Market Overview: Expanding Role of Contract Packagers in Consumer Goods

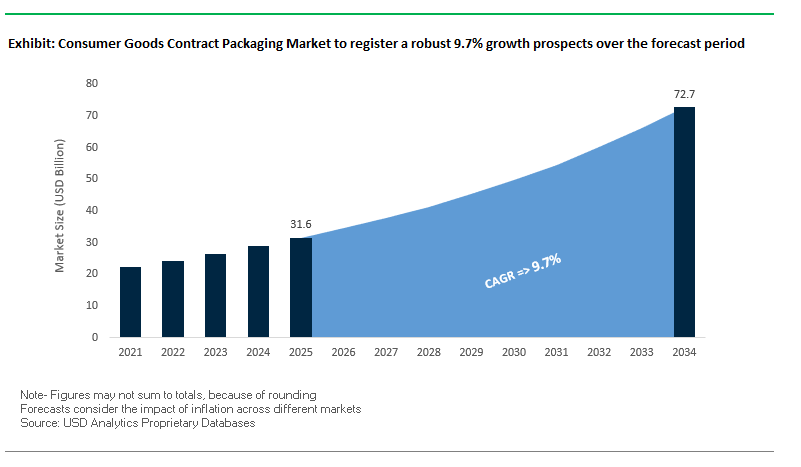

The Consumer Goods Contract Packaging Market is forecasted to reach USD 31.6 billion in 2025 and expand to USD 72.7 billion by 2034, growing at a CAGR of 9.7%. The expansion is propelled by the rising demand for flexible outsourcing solutions, where consumer goods companies partner with contract packagers to reduce operational risks, accelerate speed-to-market, and adopt sustainable packaging strategies. For industry professionals, the critical question is how contract packaging partners can deliver operational agility, zero quality incidents, and sustainability integration while enhancing traceability and brand protection.

The market is undergoing a transformation as brands prioritize agility, safety, and sustainability. Mid-sized brands are increasingly seeking packagers that provide modular production systems, enabling shorter runs and market-testing agility. Furthermore, real-time data transparency, logistics integration, and recall readiness are becoming core expectations beyond the packaging line. The emphasis on net-zero commitments from more than 60% of consumer packaged goods (CPG) brands is also shaping investment in energy-efficient equipment, recyclable monomaterial packaging, and biodegradable alternatives.

Key Insights for Professionals:

- Operational agility reduces time-to-market by 20–30%, giving mid-sized brands a competitive edge.

- Zero quality incidents is emerging as the new industry benchmark, supported by digital monitoring and rigorous training.

- Sustainability pressures are reshaping the industry, with monomaterials, biodegradable films, and energy-efficient processes leading the change.

- Contract packaging has evolved from simple assembly to full-service providers offering logistics, traceability, and data integration.

- Global packagers with automation, modular production, and digital transparency are best positioned to meet growing client expectations.

Market Analysis: Recent Industry Developments Shaping Growth

The market is being significantly shaped by digitalization, mergers, and sustainable material launches. In September 2025, a report on 3PL co-packing operations demonstrated how digitalization is now both a defensive and proactive strategy. The study highlighted that companies investing in co-pack software reduced order preparation, inventory tracking, and quality checks, while achieving a 50% faster recall response time a vital advantage for regulatory compliance and consumer trust.

In August 2025, Graphic Packaging International launched its CleanClose™ certified child-resistant paperboard laundry pod packaging, reinforcing the industry-wide pivot toward fiber-based solutions. Shortly after, in July 2025, Kenco announced the creation of its dedicated Contract Packaging Division, strengthening its integrated supply chain service portfolio. Similarly, in May 2025, MRP Solutions was recognized by the NACD as Supplier of the Year, underlining packaging leadership in innovation and supply chain excellence.

