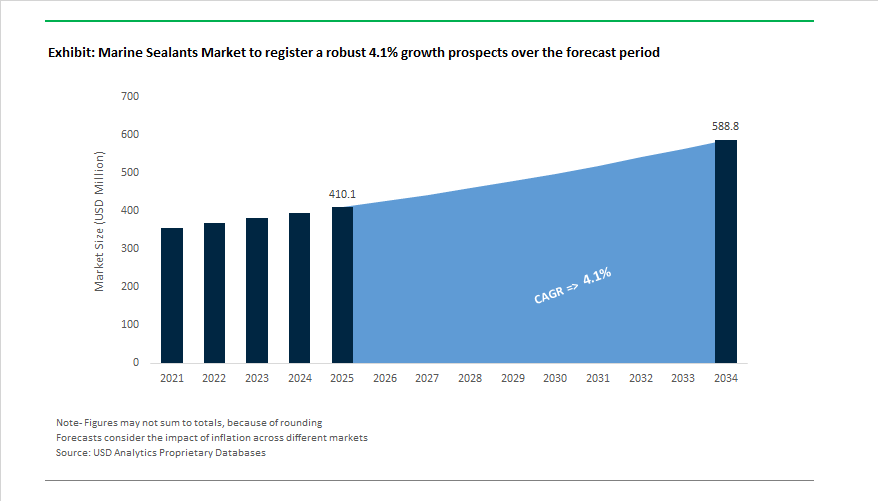

The Global Marine Sealants Market is projected to expand from USD 410.1 million in 2025 to USD 588.8 million by 2034, growing at a CAGR of 4.1%, as sealants become regulatory-critical and performance-defining materials in modern vessel construction and refurbishment. Unlike volume-driven consumables, marine sealants are specified around movement tolerance, fire performance, and long-term environmental resistance, making them integral to vessel safety certification and lifecycle durability across commercial shipping, naval platforms, offshore assets, and high-end recreational craft.

A core demand driver is the increase in structural movement and material heterogeneity in contemporary shipbuilding. Lightweight composites, aluminum superstructures, large-format glazing, and modular assemblies introduce differential thermal expansion and flexing that traditional rigid fillers cannot accommodate. As a result, high-flexibility polyurethane, silane-modified polymer (SMP), and polysulfide sealants are increasingly specified for hull-to-deck joints, windows, expansion joints, and underwater penetrations. ASTM C920 Class 50 elastomeric sealants, offering ±50% movement capability, have become a de facto benchmark in these applications, ensuring adhesion integrity under continuous vibration, wave loading, and thermal cycling.

Safety regulation is further reshaping formulation and qualification requirements. Passenger vessels, offshore platforms, and naval ships are subject to increasingly stringent IMO Fire Test Procedures (FTP Code Annex 1, Part 3), driving adoption of fire-rated sealants certified from A-0 to A-60 for bulkheads, decks, and service penetrations. At the same time, REACH compliance and VOC reduction mandates are accelerating the transition toward low-VOC polyurethane systems and bio-based SMP technologies, particularly in enclosed onboard environments where worker exposure and indoor air quality are critical. These constraints have elevated sealant selection into a risk-management decision, closely scrutinized by classification societies and shipowners alike.

Application-specific performance continues to differentiate value. In deck systems, particularly teak caulking for luxury yachts, one-component polyurethane sealants delivering 3.0 MPa tensile strength and elongation exceeding 600% are preferred for their balance of elasticity, abrasion resistance, and sandability. For structural bonding and glazing, SMP and MMA-based sealants are increasingly used in composite hull sections and large glass installations, where cohesive strengths above 10 MPa and inherent vibration damping improve durability without inducing stress cracking.

The marine sealants market is experiencing rapid innovation, capacity expansion, and regulatory alignment, reflecting both environmental and structural performance advancements.

In February 2024, Henkel AG & Co. KGaA finalized its acquisition of Seal for Life Industries, a strategic move expanding its reach in corrosion protection and sealing technologies for marine infrastructure, pipelines, and offshore assets. This acquisition solidifies Henkel’s position as a leading player in the marine MRO segment, integrating coatings and sealants under a unified sustainability-driven portfolio.

