Electrification, Damage Prevention, and Reusable Solutions Push Automotive Parts Packaging Market to USD 16.3 Billion by 2034

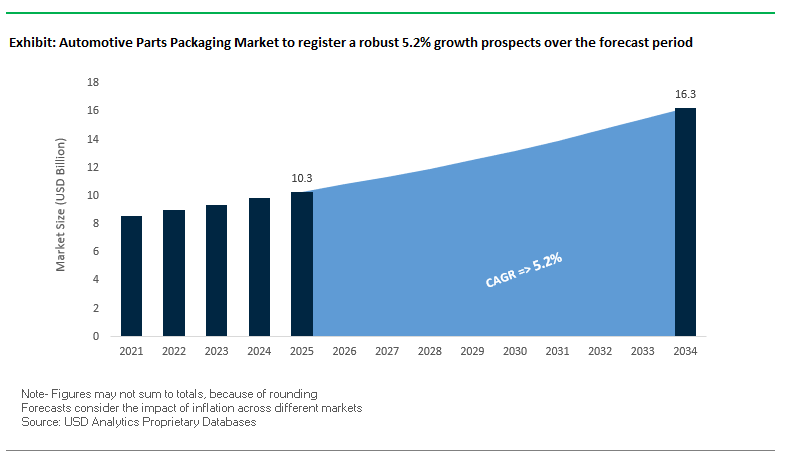

The global automotive parts packaging market is valued at USD 10.3 billion in 2025 and is projected to reach USD 16.3 billion by 2034, advancing at a steady CAGR of 5.2%. The increasing electrification of vehicles has made electrostatic discharge (ESD) protection critical for microchips, sensors, and power electronics. Even a few volts of static discharge can irreversibly damage high-value automotive electronics, making anti-static packaging a non-negotiable requirement for suppliers.

The high cost of damaged components during transit is another major factor driving demand for specialized packaging solutions. With global supply chains stretching across continents, ensuring that engines, drivetrains, sensors, and electronics arrive intact is a financial imperative for OEMs and tier suppliers. In parallel, the automotive industry is accelerating the adoption of reusable and returnable packaging formats, such as collapsible plastic crates and metal racks. These solutions not only cut packaging waste but also support circular economy goals while reducing long-term logistics costs.

Finally, the rise of electric vehicles (EVs) introduces highly specialized requirements. Components such as lithium-ion batteries require packaging that is impact-resistant, thermally insulated, and compliant with international transport regulations. This is reshaping the design and material choices for automotive packaging, pushing innovation toward safety, durability, and sustainability.

Key Insights for Industry Professionals

- ESD protection is vital for safeguarding sensitive automotive electronics.

- Damage prevention through shock- and vibration-resistant packaging reduces costly part failures.

- Reusable packaging is becoming standard for cost savings and sustainability.

- EV battery packaging demands specialized, regulation-compliant, and thermally safe formats.

Mergers, Digitalization, and Sustainable Packaging Redefine Automotive Parts Packaging Landscape

The automotive parts packaging market has seen a series of strategic expansions and technology-driven developments in recent years. In August 2025, Smurfit WestRock debuted in New York and London following its high-profile merger, creating a global leader in paper-based packaging solutions with increased capabilities for automotive supply chains. That same month, S&P Global Mobility expanded its investment in digital automotive intelligence, highlighting the growing role of data-driven insights in optimizing supply chain logistics and packaging efficiency.

In July 2025, International Paper’s acquisition of DS Smith created a new leader in sustainable paper-based packaging, expanding its reach across automotive logistics and aftermarket parts. Around the same time, University of Akron researchers and the U.S. Army developed a novel antimicrobial textile coating with potential applications in automotive interiors and protective component packaging for defense vehicles.

Collaborations have also driven innovation. BMW Group Plant Dingolfing and Landshut University (October 2024) developed an AI-powered digital tool for automating empty container counting, streamlining reusable packaging operations. Earlier, in September 2024, BMW launched the PAL973 single-use paper box, designed for container optimization and safe transport of sensitive automotive parts. In parallel, Pregis (May 2025) expanded its EVOH barrier film capacity, offering cross-industry solutions that can be adapted for anti-static automotive packaging.

