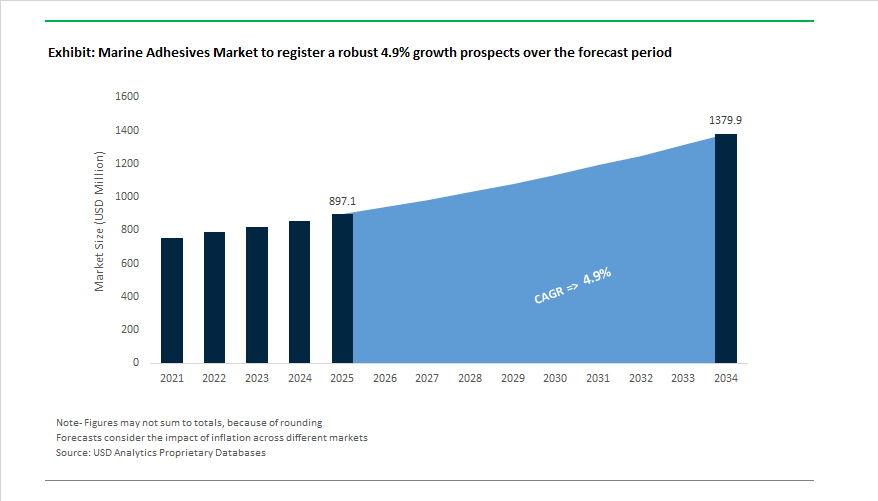

The Global Marine Adhesives Market is projected to expand from USD 897.1 million in 2025 to USD 1,379.8 million by 2034, growing at a CAGR of 4.9%, as marine construction and repair increasingly shift toward bonded, multi-material structures. Growth is not volume-led; it is driven by design complexity, maintenance economics, and compliance pressure across commercial shipbuilding, leisure craft, naval vessels, and offshore infrastructure. Adhesives have moved from auxiliary sealants to structural and semi-structural joining systems, directly influencing vessel durability, weight optimization, and lifecycle cost.

A defining market driver is the material transition underway in marine platforms. Shipyards and boatbuilders are steadily increasing the use of fiberglass, carbon-fiber composites, aluminum, and hybrid assemblies to reduce weight, improve fuel efficiency, and enhance corrosion resistance. This material mix has reduced the viability of traditional mechanical fastening, elevating the role of marine adhesives capable of bonding dissimilar substrates while absorbing vibration and accommodating hull flex. As a result, adhesives are now specified early in vessel design, particularly in hull-to-deck joints, superstructures, interiors, and offshore modules where fatigue resistance and long-term adhesion are mission-critical.

Regulatory and operational constraints are accelerating adoption of polyurethane, epoxy, and silane-modified polymer (SMP) marine adhesives. These chemistries are preferred for their balance of fast cure profiles, elasticity, and resistance to saltwater, UV exposure, and cyclic loading, while supporting compliance with DNV/GL classification requirements and ISO 9001:2015-certified manufacturing environments. At the same time, environmental and worker safety regulations are reshaping formulation strategies, driving demand for low-monomer and low-emission systems that reduce exposure risks during application in confined shipyard and onboard environments. Faster curing adhesives further reduce dry-dock and maintenance downtime, a critical economic lever for commercial fleets and offshore operators.

The marine adhesives industry is witnessing strategic expansions, technological innovations, and sustainability-oriented R&D breakthroughs that have reshaped global competition.

In August 2025, Sonoco Products Company invested USD 30 million to expand its adhesives and sealants production capacity, adding 100 million additional units annually. This expansion directly supports the rising industrial demand for marine-grade polyurethane and epoxy formulations, especially in coastal infrastructure maintenance and vessel refurbishment.

Governmental initiatives also played a pivotal role in driving market demand. In April 2025, the U.S. Fish and Wildlife Service allocated USD 21 million in Boating Infrastructure Grants across 21 states, funding over 187 new slips and nearly 7,800 feet of docking space. This large-scale infrastructure investment has directly stimulated consumption of marine MRO adhesives used for dock and harbor repair projects.

