Market Overview: Bio-Based Formulations and Hot-Melt Adoption Drive Growth

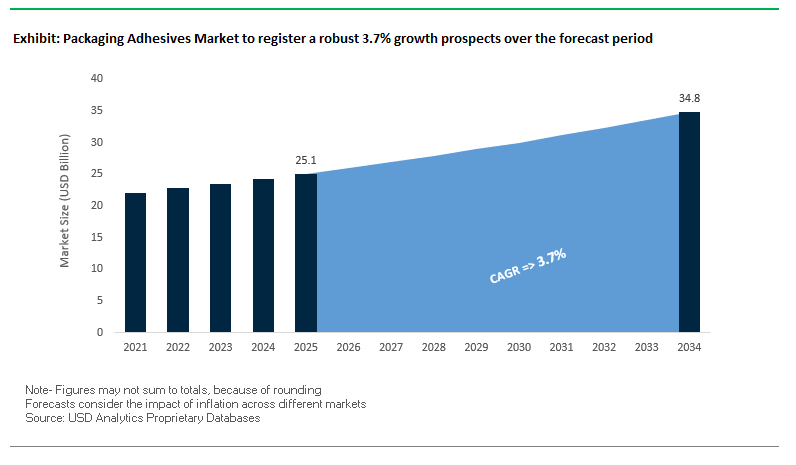

The global packaging adhesives market is projected to expand from USD 25.1 billion in 2025 to USD 34.8 billion by 2034, reflecting a steady CAGR of 3.7%. This growth is underpinned by the industry’s shift toward sustainable adhesive solutions and the increasing demand from food, beverage, consumer goods, and e-commerce packaging. Adhesives play a critical role in ensuring product safety, durability, and recyclability, making them a fundamental enabler of the packaging supply chain.

A significant transformation in the industry is the adoption of bio-based and renewable raw materials. With mounting global regulations on single-use plastics and carbon emissions, packaging manufacturers are looking for adhesives that support recyclability, compostability, and the circular economy. Water-based adhesives dominate the market as they offer VOC-compliant, food-safe solutions, while hot-melt adhesives are gaining traction in high-speed corrugated packaging and carton sealing applications. Additionally, the demand for food-safe adhesives is accelerating, as companies must comply with strict international standards to prevent harmful migration into packaged foods.

Key Insights for Industry Professionals:

- Sustainability is a top driver, with bio-based and recyclable adhesives leading innovation.

- Water-based adhesives dominate, ensuring compliance with VOC regulations and food safety standards.

- Hot-melt adhesives are rising, critical for high-speed automated packaging and corrugated applications.

- Food safety regulations are shaping adhesive development, especially in flexible packaging and retort pouches.

Market Analysis: Recent Industry Developments Strengthening Innovation

The packaging adhesives industry is undergoing rapid transformation, fueled by sustainability initiatives, acquisitions, and technological innovations.

In August 2025, Henkel introduced its EPIX technology platform, designed to enhance functional barrier protection in paper packaging, highlighting the growing need for adhesives compatible with fiber-based sustainable materials. A month earlier, in July 2025, H.B. Fuller launched eco-friendly adhesive solutions for glass bottle labeling, enabling easy wash-off to support PET recycling. This directly ties into circular economy goals, as packaging players prioritize recyclability across formats.

In June 2025, Bostik unveiled its Kizen LIME range, adhesives with more than 80% renewable content for recyclable paper and cardboard packaging. Similarly, Arkema collaborated in April 2025 with a food packaging company to create mono-material pouch adhesives, enhancing recyclability of flexible packaging. Henkel further advanced in March 2025 with its Aquence PS 3017 RE, a water-based acrylic adhesive that enables clean label removal from PET bottles, boosting recycled PET purity.

