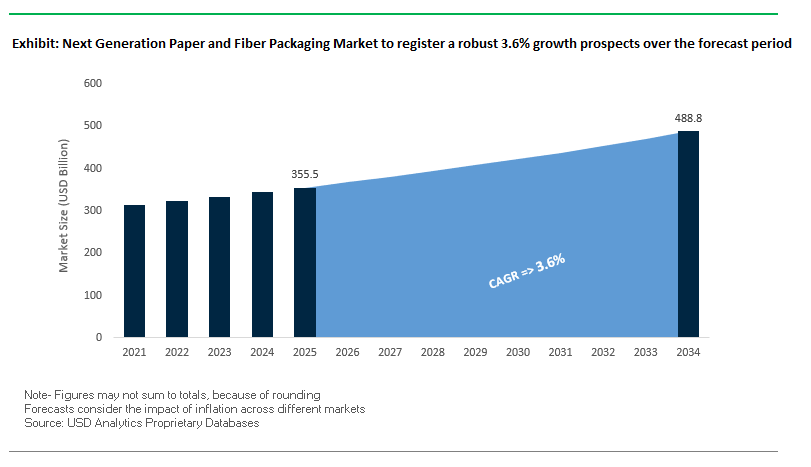

Next Generation Paper and Fiber Packaging Market to Reach $488.7 Billion by 2034 at 3.6% CAGR

The global next-generation paper and fiber packaging market is projected to grow from $355.5 billion in 2025 to $488.7 billion by 2034, recording a CAGR of 3.6%. This growth is driven by the shift from fossil-based plastics to bio-based, renewable materials, technological advancements in barrier coatings, and the rapid adoption of recycled fibers across industries. Packaging companies are increasingly investing in sustainable, recyclable, and high-performance paper solutions, meeting the demands of food, beverage, e-commerce, and hygiene sectors while aligning with regulatory and consumer sustainability goals.

Key Insights for Industry Professionals:

- Transition to bio-based materials: Increased use of non-wood fibers like sugarcane, hemp, and flax is reducing reliance on fossil-based plastics.

- Enhanced barrier performance: Innovations in coatings and material formulations allow paper packaging to rival plastic in oxygen, moisture, and grease resistance.

- Recycled fiber adoption: Over 53% of the market in 2024 utilizes recycled fibers, reflecting the emphasis on the circular economy.

- Digital integration – Internet of Packaging: QR codes, RFID, and NFC tags in paper packaging drive supply chain transparency and consumer engagement, with the global IoP market projected at $54.43 billion by 2034.

- Cross-industry relevance: Applications include food and beverage packaging, oral care, pet food, and e-commerce, providing opportunities for lightweight, durable, and sustainable solutions.

Market Analysis: Recent Developments Shaping the Global Next-Generation Paper and Fiber Packaging Industry

The next-generation paper and fiber packaging market has experienced significant advancements through material innovations, strategic partnerships, and sustainability initiatives. In September 2025, Siegwerk showcased circular packaging innovations at the 12th Specialty Films and Flexible Packaging Global Business Summit, highlighting its expanded coating capabilities after acquiring Allinova. In the same month, Nfinite Nanotechnology partnered with Amcor to enhance recyclable and compostable packaging via nanocoatings, improving oxygen barrier performance.

In August 2025, Mondi ramped up production of its FunctionalBarrier Paper Ultimate, an ultra-high barrier paper-based solution protecting against oxygen, water vapor, and grease, marking a significant step toward replacing multi-layer plastics. Simultaneously, Graphic Packaging International launched its PaperSeal® Pressed MAP Tray, reducing plastic usage by 85% in MAP applications. In July 2025, the Smurfit WestRock merger was completed, creating a global paper packaging leader positioned to drive growth in the next-generation paper and fiber packaging market.

Other notable initiatives include Graphic Packaging and Unilever’s collaboration in July 2025 on sustainable oral care packaging, Mondi and Saga Nutrition’s monomaterial pet food solution in June 2025, and Mondi’s €400 million paper machine startup in May 2025, reinforcing the company’s leadership in sustainable packaging. Meanwhile, C&J Industries expanded its plastics facility in April 2025, reflecting ongoing competition from plastic alternatives.