Product innovation continued to accelerate. In March 2025, a new solvent-free, isocyanate-free SMP sealant was introduced, offering primerless adhesion to metals and fiberglass while enhancing operator safety in professional boatyards. Meanwhile, in February 2025, a global chemical leader completed an acquisition of a specialty methacrylate adhesives manufacturer, integrating fast-cure bonding technologies that improve throughput for OEM marine assembly lines.

Sustainability remained a defining theme. In December 2024, a leading resin manufacturer unveiled a bio-based epoxy system for composite lamination, maintaining full DNV/GL type approval while increasing renewable raw material content. This innovation positions bio-based adhesives as a realistic alternative for eco-friendly yacht and ferry construction.

Regional expansions reinforced the sector’s globalization trend. By September 2024, a major sealants producer expanded its Asia-Pacific R&D center, focusing on polyurethane and MS-polymer adhesives to meet growing regional demand from commercial shipbuilding hubs in China, Japan, and South Korea. Additionally, in October 2024, a European marine coatings company partnered with an adhesive manufacturer to develop coating-compatible adhesive systems, addressing long-standing challenges in adhesion failures between primers, adhesives, and antifouling coatings.

Market Trend 1: Regulatory-Driven Transition to Low-VOC and Non-Tin Antifouling Adhesive Systems

A major transformation in the marine adhesives industry is being propelled by global environmental compliance, particularly through the enforcement of the IMO’s International Convention on the Control of Harmful Anti-fouling Systems on Ships (AFS Convention). The prohibition of organotin compounds such as tributyltin (TBT) and, more recently, the ban on cybutryne from January 2023, have accelerated the demand for non-tin antifouling coatings and cybutryne-free adhesive systems. These mandates are reshaping the formulation landscape, compelling manufacturers to innovate sustainable marine materials that align with marine environmental compliance standards.

R&D investment in low-VOC adhesives and isocyanate-free sealants has surged as leading chemical manufacturers pivot toward Silane Terminated Polymer (STP) technology. STPs are becoming a preferred choice in shipbuilding and repair due to their enhanced flexibility, safety, and environmental performance. These formulations eliminate harmful components like organo-tin and phthalates, aligning with sustainability mandates while ensuring strong adhesion even in challenging marine conditions.

In addition, the reformulation of underwater-curing epoxy systems is driving the introduction of high-performance adhesives capable of maintaining durability against hydrolysis, cohesive failure, and saltwater degradation. The convergence of regulatory compliance and material innovation is not only ensuring safety but also opening commercial pathways for eco-friendly marine adhesives optimized for next-generation vessel maintenance and coating applications.

Market Trend 2: Rising Adoption of Structural Adhesives for Composite-to-Metal and Composite-to-Composite Bonding

The structural adhesive segment of the marine adhesives market is witnessing exponential growth due to the increasing integration of carbon fiber and fiberglass composites in ship hulls, decks, and superstructures. The ongoing shift from traditional joining techniques—like welding and riveting—to structural bonding is a defining technological leap for the shipbuilding industry. Structural adhesives, especially methacrylate adhesives (MMA), are offering unmatched benefits such as superior fatigue resistance, even stress distribution, and lightweight assembly, which collectively enhance vessel structural integrity and fuel efficiency.

In multi-material shipbuilding—combining steel, composites, and aluminum—adhesive bonding mitigates galvanic corrosion risks and reduces the need for heavy fasteners, improving hydrodynamics and lowering the vessel’s carbon footprint. The global emphasis on green marine technology and lightweight vessel construction directly supports the trend, as regulatory and operational pressure mounts to reduce greenhouse gas (GHG) emissions from the maritime sector.

Technical data from composite manufacturing and performance testing further drives the reliability of these adhesives in high-stress marine applications such as deck-to-hull joints, stringer bonding, and bulkhead assembly. The shift toward high-strength structural adhesives signals a long-term movement toward performance-optimized, sustainable shipbuilding practices that balance environmental responsibility with engineering excellence.

Market Opportunity 1: Expanding Role in Offshore Wind Farm Installation and Maintenance Fleet

The global expansion of offshore wind infrastructure represents one of the most lucrative opportunities for the marine adhesives market. The growing number of installation and crew transfer vessels (CTVs), along with the complex substructures used in floating offshore wind farms, are driving demand for high-durability marine sealants and vibration-dampening adhesives.