In May 2024, 3M announced a USD 67 million expansion of its Valley, Nebraska facility, adding over 90,000 square feet to scale up manufacturing of polyurethane marine adhesive-sealants. The expansion highlights North America’s growing focus on recreational boating and repair applications, where 3M’s high-demand products such as Marine Adhesive Sealant 5200 and 4000 UV dominate the market.

DuPont’s July 2024 introduction of its new Great Stuff Wide Spray Foam Sealant marked a technology crossover into marine applications, offering thermal and gap-sealing advantages for climate-controlled vessel interiors and insulation-critical compartments.

By September 2024, Arkema’s Bostik reinforced its sustainability focus with a bio-based instant adhesive (60% renewable content), a development signaling the company’s ongoing efforts to green its polyurethane and SMP marine sealant lines. In the same month, BioBond Adhesives, Inc. established its R&D headquarters in Indiana to pioneer biodegradable plant-based sealant formulations, directly addressing sustainability pressures from yacht and interior marine manufacturers.

In November 2024, Henkel and Celanese formed a partnership to co-develop CO₂-derived emulsion polymers for adhesive and sealant production, advancing circular economy goals and decarbonization within polymer supply chains. During the same month, Arxada unveiled its Omadine® technology for antifouling coatings and adhesive additives at ChinaCoat 2024, emphasizing performance enhancements in UV and microbial resistance for integrated marine coating-sealant systems.

Regulatory developments further shaped market direction. The IMO Maritime Safety Committee’s fire safety amendments, adopted in May 2024 and effective July 2025, raised compliance requirements for Ro-Ro passenger ships, making fire-rated marine sealants a core material consideration in new builds and retrofits.

Market Trend 1: Accelerated Shift Toward Silicone and MS Polymer-Based, Non-Toxic Sealants

The transition toward silicone-based and MS polymer marine sealants is reshaping the industry, primarily due to regulatory frameworks such as the European Union’s REACH standards and the IMO MARPOL Annex VI, which strictly limit volatile emissions and toxic additives in marine operations. Modern silane-modified polymer (SMP) and MS polymer-based sealants have emerged as the preferred alternatives to solvent-based urethanes, offering Very Low VOC levels (≤40 g/L) while being solvent-free and isocyanate-free. The compliance-driven evolution reflects a broader sustainability shift toward low-emission shipbuilding materials that meet both environmental and occupational safety standards.

Performance testing drives the superior reliability of these advanced formulations. Laboratory trials on premium SMP marine sealants have demonstrated over 2,000 hours of salt spray resistance (per ASTM B117) without visible corrosion and UV retention above 96% (ISO 4892). The exceptional resistance to harsh marine conditions positions MS polymers as the benchmark for long-term durability and corrosion prevention in both vessel construction and maintenance.

Another major driver accelerating the trend is cross-sector adoption. The construction industry, a close analog to shipbuilding in material joining technologies, has already witnessed a 64% transition to MS polymer hybrid adhesives and sealants, driven by VOC regulations and enhanced performance needs. The transition serves as a predictive indicator of widespread adoption in the marine sector, as shipyards increasingly seek flexible, eco-safe, and high-strength sealing systems for hull joints, deck assemblies, and interior fixtures.

Market Trend 2: Adoption of High-Modulus, Rapid-Cure Sealants to Enable Automation and Faster Vessel Production

A pivotal development in the marine adhesives and sealants market is the integration of rapid-cure, high-modulus sealants designed to accelerate shipyard production cycles. Traditional sealants often require extended curing times, slowing assembly lines; however, modern 1C and 2C accelerated curing systems, such as proprietary PowerCure or Booster technologies, achieve handling strength within hours. The enables faster workstation transitions and minimizes downtime during the assembly of large vessel structures.

These rapid-curing systems are instrumental in advancing shipbuilding automation, especially in modular and pre-fabricated vessel construction. Although robotic automation in shipbuilding remains complex due to the irregular geometries of vessel interiors, fast-bonding sealants allow automated application systems to efficiently assemble large composite panels, bulkheads, and deck modules. The shift reduces the reliance on traditional fasteners like rivets and screws while enhancing consistency, strength, and sealing quality across production lines.

