Market Overview: Rising Demand for Immersed Membrane Bioreactor (iMBR) Systems Driving Growth

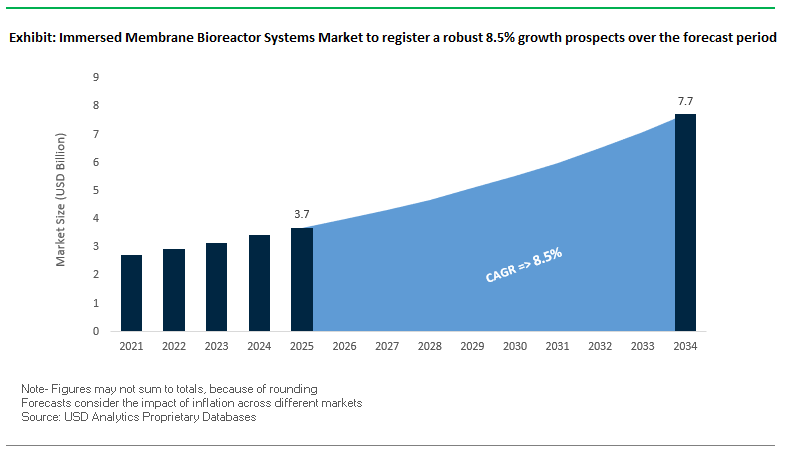

The immersed membrane bioreactor (iMBR) systems market is projected to expand significantly, reaching USD 3.7 billion in 2025 and expected to surpass USD 7.7 billion by 2034, growing at a robust CAGR of 8.5%. The rising global demand for high-quality wastewater treatment, water reuse, and compact treatment technologies in urban environments is fueling the adoption of iMBR systems worldwide.

Unlike conventional activated sludge treatment, iMBR combines biological degradation and membrane filtration in a single, compact unit, delivering superior effluent quality, operational reliability, and reduced sludge production. These advantages make iMBR systems indispensable in municipal wastewater plants, industrial facilities, and water reuse projects.

Key Insights for Buyers and Industry Stakeholders

- Superior Effluent Quality: Produces pathogen- and bacteria-free effluent suitable for water reuse and groundwater replenishment.

- Compact Footprint: Ideal for urban wastewater treatment and retrofitting existing plants where land availability is limited.

- Operational Reliability: Stable treatment performance even under fluctuating influent quality and flow conditions.

- Reduced Sludge Production: Substantial reduction in sludge volumes lowers disposal costs and improves sustainability.

- Sustainability-Driven Growth: iMBR adoption is accelerating due to stringent water reuse regulations and the rising need for climate-resilient water solutions.

Market Analysis: Technological Advancements and Strategic Developments in iMBR Systems

The immersed membrane bioreactor systems industry has witnessed a surge in research, innovation, and strategic partnerships in recent years. A growing number of developments highlight how iMBR systems are being integrated with advanced digital monitoring, renewable energy, and complementary membrane technologies to enhance efficiency.

In August 2025, German students won the Stockholm Junior Water Prize for an innovative flood warning system, underscoring the growing trend toward data-driven water management. Around the same time, researchers published findings on composite nanofiltration membranes enhanced by electrostatic air spray deposition, a breakthrough that could improve membrane hydrophilicity, stability, and separation performance in iMBR systems.

July 2025 marked significant industry activity, with the formation of Acuriant Technologies through the merger of Nanostone Water and Solecta. This consolidation aims to integrate polymeric and ceramic membrane technologies, strengthening the foundation for hybrid iMBR applications. That same month, Veolia unveiled its Memthane® anaerobic MBR system, which not only treats high-strength wastewater but also generates renewable energy in the form of biogas.

Other notable advancements include Meiden Singapore’s demonstration plant (June 2025) using ceramic flat-sheet membranes for SWRO pretreatment, and a May 2025 study highlighting the role of forward osmosis in reducing energy consumption and greenhouse gas emissions, paving the way for hybrid FO-iMBR solutions. Earlier, in January 2025, Toray Industries secured a landmark RO membrane order for Saudi Arabia’s Yanbu 4 IWP desalination project, reinforcing its global role in integrated water treatment technologies.

Trends and Opportunities Driving Growth in the Immersed Membrane Bioreactor Systems Market

Stricter Regulations and Accelerating Push for Water Reuse

One of the defining trends shaping the immersed membrane bioreactor (iMBR) systems market is the global tightening of wastewater discharge norms and the prioritization of water reuse. Governments are mandating industries and residential complexes to treat and recycle water, creating an urgent demand for iMBRs due to their ability to consistently deliver high-quality effluent with low footprint. For example, India’s Ministry of Environment, Forest, and Climate Change recently mandated that bulk consumers treating more than 5,000 liters per day must reuse at least 20% of their wastewater by 2027–28, rising to 50% by 2031. The National Green Tribunal (NGT) has imposed penalties exceeding ₹80,000 crore on states and municipalities for failing to comply, accelerating the adoption of advanced solutions like iMBRs. These policy shifts are reinforcing iMBRs as the technology of choice for compliance and sustainable water management.