In the United States, over $17 billion has been invested in offshore wind development since 2014, with approximately $1 billion directed toward ports and specialized vessels in 2022 alone. The investment directly translates into sustained demand for marine-grade bonding and sealing materials that can withstand prolonged exposure to dynamic mechanical loads and corrosive marine environments.

Similarly, the United Kingdom’s ambitious goal to achieve 50 GW of offshore wind capacity by 2030, including 5 GW of floating wind, drives a robust opportunity for adhesive suppliers. Specialized high-performance structural epoxies and deep-water bonding solutions are increasingly vital for floating substructures, turbines, and mooring assemblies exposed to extreme marine stressors. As governments and private players continue investing in renewable offshore energy, adhesive manufacturers that tailor products for offshore O&M applications stand to capture a significant share of the fast-evolving energy supply chain.

Market Opportunity 2: Innovation Potential in Rapid-Cure, Underwater Repair and Maintenance Systems

The emergence of rapid-cure, underwater bonding technologies marks another transformative opportunity for the marine adhesives industry. The cost and logistical challenges of dry-docking large vessels are pushing operators toward in-situ repair solutions that can be applied directly in submerged conditions. The demand has spurred advancements in underwater-curing epoxy formulations, incorporating phenolic and Mannich base curing agents capable of achieving underwater bonding strengths up to 5.9 MPa on metal substrates—an unprecedented benchmark for subsea applications.

Military research and defense-backed innovation have played a pivotal role in accelerating these developments. The U.S. Army Research Laboratory, in partnership with industrial partners, has developed acrylate-modified, fast-curing epoxy adhesives designed specifically for use in adverse marine conditions. These systems offer rapid strength gain, enabling emergency marine repair, submerged component bonding, and vessel integrity restoration without compromising cure performance.

As commercial maritime operators increasingly prioritize uptime and operational efficiency, demand for high-bonding, fast-curing underwater adhesives is expected to surge across both commercial and defense fleets. The growing focus on vessel downtime reduction and maintenance automation opens new commercial horizons for adhesive innovators positioned at the intersection of marine engineering and polymer science.

Marine Adhesives Market Share Insights, 2025-2034

Market Share by Component

The two-component marine adhesive systems dominate the global marine adhesives market, holding a projected 62.6% share in 2025, due to their superior strength, chemical resistance, and long-term durability in harsh marine environments. These systems—typically based on epoxy, polyurethane, and methacrylate chemistries—offer exceptional resistance to saltwater immersion, UV radiation, and mechanical fatigue, making them indispensable in boat hull bonding, structural assemblies, and underwater sealing applications. Their precise mixing ratios and high crosslink density yield strong mechanical properties that ensure structural integrity under cyclic loads and extreme temperatures. Two-component systems are the adhesive technology of choice for shipbuilding, offshore platforms, and high-performance yachts, where failure resistance and long service life are critical. With the maritime industry’s focus on lightweight composite materials and green shipbuilding technologies, two-component formulations are being tailored for composite-to-metal and composite-to-composite bonding, supporting improved fuel efficiency and corrosion prevention.

One-component marine adhesives maintain a steady share, valued for their ease of application, rapid curing, and flexibility in on-site repairs and general maintenance. These adhesives are favored in recreational boats, deck fittings, and interior bonding, where time efficiency and versatility outweigh structural performance requirements. Their user-friendly handling and low equipment dependency make them indispensable for small-scale operations and maintenance, repair, and overhaul (MRO) markets. The component segmentation underscores the industry’s prioritization of high-performance, reliability-driven adhesive systems, with two-component solutions dominating structural and high-load applications, while one-component systems cater to fast, convenient, and cost-effective repairs across the global marine ecosystem.