Earlier in March 2025, Wonnda spotlighted critical contract packaging trends, including automation, sustainability, and integrated logistics, reflecting a broader push toward digital-first operations. Regulatory oversight also played a role, as seen in January 2025, when the European Commission approved Constantia Flexibles’ acquisition of Aluflexpack, subject to divestiture conditions signaling how competition laws are influencing packaging market consolidation.

Historical developments continue to shape the current landscape. In October 2024, the merger of Smurfit Kappa and WestRock formed Smurfit WestRock, a global leader in paper-based packaging materials that directly influence contract packaging capabilities. In March 2024, Melodea introduced VBseal, a sustainable coating providing resistance against water vapor and oils, designed to replace single-use plastics in food and confectionery packaging.

Key Trends and Emerging Opportunities Driving Growth in the Consumer Goods Contract Packaging Market

Strategic Vertical Integration by Major Contract Packers to Offer E-commerce Fulfillment Services

Leading players in the consumer goods contract packaging market are expanding beyond traditional packaging services to become full-service e-commerce fulfillment partners. This vertical integration encompasses warehousing, pick-and-pack, and last-mile shipping, providing a one-stop solution for digital-native brands. The explosive growth of e-commerce has propelled this trend, as brands increasingly demand seamless end-to-end supply chain solutions to focus on product development and marketing. Companies like Kenco and Atlantic Packaging have exemplified this strategy, integrating contract packaging with distribution and automation services. Atlantic Packaging, for instance, offers turn-key solutions including right-sizing packages, automated fulfillment, and design and sourcing support, creating value-added offerings for e-commerce clients. This trend represents a major growth avenue for contract packaging firms, allowing them to capture a larger share of client spending while positioning themselves as strategic partners rather than single-service vendors.

Rapid Adoption of Right-Sizing and Automated Packaging Robotics to Reduce Material Waste and Shipping Costs

The adoption of automated right-sizing technology is reshaping the consumer goods contract packaging market. By using AI and robotics to create perfectly sized packages for each order, companies can significantly reduce void fill, excess cardboard, and dimensional shipping costs. Over-sized packages, often by as much as 40%, contribute to material waste, higher shipping fees, and poor customer unboxing experiences, making right-sizing solutions highly attractive. Providers like Ranpak are leveraging automated systems that measure product dimensions and produce custom-fit packaging, aligning with client sustainability goals and operational efficiencies. Data shows that right-sizing automation can reduce corrugate usage by an average of 12.5% per order, demonstrating tangible savings and environmental impact. This trend is transforming the value chain, moving from one-size-fits-all packaging toward a customized, data-driven approach that enhances both sustainability and cost-effectiveness.

Specialization in Compliant, Sustainable Packaging for Regulated Segments (e.g., CBD, Cannabis)

The rapidly expanding legal cannabis and CBD markets in North America and Europe present a lucrative opportunity for contract packagers specializing in regulated packaging. Products in this segment require child-resistant (CR), tamper-evident (TE), and environmentally compliant packaging to meet complex state and national regulations. This specialization offers a high barrier to entry, allowing contract packagers to differentiate themselves and command premium pricing. Brands rely on experienced packaging partners to navigate compliance and mitigate risks of product recalls or fines. Moreover, sustainability mandates in certain jurisdictions create a demand for recyclable and compostable packaging solutions, adding a layer of innovation and differentiation for specialized packagers. This opportunity not only expands service offerings but positions contract packagers as trusted regulatory and sustainability partners in high-value, rapidly growing markets.

Development of In-house Testing and Validation Labs for E-commerce Durability

The last-mile delivery of e-commerce products imposes significant stress on packages, leading to product damage and high return costs. Contract packagers investing in in-house testing and validation labs offer a compelling solution by simulating real-world distribution hazards, including drops, compression, and vibrations. For example, Atlantic Packaging’s Packaging Solution Center enables brands to validate packaging performance prior to shipping, ensuring product safety and reducing return rates. With returns representing a significant operating cost for e-commerce brands, contract packagers offering validated packaging solutions enhance brand protection, consumer satisfaction, and operational efficiency. This trend fosters deeper collaboration between contract packagers and clients, transforming packagers into strategic partners integral to the product development and e-commerce fulfillment process.