Breakthrough Innovations in Membrane Materials and Anti-Fouling Designs

Technological innovation is another major trend bolstering the iMBR systems market. Research in next-generation membranes including photocatalytic coatings and granular sludge integration is reducing fouling, one of the biggest operational challenges for bioreactors. Studies published in ACS Applied Materials & Interfaces show that photocatalytic membranes actively break down organic pollutants under light exposure, reducing chemical cleaning frequency and extending lifespan. Similarly, MDPI reported that integrating granular sludge reduces fouling significantly, lowering operating costs. These advancements are transforming iMBR economics, making them more durable, energy-efficient, and financially viable for both municipal utilities and industries.

Expansion of Decentralized and Modular Wastewater Treatment Systems

A major opportunity lies in the growing adoption of decentralized and modular wastewater treatment systems, particularly in urbanizing regions and remote communities. Immersed MBR systems, with their compact footprint and modular scalability, are ideally suited for decentralized treatment in industrial parks, hotels, and small municipalities that lack centralized sewer systems. A strong example is MANN+HUMMEL’s BIO-CEL M+ Series, a modular iMBR platform designed for decentralized applications. Its plug-and-play scalability allows capacity expansion without overhauling infrastructure, making it a cost-effective and flexible solution for emerging economies and urban areas under pressure.

Rising Adoption in High-Strength Industrial Wastewater Treatment

The industrial wastewater treatment segment presents another critical growth opportunity. Industries such as food and beverage, slaughterhouses, and textiles generate high-strength effluents with high organic loads that conventional systems struggle to treat. iMBRs, however, consistently deliver effluents well within regulatory limits. A study from a leading water technology company demonstrated that an immersed MBR deployed in a slaughterhouse achieved 97% COD removal and 96% TOC reduction, showcasing its ability to handle some of the most challenging effluents. This makes iMBRs indispensable for industries under pressure to comply with environmental laws while also pursuing water reuse and sustainability targets.

Market Share Analysis of the Immersed Membrane Bioreactor Systems Market

Market Share by Membrane Type

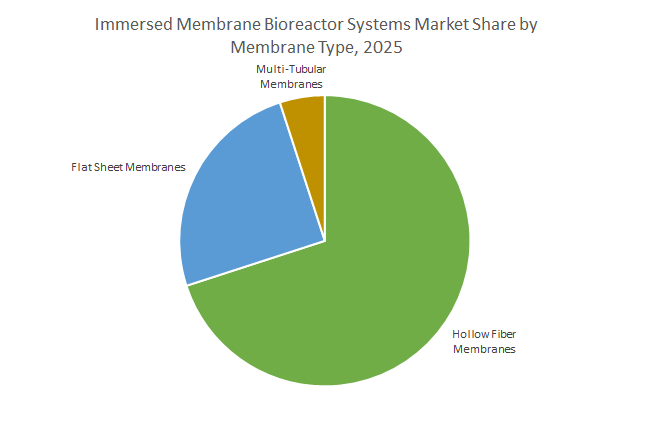

In terms of membrane type, hollow fiber membranes dominate the immersed MBR systems market with 70% projected share in 2025, largely due to their high packing density, which allows maximum membrane surface area in a compact footprint. This makes them the preferred choice for large-scale municipal wastewater treatment plants and space-constrained industrial projects. Flat sheet membranes account for about 25%, valued for their robustness and resistance to clogging from fibrous or stringy waste. They are commonly deployed in industrial wastewater treatment and smaller facilities where manual cleaning is feasible. Multi-tubular membranes, with only 5% share, are used in niche applications involving extremely high solids or complex industrial waste streams, where their clogging resistance outweighs their high cost and low packing density.

Market Share by System Configuration

By system configuration, the market is heavily dominated by internal submerged systems, projected to hold 85% share in 2025. These systems integrate membranes directly within the biological reactor, combining aeration for biological activity with air scouring to minimize fouling. Their energy efficiency, lower footprint, and simplified design make them the industry standard for both municipal and industrial plants. On the other hand, external submerged systems are expected to capture 15% share, catering to specialized use cases such as retrofitting existing wastewater treatment plants or treating highly variable industrial effluents. While they occupy a smaller share, their ability to offer independent control of biological and filtration processes makes them strategically important for industries with aggressive or inconsistent wastewater profiles.