As global shipyards pursue efficiency gains under tight delivery schedules, the adoption of fast-curing marine sealants becomes critical to meeting both production speed and performance requirements. These materials not only improve throughput but also deliver long-term fatigue resistance and elastic modulus stability, ensuring their compatibility with dynamic marine loads and vibration conditions.

Market Opportunity 1: Expansion of the Offshore Wind Vessel Fleet Driving Long-Term Sealant Demand

The offshore wind energy sector represents a rapidly expanding market for marine sealant manufacturers, particularly for Wind Turbine Installation Vessels (WTIVs) and Service Operation Vessels (SOVs). Supported by strong policy frameworks such as the U.S. Inflation Reduction Act (IRA), which extends a 30% Investment Tax Credit (ITC) for offshore wind projects, the global market has seen approximately $17 billion in offshore wind investment since 2014—including nearly $1 billion in port and vessel infrastructure in 2022 alone.

The surge in capital investment directly translates into demand for high-durability marine sealants that provide superior resistance to vibration, salt exposure, and dynamic loads experienced during turbine transport and installation. With offshore wind capacity reaching 57.6 GW by the end of 2022, the industry’s projected vessel fleet expansion is set to multiply sealant consumption for critical applications such as hull sealing, structural bonding, vibration isolation, and noise reduction in offshore service vessels.

In parallel, the UK’s ambitious 50 GW offshore wind target by 2030, including 5 GW of floating wind, reinforces the global momentum toward offshore energy vessel construction. Manufacturers offering low-VOC, high-strength, and elastomeric sealants for these specialized vessels are strategically positioned to capitalize on the expanding renewable marine economy. The intersection of sustainability regulations and offshore infrastructure growth thus defines a high-value segment for next-generation marine sealant technologies.

Market Opportunity 2: Advanced Leak-Sealing Solutions for Aging Global Port and Marine Infrastructure

A significant emerging opportunity lies in port infrastructure rehabilitation, particularly in regions with aging concrete and steel marine assets. As maritime traffic intensifies and climate change stresses coastal systems, the need for advanced leak detection and sealing solutions is becoming urgent. Global case studies in major Asian ports demonstrate the potential of non-invasive leak mitigation systems—combining advanced pressure management and injectable sealant technologies—to prevent catastrophic water loss and structural degradation.

In the infrastructure-grade sealants market, demand is rapidly rising for submerged and underwater-curable MS polymer sealants that maintain zero water migration under hydrostatic pressure. These formulations are increasingly used for dock wall repairs, lock maintenance, and concrete substructure restoration, where traditional sealants fail to adhere effectively to damp or submerged surfaces. Manufacturers focusing on hybrid and injectable sealants engineered for underwater or high-moisture applications are seeing growing demand from public infrastructure authorities and private port operators.

The trend drives a wider strategic opportunity for the marine sealants industry to expand beyond shipbuilding into critical marine infrastructure maintenance, aligning with global efforts to modernize waterway and port facilities. The development of high-performance, long-life, and environment-safe sealant systems for submerged or structural repair thus represents a high-margin growth avenue that complements the sector’s transition toward sustainability and innovation.

Marine Sealants Market Share Insights, 2025-2034

Market Share by Application Area

The below water-line sealing segment dominates the global marine sealants market, accounting for a projected 28.8% share in 2025, as it represents the most critical and technically demanding application in marine construction and maintenance. Below water-line areas—including hull seams, through-hull fittings, rudder posts, propeller shafts, and keel joints—require high-performance sealants that can withstand continuous immersion, hydrostatic pressure, saltwater exposure, and mechanical stress. Marine-grade polyurethane and polysulfide formulations are the most commonly used technologies in this segment, offering permanent flexibility, excellent adhesion to metals and composites, and long-term resistance to degradation. The dominance of this segment is reinforced by the global focus on vessel integrity and safety compliance, as sealant failure in submerged areas can lead to catastrophic water ingress and structural compromise. Furthermore, the growing use of fiber-reinforced composites and aluminum hulls in both commercial and leisure vessels has increased demand for chemically compatible, corrosion-inhibiting sealant technologies. Innovations in hybrid silane-modified polymers (SMPs) are also gaining traction below the waterline for providing superior UV stability and adhesion without primer, reflecting the industry’s shift toward eco-friendly, solvent-free solutions.