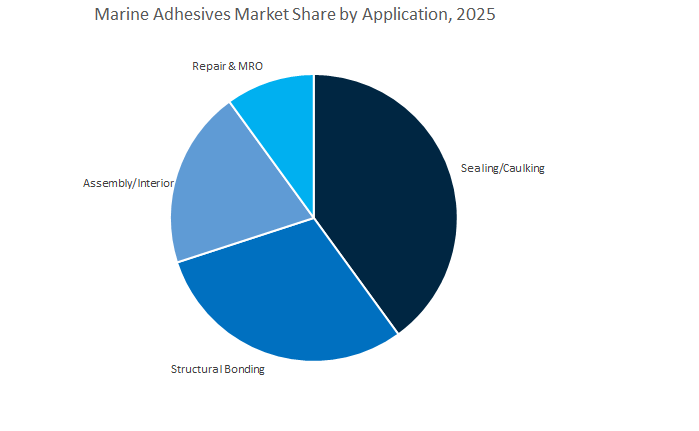

Market Share by Application

The sealing and caulking segment leads the global marine adhesives market, representing a projected 42.3% share in 2025, driven by the essential role of adhesives in waterproofing, sealing, and joint integrity across vessels and marine structures. These applications include hull-deck joints, through-hull fittings, portholes, and deck seams, where constant exposure to saltwater, vibration, and temperature cycling demands adhesives with superior elasticity, chemical resistance, and UV durability. Modern polyurethane and silicone-based sealants provide long-term flexibility and non-shrink curing, enabling maintenance of watertight integrity even under mechanical stress. Growth is further supported by the global expansion of ship repair, refit, and recreational boating industries, which increasingly rely on low-VOC, marine-grade elastomeric sealants for compliance and performance.

The structural bonding segment maintains a strong position, as adhesives replace traditional welding and mechanical fastening in modern boatbuilding and offshore construction. Their advantages—weight reduction, corrosion prevention, improved aesthetics, and vibration damping—are crucial in composite hulls, deck assemblies, and cabin structures. Advanced methacrylate and epoxy systems are enabling multi-material bonding, enhancing both design freedom and fuel efficiency. The assembly and interior applications segment includes bonding of fixtures, insulation panels, cabinetry, and decorative components, where appearance, acoustic performance, and ease of processing drive adoption. Meanwhile, the repair and maintenance (MRO) segment represents a consistent revenue stream. Demand is steady from shipyards, naval facilities, and small vessel operators, emphasizing rapid-curing, multipurpose adhesives for emergency sealing and structural reinforcement.

The Global Marine Adhesives Industry is highly specialized, with major players such as 3M, Sika, Hexion, Henkel, and H.B. Fuller dominating global supply chains. Their focus lies in developing multi-chemistry adhesive platforms—combining polyurethane, epoxy, methacrylate, and SMP technologies—to address the unique challenges of marine structure durability, regulatory compliance, and fast installation cycles.

3M’s Adhesives, Sealants & Fillers Division remains the industry standard with its 3M™ Marine Adhesive Sealant 5200, a high-strength, moisture-curing polyurethane known for permanent below-waterline bonding. To enhance operational efficiency, 3M introduced the Fast Cure 5200 variant, reducing curing times from days to less than 48 hours, a major advantage in marine repair. The company also expanded its SMP portfolio with 3M™ Marine Adhesive Sealant 4000 UV, offering UV resistance and easy disassembly.

Operating the world’s largest Weathering Research Center (WRC), 3M validates long-term UV, salt spray, and submersion performance, reinforcing its position as a leader in marine durability testing and formulation science.

Sika AG leads in elastic bonding and vibration damping for marine OEMs through its Sikaflex® line of polyurethane sealants. Its Purform® low-monomer technology sets the compliance benchmark under EU REACH standards, eliminating user safety training requirements.

Beyond adhesives, Sika’s marine product ecosystem includes SikaDamp acoustic systems and Sikafloor Marine, creating a comprehensive bonding and flooring portfolio for ferries, yachts, and naval vessels. With SikaForce® and SikaFast® methacrylate adhesives, the company addresses structural bonding of hulls, decks, and composite bulkheads, providing high fatigue resistance for long service life.

Hexion, part of Westlake Corporation, supplies its renowned EPIKOTE™ Resin MGS™ epoxy systems used extensively in marine composite manufacturing, including infusion and lamination processes. Its portfolio delivers tailored pot life options (10–600 minutes) and DNV/GL-certified structural performance.

Hexion’s EPIKOTE BP 20 bonding paste provides ambient-cure field repair solutions for unprepared composite surfaces, addressing a major challenge in marine maintenance. Its dual-system architecture—EPIKOTE resins and EPIKURE curing agents—enables full control over viscosity and cure speed, optimizing both OEM production and MRO repair efficiency.