Trends and Opportunities Shaping the Next Generation Paper and Fiber Packaging Market

Strategic Corporate Investment in Advanced Fiber Molding Technology

The global shift toward sustainable packaging is accelerating corporate investments in advanced fiber molding technologies. In late 2026, a major consumer goods company will inaugurate a $150 million facility in the Midwestern United States dedicated to producing high-precision molded pulp packaging for food and beverages. This new plant will deploy high-speed thermoforming systems to produce smooth-walled, premium containers designed to replace rigid plastic packaging. Beyond scaling volume, the focus is on quality—cosmetic and electronics packaging is evolving with advanced fiber engineered for both durability and aesthetics. A key innovation is the integration of high-resolution digital printing on molded fiber surfaces, creating branded, visually appealing, and sustainable alternatives. Furthermore, the rapid rise of e-commerce is boosting demand for molded pulp inserts and cushioning solutions to protect fragile goods such as electronics, glassware, and personal care products during last-mile delivery. This makes fiber packaging a high-growth segment positioned at the intersection of sustainability, performance, and digital retail expansion.

Government Policy Catalyzing Demand for Recyclable and Compostable Fiber Solutions

Global regulatory frameworks are exerting strong influence on packaging transitions, with the European Union’s Packaging and Packaging Waste Regulation (PPWR), effective from early 2025, leading the charge. This regulation mandates that all packaging be recyclable in an economically viable manner by 2030, effectively phasing out complex, non-recyclable composites. A critical element of the legislation is its ban on PFAS in food-contact packaging, effective August 2026, pushing the market toward natural barrier fiber solutions. National-level interventions further amplify this momentum—France implemented a ban on plastic packaging for fresh produce and a tax on non-recycled plastics in January 2025, incentivizing fiber-based alternatives. These policies are not isolated; they reflect a broader global shift where government action aligns with brand-owner sustainability commitments, accelerating fiber packaging adoption across industries such as food, retail, and pharmaceuticals.

Development and Licensing of High-Barrier, PFAS-Free Coatings

One of the most lucrative opportunities lies in developing and commercializing PFAS-free coatings that maintain barrier integrity against oil, grease, and liquids while remaining recyclable. Material science companies are racing to innovate starch- and bio-based alternatives that can match or surpass fluorochemical performance without contaminating recycling streams. A growing number of multinational foodservice chains, including Starbucks and McDonald’s, have pledged to eliminate PFAS from their packaging portfolios, influencing procurement decisions worth more than $500 billion annually. This rising demand represents a dual advantage—compliance with tightening regulations and alignment with circular economy principles. PFAS-free solutions enhance fiber recovery rates, reduce reliance on virgin pulp, and improve brand sustainability narratives, making this innovation space a pivotal driver of next-generation paper and fiber packaging.

Scaling of Mycelium and Agricultural Waste Feedstocks

The growing convergence of biotechnology and packaging offers another breakthrough opportunity: the scaling of mycelium-based and agricultural waste feedstocks. Research initiatives, such as those at IIT Madras, have demonstrated that mycelium grown on paper and crop residues can achieve compressive strengths up to ten times higher than expanded polystyrene (EPS). With India generating more than 350 million tons of agricultural waste annually, this innovation turns a disposal challenge into a high-value packaging solution. The sustainability advantage is amplified by its premium branding potential—upcycling farm waste into durable, compostable packaging resonates strongly with eco-conscious consumers. For industries like electronics, cosmetics, and premium beverages, these materials combine functionality with a compelling environmental story, offering companies a unique competitive edge in an era where consumer loyalty is deeply tied to sustainability.

Competitive Landscape of Global Next-Generation Paper and Fiber Packaging Market

The next-generation paper and fiber packaging market is characterized by intense competition, with leading players leveraging bio-based materials, high-barrier technologies, and sustainable solutions to meet the demands of food, beverage, hygiene, and e-commerce sectors. Companies focus on recycled and renewable fibers, monomaterial innovations, and digital integration, offering lightweight, recyclable, and consumer-friendly packaging solutions.

Mondi Group: Pioneering High-Barrier and Sustainable Paper Solutions

Mondi is a global leader in sustainable paper and packaging, with its FunctionalBarrier Paper range offering superior protection against oxygen, moisture, and grease. In August 2025, the company expanded production of FunctionalBarrier Paper Ultimate, a high-barrier paper-based alternative to multi-layer plastics. In September 2025, Mondi launched a patented mono-material pouch for liquid detergents, highlighting its commitment to recyclability and sustainability. Strategic investments, such as the €400 million paper machine at Štětí mill in May 2025, reinforce Mondi’s leadership in high-performance, next-generation paper packaging.