Deck-to-hull joint sealing and above water-line sealing applications form substantial segments of the market, accounting for a large share of sealant consumption across both new shipbuilding and maintenance, repair, and overhaul (MRO) operations. These applications involve exposed areas such as joints, fasteners, hatches, and deck fittings, where sealants must resist UV exposure, salt spray, thermal cycling, and vibration fatigue while maintaining elasticity. Advanced silicone and hybrid SMP sealants are widely used for their durability, non-yellowing finish, and compatibility with multiple substrates, including gelcoat, fiberglass, and aluminum. Window bonding and glazing applications are highly specialized—requiring optically clear, UV-resistant, and non-shrinking sealants that can maintain watertight integrity without compromising visibility.

Similarly, engine casing sealing and structural bonding segments serve critical roles in marine propulsion, engine housings, and equipment enclosures, demanding high heat resistance, oil compatibility, and vibration dampening. These applications are central to performance and safety in both commercial shipping and naval vessels, where polyurethane and epoxy-modified sealants ensure mechanical stability under heavy-duty conditions. Electrical housing and systems sealing, while representing a niche market, is vital for preventing corrosion and ensuring insulation in navigation electronics, sensors, and power units exposed to marine humidity.

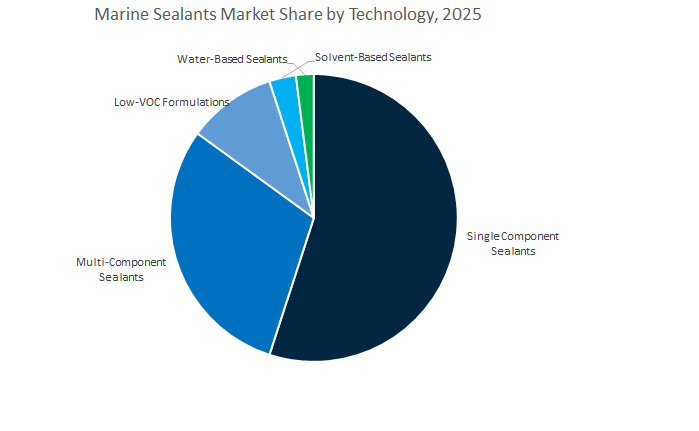

Market Share by Form/Technology

The single-component marine sealants segment leads the global marine sealants market, commanding a projected 51.6% share in 2025, driven by their ease of application, lower installation time, and versatility across repair, maintenance, and general assembly operations. Single-component formulations are preferred in shipyards, dockyards, and on-board maintenance environments where quick and consistent sealing performance is required without complex mixing or curing equipment. These sealants, available in cartridge, sausage, and bulk packaging, offer excellent adhesion, flexibility, and weathering resistance for a wide range of substrates including fiberglass, steel, aluminum, and wood. Their dominance is further supported by the rise in small vessel production, yacht refurbishing, and recreational boating maintenance, where user-friendly products enhance efficiency and reduce labor costs. Technological advancements in MS polymer (silyl-terminated polymer) sealants have further extended their performance range, providing superior UV resistance, solvent-free formulations, and improved paintability, aligning with the industry’s transition toward sustainable and low-VOC marine sealing systems.

Multi-component sealants, typically two-part polyurethane and epoxy-based systems, maintain a strong position for structural and high-performance marine applications. These systems are indispensable in shipbuilding, offshore structures, and heavy-duty industrial vessels, where maximum adhesion, mechanical strength, and chemical resistance are required. Although they demand on-site mixing and precise ratio control, their superior durability and resistance to marine fuels, oils, and hydrostatic pressure make them the material of choice for critical joints and underwater structures. Growth in naval defense programs and commercial vessel retrofits continues to bolster this segment.