M&A activity is reshaping competition. In December 2024, Arkema completed the acquisition of Dow’s flexible packaging laminating adhesives business, strengthening Bostik’s portfolio in flexible packaging. Earlier, in September 2024, Bostik launched the bio-based Kizen LIME range in collaboration with Dow and Nordson, underlining industry-wide momentum toward renewable raw materials. Henkel’s RE range, launched in May 2024, was another breakthrough, offering adhesives specifically designed for recyclability.

Innovations and Opportunities Defining the Future of the Packaging Adhesives Market

Accelerated Shift Towards Water-Based and Bio-Based Adhesive Formulations

The packaging adhesives market is witnessing an accelerated transition from solvent-based formulations to water-based and bio-based adhesives, primarily driven by regulatory mandates, sustainability initiatives, and consumer brand commitments. Governments across major regions are tightening VOC (Volatile Organic Compound) regulations to minimize environmental impact. For instance, Canada’s Volatile Organic Compound Concentration Limits for Certain Products Regulations took effect in January 2024, imposing stringent limits on adhesives and sealants. Similarly, regions such as Hong Kong have been enforcing VOC controls since 2010, reinforcing the global momentum toward low-emission adhesives.

Leading companies are also investing heavily in sustainable solutions. In June 2025, H.B. Fuller launched its Swift® Lock 8800 waterborne adhesive series tailored for high-speed flexible packaging applications, offering reduced VOC emissions alongside compliance with food safety standards. Meanwhile, bio-based formulations are gaining traction, with Bostik’s Kizen™ LIME adhesive range introduced in September 2024 containing over 80% renewable content sourced from ISCC PLUS–certified bio-based materials. These innovations reflect how adhesive producers are strategically reformulating to support circular economy goals while ensuring performance in demanding packaging operations.

Development of Functional Adhesives for PCR and Mono-Material Packaging

The rising adoption of post-consumer recycled (PCR) content and mono-material packaging structures is creating new performance challenges for adhesives. These substrates often exhibit lower surface energy or contamination, requiring adhesives with enhanced bonding capability and recyclability. Research highlights that coatings like SiOx (silicon oxide) and AlOx (aluminum oxide) are increasingly used to deliver barrier properties while keeping packaging recyclable under EU guidelines.

On the industrial front, new formulations are being engineered for high-speed compatibility. For example, Covestro’s heat-resistant coating, highlighted in Plastics Engineering (May 2023), enables BOPE-based mono-material films to run efficiently on form-fill-seal lines overcoming one of the biggest hurdles of sustainable films. Collaborative efforts are also advancing this trend. In May 2025, Henkel and Synthomer announced a partnership integrating Synthomer’s CLIMA resins into Henkel’s TECHNOMELT hot melts, reducing carbon emissions by 20% or more while maintaining performance. These advancements signal a market-wide push to ensure adhesives can support recyclability targets without compromising efficiency.

Advanced Adhesives for Smart and Active Packaging Integration

The expansion of smart and active packaging technologies such as RFID tags, NFC sensors, oxygen scavengers, and antimicrobial layers presents a high-value opportunity for adhesive innovators. Adhesives are no longer passive components but are increasingly critical for embedding functionality directly into packaging systems.

For instance, a study in the International Journal of Biological Macromolecules demonstrated how a cellulose-based adhesive with antimicrobial additives doubled the shelf life of cheese, extending it from four to eight weeks. This showcases the potential of adhesives to contribute to food safety and preservation. Similarly, active packaging systems that rely on oxygen scavengers or freshness indicators require adhesives compatible with functional additives, ensuring no interference with their performance. On the electronics side, adhesives are being developed to securely bond RFID and NFC tags onto substrates ranging from paperboard cartons to flexible polymer films. By doing so, packaging becomes an enabler of inventory management, supply chain transparency, and consumer engagement, creating a strong growth niche for specialized adhesive solutions.

