Secondary Paper and Paperboard Luxury Packaging Market Size, Overview, and Growth Outlook (2025–2034)

Secondary Paper and Paperboard Luxury Packaging Market Projected to Reach $10.2 Billion by 2034 Driven by Premium Branding and Sustainability Initiatives

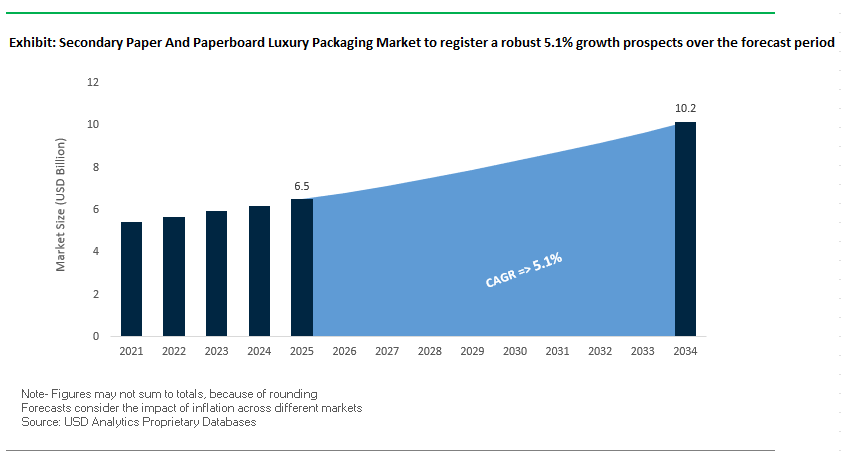

The global secondary paper and paperboard luxury packaging market is expected to grow from $6.5 billion in 2025 to $10.2 billion by 2034, at a CAGR of 5.1%. This market focuses on high-end outer packaging such as rigid boxes, folding cartons, and specialty bags for luxury items including cosmetics, spirits, and fashion products. The market combines brand aesthetics, consumer engagement, and environmental responsibility, creating opportunities for packaging manufacturers and brand owners alike.

Key Insights for Industry Professionals:

- Enhancing Brand Image: Luxury brands increasingly use premium packaging to create a memorable unboxing experience, driving customer loyalty and social media virality.

- Sustainability Focus: A 2025 study shows 86% of FMCG brands are willing to pay more for sustainable packaging, accelerating adoption of recycled fibers, biodegradable inks, and plastic-free reinforcements.

- Innovative and Functional Design: Techniques like embossing, debossing, foil stamping, magnetic closures, and specialty finishes help brands differentiate in competitive luxury segments.

- Smart Packaging Integration: Use of NFC tags and QR codes allows for interactive, personalized experiences and provides product traceability.

- Consumer Experience as a Growth Driver: Packaging serves as a physical representation of brand values, enhancing perceived quality and exclusivity.

The market is positioned at the intersection of premium design, sustainability, and consumer engagement, making it a critical area for innovation in luxury packaging.

Market Analysis: Recent Strategic Moves Highlight Sustainability and Innovation in Luxury Packaging

The secondary paper and paperboard luxury packaging market is witnessing strong momentum from sustainability initiatives, advanced materials, and strategic acquisitions. In August 2025, Klöckner Pentaplast won the German Packaging Award for its kp 100% Tray2Tray® innovation, underlining the industry's commitment to sustainable materials. In the same month, Aquapak Polymers Ltd highlighted that 86% of FMCG brands are willing to pay more for eco-friendly packaging, signaling growing market demand for sustainable solutions.

Innovation and circular economy efforts are also shaping the market. In March 2025, a Danish-Indian collaboration launched the 'From Beach to Big Bags' initiative, converting ocean-bound and inland plastic waste into recycled polypropylene (rPP) big bags for industrial use. February 2025 saw Berry Global Group partner with Mars to switch pantry jar packaging for M&M’S, SKITTLES, and STARBURST to 100% recycled plastic, eliminating 1,300 metric tons of virgin plastic annually.

Market consolidation and capacity expansion continue to be key drivers. December 2024, Sonoco acquired Eviosys, enhancing its presence in metal food cans and aerosol packaging. In October 2024, International Paper acquired UK-based DS Smith, forming one of the largest paper packaging companies globally. Concurrently, Mondi acquired Schumacher Packaging’s European operations, increasing corrugated converting capacity in Germany, Benelux, and the UK. These strategic moves underscore the market’s focus on innovation, sustainability, and operational scale.