Meanwhile, low-VOC formulations are experiencing significant growth, driven by tightening global environmental regulations and the maritime industry’s increasing emphasis on crew health, safety, and green compliance. These products, primarily water-based or solvent-free hybrids, reduce emission levels during application in confined spaces such as ship interiors, cabins, and tanks. Though solvent-based and water-based sealants represent smaller market shares, they serve specialized functions where fast cure time, surface tolerance, or specific substrate bonding is essential. Solvent-based systems, while declining, are still preferred in legacy maintenance operations, while water-based formulations are emerging for eco-conscious shipyards in regions with strict environmental norms.

The Global Marine Sealants Industry is shaped by the innovation and strategic direction of leading manufacturers like Sika AG, Henkel, H.B. Fuller, Arkema (Bostik), and Parker Hannifin (LORD Corporation). Their focus on hybrid polymer systems, low-VOC formulations, and integrated MRO solutions continues to set performance benchmarks across both OEM and aftermarket marine segments.

Sika AG dominates the marine segment with its specialized Sikaflex® Marine product range, fully certified under the IMO Marine Equipment Directive (MED). Its flagship Sikaflex®-290 DC PRO polyurethane sealant, with 600% elongation at break (ISO 527), is the industry standard for teak deck caulking and above-waterline applications. The company’s complete system approach—combining primers (Sika® Primer-290 DC) and bonding agents—ensures UV resistance and long-term adhesion on timber and composite decks.

Recent innovations such as SikaBOND®-Panel systems illustrate Sika’s strategic goal of replacing mechanical fastening and welding with lightweight, high-strength sealing and bonding systems, reducing vessel weight and installation time.

H.B. Fuller brings unmatched expertise in polysulfide and MMA (Methyl Methacrylate) sealants and adhesives, designed to endure saltwater immersion, thermal fatigue, and mechanical stress. Its solutions are widely deployed in below-waterline sealing and hull-to-deck joints, where adhesion to GRP, aluminum, and exotic composites is vital.

Through its Weld Mount System, H.B. Fuller has revolutionized adhesively bonded fastener technology, eliminating drilling requirements and reducing structural leak risks. Operating 81 production sites across 26 countries, the company supports global MRO projects with localized supply and engineering assistance.

Henkel’s acquisition of Seal for Life Industries (February 2024) marked a significant expansion into corrosion protection and subsea sealing solutions, complementing its established Loctite® range of polyurethane, silicone, and epoxy-based marine sealants.

Henkel’s focus on fast-curing one-component systems helps shipyards accelerate production cycles, while its CO₂-based polymer R&D partnership with Celanese signals a strong shift toward sustainable raw material sourcing. The company’s sealant systems cater to offshore, pipeline, and naval repair applications, ensuring both long-term durability and environmental compliance.

Arkema’s Bostik continues to lead the transition toward non-isocyanate Silane Modified Polymer (SMP) sealants known for excellent UV stability, solvent-free composition, and superior adhesion on substrates like teak, aluminum, and glass.

With a growing footprint in the recreational and luxury yacht sector, Bostik’s marine-grade SMP sealants are favored for interior and exterior finishing, offering high elasticity and minimal shrinkage. The company is investing heavily in bio-based SMP formulations, aligning with future EU environmental directives and providing high-performance non-yellowing, low-VOC alternatives to traditional polyurethanes.

Parker Hannifin, through its LORD Corporation division, provides specialized Chemlok® bonding and sealant systems for rubber-to-metal interfaces, essential in marine applications such as engine mounts, vibration dampers, and sonar components.

Its Chemlok® Cold Bond (CB) adhesive-sealants offer room-temperature curing and VOC-free bonding, making them ideal for on-site maintenance without specialized heat curing. By eliminating harmful solvents like trichloroethylene (TCE), LORD aligns with stringent EHS regulations, offering products that support quieter, more comfortable, and environmentally compliant naval operations.