Smurfit Westrock: Leading Global Paper Packaging Post-Merger

Smurfit Westrock, formed from the merger of Smurfit Kappa and WestRock, is a global leader in paper-based packaging, offering a comprehensive portfolio of corrugated and containerboard solutions. The July 2025 stock exchange debut marked the creation of a stronger global player in next-generation paper and fiber packaging. The company focuses on sustainable materials, utilizing recycled and renewable fibers to reduce its environmental footprint, while providing lightweight, durable, and recyclable solutions across e-commerce, food and beverage, and industrial applications.

Graphic Packaging International: Driving Sustainability with Innovative Paperboard Solutions

Graphic Packaging International is a leading fiber-based consumer packaging provider. In August 2025, the company introduced the PaperSeal® Pressed MAP Tray, reducing plastic use by up to 85% in MAP applications. Additionally, its July 2025 collaboration with Unilever produced sustainable paperboard packaging for oral care. Its product innovations, including Boardio™ rigid paperboard canisters and KeelClip™ paperboard clips, reflect the company’s commitment to recyclable, next-generation packaging and plastic waste reduction.

DS Smith plc: Championing Circular Design Principles in Paper Packaging

DS Smith provides sustainable corrugated and paper packaging solutions with a focus on circular economy principles. The April 2024 agreement with International Paper aims to create a global leader in sustainable packaging. DS Smith’s Circular Design Principles and metrics guide customers to reduce waste, extend material life, and replace problematic plastics, aligning with environmental sustainability and low-carbon objectives.

Paptic Ltd.: Innovating Wood Fiber-Based Alternatives to Plastics

Paptic Ltd., a Finnish innovator, produces sustainable packaging materials from wood fibers, offering a bio-based alternative to plastics. In September 2025, Paptic received the ScanStar Award for hygiene packaging innovation and expanded into the hygiene and feminine care sector. With a EUR 27.5 million financing round, the company is scaling production and partnering with global brands to replace plastics in applications like carrier bags, fruit and vegetable packaging, and candy bags, emphasizing sustainability, recyclability, and circular material use.

Next Generation Paper and Fiber Packaging Market Share Insights

Barrier Coatings Dominate Market Share by Technology in the Next Generation Paper and Fiber Packaging Industry

Barrier coatings hold the dominant 40% share in 2025, acting as the technological backbone of next generation paper and fiber packaging. Their role is critical in enabling paper-based substrates to replace plastic by offering resistance to grease, moisture, oxygen, and oils, thereby making them viable for direct food contact applications like quick-service restaurant wraps, frozen foods, and beverage cartons. The rise of PLA- and PHA-based biopolymer coatings underpins their adoption, aligning with global legislation on single-use plastics. Molding and forming technologies capture 25% share, driven by pulp and molded fiber solutions replacing EPS foam in protective e-commerce packaging, electronics cushioning, and cosmetic trays. Digital printing, with a 15% share, is growing rapidly due to the e-commerce boom and rising demand for short-run, high-resolution, and customizable graphics that enhance consumer engagement and brand identity. Lamination remains relevant at 12%, though it is evolving towards paper-to-paper lamination and recyclable mono-material structures that retain strength without compromising recyclability. The “others” category, at 8%, includes innovations such as 3D-printed fiber prototypes and NFC-integrated paper substrates, which are steadily expanding niche opportunities in luxury and smart packaging.

Food & Beverage Leads Market Share by End-Use Industry in the Next Generation Paper and Fiber Packaging Industry

Food and beverages account for 40% of global demand, making it the largest end-use segment for next generation paper and fiber packaging. The sector’s leadership stems from its urgent push to replace multi-layer plastics with compostable and recyclable fiber-based alternatives in packaging formats ranging from quick-service restaurant wraps and grease-resistant bakery boxes to water-resistant beverage cartons and paper bottles. E-commerce and logistics hold a substantial 25% share, fueled by the replacement of plastic void fill and mailers with molded fiber, recyclable tapes, and branded corrugated shippers that align with both sustainability targets and consumer expectations for plastic-free deliveries. Electronics and electricals, with 15% share, are increasingly turning to molded fiber trays and anti-static paper solutions to reduce reliance on foams while aligning with corporate ESG commitments. Cosmetics and personal care packaging contributes 10%, leveraging premium finishes and advanced fiber designs to balance luxury aesthetics with sustainability claims. Pharmaceuticals and healthcare, with an 8% share, cautiously adopt fiber-based secondary packaging for blister backings and medical device cartons under strict compliance frameworks. The remaining 2% of applications fall within automotive, industrial, and luxury sectors, where fiber-based solutions are being piloted as sustainable alternatives in protective transit and brand-focused secondary packaging.