Henkel’s Adhesive Technologies Division, leveraging its Loctite brand, delivers a global range of epoxies, polyurethanes, and hybrid polymer adhesives for marine and offshore use. The company is heavily investing in automation-ready dispensing solutions for high-volume shipyards, improving process reliability and productivity. Henkel’s hybrid polymer technologies merge polyurethane elasticity with SMP fast-curing performance, ensuring long-lasting bonds across mixed substrates like metal, GRP, and thermoplastics. Its marine product line supports both OEM assembly and elastic sealing applications, emphasizing vibration tolerance and long-term elasticity.

H.B. Fuller specializes in methyl methacrylate (MMA) and two-part epoxy adhesives that deliver exceptional fatigue and chemical resistance for high-speed and heavy-duty vessels. These formulations are engineered for bonding metal-to-GRP and composite-to-metal joints in structural marine applications. The company’s strategic priority is low-VOC, high-solids formulations aligned with green shipbuilding standards. With its global supply chain and technical centers in North America, Europe, and APAC, H.B. Fuller provides end-to-end engineering adhesive support to commercial shipyards and naval contractors worldwide.

Country Analysis: Global Marine Adhesives Industry Hubs

India: Rising Domestic Shipbuilding and Green Maritime Initiatives Boost Marine Adhesive Demand

India has emerged as one of the fastest-growing shipbuilding markets in Asia, driven by substantial public and private sector investments. The Indian government’s ₹69,725 crore maritime modernization package (announced in September 2025) includes the Shipbuilding Financial Assistance Scheme (SBFAS) and a ₹25,000 crore Maritime Development Fund (MDF) to strengthen financial capacity and expand vessel production capabilities. The initiatives are directly fueling demand for marine-grade structural adhesives, sealants, and composite bonding materials across new construction and repair operations.

Public sector undertakings (PSUs) in oil and gas are set to commission over 110 vessels over the next decade, creating consistent domestic demand for epoxy and polyurethane adhesives tailored for offshore and onshore applications. Simultaneously, Cochin Shipyard’s development of India’s first hydrogen-fuel-powered ferry (2024) signals a national push toward green shipping, spurring R&D into eco-friendly, low-VOC, and high-temperature-resistant marine sealants compatible with alternative energy propulsion systems.

The Atmanirbhar Bharat (Self-Reliant India) initiative continues to stimulate indigenous defense shipbuilding projects, including high-strength adhesive applications in aircraft carriers such as INS Vikrant. As India’s shipyards scale up, supported by new infrastructure like the proposed ₹15,000 crore Tamil Nadu shipbuilding complex, the nation is poised to become a strategic manufacturing hub for advanced marine bonding technologies in Asia-Pacific.

United States: High-Value MRO, Offshore Energy, and Defense Spending Drive Adhesive Innovation

The U.S. marine adhesives market is characterized by its focus on high-performance materials, sustainability, and defense-grade formulations. The country’s leading players—including 3M, H.B. Fuller, Dow Inc., and Sika Group—continue to pioneer solvent-free epoxy and polyurethane systems that meet ASTM and military-grade (MIL) specifications for naval and industrial applications.

The 2025 acquisition of HPS North America by Sika Group strengthened its foothold in marine and infrastructure adhesives, while U.S. firms are also innovating in UV-resistant silicone sealants and non-yellowing deck caulking materials for the luxury yacht and recreational boating markets. The growing offshore wind energy sector further contributes to market diversification, with specialized underwater adhesives and subsea bonding systems being engineered for turbine anchoring and maintenance.

Meanwhile, ongoing U.S. Department of Defense (DoD) programs sustain long-term demand for high-strength polyurethane and thermally stable epoxy adhesives in naval shipbuilding and retrofitting. As sustainable manufacturing takes priority, manufacturers are also expanding production of low-emission, bio-based adhesives to comply with EPA environmental standards—cementing the U.S. as a leader in premium marine adhesive innovation and performance materials.