Country Analysis: Global Marine Sealants Industry

China: Shipbuilding Expansion and VOC Regulation Drive Polyurethane Marine Sealant Demand

China remains the largest shipbuilding nation in the world, and The dominance extends to its consumption of marine-grade polyurethane and silicone sealants. The country’s massive output of LNG carriers, container ships, and commercial vessels fuels a high-volume demand for durable, cost-efficient, and rapid-cure marine sealants suitable for both hull and deck applications.

The Chinese government’s push for “green manufacturing” and maritime modernization is reinforcing the shift toward low-VOC, solvent-free formulations, including waterborne and hybrid sealants. The establishment of new OEM shipyards in coastal hubs such as Jiangsu and Guangdong has created demand for fast-curing polyurethane sealants that enable same-day painting and sanding, improving production efficiency. Moreover, expanded naval and port infrastructure—including new terminals, drydocks, and waterfront facilities—continues to generate significant consumption of industrial-grade polysulfide sealants for joint waterproofing and corrosion protection.

China’s focus on scaling both commercial and defense shipbuilding has made it a strategic global hub for marine bonding and sealing technologies, with increasing opportunities for international sealant manufacturers supplying certified fire- and corrosion-resistant materials for export-compliant vessels.

South Korea: LNG Carrier Production Spurs Demand for High-Performance Hybrid Marine Sealants

South Korea’s shipbuilding leadership, particularly in LNG carriers and ultra-large container ships, drives consistent demand for premium marine sealants that can endure extreme mechanical and thermal stresses. Korean shipyards—home to industry leaders like Hyundai Heavy Industries, Daewoo Shipbuilding & Marine Engineering, and Samsung Heavy Industries—prioritize high-performance silicone and MS Polymer hybrid sealants that deliver superior UV resistance and elasticity.

In alignment with stringent environmental regulations, South Korea is increasingly adopting low-VOC, solvent-free hybrid sealants, a shift influenced by the EU’s REACH standards due to the high proportion of vessels exported to Europe. Domestic R&D collaborations between Korean chemical companies and shipyards are focusing on zero-leakage rotary seal systems for propulsion and rudder assemblies, enhancing long-term vessel integrity.

The nation’s ongoing naval procurement and fleet modernization programs also sustain demand for defense-grade marine sealants featuring resistance to fire, salt corrosion, and pressure extremes. As a result, South Korea continues to play a central role in advancing next-generation marine sealing technologies within the Asia-Pacific region.

Japan: Precision Marine Manufacturing Fuels High-Quality Silicone and MS Polymer Sealant Market

Japan’s marine industry emphasizes precision manufacturing, high quality, and environmental responsibility, creating steady demand for silicone and MS Polymer hybrid sealants used in commercial and defense shipbuilding. With its large fleet of ferries, fishing vessels, and high-speed crafts, Japan requires consistent supplies of certified polysulfide and polyurethane caulking compounds for maintenance, repair, and overhaul (MRO) operations.

Japanese adhesive and sealant manufacturers are spearheading the development of low-emission and eco-certified marine sealants, supporting the country’s transition toward sustainable shipbuilding materials. Investments in composite boat construction—including hybrid-material hulls—necessitate adhesion promoters and flexible sealants designed for mixed substrates. Furthermore, Japan’s luxury yacht and high-speed craft industries demand non-sag, custom-color polyurethane sealants that provide superior aesthetic and mechanical performance.

United States: Advanced Naval and Recreational Marine Applications Dominate Sealant Use

The United States marine sealants market spans defense, recreational, and commercial marine applications, characterized by strong innovation and regulatory oversight. In the recreational boating sector, brands like 3M Marine, RPM International, and TotalBoat dominate with easily tooled polyurethane and silicone sealants distributed through major MRO channels. The sector’s robust aftermarket maintenance culture ensures recurring demand for high-durability cartridge sealants that simplify application and reduce curing time.

In parallel, U.S. Navy shipbuilding and modernization programs continue to require blast- and fire-resistant sealants that comply with military standards (MIL-S-8802, MIL-PRF-81733). The specialized products are essential for structural joints, hatches, and under-deck sealing in advanced naval vessels.