Adhesives Enabling Full Circularity through Dissolution, Debonding, and Re-Pulping

Perhaps the most transformative opportunity lies in adhesives designed to actively enable circularity. Beyond being “recycling compatible,” next-generation adhesives are engineered for controlled debonding, clean dissolution, and efficient material recovery.

Technologies like wash-off adhesives, developed by companies such as HERMA and UPM Raflatac, are already improving PET recycling streams by allowing plastic labels to detach cleanly during the washing process. In fiber-based packaging, adhesives that dissolve fully during the re-pulping process are key to preventing “stickies,” ensuring higher-quality recycled paper. Additionally, research into solvent-based delamination highlights selective dissolution as a method for separating layers and adhesives, producing purer recyclates for flexible packaging. By addressing these challenges, adhesives become central to the packaging circular economy, opening doors for adhesive manufacturers to position themselves as sustainability enablers across the packaging value chain.

Competitive Landscape: Leading Players in Packaging Adhesives Market

The packaging adhesives industry is highly consolidated, with innovation driven by sustainability, acquisitions, and product performance. Global leaders are reshaping competition through bio-based formulations, recyclable compatibility, and high-performance adhesive technologies.

Henkel AG & Co. KGaA: Driving Circularity with RE and EPIX Platforms

Henkel is a global leader in adhesives, offering hot-melt, water-based, and pressure-sensitive adhesives under its Technomelt and Loctite brands. In August 2025, it launched its EPIX platform for barrier-coated paper packaging, addressing sustainability challenges. Its RE range of adhesives further enhances recyclability across packaging formats. With strong R&D and global reach, Henkel’s strategy is focused on sustainability, innovation, and carbon footprint reduction, making it a leading partner for industries from food to e-commerce.

H.B. Fuller Company: Sustainability-Centered Adhesive Solutions

H.B. Fuller delivers a diverse portfolio of hot-melt and water-based adhesives for flexible packaging, labeling, and carton sealing. In July 2025, it introduced sustainable glass bottle labeling adhesives, enabling easy label wash-off for PET recycling. Its Advantra Earthic™ carbon-neutral adhesives and Open Sesame® fiber-based tear tapes highlight its push toward plastic-free packaging. With a strong sustainability focus, H.B. Fuller is addressing energy reduction, waste minimization, and improved recyclability for global packaging leaders.

Arkema S.A. (Bostik): Expanding Through Acquisitions and Renewable Adhesives

Through its Bostik division, Arkema has emerged as a powerhouse in packaging adhesives, offering high-performance laminating adhesives for flexible packaging. The acquisition of Dow’s laminating adhesives business in December 2024 solidified its market presence. Its Kizen LIME adhesives, with over 80% renewable content, cater to recyclable paper and cardboard packaging. Bostik emphasizes bio-based innovation, food safety compliance, and recyclability, positioning itself as a strategic partner for FMCG and industrial players.

Dow Inc.: Supplying Foundational Chemistry for Adhesive Innovation

Although Dow divested its laminating adhesives division to Arkema, it remains a key supplier of raw materials, including polyolefins and acrylics used in adhesive formulations. Its AFFINITY RE brand, developed with Bostik for bio-based adhesives, illustrates Dow’s role in enabling partners to innovate sustainably. By focusing on bio-based chemistry and recycled content materials, Dow plays a critical role in advancing eco-friendly packaging adhesives globally.

Ashland Global Holdings Inc.: Specialty Additives Enhancing Adhesive Performance

Ashland contributes through polymer additives and performance enhancers used in water-based adhesive formulations. Its Natrosol™ and Aquaflow™ product lines are essential for improving adhesion, sag resistance, and functionality of packaging adhesives. In July 2025, Ashland advanced its $60 million manufacturing network optimization plan, designed to streamline operations and improve profitability. With expertise in polymer chemistry, Ashland ensures durability, safety, and compliance, supporting adhesive manufacturers serving labels, corrugated packaging, and specialty packaging markets.