Secondary Paper and Paperboard Luxury Packaging Market: Regulatory Shifts and Digital Transformation Unlocking Growth

Mandated Elimination of Plastic and Non-Recyclable Components from Secondary Packaging

The secondary paper and paperboard luxury packaging market is undergoing a regulatory-driven transformation as governments enforce stricter rules on the use of plastics and non-recyclable materials. The EU’s Packaging and Packaging Waste Regulation (PPWR), effective since February 2025, requires all packaging to be recyclable in an economically viable way by 2030, directly impacting laminated boxes, plastic inserts, and composite structures historically used in luxury packaging. This shift forces brands to prioritize fiber-based designs that maintain luxury aesthetics while ensuring compliance with recyclability mandates. On the corporate side, LVMH’s LIFE 360 sustainability program, detailed in its 2024 environmental report, highlights how luxury groups are pledging to phase out fossil-based materials and embed “creative circularity” across all packaging lines. Such initiatives not only ensure compliance but also enhance brand equity as eco-conscious consumers increasingly scrutinize packaging choices. The push to eliminate plastics is no longer a peripheral adjustment; it is now a central market driver, reshaping how premium brands approach structural and decorative elements in secondary packaging.

Strategic Investment in Advanced Digital Printing for Hyper-Personalization

Luxury brands are leveraging advanced digital printing technologies to deliver hyper-personalized packaging solutions at scale. Unlike traditional offset printing, which requires costly plates and long lead times, digital printing enables mass customization with minimal setup costs. A 2024 industry report notes that brands can now add unique names, messages, or bespoke patterns on each box within a production run, a breakthrough in personalization previously unattainable in luxury packaging. This capability is particularly valuable for limited editions and seasonal collections, where agility and exclusivity are critical differentiators. Furthermore, digital printing supports on-demand production, minimizing overstock and reducing waste, aligning with the industry’s broader sustainability goals. By combining personalization with speed-to-market, brands can create a stronger emotional bond with consumers, driving loyalty while maintaining cost-effectiveness for small-batch runs. This is rapidly becoming a strategic investment area for luxury houses seeking to differentiate their packaging through design innovation and sustainability.

Development of High-Performance Molded Fiber Inserts and Structures

The replacement of traditional plastic and foam inserts with high-performance molded fiber solutions presents a major opportunity in the secondary luxury packaging market. Advanced processes such as wet-pressed and thermoformed pulp molding now enable inserts with ultra-smooth surfaces, fine detailing, and soft-touch finishes, qualities once associated only with plastic. According to a 2024 industry case study, these molded fiber inserts not only offer premium aesthetics but also deliver superior protection for fragile items such as cosmetics, watches, and fine jewelry. Additionally, they are manufactured from 100% recycled fibers, making them fully recyclable with household paper waste and eliminating landfill-destined multi-material packaging. This innovation directly supports the circular economy, offering luxury brands a way to enhance their unboxing experience while meeting regulatory and consumer sustainability demands. For luxury packaging manufacturers, the scaling of molded fiber production capacity represents a profitable growth avenue as more brands pivot to this eco-luxury material.

Integration of NFC and Smart Technologies for Authentication and Engagement

The integration of smart packaging technologies such as NFC tags and embedded sensors within rigid luxury boxes is redefining both brand protection and consumer experience. Counterfeiting remains a multi-billion-dollar problem in the luxury sector, and NFC-enabled packaging provides instant product authentication with a simple smartphone tap. A 2025 technical overview from an NFC technology provider demonstrated how discreetly embedded tags create unique digital identities for each unit, providing a reliable shield against counterfeit infiltration. Beyond security, the opportunity lies in consumer engagement—NFC-enabled packaging can serve as a gateway to exclusive brand content, craftsmanship stories, or loyalty rewards, effectively extending the unboxing into a personalized digital journey. A report on luxury smart packaging notes that this dual functionality—protection and engagement—is rapidly gaining traction among high-end brands, making it a critical innovation area. For luxury groups, integrating smart features into paper-based packaging combines sustainability, authenticity, and digital connectivity, aligning with both regulatory imperatives and evolving consumer expectations.

Competitive Landscape: Leading Companies Are Driving Innovation and Sustainability in Luxury Paperboard Packaging

The secondary paper and paperboard luxury packaging market is dominated by global players leveraging materials expertise, manufacturing capabilities, and innovative design to deliver high-performance and sustainable packaging solutions.