Environmental regulations led by the EPA and California’s Air Resources Board (CARB) are accelerating the adoption of low-VOC hybrid formulations, particularly in the new boat construction sector. Furthermore, rapid-cure adhesive/sealant systems are being integrated into high-volume production facilities to cut assembly times and improve operational efficiency. The positions the U.S. as a global benchmark for high-performance and sustainable marine sealant innovation.

Germany and the Netherlands: Europe’s Green Shipping Leaders and Innovation Powerhouses

Germany and the Netherlands remain at the forefront of Europe’s sustainable shipbuilding and MRO (maintenance, repair, and overhaul) markets, defined by strict environmental standards and high adoption of hybrid and silicone marine sealants. European compliance frameworks—such as the International Maritime Organization (IMO) environmental regulations and the EU Green Deal directives—are pushing shipbuilders toward solvent-free, low-VOC technologies.

In 2024, Sika AG expanded its marine-grade hybrid sealant range, introducing a high-adhesion, low-emission formulation suitable for mixed-material hulls and composite yachts. European fleets’ increasing maintenance needs, including offshore installations and merchant ships, further drive demand for high-chemical-resistance polysulfide sealants.

Additionally, the luxury yacht segment in Northern Europe—particularly in the Netherlands—is a significant consumer of aesthetic hybrid sealants optimized for deck caulking, high-gloss finishes, and flexible jointing. Supported by active shipyard investments and EU-driven circular economy goals, the region remains the epicenter of marine sealant R&D, sustainability, and design innovation in the global market.

Brazil: Offshore Energy Projects and Naval Infrastructure Boost Marine Sealant Consumption

Brazil’s marine sealants market is closely tied to its offshore oil and gas industry, where extreme operational environments require chemically resistant and pressure-tolerant sealing materials. Major offshore platforms, including FPSOs (Floating Production Storage and Offloading units), rely heavily on high-performance polysulfide and polyurethane sealants capable of withstanding prolonged saltwater exposure and dynamic stresses.

Contracts from Petrobras and the Brazilian Navy for fleet upgrades and platform maintenance continue to generate consistent demand for certified high-pressure static and rotary seals. Simultaneously, Brazil’s expanding port and coastal infrastructure for trade and logistics fuels the consumption of industrial-grade marine sealants in civil maritime construction.

As local manufacturing and supply chain capabilities grow, Brazil is also witnessing greater adoption of locally stocked sealing solutions to minimize downtime in marine MRO operations. The country’s ongoing investments in energy and infrastructure position it as Latin America’s primary growth engine for the marine sealants industry.

Marine Sealants Market Report Scope

Marine Sealants Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$410.1 Million

|

|

Market Size (2034)

|

$588.8 Million

|

|

Market Growth Rate

|

4.1%

|

|

Segments

|

By Product Type (Polyurethane Sealants, Silicone Sealants, Polysulfide Sealants, Hybrid MS Polymer Sealants, Butyl Sealants, Acrylic Sealants, Epoxy-based Sealants), By Application Area (Below Water-Line Sealing, Above Water-Line Sealing, Deck to Hull Joint Sealing, Window Bonding/Glazing, Electrical Housing Sealing, Engine Casing Sealing, Structural Bonding), By End-User Vessel Type (Commercial Shipbuilders, Recreational Boat Manufacturers, Defense & Naval Vessels, Fishing Vessels, High-Speed Craft, Offshore Oil & Gas Vessels), By Function (New Vessel Construction, Maintenance, Repair, & Overhaul, Custom Fabrication/Retrofit, Defense and Naval Applications), By Form (Single Component Sealants, Multi-Component Sealants, Solvent-Based Sealants, Water-Based Sealants, Low-VOC Formulations), By Substrate (Metal, Composite/Fiberglass, Wood, Plastic, Concrete

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Sika AG, Henkel AG & Company, KGaA, The 3M Company, Bostik S.A., H.B. Fuller Company, Dow, RPM International Inc., SABA, Illinois Tool Works, BASF SE, Wacker Chemie AG, Franklin International, Mapei S.p.A, Adshead Ratcliffe & Co Ltd., Soudal N.V.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Marine Sealants Market Segmentation