Packaging Adhesives Market Share Insights

Polyurethane Leads Packaging Adhesives Market Share by Resin Type

Polyurethane adhesives hold the largest share at 30% of the packaging adhesives market, driven by their superior flexibility, heat resistance, and chemical compatibility in high-performance packaging applications. Their indispensability in flexible packaging lamination, frozen food applications, and case/carton sealing where durability is critical has made them the go-to choice for brand owners and converters alike. Acrylics hold a strong position in pressure-sensitive labels and tapes, EVA remains dominant in hot-melt adhesives for high-speed carton sealing, and bio-based resins are emerging rapidly due to sustainability mandates. However, polyurethane’s balance of performance and versatility ensures it leads both in market share and technological innovation. With rising demand for lightweight, multilayer packaging formats that require strong, long-lasting bonds, polyurethane continues to anchor adhesive demand across diverse end-use industries.

Cases & Cartons Dominate Packaging Adhesives Market Share by Application

Cases and cartons represent the largest application share at 28% of the global packaging adhesives market, reflecting their ubiquity in global supply chains. Every corrugated case and retail carton requires reliable adhesives that can withstand high-speed automation and harsh logistics environments, making this the single largest volume driver. Flexible packaging follows closely, propelled by the shift toward multilayer laminates that demand advanced polyurethane adhesives for extended shelf life and product safety. Labels and tapes continue to expand with the boom in e-commerce, while folding cartons, particularly for cosmetics and electronics, require precision adhesive performance for aesthetic and functional integrity. Specialty packaging, though smaller, plays a critical role in medical and niche applications where sterilization resistance and chemical compatibility are essential. Still, the sheer volume of global shipping and retail-ready cartons ensures cases and cartons remain the centerpiece of adhesive consumption, driving continuous innovation in speed, strength, and sustainability.

United States: Consumer Preferences and Sustainable Adhesive Technologies Driving Growth

The U.S. packaging adhesives market is witnessing significant growth, fueled by evolving consumer preferences for lightweight, flexible, and convenient packaging, especially in the food and beverage sectors. The booming e-commerce industry is a primary catalyst, with demand for adhesives capable of supporting high-speed automated packaging lines and providing tamper-proof seals for shipping.

Technological advancements are also shaping the market, with companies developing water-based and solvent-free adhesives to meet stringent environmental standards and brand owner requirements. Notable developments include Arkema’s acquisition of Dow's flexible packaging laminating adhesives business, expanding sustainable adhesive solutions. Additionally, regulatory policies from the EPA and FDA are driving the adoption of low VOC, food-safe adhesives, while sustainability initiatives encourage adhesives that support recyclability and renewable material use, aligning with corporate environmental goals.

Germany: Circular Economy Leadership and Eco-Innovation Fueling Market Expansion

Germany’s packaging adhesives market is heavily influenced by strict regulations, including the EU Packaging and Packaging Waste Regulation (PPWR), creating a high demand for eco-friendly and recyclable adhesive solutions. The country’s focus on a circular economy has promoted collaboration between manufacturers and end-users to develop adhesives that integrate recycled content and facilitate sustainable packaging operations.

Technological innovations are driving product development, with companies like Henkel and Wacker Chemie AG creating adhesives that are both lightweight and sustainable, supporting flexible packaging in food, pharmaceuticals, and personal care industries. The adoption of eco-design principles and tankless systems is also boosting market value, offering higher performance adhesives with reduced material usage, further strengthening Germany’s position as a hub for advanced and sustainable adhesive technologies.

China: Industrialization and High-Performance Adhesives Transforming the Market

China’s packaging adhesives industry is propelled by rapid industrial expansion and growing manufacturing activity in food, e-commerce, and logistics sectors. The country is investing heavily in automation and AI technologies, including robotics, to enhance efficiency and meet the demand for automated packaging solutions.