Smurfit Kappa Group: Creating Sustainable, High-Impact Packaging Solutions for Luxury Brands

Smurfit Kappa offers a wide range of recyclable and reusable corrugated solutions for e-commerce and retail applications. In July 2024, its merger with WestRock formed Smurfit WestRock, a global packaging giant with over 100,000 employees across 40 countries. The company excels in vertically integrated production and packaging machinery development, providing innovative solutions for diverse markets while maintaining a strong focus on sustainability and brand differentiation.

Mondi Group: Expanding European Capacity with Sustainable Paperboard Solutions

Mondi Group is recognized for sustainable packaging solutions across construction, automotive, and consumer sectors. In October 2024, Mondi acquired Schumacher Packaging’s German, Benelux, and UK corrugated operations, valued at €634 million, significantly increasing European production capacity. Mondi leverages a vertically integrated business model and material expertise to provide high-quality, compliant packaging that aligns with premium brand expectations.

International Paper Company: Scaling Global Reach Through Strategic Acquisitions

International Paper provides containerboard, corrugated boxes, and paper-based products. Its October 2024 acquisition of DS Smith for $7.2 billion expands its global footprint, making it a major competitor to Smurfit WestRock. The company focuses on innovation, vertical integration, and operational efficiency to deliver sustainable luxury packaging solutions across multiple industries.

Graphic Packaging Holding Company: Driving Sustainable Growth in Fiber-Based Packaging

Graphic Packaging specializes in folding cartons, cups, and paperboard packaging for food, beverage, and consumer products. In May 2021, it acquired AR Packaging, a European folding carton leader, for $1.45 billion, strengthening its sustainability credentials and European market presence. The company prioritizes eco-friendly materials, vertical integration, and compliance with global sustainability goals.

WestRock Company: Leveraging Scale and Expertise to Enhance Luxury Packaging Capabilities

WestRock offers containerboard, corrugated boxes, and paper-based packaging products. Its July 2024 merger with Smurfit Kappa formed Smurfit WestRock, creating a global powerhouse with extensive resources and expertise. WestRock focuses on innovative, compliant, and high-quality packaging solutions, supporting brands in delivering premium consumer experiences while meeting sustainability objectives.

Secondary Paper And Paperboard Luxury Packaging Market Share Insights, 2025-2034

Boxes Dominate Market Share by Product Type in the Secondary Paper and Paperboard Luxury Packaging Industry

Boxes hold the largest share at 45% of the secondary paper and paperboard luxury packaging market, underscoring their central role as the primary medium for premium presentation. Luxury rigid set-up boxes with magnetic closures, plush interiors, and foil-stamped finishes not only protect high-value goods but also create an immersive unboxing experience that consumers associate with exclusivity and craftsmanship. Their dominance is rooted in versatility—used extensively across cosmetics, jewelry, spirits, and electronics—where the box itself becomes an extension of the product’s brand value. The rise of sustainably engineered paperboards with high recycled content further enhances their relevance as brands balance eco-conscious mandates with premium aesthetics. While bags, display formats, and sleeves are expanding, boxes remain the undisputed cornerstone of luxury brand packaging strategies.

Cosmetics & Fragrances Lead Market Share by End-Use in the Secondary Paper and Paperboard Luxury Packaging Industry

Cosmetics and fragrances account for 30% of end-use share, making them the largest driver of luxury paper-based packaging. In this highly competitive sector, packaging is not a protective afterthought but a strategic brand differentiator, with elaborate paperboard boxes, drawer-style cartons, and multi-layered gift sets creating a sense of theater. The demand is fueled by premium skincare and fragrance launches, where packaging must balance aesthetic indulgence with sustainability through FSC-certified boards, biodegradable coatings, and refillable systems. For consumers, the box or sleeve becomes part of the luxury experience, shaping perceptions of efficacy and value. As personal care evolves toward high-margin niche and artisanal products, the cosmetics & fragrance segment continues to set benchmarks for design innovation, sustainability, and brand storytelling in luxury packaging.

European Union: PPWR, ESPR, and Mergers Driving Sustainable Luxury Paper Packaging

The European Union secondary paper and paperboard luxury packaging market is undergoing a structural transformation under the Packaging and Packaging Waste Regulation (PPWR), which became effective in February 2025. This legislation enforces recycled content and reuse targets, accelerating the transition to mono-material paperboard solutions that replace complex laminates. The Ecodesign for Sustainable Products Regulation (ESPR), effective mid-2024, adds another layer of compliance by mandating a Digital Product Passport (DPP), requiring transparency on recyclability and material origin. In addition, the ban on PFAS in food contact materials from August 2026 is driving innovation in alternative barrier coatings that maintain luxury-grade performance without harmful substances.