Emerging Trends Transforming the Automotive Parts Packaging Market

Strategic Shift Towards Reusable Packaging Systems (RPS) and Closed-Loop Logistics

One of the most defining trends in the automotive parts packaging market is the large-scale transition from disposable, single-use packaging toward reusable packaging systems (RPS) and closed-loop logistics. Automotive OEMs and Tier-1 suppliers are investing heavily in standardized, trackable containers and racks to cut packaging waste, reduce operational costs, and improve supply chain efficiency. A case study highlights how a reusable packaging model eliminated 22,000 tonnes of cardboard waste and reduced CO₂ emissions by 18,000 tonnes, marking a 59% decrease compared to disposable packaging. Global OEMs like General Motors, which reuses or recycles nearly 97% of waste across 90+ landfill-free facilities, are demonstrating the operational and sustainability benefits of reuse-driven systems. Similarly, Ford has pioneered transcontinental closed loops between Europe, South Africa, and the Americas, proving the scalability of this model. Furthermore, the integration of IoT sensors and RFID tags into reusable containers enhances real-time asset visibility, ensuring parts are tracked across return flows. This transformation positions reusable packaging not only as a sustainability milestone but as a cost-effective, technology-enabled standard in automotive logistics.

Adoption of Smart & Connected Packaging for Enhanced Traceability and Damage Prevention

The adoption of smart packaging solutions is accelerating as automotive manufacturers face rising risks of in-transit part damage and theft, particularly for high-value components like EV batteries and ADAS modules. Smart packaging, powered by IoT sensors, RFID tags, and QR codes, provides real-time data on shock, temperature, humidity, and location, ensuring that fragile and costly parts are delivered intact. Studies highlight that real-time visibility allows logistics providers to identify high-risk routes, detect handling issues, and prevent future losses through data-backed interventions. With the EU emphasizing resilience and sustainability in its economy, smart packaging’s “digital twin” technology is becoming a critical enabler for predictive logistics. Logistics firms are even introducing shipment “health scores” that predict risks before they occur, enabling proactive rerouting or protective measures. This shift is transforming packaging from a passive container into an active supply chain intelligence system, helping companies save billions in replacement costs and production downtime.

Opportunities Driving Growth in the Automotive Parts Packaging Industry

Development of High-Performance Sustainable Cushioning Materials

A major growth opportunity in the automotive parts packaging industry lies in the development of next-generation cushioning materials that balance sustainability with high-performance protection. With increasing regulations phasing out plastic foams like EPS, packaging manufacturers are innovating with bio-based, compostable, and recyclable materials derived from mushrooms, agricultural waste, and recycled pulp. For example, molded pulp engineered with advanced compression strength now rivals EPS in shock absorption and durability, making it suitable for fragile parts such as sensors and ECUs. Automotive suppliers are collaborating with packaging firms to conduct rigorous vibration and drop tests to validate performance in real-world shipping. Beyond compliance with sustainability mandates, these materials open a high-value niche market for eco-friendly cushioning solutions, helping OEMs reduce landfill waste while maintaining component protection standards. This evolution represents a dual advantage meeting environmental goals while unlocking new revenue streams for packaging innovators.

Packaging Optimization for the Aftermarket and E-commerce Channel

The surge in online automotive parts sales through platforms like Amazon and RockAuto is creating a fast-growing demand for e-commerce-ready packaging solutions tailored for direct-to-consumer delivery. Unlike bulk dealership shipments, e-commerce packaging must be right-sized to minimize dimensional weight charges, durable enough for parcel handling, and designed to enhance the unboxing experience for consumers. With dimensional weight pricing directly influencing costs, OEMs and aftermarket suppliers are prioritizing optimized packaging designs that reduce excess volume while ensuring protection for irregularly shaped auto parts. At the same time, branded packaging solutions such as custom-molded pulp inserts, printed boxes, and easy-open features are being adopted to reinforce brand image and consumer trust. As online sales continue to expand, this segment offers packaging companies a lucrative opportunity to differentiate their offerings, blending cost efficiency, protection, and premium branding to meet the evolving demands of automotive e-commerce.