High-performance adhesives are a key market trend, with hot-melt adhesives featuring fast setting times and strong bonding capabilities becoming increasingly essential for high-speed packaging lines. The government’s dual carbon goals are also influencing the sector, encouraging the development of eco-friendly, reusable, and reduced-material packaging solutions, solidifying China’s position as a leader in technologically advanced and sustainable adhesive solutions.

India: E-commerce Growth and Sustainable Adhesive Innovations Driving Market Demand

India’s packaging adhesives market is benefiting from governmental initiatives like Make in India and Zero Effect Zero Defect, which encourage domestic production and support regulatory compliance and industrial investments. The rapid expansion of e-commerce and online grocery platforms is a key driver, boosting demand for durable, hygienic, and lightweight adhesives suitable for high-speed packaging operations.

Sustainability is increasingly critical, with Plastic Waste Management (Amendment) Rules fostering demand for biodegradable and eco-friendly adhesives. The Indian adhesives industry is also innovating through low-VOC formulations, bio-based raw materials, and smart adhesive technologies, combining environmental responsibility with enhanced performance, making India a rapidly evolving market for sustainable and high-performance packaging adhesives.

Brazil: Regulatory Measures and Technological Advancements Enhancing Market Growth

In Brazil, stringent regulations against single-use plastics are promoting the adoption of reusable and durable adhesive solutions. The National Solid Waste Policy supports a circular economy, driving the transition toward sustainable packaging adhesives. Technological advancements, including the use of robotics and AI, are enhancing production efficiency, enabling automated sorting, defect detection, and high-quality adhesive applications.

The market is witnessing a strong shift toward sustainability and innovation, exemplified by COIM Group’s expansion in water-based adhesives for rapid packaging in food and detergent sectors. Strategic partnerships and increased patent filings in adhesive technologies highlight Brazil’s dynamic focus on innovative, eco-friendly, and high-performance adhesives, strengthening the country’s packaging industry ecosystem.

Japan: Advanced Recycling and Smart Adhesives Shaping Industry Trends

Japan’s packaging adhesives market leverages one of the world’s highest rates of plastic and paper recycling, supported by the Plastic Resource Circulation Act, fostering circular packaging solutions. The market is moving toward bio-based materials to meet environmental goals, particularly for food and pharmaceutical packaging, with collaborations among companies like LyondellBasell, Shiseido, Futamura Chemical, and Iwatani driving innovation.

Functionality and performance are central to market development. Japanese firms, including Toyochem Co., Ltd., are pioneering adhesives for flexible packaging, while academic research focuses on smart adhesives and sealants with properties like self-healing, thermal conductivity, and environmental responsiveness. These advancements position Japan as a global leader in innovative, sustainable, and technologically advanced packaging adhesives.

Packaging Adhesives Market Report Scope

Packaging Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$25.1 Billion

|

|

Market Size (2034)

|

$34.8 Billion

|

|

Market Growth Rate

|

3.7%

|

|

Segments

|

By Technology (Water-based, Solvent-based, Hot-Melt, Reactive & Others), By Resin Chemistry (Acrylics, Polyurethane, EVA, Styrenic Block Copolymers, Natural/Bio-based), By Application (Cases & Cartons, Flexible Packaging, Folding Cartons, Labels & Tapes, Sealing, Specialty Packaging), By End-Use Industry (Food & Beverages, Pharmaceuticals & Healthcare, E-commerce Retail Fulfillment, Personal Care & Cosmetics, Industrial & Consumer Goods, Other Industries)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, H.B. Fuller Company, The Dow Chemical Company (Dow Inc.), Arkema S.A. (Bostik), 3M Company, Sika AG, Avery Dennison Corporation, Wacker Chemie AG, DIC Corporation, Ashland Global Holdings Inc., Pidilite Industries Limited, Huntsman Corporation, Jowat SE, Toyochem Co., Ltd., BASF SE

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Packaging Adhesives Market Segmentation