United States: Innovation Driven by Regulations and Corporate Investments in Next Generation Paper and Fiber Packaging

The United States is emerging as a pivotal market for next generation paper and fiber packaging, with regulatory mandates and corporate initiatives shaping the industry’s trajectory. State-level Extended Producer Responsibility (EPR) laws, spearheaded by California’s SB 54, along with PFAS-free mandates across several states, are forcing manufacturers to accelerate the shift toward safer, recyclable, and compostable alternatives. These legal frameworks are creating a fertile environment for innovation, particularly in the food service and e-commerce industries where the demand for eco-friendly packaging is rapidly growing.

Technological innovation is also reshaping the U.S. market, with manufacturers developing advanced barrier coatings that use clay- or plant-based solutions to replace fluorinated chemistries. Ahlstrom’s 2024 launch of LamiBak™ base paper for flexible food packaging exemplifies this shift toward functional yet sustainable products. Investments are further fueling this momentum, such as Sappi’s $500 million machine conversion in Maine and the U.S. Department of Energy’s $52 million funding for cellulose-based films. Together, these efforts position the U.S. as a frontrunner in scaling sustainable paper and fiber packaging solutions for high-volume applications like food service containers, corrugated e-commerce cartons, and retail-ready packaging.

Germany: Circular Economy Leadership Driving Next Generation Fiber-Based Packaging

Germany remains one of the most advanced and influential markets for next generation paper and fiber packaging, guided by the EU’s Packaging and Packaging Waste Regulation (PPWR). This regulatory framework, coupled with Germany’s own reusable packaging obligation implemented in 2023, compels businesses to offer environmentally friendly alternatives to single-use plastics. Such stringent policies are accelerating the adoption of recyclable mono-material solutions, particularly in sectors where sustainability has become a non-negotiable requirement.

Technological innovation further reinforces Germany’s leadership. Local companies are pioneering high-performance, lightweight, and recycled paperboard solutions for food, beverage, and pharmaceutical packaging. The country’s advanced recycling infrastructure and commitment to circular economy practices allow brands to close the loop more effectively than in many other markets. Demand is surging in food and pharmaceuticals, where fiber-based packaging now safeguards cereals, frozen foods, cosmetics, and OTC medications while meeting both regulatory and consumer expectations for eco-responsibility.

China: Government Support and High-Tech Manufacturing Strengthen Next Gen Paper Packaging

China’s next generation paper and fiber packaging market is growing under the influence of strong governmental support and manufacturing innovation. Policies linked to the nation’s “dual-carbon” targets encourage companies to use sustainable feedstocks like agricultural residues for pulp production. These efforts align with broader strategies to upgrade the high-end manufacturing sector, ensuring paper and fiber packaging aligns with China’s sustainability roadmap.

Chinese producers are also at the forefront of technological upgrades, leveraging automation and artificial intelligence for quality control and efficiency. Companies like Yibin Hiest Fiber have introduced man-made cellulosic fiber lines that integrate recycled content, highlighting China’s innovation capacity. With the nation’s booming e-commerce, electronics, and consumer goods industries, the demand for lightweight, durable, and eco-friendly packaging is accelerating. Smartphone boxes, cosmetics packaging, and personal care cartons represent key growth segments, supported by rising capital inflows from both government and private investors.

India: Agricultural Residues and Policy Push Fuel Next Generation Fiber Packaging Growth

India represents one of the most promising growth markets for next generation paper and fiber packaging, thanks to its abundant agricultural residues and strong government initiatives. The “Make in India” program and the Production Linked Incentive (PLI) scheme are channeling investments into domestic production, while nearly 500 million tonnes of agricultural residues remain available as an underutilized feedstock for fiber-based packaging. This resource advantage positions India as a potential global leader in sustainable paper and fiber solutions.

Technological and corporate investments are also reshaping the market. Ahlstrom’s 2024 collaboration with The Paper People to develop fiber-based frozen food packaging highlights the emphasis on food-safe and sustainable innovations. Meanwhile, a 2024 roundtable by Canopy, Invest India, and the UN India projected India’s potential to produce over 10 million tonnes of next generation fiber and attract $15 billion in investments by 2033. Rising demand from e-commerce, pharmaceuticals, and FMCG sectors, coupled with the growth of organized retail, is ensuring that sustainable packaging becomes integral to brand identity and supply chain efficiency.