Competitive Landscape: Leading Companies in Consumer Goods Contract Packaging

The global consumer goods contract packaging industry is marked by strong competition among logistics providers, packaging manufacturers, and specialized co-packers. Companies are expanding their service portfolios, investing in sustainable solutions, and leveraging automation and digital platforms to remain competitive in an industry that demands speed, safety, and sustainability.

Sonoco Products Company expands with sustainable innovation

Sonoco is a global packaging leader serving food, beverage, and personal care industries with rigid paper containers, flexible films, and protective packaging. In July 2025, the company announced a USD 30 million investment in adhesives and sealants production, strengthening its position in flexible packaging. Sonoco’s EnviroSense™ range reinforces its commitment to recyclable solutions, while its global footprint enables single-source packaging partnerships for multinational corporations.

DHL Supply Chain strengthens digital-first packaging services

DHL Supply Chain has expanded its contract packaging capabilities in North America as of September 2025, emphasizing sustainable and cost-effective solutions. Its integration of automation and digital transformation enhances service efficiency while meeting customer sustainability goals. DHL’s strength lies in its global supply chain expertise, allowing it to offer end-to-end packaging and logistics solutions that align with fast-changing consumer markets.

Assemblies Unlimited Inc. focuses on flexible fulfillment solutions

Assemblies Unlimited provides a wide range of services including primary/secondary packaging, shrink wrapping, and club store packaging across North America. The company emphasizes sustainable materials and lightweighting innovations to enhance environmental performance. By combining continuous improvement with customizable packaging formats, Assemblies Unlimited supports both food and industrial clients with scalable, supply chain-ready packaging solutions.

Aaron Thomas Company Inc. leverages North American market strength

Aaron Thomas Company specializes in blending, filling, primary and secondary packaging, and kitting services. Its operations are deeply rooted in North America, offering tailored services across diverse industries. The company’s investments in sustainable packaging materials and efficiency-focused technologies ensure alignment with evolving customer demands while reinforcing its position as a trusted co-packing partner in the region.

Jones Packaging Inc. launches fully recyclable folding cartons

Jones Packaging delivers labeling, folding cartons, and design services for healthcare, food, and consumer goods industries. In July 2025, the company launched 100% recycled paperboard folding cartons, positioning itself as a pioneer in eco-friendly packaging innovation. With integrated manufacturing and design capabilities, Jones Packaging provides clients with single-source, sustainable, and innovative solutions, strengthening its competitive advantage.

Consumer Goods Contract Packaging Market Share Insights

Primary Packaging Commands Market Share by Service Type in Consumer Goods Contract Packaging

Primary packaging holds the clear lead (45% share) because it delivers the highest value density filling, sealing, and labeling the saleable unit where product integrity, GMP/QA, and brand equity converge. Outsourcing these capital-intensive, format-specific operations lets brand owners scale quickly for promotions, seasonal spikes, and SKU proliferation without adding lines or validation burden. Contract packagers win here by combining specialized fillers (for viscous, particulate, aerosol, and sterile formats), rapid changeovers, and digital serialization/vision systems that compress time-to-market. Secondary packaging follows as e-commerce and omnichannel retail drive shelf-ready packs, kitting, and multipacks; tertiary packaging remains a smaller but essential logistics layer, bundled by full-service co-packers to optimize pallet efficiency, damage reduction, and total landed cost.

Food & Beverages Leads Market Share by End-Use in Consumer Goods Contract Packaging

Food & beverages (40%) is the anchor end-use because of unmatched volume, short shelf life, and the compliance load (HACCP/SQF) that makes outsourced co-packing economical. Contract partners enable portion control, variety packs, and retail-ready displays while safeguarding cold-chain and allergen segregation. Homecare & personal care relies heavily on contract packaging for high-mix, fast-refresh portfolios bundles (shampoo/conditioner), premium finishes, and aerosol handling where aesthetic accuracy and speed to shelf matter. Pharmaceuticals & medical is a smaller but premium niche driven by cGMP/ISO 13485, sterile kit assembly, and mandated serialization; electronics growth centers on protective secondary/tertiary systems (anti-static, custom foam, clamshells) that cut in-transit damage for high-value SKUs.