Global Leaders Compete Through Sustainable Packaging, Anti-static Solutions, and Automotive-focused Innovations

The competitive landscape of the automotive parts packaging market is defined by global leaders in paper, protective, and specialty packaging. Companies are differentiating themselves through M&A activity, circular economy strategies, and high-performance product innovations tailored to automotive supply chains.

Smurfit WestRock: Expanding Automotive Reach with Paper-based Anti-static Solutions

Following its August 2025 merger, Smurfit WestRock operates in 42 countries with extensive corrugated packaging capabilities. Its automotive portfolio includes VCI-treated corrugated boxes that prevent corrosion of metal components during long-distance transit. With sustainability at its core, the company is positioned as a major partner for OEMs seeking paper-based, recyclable packaging tailored to sensitive parts.

Sealed Air Corporation: Protective Packaging Leader with Anti-static Foam and Cushioning

Rebranded as SEE in 2023, Sealed Air provides Bubble Wrap cushioning and Instapak foam systems with static dissipative properties, widely used for automotive electronics. The company leverages its global R&D network and expertise in protective packaging to deliver sustainable, high-performance solutions that enhance supply chain safety and efficiency for automotive manufacturers.

Pregis LLC: Driving Sustainability with Recycled-content Anti-static Films

Pregis offers a wide range of ESD-protective cushioning, void-fill, and foam systems. Its AirSpeed Renew line, featuring at least 30% recycled or renewable content, represents its commitment to sustainability while delivering high protective performance. By helping automotive customers cut costs and minimize product damage, Pregis positions itself as a key innovator in returnable and disposable protective packaging formats.

Mondi Group: Enhancing Automotive Logistics with Sustainable Corrugated Solutions

Mondi supports automotive supply chains with corrugated transport packaging and custom container solutions. Its recent innovations include tamper-proof printed packaging and collapsible pallets that optimize warehouse storage and logistics efficiency. Mondi’s vertical integration and focus on material-neutral solutions give it a competitive edge in providing durable and lightweight automotive packaging.

DS Smith plc: Scaling Global Automotive Packaging Through International Paper Acquisition

With its July 2025 acquisition by International Paper, DS Smith has expanded its global presence, offering anti-static boxes and sustainable corrugated packaging for automotive applications. Its circular business model, focused on reducing waste and maximizing recyclability, is aligned with the automotive industry’s push toward sustainability. DS Smith’s integrated model from paper production to recycling strengthens its ability to serve multinational automotive OEMs.

Automotive Parts Packaging Market Share Insights

Reusable Packaging Dominates Automotive Parts Packaging Market Share by Type

Reusable packaging has emerged as the dominant type in automotive parts packaging, accounting for 58% of the market in 2025. The adoption of returnable transit containers, plastic totes, and metal racks reflects the industry’s commitment to sustainability and cost efficiency, providing long-term savings and robust protection for high-value components in automated supply chains. Expendable packaging, though secondary, remains essential for export markets, low-volume production, and aftermarket parts distribution where reverse logistics of reusables are impractical. The balance between these two types underscores the automotive sector’s dual priorities of circular economy practices and global logistics flexibility.

Powertrain and Electronics Drive Market Share by Application in Automotive Parts Packaging

Among applications, powertrain and drivetrain components hold the largest share at 25%, reflecting the need for rugged, precision-engineered packaging to safeguard engines, transmissions, and other heavy, high-value parts against corrosion and micro-damage. Electronics follow closely at 22%, representing the fastest-growing application as electrification and autonomous technologies drive demand for protective packaging with electrostatic discharge (ESD) control and cushioning. Interior components, chassis, suspension, and vehicle body parts collectively contribute significant volume, each requiring tailored solutions to prevent scratches, rust, or structural damage during transit. The “others” category, including fluids, batteries, and miscellaneous fasteners, highlights the diversity of packaging requirements across the automotive value chain. Together, powertrain reliability and electronics innovation remain the leading forces shaping application-level packaging demand.