The EU market is further shaped by industry consolidations. The merger of Smurfit Kappa and WestRock has created a global paper packaging leader with unmatched capacity to optimize supply chains, harmonize sustainability audits, and scale innovation across Europe. At the same time, startups like Xampla, which raised $14 million for its plant-based plastic alternatives, and Paptic Ltd, which secured EUR 27.5 million to expand wood-fiber-based packaging, highlight the EU’s strong role as an innovation hub for luxury packaging solutions.

United States: EPR Laws, FSMA, and Smart Packaging Innovation

In the United States secondary paper and paperboard luxury packaging market, sustainability regulations and smart packaging technology are defining growth. Seven states, including Maryland, have enacted Extended Producer Responsibility (EPR) laws, with obligations for Producer Responsibility Organizations (PROs) to fund up to 90% of packaging waste management costs by 2030. Simultaneously, the EPA’s national recycling target of 50% by 2030 is encouraging luxury brands to re-engineer secondary packaging with recycled paperboard and traceable materials.

Luxury packaging players are also investing in RFID- and QR-enabled smart packaging, providing tamper evidence, real-time inventory tracking, and consumer engagement. This is particularly relevant in pharmaceuticals, personal care, and high-value e-commerce segments. Additionally, the Infrastructure Investment and Jobs Act is fueling investments in local recycling facilities and advanced manufacturing, supporting the growth of domestically produced sustainable luxury packaging. This creates a strong ecosystem for brands to meet sustainability targets while enhancing brand storytelling and consumer trust.

China: Regulatory Push, Premium Demand, and Green Innovation in Luxury Packaging

The China secondary paper and paperboard luxury packaging market is benefiting from both government policy and surging premium product demand. Under the 14th Five-Year Plan, the NDRC and MEE are reinforcing plastic pollution control, accelerating the adoption of paper-based alternatives for luxury secondary packaging. From June 1, 2025, regulations require express delivery companies to prioritize eco-friendly and reusable packaging, directly impacting e-commerce packaging choices.

The country’s rapidly growing premium goods and luxury market is fueling demand for aesthetic, sustainable paperboard packaging that communicates both brand prestige and eco-responsibility. China is also promoting remanufacturing and tax incentives for companies using green technologies, boosting the competitiveness of local packaging producers. Industry engagement in events such as the Green Packaging Action awards further highlights the sector’s innovation focus and regulatory alignment.

India: EPR, Paper Innovation, and Rising Beauty Industry Driving Demand

The India secondary paper and paperboard luxury packaging market is being shaped by the Plastic Waste Management (Amendment) Rules, 2024, which place strong emphasis on Extended Producer Responsibility (EPR). From July 1, 2025, all plastic components in packaging must be traceable via barcodes or QR codes, making compliance a crucial driver for brands transitioning to paperboard alternatives. Key stakeholders such as the Indian Paper Manufacturers Association (IPMA) and the Central Pollution Control Board (CPCB) are working to align paper packaging standards with sustainability goals.

Research institutions like the Central Pulp and Paper Research Institute (CPPRI) are spearheading innovations in green pulping and bleaching technologies, enhancing the environmental profile of luxury paperboard solutions. A strong demand driver is the beauty and personal care industry, where premium brands increasingly favor aesthetic and sustainable rigid paperboard packaging. This combination of policy pressure, industry research, and consumer lifestyle shifts is positioning India as an emerging hub for sustainable luxury paper packaging.

Japan: Plastic Resource Circulation Strategy and Paper Innovation Leading Market Transformation

The Japan secondary paper and paperboard luxury packaging market is accelerating its transition away from plastics under the Plastic Resource Circulation Strategy, which requires all plastic packaging to be reusable or recyclable by 2025. The Plastic Resource Circulation Promotion Law, also effective in 2025, enforces the reduction or redesign of 12 single-use plastic products, pushing luxury brands to adopt paper-based secondary packaging.