United States Consumer Goods Contract Packaging Market Accelerated by EPR Regulations and Automation

The U.S. consumer goods contract packaging market is navigating a fragmented regulatory environment, with recent Extended Producer Responsibility (EPR) bills shifting recycling and waste management responsibilities to producers. This has driven consumer packaged goods (CPG) companies to partner with co-packers proficient in sustainable materials and efficient recycling processes. Technological advancements in automation and robotics are central to addressing labor shortages and increasing production efficiency. High-volume, high-mix production is being supported by automation-ready secondary packaging lines, with some companies achieving up to an 85% reduction in line labor after multi-million-dollar upgrades without compromising output.

Corporate investments underscore the sector’s strategic growth, with firms like GenNx360 Capital Partners expanding specialized packaging capabilities through investments in Nutra-Med Packaging, particularly in the pharmaceutical segment. Key applications span food and beverage, personal care, and e-commerce sectors, where direct-to-consumer (DTC) brands demand flexible, scalable packaging solutions. Sustainability initiatives are accelerating, with companies reformulating grease-resistant papers with clay or plant-based coatings and leveraging public-sector-backed cellulose-based films. Additionally, co-packers are optimizing e-commerce fulfillment through integrated protective, branded, and data-rich packaging solutions, helping retailers reduce last-mile costs and meet rapid delivery expectations.

Germany Consumer Goods Contract Packaging Market Strengthened by Circular Economy Leadership and Industry 4.0 Integration

Germany’s contract packaging market is tightly regulated under the Packaging Act (VerpackG) and the EU Packaging and Packaging Waste Regulation (PPWR), effective February 2025, requiring full recyclability or reusability of all packaging by 2030. Compliance with Extended Producer Responsibility (EPR) systems and the LUCID Packaging Register drives innovation in recyclable packaging design, while the German Supply Chain Act (LkSG) ensures adherence to human rights and environmental standards throughout global supply chains.

Technological innovation is a priority, with increased demand for machinery capable of handling bio-based and sustainable materials. Digitalization initiatives, such as Germany’s Plattform Industrie 4.0, integrate cyber-physical systems and IoT into manufacturing processes, enhancing productivity and operational efficiency. Key applications remain focused on food, beverage, and retail sectors, with growing demand for packaging tailored to organic foods and fresh produce. R&D collaborations are fostering the creation of lighter, stronger, and environmentally friendly packaging solutions, positioning Germany as a leader in sustainable and technologically advanced contract packaging.

China Consumer Goods Contract Packaging Market Propelled by Green Policies and Domestic Manufacturing Expansion

China’s consumer goods contract packaging market is being reshaped by the government’s “dual carbon” goal and the March 2024 “Action Plan for Promoting Large-Scale Equipment Updates and Consumer Goods Replacement,” which encourage the adoption of sustainable materials and recycling practices. Regulatory reforms, including limits on packaging layers, void ratios, and cost, directly impact contract packagers in food and cosmetics sectors, emphasizing sustainability and efficiency.

Technological advancements in automation, AI, and the integration of “5G plus industrial internet” are optimizing production processes and flexible manufacturing capacity. The government also mandates express delivery companies to prioritize eco-friendly, reusable packaging. A significant domestic push is underway to substitute imported technology, with local companies expanding production capacity to meet the surging demand for high-quality, circular packaging solutions. Rapid growth in e-commerce, fresh food, and food delivery industries further drives demand, while China’s substantial patent activity demonstrates its leadership in packaging innovation and research.