United States: Regulatory Standards and EV Growth Reshape Automotive Parts Packaging

The U.S. automotive parts packaging market is heavily influenced by strict regulatory oversight from the National Highway Traffic Safety Administration (NHTSA) and the U.S. Environmental Protection Agency (EPA), which set safety, emissions, and fuel efficiency standards that indirectly impact packaging design. This regulatory environment pushes manufacturers to innovate packaging that can handle more complex components while aligning with compliance standards. Additionally, sustainability has become a cornerstone of packaging strategies, with companies embracing reusable and returnable packaging systems to cut costs and reduce waste. Materials such as corrugated cardboard and engineered foams are increasingly replacing polystyrene, ensuring recyclability while maintaining product protection.

Another key trend in the U.S. is the expansion of aftermarket and electric vehicle (EV) applications, which require highly specialized packaging for batteries, electronic modules, and replacement parts. The growth of the EV sector has fueled demand for shock-resistant, insulated packaging that guarantees safety during transit. At the same time, supply chain dynamics shaped by the United States-Mexico-Canada Agreement (USMCA) are encouraging nearshoring, which is influencing packaging choices to ensure efficiency in cross-border logistics. Federal and state incentives for clean technology are also accelerating the development of innovative packaging solutions tailored to next-generation automotive components.

China: Green Transformation and Domestic Manufacturing Power Automotive Packaging

China’s automotive parts packaging market is undergoing a green transformation under the government’s “dual carbon” strategy, which promotes eco-friendly, reusable, and recyclable materials across the industrial value chain. The rapid adoption of EVs and hybrid vehicles has intensified the demand for specialized packaging for batteries and high-voltage components, positioning packaging as a critical enabler in China’s EV leadership. Regulatory reforms targeting over-packaging are reshaping packaging design to prioritize efficiency, cost savings, and sustainability.

The market is also witnessing technological disruption through automation and AI integration, with “5G plus industrial internet” driving flexible and high-speed packaging solutions. The government’s “Made in China 2025” strategy further emphasizes domestic substitution, pushing local manufacturers to lead in advanced automotive parts and their packaging. Joint ventures, such as collaborations between Ashok Leyland and CALB Group, highlight how partnerships are spurring innovation in packaging for next-generation batteries. With the world’s largest automotive production and sales base, China’s packaging market is anchored by both OEM demand and the thriving aftermarket, making efficiency, safety, and sustainability top priorities.

Germany: Circular Economy Leadership Drives Packaging Innovation

Germany’s automotive parts packaging market is shaped by the EU Packaging and Packaging Waste Regulation (PPWR), which mandates that all packaging must be fully recyclable or reusable by 2030. This stringent framework, combined with Germany’s Packaging Act (VerpackG), places responsibility for packaging waste management squarely on producers, accelerating the adoption of circular economy practices. As a result, German manufacturers are investing in reusable crates, recyclable containers, and lightweight packaging solutions to meet both domestic and EU-wide sustainability goals.

Technological innovation is another defining characteristic of the German market, where companies are pioneering Vapour Corrosion Inhibitor (VCI) technology to protect metal parts during transit, particularly for exports. The market is especially strong in high-value automotive components such as engines, transmissions, and electronic systems, which require packaging that balances strength, corrosion resistance, and compliance with recycling systems. Backed by significant R&D investments and public-private collaborations, Germany continues to act as a global hub for the development of lighter, stronger, and sustainable packaging materials that align with its leadership in advanced automotive manufacturing.

India: Policy Incentives and Export Growth Propel Packaging Demand

India’s automotive parts packaging market is being reshaped by government programs such as the “Make in India” initiative and the Production-Linked Incentive (PLI) scheme, which allocates over USD 3 billion to promote advanced automotive technology manufacturing. These policies are fueling a surge in EV component production, necessitating advanced packaging for batteries, sensors, and delicate high-value parts. Regulatory oversight from bodies such as the Ministry of Textiles and CDSCO also indirectly influences material quality and safety in automotive packaging.