Japan’s strategy includes doubling renewable material usage by 2030 and mandating strict waste sorting systems. This has spurred cutting-edge innovations in barrier-coated paperboard materials, such as Nippon Paper Industries’ SHIELDPLUS, which provides oxygen and odor barriers essential for luxury packaging. These innovations are enabling Japanese brands in cosmetics, beverages, and premium retail to offer eco-conscious luxury packaging without compromising performance or brand value.

Brazil: Reverse Logistics and Solid Waste Laws Shaping Paperboard Luxury Packaging

The Brazil secondary paper and paperboard luxury packaging market is heavily influenced by the National Solid Waste Policy (PNRS), which mandates a reverse logistics system that holds producers responsible for recycling and end-of-life packaging recovery. In January 2025, Law No. 15,088 banned the import of waste materials, including paper and paper derivatives, compelling industries to source and recycle domestically.

Government-led sustainability efforts are encouraging luxury brands to adopt secondary paperboard packaging solutions with recyclable coatings and minimal environmental footprint. The emphasis on reuse, recycling, and sustainable design aligns with global luxury brand strategies, creating new opportunities for premium paperboard converters and packaging designers in Brazil. This policy-driven market is expected to strengthen domestic circular economy practices while supporting international brands in meeting global sustainability benchmarks.

Secondary Paper and Paperboard Luxury Packaging Market Report Scope

Secondary Paper And Paperboard Luxury Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$6.5 Billion

|

|

Market Size (2034)

|

$10.2 Billion

|

|

Market Growth Rate

|

5.1%

|

|

Segments

|

By Material (Paperboard, Corrugated Board, Molded Pulp), By Product Type (Boxes, Bags, Wraps, Display Packaging, Cardboard Sleeves), By End-Use Industry (Cosmetics & Fragrances, Confectionery & Gourmet Food, Wines & Spirits, Watches & Jewellery, Fashion & Accessories, Electronics)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Smurfit Kappa Group Plc, WestRock Company, International Paper Co., Graphic Packaging Holding Company, Mondi Group, Stora Enso Oyj, DS Smith Plc, Rengo Co., Ltd., Oji Holdings Corporation, GPA Global, Pusterla 1880 S.p.A., IPL Packaging, Hunter Luxury, Keenpac, Cosfibel Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Secondary Paper And Paperboard Luxury Packaging Market Segmentation

By Material

- Paperboard

- Corrugated Board

- Molded Pulp

By Product Type

- Boxes

- Bags

- Wraps

- Display Packaging

- Cardboard Sleeves

By End-Use Industry

- Cosmetics & Fragrances

- Confectionery & Gourmet Food

- Wines & Spirits

- Watches & Jewellery

- Fashion & Accessories

- Electronics

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Secondary Paper And Paperboard Luxury Packaging Market

- Smurfit Kappa Group Plc

- WestRock Company

- International Paper Co.

- Graphic Packaging Holding Company

- Mondi Group

- Stora Enso Oyj

- DS Smith Plc

- Rengo Co., Ltd.

- Oji Holdings Corporation

- GPA Global

- Pusterla 1880 S.p.A.

- IPL Packaging

- Hunter Luxury

- Keenpac

- Cosfibel Group

* List Not Exhaustive

Methodology

USDAnalytics employs a comprehensive research methodology to deliver actionable insights into the global secondary paper and paperboard luxury packaging market. Our approach combines extensive secondary research, including regulatory filings, sustainability reports, corporate press releases, and industry publications, with primary interviews involving luxury brand packaging managers, converters, material suppliers, and technology solution providers. Market sizing and forecasting consider segmentation by material (paperboard, corrugated board, molded pulp), product type (boxes, bags, wraps, display packaging, cardboard sleeves), and end-use industry (cosmetics & fragrances, confectionery & gourmet food, wines & spirits, watches & jewellery, fashion & accessories, electronics), while incorporating regional dynamics such as EU PPWR and ESPR, U.S. EPR laws, China’s green packaging incentives, Japan’s Plastic Resource Circulation Strategy, India’s traceability regulations, and Brazil’s PNRS. Our methodology evaluates key trends including sustainability initiatives, high-performance molded fiber inserts, smart and NFC-enabled packaging, digital printing for hyper-personalization, and luxury aesthetic innovations. Competitive landscape analysis examines strategic acquisitions, mergers, and product innovations by leading players such as Smurfit Kappa, WestRock, International Paper, Mondi Group, and Graphic Packaging, enabling industry professionals to identify growth opportunities, regulatory compliance strategies, and market drivers within the evolving luxury packaging ecosystem.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.