China: Global Shipbuilding Dominance and Technological Localization Define Market Growth

China continues to dominate the global marine adhesives industry, driven by its unrivaled shipbuilding capacity and rapid advancements in high-durability composite materials. The 2025 expansion of Sika’s manufacturing operations in Xi’an and Suzhou underscores the localization of adhesive production to serve booming marine, construction, and industrial segments. As a result, China’s adhesive supply chain has become increasingly self-reliant and integrated with its vast shipbuilding ecosystem.

In addition, Arxada’s Omadine® antifouling technology, presented at ChinaCoat 2024, is setting a new standard in marine coating and adhesive performance, particularly for corrosion resistance and microbial protection in harsh marine environments. National Green Development policies and stricter VOC emission controls are compelling domestic producers to transition toward waterborne, solventless, and low-VOC polyurethane systems.

China’s major shipyards—producing both commercial and defense-grade vessels—are scaling their use of marine-grade epoxies and MS polymer adhesives for deck bonding, hull lamination, and composite reinforcement. Combined with the government’s focus on renewable energy and offshore wind construction, the country’s adhesive market is evolving rapidly into a technology-intensive, globally competitive sector.

Germany: Sustainable Innovation and R&D Excellence in Marine Bonding Technologies

Germany remains at the forefront of marine adhesive R&D and sustainability-driven formulation development. The country’s chemical sector, led by Henkel, BASF, and Covestro, is pioneering low-carbon, solvent-free adhesive technologies in compliance with EU REACH and Green Deal regulations. Henkel’s 2024 partnership with Celanese to develop adhesives derived from captured CO₂ feedstocks exemplifies the country’s drive to integrate carbon-neutral materials into marine applications.

The German market’s emphasis on bio-based, low-VOC, and recyclable bonding solutions aligns with Europe’s increasing maritime decarbonization goals. In addition, German R&D centers are exploring self-healing epoxy networks and advanced MS polymer sealants, engineered to withstand prolonged exposure to saltwater, temperature fluctuations, and mechanical stress.

Germany’s expertise extends into composite-intensive boat manufacturing, where flexible polyurethane and acrylic hybrid adhesives are used for vibration damping, acoustic insulation, and long-term bonding reliability. As the EU mandates stricter emissions and circularity standards, Germany’s marine adhesive sector continues to lead Europe in green chemistry and high-performance materials innovation.

South Korea and Japan: Asia-Pacific Leaders in Shipbuilding and Composite Integration

South Korea and Japan dominate global shipbuilding output, accounting for over 50% of large commercial vessel construction, including LNG carriers and ultra-large container ships. The leadership translates into consistent demand for structural epoxy, polyurethane, and acrylic marine adhesives that deliver superior mechanical strength and long-term seawater resistance.

Shipyards such as Hyundai Heavy Industries, Samsung Heavy Industries, and Mitsubishi Heavy Industries are increasingly utilizing advanced fire-retardant and low-outgassing adhesives for high-capacity maritime vessels and next-generation LNG fuel systems. The integration of lightweight composite materials and FRP (fiber-reinforced polymer) components in ship hulls and superstructures further drives the need for high-tensile, flexible marine bonding systems.

Strategic acquisitions by Sika Group—such as the 2010 acquisition of Henkel Japan Ltd.’s Construction Sealant Business and subsequent investments in South Korea—underline the localization of specialty adhesive manufacturing across Northeast Asia.

Singapore: Maritime Infrastructure Hub for Asia-Pacific Repair and Maintenance

Singapore’s role as a global maritime and logistics hub makes it a pivotal market for marine infrastructure adhesives and repair sealants. With over 130,000 vessel calls annually, the city-state’s ship repair and maintenance sector drives high-volume demand for industrial polyurethane, epoxy, and silicone adhesives used in structural reinforcement, coating repair, and dock sealing applications.

In early 2025, Sika Group expanded its Asia-Pacific footprint by opening a new production plant in Singapore and acquiring Elmich Pte Ltd, reinforcing its supply capabilities across Southeast Asia’s marine construction ecosystem. The country’s maritime modernization efforts, combined with its commitment to green port development, are stimulating adoption of eco-friendly, rapid-curing adhesives designed for underwater and coastal applications.

With its advanced logistics infrastructure and strategic location, Singapore stands as a key regional hub for high-performance marine adhesives, serving both vessel maintenance and large-scale port infrastructure projects across the Indian Ocean and Southeast Asia.

