textile OEMs seeking eco-certified suppliers.

The transition toward seamless, lightweight, and high-performance activewear is driving the innovation of wash-durable polyurethane reactive (PUR) adhesives and thermoplastic bonding films. These systems are designed to withstand extreme conditions—repeated washing, sweat exposure, and mechanical stretch—without delamination or stiffness, ensuring performance integrity in garments like compression wear, outdoor jackets, and athletic leggings.

Unlike conventional hot melts, PUR fabric glues chemically cross-link upon exposure to moisture, forming a permanent, flexible polymer network. Advanced PUR systems exhibit superior elasticity retention—maintaining adhesive strength even after 30+ industrial washing cycles—a benchmark requirement for technical sportswear and professional uniforms. Their resistance to thermal cycling and flex fatigue provides unmatched stability in dynamic garment areas such as seams, hems, and joints.

Thermoplastic polyurethane (TPU)-based films, typically 30–100 µm thick, are revolutionizing bonding in seamless garments. These materials enable invisible joins with smooth internal finishes, eliminating chafing and bulk associated with stitching. The is particularly advantageous for next-generation compression garments and stretchable activewear, where comfort, flexibility, and aesthetics are primary consumer drivers.

The rise of automated adhesive bonding machinery across Asia-Pacific manufacturing hubs is streamlining apparel assembly. Compared to manual sewing, automated bonding ensures higher precision, repeatability, and speed, reducing dependency on skilled labor and minimizing quality inconsistencies from tension-based stitching. The shift is expected to increase fabric adhesive adoption by over 20% in performance textile manufacturing by 2028 as brands prioritize consistency and scalability.

The sustainability imperative is reshaping adhesive formulation chemistry across textile manufacturing. With rising concern over PFAS, APEO surfactants, and VOC emissions, adhesive producers are pivoting toward water-based, non-toxic, and biodegradable solutions that maintain comparable mechanical strength to traditional solvent-based adhesives.

International frameworks such as REACH, OEKO-TEX® STANDARD 100, and California’s Proposition 65 are pushing the fabric adhesive industry toward zero-VOC chemistries. Water-based polyurethane and acrylic emulsions are becoming preferred for fabric lamination and garment assembly, providing robust adhesion with minimal odor, faster drying, and improved worker safety. The trend aligns with the apparel industry’s shift toward green manufacturing and closed-loop production.

Innovations in starch-modified adhesive systems, derived from corn and pea starch, are redefining water-based bonding performance. These adhesives exhibit enhanced water resistance and heat durability, suitable for coating and lamination in both woven and nonwoven fabrics. Such formulations effectively replace petroleum-based polymers while eliminating hazardous emissions caused by pyrolysis of traditional oily glues.

Major apparel brands are publicly committing to chemical transparency and non-toxic materials by 2030. The has accelerated R&D in renewable fabric glue chemistries, promoting long-term competitiveness for manufacturers compliant with LEED-certified production and circular textile design standards.

The rise of DIY culture, visible mending, and sustainable fashion movements presents a rapidly growing consumer-facing opportunity for ready-to-use, fast-curing fabric adhesives. With the global shift toward slow fashion and garment longevity, consumers increasingly prefer self-repair solutions over replacement, supporting the broader circular economy transition.

Studies show that extending the life of a garment by just nine months can reduce its environmental footprint—carbon, water, and waste—by 20–30% annually. The has directly stimulated retail demand for permanent fabric glues that can repair tears, hems, and embellishments while maintaining flexibility and wash-resistance comparable to sewn joints.

Online sales analytics report that consumer-grade textile adhesives—marketed for quick repairs and craft applications—achieve monthly sales exceeding 2,500 units per SKU on platforms such as Amazon and Etsy. These products, often branded as “no-sew fabric glues” or “fabric fusion adhesives,” are highly rated for durability, ease of application, and compatibility with both synthetic and natural fibers.

As fashion brands adopt take-back and repair programs, private-label opportunities for adhesive manufacturers are expanding. Co-branding between textile care companies and adhesive producers offers a path for eco-certified repair kits and sustainable fashion accessories, driving additional retail visibility and consumer trust.