Brazil Consumer Goods Contract Packaging Market Advancing Through Regulatory Support and Sustainable Investments

Brazil’s consumer goods contract packaging market is influenced by the National Solid Waste Policy and 2024 legislation banning single-use disposable items, targeting a 2030 deadline for fully compostable or recyclable packaging. Technological advancements, including robotics and AI, are enhancing production efficiency and quality control, with developments in biodegradable films using carboxymethyl cellulose (CMC) from sugarcane bagasse.

Corporate investments highlight market momentum, with Smurfit Westrock committing R$840 million to expand production in Santa Catarina, addressing domestic and international demand for sustainable packaging. Key applications are concentrated in food, beverage, and cosmetics sectors, with Brazil’s expanding food processing industry driving the need for advanced packaging solutions. Government support through FINEP, exemplified by Melhoramentos’ R$40 million investment in a cellulose fiber packaging facility, underscores the nation’s commitment to sustainable manufacturing. The Brazilian market is witnessing rapid growth in eco-friendly contract packaging, powered by technological innovation, corporate investments, and regulatory incentives promoting circular economy practices.

Consumer Goods Contract Packaging Market Report Scope

Consumer Goods Contract Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$31.6 Billion

|

|

Market Size (2034)

|

$72.7 Billion

|

|

Market Growth Rate

|

9.7%

|

|

Segments

|

By Service Type (Primary Packaging, Secondary Packaging, Tertiary Packaging), By End-Use Industry (Food & Beverages, Homecare & Personal Care, Pharmaceuticals & Medical, Electronics, Others), By Packaging Format (Flexible Packaging, Rigid Packaging)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Mondi Group, Smurfit Kappa Group plc, Huhtamaki Oyj, Constantia Flexibles, Sonoco Products Company, DS Smith plc, WestRock Company, Sealed Air Corporation, Silgan Holdings Inc., Berry Global Group, Inc., Assemblies Unlimited Inc., Unicep Packaging, Kenco Logistics Services, Sanner GmbH

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Consumer Goods Contract Packaging Market Segmentation

By Service Type

- Primary Packaging

- Secondary Packaging

- Tertiary Packaging

By End-Use Industry

- Food & Beverages

- Homecare & Personal Care

- Pharmaceuticals & Medical

- Electronics

- Others

By Packaging Format

- Flexible Packaging

- Rigid Packaging

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Consumer Goods Contract Packaging Market

- Amcor plc

- Mondi Group

- Smurfit Kappa Group plc

- Huhtamaki Oyj

- Constantia Flexibles

- Sonoco Products Company

- DS Smith plc

- WestRock Company

- Sealed Air Corporation

- Silgan Holdings Inc.

- Berry Global Group, Inc.

- Assemblies Unlimited Inc.

- Unicep Packaging

- Kenco Logistics Services

- Sanner GmbH

* List Not Exhaustive

Methodology

The Consumer Goods Contract Packaging Market analysis has been conducted by USDAnalytics using a rigorous methodology designed to deliver actionable insights for industry professionals. The study combines primary research interviews with key stakeholders including contract packagers, brand owners, logistics providers, and regulatory authorities with extensive secondary research covering corporate press releases, annual reports, sustainability initiatives, patent filings, industry journals, and regulatory documentation. USDAnalytics analyzed global trends in automation, modular production, right-sizing, sustainable materials, and e-commerce fulfillment integration, while also assessing regional regulatory impacts such as the EU Packaging and Packaging Waste Regulation (PPWR), U.S. Extended Producer Responsibility (EPR) bills, and Brazil’s National Solid Waste Policy. Quantitative modeling was applied to estimate market size, growth rate, and segmentation by service type, end-use industry, and packaging format, while qualitative insights explored emerging opportunities, strategic vertical integration, and technology adoption. The methodology ensures a holistic perspective on operational agility, zero quality incidents, sustainability integration, and digital transparency, providing a comprehensive, forward-looking view of the consumer goods contract packaging market.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.