Marine Adhesives Market Report Scope

Marine Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$897.1 Million

|

|

Market Size (2034)

|

$1379.8 Million

|

|

Market Growth Rate

|

4.9%

|

|

Segments

|

By Resin Type (Epoxy Adhesives, Polyurethane Adhesives, Silicone Adhesives, Acrylic Adhesives, Others), By Component (One-Component, Two-Component), By Substrate (Composites, Metals, Plastics, Wood), By Application (Structural Bonding, Sealing/Caulking, Assembly/Interior, Repair & MRO), By End-Use Vessel (Commercial Vessels, Passenger Vessels, Recreational Vessels, Naval/Defense

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

3M Company, Henkel AG & Co. KGaA, Sika AG, H.B. Fuller Company, Arkema Group, Huntsman Corporation, Dow Inc., Ashland Global Holdings Inc., Scott Bader Company Ltd, Gurit Holding AG, LORD Corporation, Master Bond Inc., ITW Performance Polymers, Permabond LLC, DELO Industrial Adhesives

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Marine Adhesives Market Segmentation

By Resin/Chemical Type

- Epoxy Adhesives

- Polyurethane Adhesives

- Silicone Adhesives

- Acrylic Adhesives

- Others

By Component

- One-Component

- Two-Component

By Substrate

- Composites

- Metals

- Plastics

- Wood

By Application

- Structural Bonding

- Sealing/Caulking

- Assembly/Interior

- Repair & MRO

By End-Use Vessel

- Commercial Vessels

- Passenger Vessels

- Recreational Vessels

- Naval/Defense

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Global Marine Adhesives Market

- 3M Company

- Henkel AG & Co. KGaA

- Sika AG

- H.B. Fuller Company

- Arkema Group

- Huntsman Corporation

- Dow Inc.

- Ashland Global Holdings Inc.

- Scott Bader Company Ltd

- Gurit Holding AG

- LORD Corporation

- Master Bond Inc.

- ITW Performance Polymers

- Permabond LLC

- DELO Industrial Adhesives

*- List not Exhaustive

Research Coverage

USDAnalytics presents a practitioner-grade assessment of the Global Marine Adhesives Market, where this report investigates how epoxy, polyurethane, silicone, acrylic, SMP and hybrid systems are redefining structural bonding, sealing, and corrosion protection in shipbuilding, offshore platforms, and marine MRO. It maps certification pathways (e.g., DNV/GL type approvals), low-monomer innovations, and greener chemistries alongside throughput gains in composite-to-metal joining; catalogs regulatory and OEM specification shifts that elevate fatigue resistance, osmosis control, and vibration damping; and consolidates multi-region demand signals from commercial, defense, and recreational fleets. The study distills breakthroughs in fast-cure, primerless adhesion and underwater repair epoxies; analysis reviews technology roadmaps, investment moves, and supply-chain localization; and highlights adoption patterns tied to lightweighting, dock modernization, and offshore wind logistics. Built for specification writers, yard engineers, and sourcing leaders, this report is an essential resource for translating standards, safety rules, and lifecycle economics into adhesive selection, application design, and tender compliance.

Scope Highlights

Segmentation (covered in this study):

- By Resin/Chemical Type: Epoxy Adhesives; Polyurethane Adhesives; Silicone Adhesives; Acrylic Adhesives; Others

- By Component: One-Component; Two-Component

- By Substrate: Composites; Metals; Plastics; Wood

- By Application: Structural Bonding; Sealing/Caulking; Assembly/Interior; Repair & MRO

- By End-Use Vessel: Commercial Vessels; Passenger Vessels; Recreational Vessels; Naval/Defense

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Timeframe: Historic data 2021–2024 and forecasts 2025–2034.

Companies: Analysis/profiles of 15+ companies (from 3M Company; Henkel AG & Co. KGaA; Sika AG; H.B. Fuller Company; Arkema Group; Huntsman Corporation; Dow Inc.; Ashland Global Holdings Inc.; Scott Bader Company Ltd; Gurit Holding AG; LORD Corporation; Master Bond Inc.; ITW Performance Polymers; Permabond LLC; DELO Industrial Adhesives).

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.