Japan: Regulatory Shifts and Premium Packaging Standards Shape Fiber-Based Solutions

Japan’s next generation paper and fiber packaging market is being reshaped by new regulatory rules for food packaging introduced in June 2025. The shift to a “positive list” system for allowable synthetic materials has created opportunities for paper-based packaging with safe coatings and additives. This regulatory tightening reinforces Japan’s strong sustainability agenda while ensuring consumer safety in food-contact applications.

Japanese companies are well known for combining high functionality with aesthetics in packaging, and this extends into their fiber-based innovations. Nippon Paper Industries’ SHIELDPLUS®—a barrier material that preserves oxygen and flavors—demonstrates Japan’s focus on advanced coatings and finishes. Corporations like Nissui are also setting clear guidelines to reduce plastic usage, including replacing plastic trays with mono cartons. With strong demand from food, beverage, and electronics industries, Japan’s market thrives on its reputation for premium packaging that not only protects but also elevates the consumer experience.

Next Generation Paper and Fiber Packaging Market Report Scope

Next Generation Paper and Fiber Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$355.5 Billion

|

|

Market Size (2034)

|

$488.7 Billion

|

|

Market Growth Rate

|

3.6%

|

|

Segments

|

By Material Type (Molded Pulp, Corrugated Board, Paperboard, Kraft Paper, Bagasse-based Packaging, Others), By Technology (Barrier Coatings, Molding and Forming, Digital Printing, Lamination, Others), By End-Use Industry (Food & Beverage, Electronics & Electricals, Cosmetics & Personal Care, E-commerce & Logistics, Pharmaceuticals & Healthcare, Others), By Application (Boxes & Cartons, Trays & Clamshells, Films & Wraps, Bags & Pouches, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

International Paper Company, WestRock Company, Smurfit Kappa Group PLC, DS Smith Plc, Graphic Packaging Holding Company, Mondi Group, Huhtamaki Oyj, Stora Enso Oyj, Sonoco Products Company, Rengo Co., Ltd., Paptic Ltd., Ahlstrom, Koehler Paper Group, Walki Group, Billerud AB

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Next Generation Paper and Fiber Packaging Market Segmentation

By Material Type

- Molded Pulp

- Corrugated Board

- Paperboard

- Kraft Paper

- Bagasse-based Packaging

- Others

By Technology

- Barrier Coatings

- Molding and Forming

- Digital Printing

- Lamination

- Others

By End-Use Industry

- Food & Beverage

- Electronics & Electricals

- Cosmetics & Personal Care

- E-commerce & Logistics

- Pharmaceuticals & Healthcare

- Others

By Application

- Boxes & Cartons

- Trays & Clamshells

- Films & Wraps

- Bags & Pouches

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Next Generation Paper and Fiber Packaging Market

- International Paper Company

- WestRock Company

- Smurfit Kappa Group PLC

- DS Smith Plc

- Graphic Packaging Holding Company

- Mondi Group

- Huhtamaki Oyj

- Stora Enso Oyj

- Sonoco Products Company

- Rengo Co., Ltd.

- Paptic Ltd.

- Ahlstrom

- Koehler Paper Group

- Walki Group

- Billerud AB

* List Not Exhaustive

Methodology

USDAnalytics employs a rigorous, data-driven methodology to provide actionable insights into the global next-generation paper and fiber packaging market. Our approach combines primary research, including interviews with packaging engineers, sustainability specialists, and supply chain managers, with secondary research from regulatory frameworks, industry reports, patent filings, company disclosures, and academic publications. Market sizing and forecasting leverage historical trends, adoption rates of bio-based fibers (bagasse, hemp, sugarcane, flax), recycled materials, barrier coatings, and digital packaging technologies such as QR codes, NFC, and RFID tags. Technological trends, including molded pulp innovations, PFAS-free coatings, mycelium-based feedstocks, and high-barrier paper solutions, are analyzed alongside regulatory influences from the EU, U.S., Japan, and other key markets, ensuring compliance-driven growth insights. Competitive intelligence evaluates strategic mergers, product launches, and sustainability initiatives by leading players such as Mondi Group, Smurfit WestRock, DS Smith, Paptic Ltd., and Graphic Packaging International, highlighting their deployment of recyclable, compostable, and digitally enabled paper and fiber packaging solutions. This comprehensive methodology ensures USDAnalytics delivers precise, professional, and market-ready insights for industry professionals navigating the evolving landscape of sustainable, high-performance packaging.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.