China: Regulatory Push and Advanced MBR Applications

The China immersed MBR systems market is experiencing robust growth driven by stringent industrial wastewater regulations and government-backed initiatives for water reuse. The Ministry of Ecology and Environment (MEE) enforces strict discharge standards, prompting industries to adopt advanced MBR technologies for compliance. Under the 14th Five-Year Plan, water reuse is a priority, with MBR systems playing a central role in achieving national targets for sustainable water management.

Technological advancements in 2024 include the development of hollow-fiber ultrafiltration membranes with enhanced antifouling properties, aimed at reducing maintenance costs and improving the long-term efficiency of immersed MBR systems. Key industrial applications span zero-liquid discharge (ZLD) systems in textile and petrochemical sectors, where MBRs are valued for their robustness and capacity to handle high-solids-content wastewater. A 2024 report highlighted the widespread adoption of immersed MBR technology in China to tackle water scarcity and industrial pollution.

United States: Federal Funding and Corporate Innovation Driving Adoption

The U.S. immersed MBR systems market benefits from significant government funding and innovation-driven R&D. The Bipartisan Infrastructure Law allocates over $50 billion to the EPA to enhance water infrastructure, with a focus on addressing emerging contaminants such as PFAS, which require advanced MBR filtration solutions.

Academic research funded by the National Science Foundation (NSF) further accelerates innovation in membrane technologies for water purification and chemical separation. Key corporate initiatives include Veolia Water Technologies and Evoqua Water Technologies, which deploy immersed MBR systems for regulated water treatment. In 2024, Koch Separation Solutions launched a new modular MBR product line, simplifying installation and maintenance in municipal and industrial wastewater treatment facilities.

India: Government Missions and Green Bonds Supporting MBR Growth

India’s immersed MBR systems market is expanding rapidly, fueled by government programs such as the Jal Jeevan Mission, which promotes clean water access in rural areas. The Department of Science & Technology (DST) also supports R&D in nano-material and filtration technologies, enhancing the adoption of advanced MBR systems.

Infrastructure investments underscore the market’s growth: the Ghaziabad Nagar Nigam issued India’s first Certified Green Municipal Bond, raising ₹150 crore to fund a Tertiary Sewage Treatment Plant (TSTP) employing immersed MBR technology. Additionally, VA TECH WABAG’s seven-year O&M contract for the 110 MLD SWRO Nemmeli Desalination Plant demonstrates strong financial commitment to maintaining membrane-based water treatment infrastructure, highlighting the increasing reliance on immersed MBR systems for industrial and municipal wastewater reuse.

Germany: Industrial MBR Leadership and Technological Expertise

Germany leads the immersed MBR systems market in Europe through a combination of regulatory compliance and industrial expertise. Companies like PWT Wassertechnik specialize in industrial wastewater treatment, leveraging immersed MBR technology to ensure efficient water reuse while adhering to strict EU environmental standards.

Technological developments are exemplified by Berghof Membranes, which in 2024 expanded its global supply of ceramic tubular membranes for MBR projects. Although tubular, this demonstrates Germany’s focus on robust membrane solutions. Corporate initiatives from MANN+HUMMEL further strengthen the market, combining advanced membrane systems with digital water management solutions to address industrial water challenges and promote green energy initiatives.

Japan: Academic and Corporate R&D Pioneering MBR Innovations

The Japan immersed MBR systems market is distinguished by cutting-edge academic and corporate research. In 2025, Toray introduced a next-generation hollow fiber membrane with 20% higher permeability and reduced fouling, designed to lower operational costs for MBR systems.

The Ministry of the Environment allocated USD 1.2 billion in 2024 to promote sustainable infrastructure, including wastewater treatment systems incorporating MBR technology. Japan’s extensive MBR applications over 3,000 full-scale plants span small-scale industrial and household systems to large municipal facilities. Metawater’s ceramic membrane filtration systems exemplify Japan’s capability in providing clean tap water while enhancing operational efficiency and reducing turbidity, demonstrating the country’s leadership in advanced immersed MBR solutions.

Australia: Water Stress Driving Recycling and Advanced MBR Research

Australia’s immersed MBR systems market is strongly influenced by national water scarcity challenges. The country is a global leader in water recycling and reuse, with initiatives such as the Australian Water Recycling Centre of Excellence funding projects that demonstrate the cost-effectiveness of ceramic membranes for secondary effluent containing high organic matter.

Technological adoption includes the Narromine Shire Council’s innovative water treatment system, featuring next-generation submerged flat-sheet ceramic membrane technology from Cerafiltec. Academic research by Victoria University’s Institute for Sustainable Industries and Liveable Cities (ISILC) is enhancing water recovery from desalination and minimizing fouling and scaling, tackling critical challenges for immersed MBR systems. This positions Australia as a key player in innovative and sustainable membrane-based water treatment solutions.