By Chemical Base/Product Type

- Polyurethane Sealants

- Silicone Sealants

- Polysulfide Sealants

- Hybrid MS Polymer Sealants

- Butyl Sealants

- Acrylic Sealants

- Epoxy-based Sealants

By Application Area

- Below Water-Line Sealing

- Above Water-Line Sealing

- Deck to Hull Joint Sealing

- Window Bonding/Glazing

- Electrical Housing Sealing

- Engine Casing Sealing

- Structural Bonding

By End-User Vessel Type

- Commercial Shipbuilders

- Recreational Boat Manufacturers

- Defense & Naval Vessels

- Fishing Vessels

- High-Speed Craft

- Offshore Oil & Gas Vessels

By Function

- New Vessel Construction

- Maintenance, Repair, & Overhaul

- Custom Fabrication/Retrofit

- Defense and Naval Applications

By Form/Technology

- Single Component Sealants

- Multi-Component Sealants

- Solvent-Based Sealants

- Water-Based Sealants

- Low-VOC Formulations

By Substrate

- Metal

- Composite/Fiberglass

- Wood

- Plastic

- Concrete

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Global Marine Sealants Market

- Sika AG

- Henkel AG & Company, KGaA

- The 3M Company

- Bostik S.A.

- H.B. Fuller Company

- Dow

- RPM International Inc.

- SABA

- Illinois Tool Works

- BASF SE

- Wacker Chemie AG

- Franklin International

- Mapei S.p.A

- Adshead Ratcliffe & Co Ltd.

- Soudal N.V.

*- List not Exhaustive

Research Coverage

Anchored in real-world shipyard practices and evolving compliance, USDAnalytics delivers an executive-ready deep dive into the Global Marine Sealants Market, where this report investigates how formulation advances and application engineering reshape watertight integrity, vibration control, and lifecycle cost. It maps certification pathways, supply-chain moves, and material science inflection points; consolidates performance data for polyurethane, silicone, polysulfide, hybrid MS polymer, and specialty systems; and benchmarks adoption across commercial, naval, offshore, and leisure fleets. The study curates breakthroughs in low-VOC/low-hazard chemistries, fire-rated assemblies, rapid-cure automation, and below-waterline durability; analysis reviews procurement patterns, regional capacity shifts, and retrofit economics; and highlights how sealant selection interacts with composite structures, glazing, and modular outfitting. Built for specifiers, technical buyers, and program managers, this report is an essential resource for translating standards and operating risks into optimal joint design, substrate compatibility, and project delivery outcomes.

Scope Highlights

Segmentation (covered in this study):

- By Chemical Base/Product Type: Polyurethane Sealants; Silicone Sealants; Polysulfide Sealants; Hybrid MS Polymer Sealants; Butyl Sealants; Acrylic Sealants; Epoxy-based Sealants

- By Application Area: Below Water-Line Sealing; Above Water-Line Sealing; Deck to Hull Joint Sealing; Window Bonding/Glazing; Electrical Housing Sealing; Engine Casing Sealing; Structural Bonding

- By End-User Vessel Type: Commercial Shipbuilders; Recreational Boat Manufacturers; Defense & Naval Vessels; Fishing Vessels; High-Speed Craft; Offshore Oil & Gas Vessels

- By Function: New Vessel Construction; Maintenance, Repair, & Overhaul; Custom Fabrication/Retrofit; Defense and Naval Applications

- By Form/Technology: Single Component Sealants; Multi-Component Sealants; Solvent-Based Sealants; Water-Based Sealants; Low-VOC Formulations

- By Substrate: Metal; Composite/Fiberglass; Wood; Plastic; Concrete

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Timeframe: Historic data 2021–2024 and forecasts 2025–2034.

Companies: Analysis/profiles of 15+ companies, including Sika AG; Henkel AG & Company, KGaA; The 3M Company; Bostik S.A.; H.B. Fuller Company; Dow; RPM International Inc.; SABA; Illinois Tool Works; BASF SE; Wacker Chemie AG; Franklin International; Mapei S.p.A; Adshead Ratcliffe & Co Ltd.; Soudal N.V.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.