The convergence of electronics and textiles in smart clothing and medical wearables is creating a high-value frontier for fabric glues with electrical insulation, flexibility, and biocompatibility. Adhesives in the segment act not only as bonding agents but also as protective barriers and structural reinforcements for delicate electronic circuits embedded within fabrics.

The success of wearable sensors, conductive yarns, and textile antennas depends on adhesives that offer mechanical flexibility, thermal stability, and insulation without disrupting electrical pathways. Innovations like anisotropic conductive adhesives (ACAs) allow precise directional conductivity, enabling accurate signal transfer in wearable diagnostics, such as ECG monitoring garments and health-tracking smart bands.

For long-term usability, wearable electronics require glues that maintain adhesion and flexibility through 30+ wash cycles, resist sweat corrosion, and perform under body temperature variations. Manufacturers are introducing thermosetting epoxy-silicone hybrids and stretchable polyurethane systems with Shore A hardness between 30–60, achieving consistent signal transmission and sensor retention over extended product lifespans.

The increasing adoption of textile electrodes and bio-integrated garments in sports and healthcare sectors drives the need for adhesives that combine biocompatibility and mechanical resilience. Fabric glues tailored for e-textiles play a vital role in connecting sensors, microchips, and wiring without compromising wearer comfort or garment aesthetics.

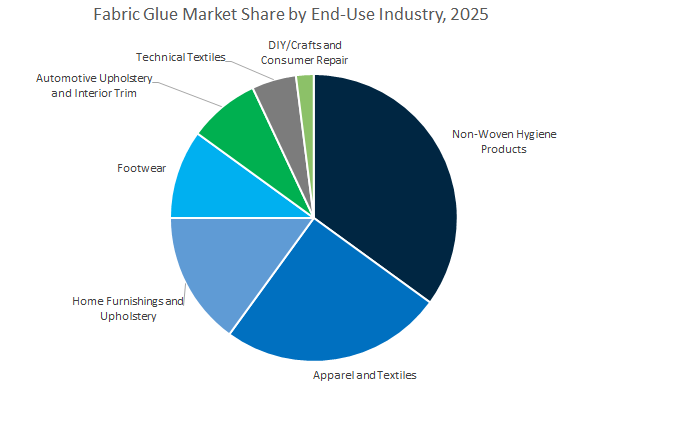

Fabric Glue Market Share Insights, 2025-2034

Water-based or emulsion adhesives dominate the global fabric glue industry, accounting for approximately 47.1% of the total market share in 2025. Their leadership is attributed to a powerful combination of eco-friendly chemistry, user safety, and cost efficiency, making them indispensable in both industrial textile production and consumer markets. These adhesives use polymer dispersions such as PVA, acrylic, or EVA in water, providing strong adhesion to a wide range of fabrics without toxic emissions or flammability concerns. This positions them as the preferred choice for non-woven hygiene products, apparel assembly, and home furnishings, where low VOC content, wash resistance, and flexibility are essential. The rising demand for sustainable manufacturing and compliance with REACH and EPA regulations further accelerates their adoption. Additionally, water-based formulations enable easy cleanup, fast drying, and compatibility with automated textile production lines, making them ideal for mass production of hygiene disposables, medical textiles, and garment assembly. With growing consumer preference for non-toxic and odor-free glues, this segment is expected to maintain its dominance across all major fabric bonding applications.

Hot Melt Adhesives (HMAs) are rapidly expanding their footprint in the fabric glue market, supported by their advantages in production speed, precision, and bond strength. These thermoplastic formulations—often based on EVA, polyolefin, or TPU—are widely used in automotive upholstery, footwear, and non-woven hygiene product manufacturing, where instant tack and fast solidification reduce cycle times. Their solvent-free, low-waste process aligns with sustainability goals, while their resistance to moisture and heat enhances product durability. Hot melts are particularly favored in disposable hygiene products like baby diapers and sanitary pads, where automated spray or slot application ensures consistent, reliable bonding. In addition, HMAs are finding increasing use in technical and functional textiles, including sportswear and filtration materials, due to their ability to bond complex fabric composites. As automation in textile and hygiene product manufacturing intensifies globally, hot melt adhesives will continue to gain share from traditional water-based systems, driven by efficiency and precision demands.