Technological adoption is another major trend, with manufacturers deploying automated packaging systems, traceability technologies, and precision packaging designs to meet rising quality expectations. India is also emerging as a global export hub under the China+1 strategy, as global OEMs diversify supply chains. This expansion requires robust, export-ready packaging that can withstand long-haul international shipping. Strategic collaborations, such as joint ventures between Indian firms and Chinese battery makers like CALB Group, are strengthening the country’s role in advanced automotive packaging. Backed by growing investments in infrastructure and EV production plants, India is positioned as a fast-growing hub for sustainable, reliable, and cost-efficient automotive packaging solutions.

Japan: Precision Manufacturing and Automation Define Packaging Standards

Japan’s automotive parts packaging market reflects the country’s leadership in precision manufacturing and lightweighting technologies. Packaging is being optimized with lighter yet durable materials that support the broader automotive industry’s focus on fuel efficiency and emissions reduction. The government’s emphasis on supply chain security and high-quality standards further drives the demand for tailored packaging solutions, particularly for electronics, semiconductors, and EV components.

Corporate giants such as Denso Corporation and Aisin Corporation are setting benchmarks in innovative packaging by investing in advanced solutions tailored to specific parts. Automation plays a crucial role, with Japan’s highly automated manufacturing and logistics systems requiring packaging designed for seamless integration with robotic handling. Additionally, academic and research institutions are pioneering the use of smart materials and sustainable alternatives to meet both functional and environmental goals. With a strong culture of collaboration between industry and academia, Japan continues to lead in creating next-generation automotive parts packaging solutions that balance precision, efficiency, and sustainability.

Automotive Parts Packaging Market Report Scope

Automotive Parts Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$10.3 Billion

|

|

Market Size (2034)

|

$16.3 Billion

|

|

Market Growth Rate

|

5.2%

|

|

Segments

|

By Packaging Type (Expendable, Reusable), By Material Type (Plastics, Paper & Paperboard, Wood, Metal, Others), By Application (Powertrain & Drivetrain, Vehicle Body, Electronics, Interior Components, Chassis & Suspension, Others), By End-User (OEMs, Aftermarket), By Product Type (Heavy Parts, Medium Parts, Small Parts)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Smurfit Kappa Group, Mondi Group, DS Smith Plc, WestRock Company, International Paper Company, Nefab AB, Sonoco Products Company, Pregis LLC, Sealed Air Corporation, Huhtamäki Oyj, Menasha Corporation, Amcor plc, Greif, Inc., Shurtape Technologies, LLC, Uline

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Automotive Parts Packaging Market Segmentation

By Packaging Type

By Material Type

- Plastics

- Paper & Paperboard

- Wood

- Metal

- Others

By Application

- Powertrain & Drivetrain

- Vehicle Body

- Electronics

- Interior Components

- Chassis & Suspension

- Others

By End-User

By Product Type

- Heavy Parts

- Medium Parts

- Small Parts

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Automotive Parts Packaging Market

- Smurfit Kappa Group

- Mondi Group

- DS Smith Plc

- WestRock Company

- International Paper Company

- Nefab AB

- Sonoco Products Company

- Pregis LLC

- Sealed Air Corporation

- Huhtamäki Oyj

- Menasha Corporation

- Amcor plc

- Greif, Inc.

- Shurtape Technologies, LLC

- Uline

* List Not Exhaustive

Methodology

USDAnalytics employs a comprehensive and industry-focused research methodology to deliver actionable insights into the global automotive parts packaging market. Our approach combines primary research, including interviews with automotive OEMs, tier suppliers, packaging manufacturers, and industry regulators, with extensive secondary research derived from verified company reports, trade journals, patents, and news sources. Market sizing, growth projections, and forecasts are generated using proprietary quantitative models that account for electrification trends, ESD-sensitive component protection, reusable packaging adoption, and global supply chain dynamics. Competitive intelligence focuses on strategic mergers, digitalization initiatives, sustainability-driven innovations, and new material developments by leading companies such as Smurfit WestRock, Pregis, Sealed Air, and DS Smith. Regional analysis spans major markets including the U.S., Germany, China, India, and Japan, emphasizing regulatory frameworks, technological adoption, and evolving demand in both OEM and aftermarket channels. USDAnalytics ensures all data points are triangulated across multiple credible sources, providing industry professionals with precise, insightful, and actionable guidance on cost optimization, risk mitigation, and sustainable packaging strategies.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.