By Technology

- Water-based

- Solvent-based

- Hot-Melt

- Reactive & Others

By Resin Chemistry

- Acrylics

- Polyurethane

- EVA

- Styrenic Block Copolymers

- Natural/Bio-based

By Application

- Cases & Cartons

- Flexible Packaging

- Folding Cartons

- Labels & Tapes

- Sealing

- Specialty Packaging

By End-Use Industry

- Food & Beverages

- Pharmaceuticals & Healthcare

- E-commerce Retail Fulfillment

- Personal Care & Cosmetics

- Industrial & Consumer Goods

- Other Industries

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Packaging Adhesives Market

- Henkel AG & Co. KGaA

- H.B. Fuller Company

- The Dow Chemical Company (Dow Inc.)

- Arkema S.A. (Bostik)

- 3M Company

- Sika AG

- Avery Dennison Corporation

- Wacker Chemie AG

- DIC Corporation

- Ashland Global Holdings Inc.

- Pidilite Industries Limited

- Huntsman Corporation

- Jowat SE

- Toyochem Co., Ltd.

- BASF SE

*List not Exhaustive

Research Coverage

This report by USDAnalytics investigates the global packaging adhesives market, providing a comprehensive analysis of technological breakthroughs, sustainability innovations, and market dynamics shaping adhesive solutions across industries. The analysis reviews recent advancements in bio-based, water-based, and hot-melt adhesive formulations, highlighting their critical role in supporting recyclable, compostable, and circular packaging solutions. This report also explores functional adhesives for mono-material packaging, post-consumer recycled (PCR) content, and smart packaging integration, alongside innovations enabling debonding, dissolution, and re-pulping to enhance circularity. Competitive developments, including strategic acquisitions, partnerships, and regional expansion strategies, are evaluated, making this report an essential resource for industry professionals seeking actionable insights on investment, product development, and regulatory compliance. USDAnalytics’ analysis emphasizes the evolution of adhesive technologies in high-speed automated packaging, food-safe applications, and e-commerce fulfillment, providing a forward-looking perspective on market growth, emerging opportunities, and sustainability-driven innovations.

Scope Highlights:

- Segmentation: By Technology (Water-based, Solvent-based, Hot-Melt, Reactive & Others), By Resin Chemistry (Acrylics, Polyurethane, EVA, Styrenic Block Copolymers, Natural/Bio-based), By Application (Cases & Cartons, Flexible Packaging, Folding Cartons, Labels & Tapes, Sealing, Specialty Packaging), By End-Use Industry (Food & Beverages, Pharmaceuticals & Healthcare, E-commerce Retail Fulfillment, Personal Care & Cosmetics, Industrial & Consumer Goods, Other Industries)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa

- Timeframe: Historic data from 2021 to 2024 and forecast data from 2025 to 2034

- Companies: Analysis and profiles of 15+ leading companies, including Henkel, H.B. Fuller, Arkema (Bostik), Dow, 3M, Sika, Avery Dennison, Wacker Chemie, BASF, Ashland, and Pidilite

Methodology

USDAnalytics employed a multi-tiered research methodology combining primary and secondary sources to deliver a comprehensive market perspective. Primary research involved detailed interviews and consultations with adhesive manufacturers, packaging converters, OEMs, distributors, and end-users to gather insights on technology adoption, product performance, and regulatory compliance. Secondary research incorporated analysis of corporate filings, patent data, trade journals, regulatory updates, and sustainability reports to validate market trends and historic performance. Quantitative modeling techniques were used to estimate market size, share, and growth rates across resin chemistries, technologies, and end-use applications. Qualitative analysis assessed competitive strategies, innovation pipelines, and regional dynamics, including the adoption of sustainable formulations and smart packaging adhesives. This rigorous approach ensures reliable forecasts, strategic insights, and actionable guidance for professionals seeking to optimize production, sustainability, and product development in the global packaging adhesives market.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.