The non-woven hygiene products segment is the largest and most dynamic consumer of fabric adhesives, commanding 36.2% of the global market share in 2025. This dominance is driven by the expanding global demand for baby diapers, feminine hygiene products, and adult incontinence solutions, particularly in emerging economies. Fabric glues play a critical role in assembling non-woven substrates, bonding elastic materials, and securing absorbent cores while maintaining breathability, softness, and skin safety. Manufacturers are increasingly adopting low-temperature hot melt and water-based adhesive systems to ensure faster production and minimize substrate damage. In addition, heightened hygiene awareness post-pandemic and demographic factors such as aging populations are propelling long-term growth. The continuous shift toward biodegradable and compostable hygiene materials also supports innovations in bio-based and low-VOC adhesive formulations, positioning this segment as the cornerstone of both volume and technology development in the fabric glue market.

The apparel and textiles segment, together with footwear manufacturing, represents a significant portion of the global fabric adhesive market, driven by the ongoing shift from stitching to adhesive bonding. In apparel, fabric glues are used for seam sealing, hemming, and attaching decorative trims, offering flexibility, lightweight comfort, and waterproofing advantages over traditional sewing. The rise of athleisure, technical clothing, and sustainable fashion has amplified the need for durable yet flexible adhesives that maintain performance through repeated washing and wear. In footwear, adhesives are critical for upper-to-sole bonding, fabric overlays, and reinforcement layers, ensuring high durability and precision in design. The adoption of reactive and hot melt adhesives allows for improved process efficiency and reduced labor dependency. With the fast-fashion sector demanding cost-effective, high-throughput bonding methods and the luxury segment seeking superior finish quality, fabric adhesives are becoming integral to the next generation of textile and footwear production processes.

The Global Fabric Glue Market is defined by a blend of chemical innovation, sustainability compliance, and textile specialization. Market leaders such as Henkel AG & Co. KGaA, H.B. Fuller Company, Bostik (Arkema Group), and Sika AG dominate through deep expertise in polyurethane reactive adhesives, hot melts, and bio-based textile polymers. Their R&D investments target wash durability, low-temperature bonding, and sustainability certification, aligning with global nonwoven, apparel, and industrial textile trends.

Henkel remains the leading innovator in PUR and hot-melt fabric glue technologies, addressing seam-free garment assembly and technical textile lamination. The company’s Adhesive Technologies division, which generated EUR 10.97 billion in 2024, accounts for over half of total sales. Henkel’s Technomelt PUR compounds are both Bluesign® and Oeko-Tex® 100 certified, validating their eco-compliance for apparel and home textiles. Its soft-touch, elastic bonding systems are engineered for sportswear, lingerie, and waterproof outdoor gear, combining flexibility with high tensile adhesion.

H.B. Fuller leads the market in water-based polymer emulsions and hot-melt systems for nonwoven and technical fabric bonding. Its Swift®lock series, including Swift®lock 6717, offers medical-grade durability, surviving over 100 sterilization cycles without delamination. The company’s adhesives portfolio—comprising acrylic, VAE, and styrene-acrylic binders—supports low-VOC and APE-free textile coatings. With a strong focus on renewable chemistry, its Swift®lock 6490 adhesive contains up to 90% bio-based content, cementing its leadership in sustainable adhesive innovation.

Bostik, part of the Arkema Group, specializes in high-performance textile adhesives for laminated fabrics, disposable hygiene, and no-sew garments. Leveraging Arkema’s materials science expertise, Bostik is advancing bio-based copolyester and copolyamide resins for sustainable bonding. Its Heat-Activated Film Adhesives (HAF) and Instant Bonding Systems enable seam-free garment production, critical for lingerie, sportswear, and outdoor performance apparel. The company’s global footprint extends across Europe, Asia, and North America, where it supports large-scale textile assembly lines through rapid-curing, breathable adhesives.

Sika AG holds a strong global position in industrial and textile bonding, driven by its proprietary Purform® polyurethane technology. The innovation ensures <0.1% monomeric diisocyanate content, removing REACH safety training requirements for operators. Its Sikaflex® line provides superior elasticity, water resistance, and color stability, ideal for automotive upholstery, industrial textiles, and light-colored fabrics. Additionally, its Co-Elastic Technology (CET) demonstrates that water-based flexible adhesives can deliver durable, water-immersion-resistant performance, bridging the gap between performance and sustainability in fabric bonding.

Vietnam is emerging as one of the fastest-growing hubs in the global fabric glue and textile adhesives market, supported by robust apparel exports, a thriving technical textiles sector, and rising foreign investment in industrial manufacturing. The country’s competitive advantage as a global apparel production center has accelerated the demand for industrial-grade textile bonding agents and specialty fabric glues used in high-performance and durable fabric applications. In October 2025, UPM Adhesive Materials announced a new slitting and distribution terminal near Hanoi, underscoring Vietnam’s strategic role as a regional adhesives distribution base, catering to durables, electronics, and apparel sectors.

Foreign Direct Investment (FDI) in Vietnam surged by 33% in the first half of 2025, led by manufacturing—fueling domestic demand for fabric and upholstery adhesives across garment, footwear, and furniture sectors. Furthermore, the shift toward eco-friendly waterborne adhesive formulations—similar to those used in construction and upholstery—aligns with the nation’s green industrial policy goals. With its combination of manufacturing growth, foreign investment, and sustainability adoption, Vietnam is positioning itself as a key Asian supplier in the industrial and technical textile adhesives market.

Germany stands as Europe’s epicenter for advanced fabric glue technologies, driven by the European Union’s circular economy mandates and national initiatives promoting sustainable chemistry. The revised EU Waste Framework Directive, which requires separate household textile waste collection by January 2025, is transforming adhesive development toward recycling-compatible and de-bondable textile glues. The regulation directly influences both adhesive manufacturers and textile producers, leading to a surge in R&D activity focused on reversible bonding agents that simplify textile recycling processes.

Projects such as the EU-funded T-REX (Textile Recycling EXcellence) initiative—featuring major participants like BASF SE and ADIDAS AG—are pioneering recycling-friendly adhesive ecosystems that enable fabric recovery without degrading material quality. Additionally, Germany’s High-Tech Strategy 2025 and tax incentives under Forschungszulagengesetz (FzulG) are bolstering private sector R&D, especially in next-generation waterborne textile adhesives that comply with REACH standards. By combining circularity-focused regulation, material innovation, and industrial collaboration, Germany is reinforcing its leadership in the European sustainable fabric adhesive market.

China remains the world’s largest producer and consumer of textile adhesives, with new environmental regulations pushing rapid innovation in eco-friendly and low-VOC fabric glue formulations. The implementation of GB 30981.1–2025 and GB 30981.2–2025 national standards—targeting limits on hazardous substances in coatings—will take full effect by June 2026, compelling manufacturers to adopt low-formaldehyde and non-aromatic textile adhesives. The regulatory tightening aligns with China’s broader industrial environmental strategy under its “Made in China 2025” policy.

The release of GB 26572-2025 (China RoHS), which restricts four major phthalates in electronic equipment, is also affecting the production of flexible adhesives used in smart textiles, wearable electronics, and conductive fabrics. Moreover, China’s move toward harmonizing with the UN Globally Harmonized System (GHS) for chemical classification enhances export competitiveness and ensures compliance across global supply chains. As the country continues to lead in technical textile manufacturing, from apparel to industrial fabrics, its regulatory-driven transition to safer, low-emission, and high-performance textile bonding solutions is cementing China’s dominance in the global fabric glue and textile adhesives industry.

The United States fabric glue market is increasingly defined by high-performance adhesives for smart textiles, protective apparel, and nonwoven materials. With the rapid rise of wearable electronics, U.S. manufacturers are developing conductive, flexible, and washable adhesive systems that seamlessly integrate sensors and circuits into textiles without affecting comfort or durability. The technological transformation is strengthening the country’s position in smart apparel, defense textiles, and medical wearables.

Innovation in the nonwoven sector is another major catalyst. The Association of the Nonwoven Fabrics Industry (INDA) has highlighted groundbreaking progress in chemical recycling technologies for mixed polyester nonwovens, driving demand for compatible waterborne adhesives that maintain integrity during recycling. The market is also witnessing a strong shift toward solvent-free and water-based textile adhesives, aligning with the EPA’s environmental standards and consumer preference for sustainable materials. The convergence of sustainability, smart material integration, and advanced textile engineering is positioning the U.S. as a major innovation hub for high-performance and eco-conscious fabric adhesives globally.

India’s fabric glue and nonwoven adhesives market is experiencing accelerated expansion, supported by industrial investment, population-driven hygiene demand, and government-led manufacturing growth. In July 2025, Spunweb Nonwoven Limited launched a ₹60.98 crore IPO to expand production of polypropylene spunbond nonwoven fabrics—a material heavily reliant on nonwoven hygiene adhesives for baby diapers, feminine care, and medical applications. The surge in disposable income and urbanization has led to exponential growth in hygiene product consumption, making India a critical market for amorphous poly alpha olefin (APAO) and Styrenic Block Copolymer (SBC)-based adhesive formulations.

Global adhesive leaders such as Henkel AG, H.B. Fuller, and Arkema Group maintain a strong presence in India, offering customized, high-bond strength nonwoven adhesive systems suited for regional climatic and manufacturing conditions. Simultaneously, rapid growth in industrial textiles, packaging, and automotive upholstery is increasing the use of industrial-grade water-based fabric glues. As India expands its nonwoven capacity and invests in technical textile innovation, the country is becoming a major growth engine for the Asia-Pacific textile adhesives market.

The European Union (EU) continues to play a pivotal role in shaping the sustainable future of textile and fabric adhesive chemistry, thanks to progressive environmental regulations and circular economy policies. The implementation of the Waste Framework Directive (2025), coupled with the EU Strategy for Sustainable and Circular Textiles, is accelerating R&D in biodegradable, solvent-free, and recyclable textile adhesive formulations. The regulatory framework compels manufacturers across member states to innovate in de-bondable and chemically recyclable adhesives that allow fabrics and laminates to be efficiently separated for reuse.

Moreover, EU-backed innovation consortia are promoting next-generation bio-based polymer emulsions and polyurethane dispersions as sustainable alternatives to traditional solvent-based glues. The synergy between legislative enforcement, corporate sustainability commitments, and EU-funded research programs has positioned the bloc as a global leader in eco-conscious adhesive technologies. Consequently, Europe is expected to maintain its status as the most advanced region for recyclable and environmentally compliant textile adhesives, setting global benchmarks for sustainability in the fabric glue industry.

Fabric Glue Market Report Scope

Fabric Glue Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.2 Billion

|

|

Market Size (2034)

|

$2.3 Billion

|

|

Market Growth Rate

|

7.4%

|

|

Segments

|

By Product Chemistry (Acrylic-based Adhesives, Polyurethane Adhesives, Ethylene Vinyl Acetate Hot Melts, Styrenic Block Copolymers, Natural Rubber Latex, Plastic-Based Adhesives, Cyanoacrylate), By Technology (Water-Based/Emulsion Adhesives, Solvent-Based Adhesives, Hot Melt Adhesives, Pressure-Sensitive Adhesives, Reactive Adhesives, Film/Web Adhesives), By Function (Permanent Bond Adhesives, Temporary/Repositionable Adhesives, Heat Seal Adhesives), By End-Use Industry (Apparel and Textiles, Non-Woven Hygiene Products, Automotive Upholstery and Interior Trim, Footwear, Home Furnishings and Upholstery, Technical Textiles, DIY/Crafts and Consumer Repair), By Application Method (Liquid/Gel Dispense, Aerosol/Spray Application, Roll Coating/Laminating, Extrusion/Beading

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, H.B. Fuller Company, The Dow Chemical Company, BASF SE, 3M Company, Sika AG, Arkema SA, Huntsman Corporation, Pidilite Industries Ltd., Avery Dennison Corporation, NANPAO RESINS CHEMICAL GROUP, Toray Industries, Inc., Master Bond, Inc., RPM International Inc., Wacker Chemie AG

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Product Chemistry

- Acrylic-based Adhesives

- Polyurethane Adhesives

- Ethylene Vinyl Acetate Hot Melts

- Styrenic Block Copolymers

- Natural Rubber Latex

- Plastic-Based Adhesives

- Cyanoacrylate

By Technology/Formulation

- Water-Based/Emulsion Adhesives

- Solvent-Based Adhesives

- Hot Melt Adhesives

- Pressure-Sensitive Adhesives

- Reactive Adhesives

- Film/Web Adhesives

By Function

- Permanent Bond Adhesives

- Temporary/Repositionable Adhesives

- Heat Seal Adhesives

By End-Use Industry

- Apparel and Textiles

- Non-Woven Hygiene Products

- Automotive Upholstery and Interior Trim

- Footwear

- Home Furnishings and Upholstery

- Technical Textiles

- DIY/Crafts and Consumer Repair

By Application Method

- Liquid/Gel Dispense

- Aerosol/Spray Application

- Roll Coating/Laminating

- Extrusion/Beading

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- Henkel AG & Co. KGaA

- H.B. Fuller Company

- The Dow Chemical Company

- BASF SE

- 3M Company

- Sika AG

- Arkema SA

- Huntsman Corporation

- Pidilite Industries Ltd.

- Avery Dennison Corporation

- NANPAO RESINS CHEMICAL GROUP

- Toray Industries, Inc.

- Master Bond, Inc.

- RPM International Inc.

- Wacker Chemie AG

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the Global Fabric Glue Market across performance-critical uses in apparel, footwear, nonwovens, automotive interiors, home furnishings, and technical textiles; it delivers analysis reviews of chemistry choices, bond-line engineering, wash/sterilization durability, and automation-readiness while mapping regulatory trajectories (REACH, OEKO-TEX®, Prop 65) and procurement risks (feedstocks, energy intensity). It highlights breakthroughs in low-monomer PUR systems, bio-based hot melts validated to ASTM D6866, PU films for seamless apparel, and e-textile-ready insulating bonds—translating lab metrics (peel, shear, flex-fatigue, MVTR) into factory KPIs (line speed, set time, rework rates, cost-in-use). With side-by-side vendor benchmarking, price/technology heatmaps, and scenario planning for sustainability and reshoring, this report is an essential resource for R&D, sourcing, and operations leaders seeking safer, faster, and more durable fabric bonding at scale.

Scope Highlights

Segmentation:

- By Product Chemistry: Acrylic-based Adhesives; Polyurethane Adhesives; Ethylene Vinyl Acetate Hot Melts; Styrenic Block Copolymers; Natural Rubber Latex; Plastic-Based Adhesives; Cyanoacrylate.

- By Technology/Formulation: Water-Based/Emulsion; Solvent-Based; Hot Melt; Pressure-Sensitive; Reactive; Film/Web Adhesives.

- By Function: Permanent Bond; Temporary/Repositionable; Heat Seal.

- By End-Use Industry: Apparel & Textiles; Non-Woven Hygiene Products; Automotive Upholstery & Interior Trim; Footwear; Home Furnishings & Upholstery; Technical Textiles; DIY/Crafts & Consumer Repair.

- By Application Method: Liquid/Gel Dispense; Aerosol/Spray; Roll Coating/Laminating; Extrusion/Beading.

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Horizon: Historic data 2021–2024 and forecasts 2025–2034.

Companies: 15+ company analyses/profiles covering strategy, product portfolios, certifications, and sustainability roadmaps.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.