Competitive Landscape: Leading Players Shaping the Immersed Membrane Bioreactor Market

The global iMBR systems market is highly competitive, with major players driving advancements in membrane innovation, system integration, and large-scale project deployment. Companies are increasingly focusing on energy efficiency, sustainability, and digital monitoring to stay ahead in this fast-growing market.

SUEZ Water Technologies & Solutions: Driving Innovation in iMBR with LEAPmbr Technology

As part of Veolia, SUEZ is a pioneer in immersed membrane bioreactor technology with its LEAPmbr® system. The company integrates advanced treatment processes to deliver reuse-quality effluent, catering to both municipal and industrial applications. Through partnerships like its five-year collaboration with CNRS, SUEZ is advancing research in micropollutant removal and resource recovery. Its expertise in executing large-scale projects, including China’s largest industrial seawater desalination facility, highlights its dominance in the global iMBR systems market.

Kubota Corporation: Pioneering Flat-Sheet Membrane Technology in iMBR Systems

Kubota is widely recognized as the pioneer of flat-sheet membranes in iMBR systems. Its technology delivers robustness, easy maintenance, and resistance to mechanical damage, making it a top choice for municipal wastewater treatment. With a global footprint of MBR installations, Kubota focuses heavily on energy efficiency and compact system design, ensuring its solutions align with the needs of urban wastewater reuse projects.

Toray Industries, Inc.: Advancing Sustainability with High-Performance iMBR Membranes

Toray leverages its polymer science expertise to design long-lasting, fouling-resistant iMBR membranes that reduce operational costs. The company is committed to sustainable innovation, introducing next-generation materials that extend membrane lifespan. With its diverse portfolio of RO, NF, UF, and MF membranes, Toray provides integrated water treatment solutions. Its participation in large-scale desalination projects worldwide reinforces its leadership in the iMBR industry.

Xylem Inc.: Integrating Smart Technologies into Immersed MBR Systems

Xylem is a holistic water solutions provider, offering pumps, mixers, control systems, and advanced iMBR technologies. The company strengthens its market position through strategic acquisitions, such as Baycom in August 2025, which expanded its smart water solutions portfolio. Xylem emphasizes digital integration and predictive maintenance within iMBR systems, while also gaining visibility by supporting global water innovation events like the Stockholm Junior Water Prize.

Ovivo: Focused on Advanced Membrane Technologies for Complex Applications

Ovivo operates across 18 countries, delivering customized wastewater treatment solutions with a strong emphasis on iMBR systems. Its proprietary technologies and integration expertise allow it to address complex industrial water treatment challenges. In August 2025, Ovivo announced the sale of its Electronics division to Ecolab for USD 1.8 billion, enabling it to sharpen its focus on its core water and wastewater business, including advanced iMBR applications.

Koch Separation Solutions (Kovalus): Expanding Integrated Solutions for iMBR Applications

Rebranded as Kovalus Separation Solutions in 2023, following its acquisition by Sun Capital Partners, the company has been strategically enhancing its membrane filtration and separation technologies. Innovations like INDU-COR HD, designed for high packing density and reduced costs, strengthen its presence in wastewater treatment. Kovalus delivers integrated water solutions combining membrane filtration, ion exchange, and evaporation systems, serving industries such as food and beverage, automotive, and life sciences.

Immersed Membrane Bioreactor Systems Market Report Scope

Immersed Membrane Bioreactor Systems Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.7 Billion

|

|

Market Size (2034)

|

$7.7 Billion

|

|

Market Growth Rate

|

8.5%

|

|

Segments

|

By Membrane Type (Hollow Fiber Membranes, Flat Sheet Membranes, Multi-Tubular Membranes), By System Configuration (Internal Submerged Systems, External Submerged Systems), By Application (Municipal Wastewater Treatment, Industrial Wastewater Treatment), By Filtration Mode (Aerobic MBR Systems, Anaerobic MBR Systems), By End-User (Municipal Authorities, Industrial Facilities, Commercial Establishments), By Capacity (Small-Scale (Below 1 MLD), Medium-Scale (1–20 MLD), Large-Scale (Above 20 MLD))

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

SUEZ, Veolia, Kubota Corporation, Toray Industries, Inc., Pentair plc, Xylem Inc., Asahi Kasei Corporation, Mitsubishi Chemical Corporation, Evoqua Water Technologies, The Dow Chemical Company, MANN+HUMMEL, Koch Industries, V.A. TECH WABAG Ltd., Alfa Laval, DuPont de Nemours, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Immersed Membrane Bioreactor Systems Market Segmentation

By Membrane Type

- Hollow Fiber Membranes

- Flat Sheet Membranes

- Multi-Tubular Membranes

By System Configuration

- Internal Submerged Systems

- External Submerged Systems

By Application

- Municipal Wastewater Treatment

- Industrial Wastewater Treatment

- Food & Beverage Industry

- Pharmaceutical & Biotechnology

- