Market Overview: Growing Role of Film Adhesives in High-Performance Applications

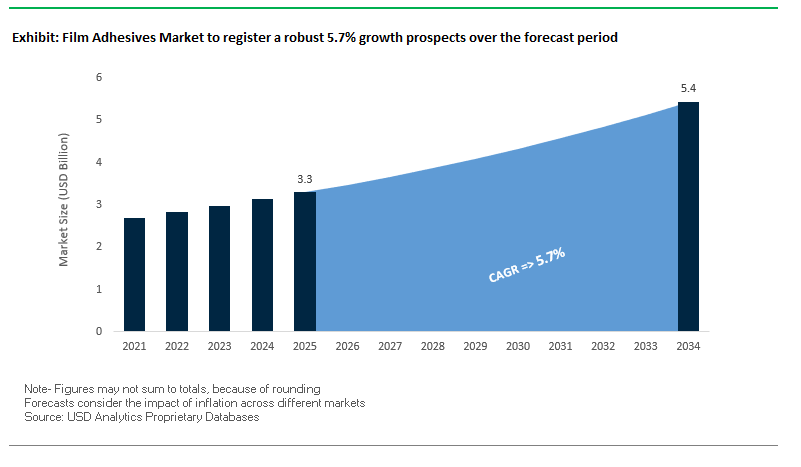

The Global Film Adhesives Market is projected to grow from USD 3.3 billion in 2025 to USD 5.4 billion by 2034, advancing at a CAGR of 5.7%. Film adhesives have emerged as a critical enabler in industries such as electronics, automotive, aerospace, and flexible packaging, where bonding strength, precision, and reliability are non-negotiable. Unlike liquid or paste adhesives, film adhesives are supplied in a solid, flexible sheet form, enabling controlled application, uniform bond lines, and minimal waste in high-value manufacturing processes.

A primary growth driver is the surging demand for hot melt adhesive films, valued for their rapid bonding, strong adhesion, and suitability for automated production lines. These adhesives are particularly popular in packaging and assembly operations, where speed and efficiency are paramount. In the electronics sector, the miniaturization of devices has amplified the importance of film adhesives for multi-layer flexible circuits, touch screens, and display components, all of which require thermal stability and chemical resistance.

Sustainability is also shaping market dynamics, with manufacturers investing in low-VOC, solvent-free, and bio-based film adhesives to meet stringent environmental regulations. In parallel, industries such as automotive and aerospace are increasingly relying on adhesive films for bonding composites and lightweight materials, contributing to reduced vehicle weight and improved fuel efficiency.

Key Insights for Industry Professionals:

- Market forecast: USD 3.3B (2025) → USD 5.4B (2034), CAGR 5.7%.

- Hot melt adhesive films gaining adoption for fast, efficient assembly.

- Electronics sector driving demand for precision bonding of miniaturized devices.

- Rising adoption of low-VOC, solvent-free, and bio-based adhesives.

- Automotive and aerospace lightweighting accelerating composite bonding applications.

Market Analysis: Recent Developments in the Film Adhesives Industry

The Film Adhesives Market is undergoing transformative changes, marked by new product launches, strategic mergers, and material innovations. Companies are focusing on enhancing adhesive performance while aligning with sustainability goals.

In August 2025, Park Aerospace Corp. introduced its Aeroadhere™ FAE-350-1 Structural Film Adhesive, specifically engineered for aerospace primary and secondary structures, reflecting the sector’s growing reliance on lightweight, high-strength adhesives. The same month, the Amcor–Berry Global merger was finalized, creating a packaging giant with broader capabilities in flexible packaging and adhesive film integration.

Earlier in April 2025, Smurfit Kappa and WestRock completed their merger, consolidating leadership in paper-based packaging, a move that will likely impact the use of lamination adhesives in corrugated and cartonboard solutions. In December 2024, DuPont™ showcased its Printed Tedlar® PVF Solutions at the Taipei Building Show, demonstrating the synergy between adhesive films and advanced building materials.

On the electronics front, 3M launched new optically clear adhesive films (November 2024) for touchscreens and displays, improving visual clarity and durability—a critical requirement in the consumer electronics industry. Meanwhile, Bostik (Arkema) unveiled solventless laminating adhesives (September 2024) to advance sustainability in flexible packaging.

Emerging Trends Transforming the Global Film Adhesives Market

Development of High-Thermal-Conductivity Dielectric Films for Electric Vehicles

The increasing electrification of the automotive industry is creating unprecedented demand for film adhesives that not only deliver strong structural bonding but also provide efficient thermal management. High-thermal-conductivity dielectric films are becoming essential in EV battery pack assembly, power module attachment, and electric motor construction, where adhesives must withstand high temperatures and repetitive thermal cycling. Industry studies on EV thermal management emphasize that thermally conductive adhesives help dissipate heat generated during charging and discharging, extending battery life, enhancing safety, and preventing thermal runaway. Leading adhesive companies are investing heavily in specialized epoxy resin formulations that achieve thermal conductivity levels as high as 2.1 W/m·K, offering manufacturers both energy efficiency and simplified curing processes. These adhesives are already being deployed to bond battery cells to cooling plates, ensuring vibration resistance and long-term durability in EV batteries. With global EV adoption accelerating, the market for thermally conductive film adhesives presents a major growth avenue, positioning companies that provide dual-function materials—thermal management plus structural stability—at a significant competitive advantage.

Adoption of Curing-On-Demand Technologies for Automation and Precision

Automation and precision are reshaping the electronics assembly industry, and curing-on-demand film adhesives are central to this transition. Unlike conventional heat-cured films, these adhesives cure instantly when triggered by UV light, pressure, or other stimuli, enabling high-speed production lines, enhanced precision, and simplified reworkability. According to specialty materials research, light-curable adhesives can cure in seconds, drastically improving throughput while eliminating the need for mixing or complex handling. Industry leaders are commercializing UV-curable die-attach film adhesives that offer consistent bondline thickness and eliminate liquid dispensing, unlocking new efficiencies in automated electronics assembly. R&D efforts are also focusing on dual-cure systems, combining UV curing with secondary heat or moisture activation for shadowed areas, ensuring complete curing in complex assemblies. This innovation is reshaping the film adhesives value chain, lowering labor costs, improving quality control, and fostering collaborations between adhesive manufacturers and automation equipment providers. As manufacturers seek to optimize precision and scalability, curing-on-demand adhesives are becoming a disruptive force in the market.

Formulation of Sustainable and Recyclable Adhesive Systems for Circular Economy

Sustainability is no longer optional, and the film adhesives market is facing a major opportunity with the development of recyclable adhesive systems that align with circular economy principles. Traditional adhesives often hinder disassembly, making recycling of multi-material products—such as electronics, EV batteries, and automotive components—highly inefficient. Innovative adhesive systems now allow for clean separation at end-of-life, enabling recovery of valuable materials. Industry publications highlight that “design for sustainability” requires adhesives to be compatible with recycling processes from the earliest stages of product development. Several adhesive manufacturers are pioneering thermoplastic film adhesives that can be reheated to enable disassembly, a critical breakthrough for smartphones, laptops, and consumer electronics recycling. This opportunity extends beyond technical innovation to brand value, as manufacturers can market recyclable adhesives as both functional and eco-conscious solutions, directly appealing to sustainability-driven consumers. On a value chain level, these advancements are fostering collaboration between adhesive makers, product designers, and recyclers, creating an integrated ecosystem that enhances both environmental compliance and profitability.

Miniaturization and High-Frequency Performance for 5G/6G Infrastructure

The deployment of 5G and upcoming 6G networks requires adhesives that can meet unprecedented technical specifications, particularly in the areas of signal integrity, low dielectric loss, and ultra-thin bonding. Traditional liquid adhesives, with higher dielectric constants, often interfere with high-frequency signal transmission, creating opportunities for film adhesives engineered for minimal signal loss at mmWave frequencies. Technical studies on 5G antennas underscore the importance of adhesives with low dielectric constant and low loss tangent, ensuring stable performance at ultra-high frequencies. To meet this demand, manufacturers are introducing ultra-thin film adhesives with uniform bondline thickness using materials such as liquid crystal polymers (LCPs), which retain their electrical properties even under extreme conditions. These advanced formulations are proving critical for semiconductor packaging, antenna modules, and next-gen base station equipment. The opportunity extends beyond product innovation—this segment is driving new partnerships between adhesive suppliers and semiconductor manufacturers, forging a value chain that integrates electronic reliability with next-generation wireless performance. With global investment in 5G infrastructure soaring and 6G research underway, companies that can supply high-frequency-optimized adhesives are set to capture a significant share of this fast-growing market.

Competitive Landscape: Key Companies Shaping the Film Adhesives Market

The Global Film Adhesives Industry is competitive, with leaders leveraging material science expertise, global distribution, and sustainability-driven innovation to expand their market share.

Henkel AG & Co. KGaA focuses on sustainable adhesive innovation

Henkel is a global leader with its Loctite® brand, offering a wide portfolio of film adhesives for packaging, automotive interiors, and structural applications. The company invests heavily in low-VOC and solvent-free adhesives, aligning with sustainability regulations. Its strategy emphasizes digital integration and customized bonding solutions, ensuring efficiency in supply chain operations.

3M Company advances optically clear adhesives for electronics

3M leverages its deep materials science expertise to develop specialized adhesives for electronics, medical devices, and aerospace. In November 2024, it launched new optically clear adhesive films that enhance touchscreen clarity and durability. Its portfolio includes pressure-sensitive films and transfer tapes, widely used in structural and electronic bonding. 3M’s focus is on sustainable design and advanced electronics applications.

H.B. Fuller strengthens polyurethane-based film adhesive portfolio

H.B. Fuller is expanding in high-performance industrial adhesives, particularly polyurethane film adhesives known for strength and durability. Its solutions serve flexible packaging, automotive trim bonding, and electronics assembly. The company’s strategy involves targeted acquisitions and investments in sustainable innovation, reinforcing its position in industrial and consumer adhesives.

Arkema Group expands solventless and UV-curable adhesive technologies

Through its subsidiary Bostik, Arkema offers a multi-technology portfolio spanning solventless, hot melt, and waterborne film adhesives. In September 2024, Bostik launched a new solventless laminating adhesive line, strengthening its role in flexible packaging. Arkema is also advancing UV-curable and moisture-curing adhesives, aligning with faster curing times and eco-friendly regulations.

Dow Chemical Company leads with specialty adhesive coatings

Dow is a key player in materials and polymer innovation, offering silicone release coatings, fluoropolymer adhesives, and flexible electronics bonding solutions. Its adhesive technologies are widely used in tapes, labels, and electronic components, where high frequency and thermal stability are required. Dow’s focus is on sustainability and next-generation electronics packaging, backed by continuous R&D.

Film Adhesives Market Share Insights

Epoxy Films Dominate Market Share by Adhesive Type in the Film Adhesives Industry

Epoxy adhesives hold the largest share of the film adhesives industry, accounting for 35% of the market. Their dominance is attributed to their unmatched structural strength, thermal resistance, and long-term durability, which make them indispensable in aerospace, automotive, and high-performance electronics. These industries demand bonding solutions that can withstand extreme stress, vibration, and environmental exposure without compromising reliability. Epoxy films are widely deployed in composite-to-metal bonding for aircraft structures, high-load automotive parts, and semiconductor die-attach processes, where product failure is not an option. The combination of superior mechanical integrity and chemical resistance ensures that epoxy adhesives remain the backbone of critical manufacturing applications, anchoring their top market share despite higher cost compared to alternatives.

Electronics Secure the Largest Market Share by End-Use in the Film Adhesives Industry

Electronics account for 40% of demand in the film adhesives market, making them the leading end-use sector. This dominance is driven by the rapid miniaturization of devices, proliferation of flexible printed circuits, and growing reliance on multilayer laminates in smartphones, wearables, and IoT devices. Film adhesives play a pivotal role in bonding delicate components, providing EMI shielding, and enabling thermal management, all of which are crucial for device performance and longevity. As consumer electronics and electric vehicles continue to drive exponential demand for advanced semiconductors and displays, electronics packaging and assembly requirements will further cement this sector’s leadership in the market.

United States Film Adhesives Market Driven by Low-VOC Technologies and Advanced Packaging Solutions

The U.S. film adhesives market is heavily influenced by Environmental Protection Agency (EPA) regulations on volatile organic compounds (VOC), prompting a shift from solvent-based to water-based and low-VOC adhesive technologies. Technological advancements are reshaping the industry, with innovations like epoxy silane-free laminating adhesives for flexible packaging offering strong adhesion, durability, and enhanced environmental performance. Notable product launches include Drytac’s SpotOn Duo in August 2025, a double-sided graphics adhesive film with permanent adhesion on one side.

Corporate investments are expanding production capacity for sustainable solutions, exemplified by Sonoco Products Co.’s $30 million facility expansion in August 2025, adding 100 million additional units of adhesive packaging. Key applications span electronics, automotive, and packaging sectors, driven by the demand for lightweight vehicles and miniaturized electronics requiring efficient bonding solutions. Sustainability is a core focus, with companies like Avery Dennison developing recyclable RFID labels, while government initiatives such as the CHIPS and Science Act are directly boosting demand for high-quality adhesives to protect sensitive semiconductor components.

Germany Film Adhesives Market Strengthened by Circular Economy Leadership and Advanced Industrial Applications

Germany’s film adhesives market operates under a stringent regulatory framework, including the EU Packaging and Packaging Waste Regulation (PPWR), which mandates full recyclability or reusability by 2030. The national Extended Producer Responsibility (EPR) system incentivizes manufacturers to produce recyclable packaging, driving innovation in adhesive technologies. Companies are also investing in machinery capable of handling sustainable materials, while initiatives like digital product passports and packaging watermarks improve material transparency and recycling.

Technological innovation is central, with the Utz Group investing in nanotube-based ESD materials to provide superior protection for electronics without contamination issues from carbon black. Key applications focus on automotive, electronics, and industrial sectors, with electric vehicle (EV) production and advanced manufacturing increasing demand for adhesives that safeguard sensors and battery systems. Sustainability efforts are reinforced by PPWR mandates on reusable transport packaging, while strategic collaborations between adhesive producers and brand owners are shaping high-performance, environmentally responsible solutions.

China Film Adhesives Market Expanding Through Domestic Manufacturing and Government Sustainability Initiatives

China’s film adhesives industry is being propelled by governmental sustainability goals, including the 2025 Action Plan for Promoting Large-Scale Equipment Updates, which encourages recycling and the adoption of sustainable materials. Regulatory reforms addressing excessive packaging, effective since September 2023, influence adhesive applications in e-commerce and consumer goods.

Technological advancements, particularly AI-driven automation and the integration of “5G plus industrial internet,” are optimizing production efficiency and flexible manufacturing capacity. Local companies like YG are expanding domestic production, exemplified by their 120-acre automotive adhesive film facility with a 4,000-square-meter Class 1000 cleanroom. Key applications are concentrated in automotive, electronics, and e-commerce packaging, with the country’s strong manufacturing base and digital printing needs driving significant growth for high-quality, circular film adhesives.

Japan Film Adhesives Market Innovating Through High-Performance Materials and Regulatory Sustainability

Japan’s film adhesives market is at the forefront of precision manufacturing, with the automotive sector representing a crucial application. Advanced technologies, including high-performance films with superior barrier properties and IoT integration for real-time monitoring, are transforming the market. Nippon Molding’s investments in dry-molded fiber technologies demonstrate a shift toward sustainable production with lower energy and water usage.

Regulatory guidance, under the Plastic Resource Circulation Act effective since April 2022, promotes environmentally friendly design and reduces single-use plastics. The industry is innovating in functionality, producing adhesives with high dimensional stability, resistance to deformation, and specialized properties for demanding applications. Corporate collaborations, such as Sika AG’s acquisition of Hamatite from Yokohama Rubber Co., are expanding technological capabilities and strengthening the market’s competitive dynamics across automotive and construction segments.

United Kingdom Film Adhesives Market Accelerating Through Extended Producer Responsibility and Sustainable Innovation

The UK film adhesives market is being reshaped by the new Extended Producer Responsibility (EPR) system, which places recycling obligations on producers, and initiatives like the UK Plastics Pact that encourage sustainable packaging. Companies are actively investing in eco-friendly adhesives made from recycled and bio-based materials, with products designed for easy de-bonding and recyclability.

Technological innovation is driven by the country’s robust research ecosystem in chemical and materials sciences, leading to durable, high-bonding, and environmentally friendly adhesive formulations. Key applications are concentrated in consumer goods, food and beverage, and automotive sectors, supported by the UK’s strong manufacturing base. Corporate investments and collaborations with research institutions are accelerating the production of sustainable film adhesives, positioning the UK as a leader in environmentally responsible packaging solutions.

Film Adhesives Market Report Scope

Film Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.3 Billion

|

|

Market Size (2034)

|

$5.4 Billion

|

|

Market Growth Rate

|

5.7%

|

|

Segments

|

By Adhesive Type (Acrylic, Epoxy, Polyurethane, Silicone, Others), By Technology (Solvent-Based, Water-Based, Hot-Melt, Others), By End-Use Industry (Automotive, Electronics, Aerospace, Packaging, Medical & Healthcare, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

3M Company, Henkel AG & Co. KGaA, Avery Dennison Corporation, H.B. Fuller Company, Sika AG, Arkema S.A., Nitto Denko Corporation, Dow Inc., Lohmann GmbH & Co. KG, Tesa SE, Toyochem Co., Ltd., Delo Industrial Adhesives, Mactac Americas, Wacker Chemie AG, Jowat SE

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Film Adhesives Market Segmentation

By Adhesive Type

- Acrylic

- Epoxy

- Polyurethane

- Silicone

- Others

By Technology

- Solvent-Based

- Water-Based

- Hot-Melt

- Others

By End-Use Industry

- Automotive

- Electronics

- Aerospace

- Packaging

- Medical & Healthcare

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Film Adhesives Market

- 3M Company

- Henkel AG & Co. KGaA

- Avery Dennison Corporation

- H.B. Fuller Company

- Sika AG

- Arkema S.A.

- Nitto Denko Corporation

- Dow Inc.

- Lohmann GmbH & Co. KG

- Tesa SE

- Toyochem Co., Ltd.

- Delo Industrial Adhesives

- Mactac Americas

- Wacker Chemie AG

- Jowat SE

* List Not Exhaustive

Methodology

USDAnalytics employed a rigorous, multi-dimensional research methodology to deliver an authoritative analysis of the Global Film Adhesives Market. The approach combined primary research—including interviews with adhesive manufacturers, R&D leaders, and industry supply chain experts—with secondary research from company reports, press releases, regulatory filings, and industry publications. Quantitative forecasting models were applied to assess market growth by adhesive type, technology, and end-use sector, while qualitative insights explored trends such as hot-melt films, curing-on-demand technologies, thermal management adhesives, and sustainable, recyclable formulations. Regional dynamics in the U.S., Germany, China, Japan, and the UK were analyzed in detail, considering environmental regulations, circular economy initiatives, and automotive, electronics, aerospace, and packaging adoption. USDAnalytics also examined recent innovations in high-frequency 5G/6G adhesives, dielectric and optically clear films, and lightweight composite bonding, ensuring a holistic, data-driven perspective that equips industry professionals with actionable insights for strategic planning, technology investment, and operational optimization in the rapidly evolving film adhesives landscape.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.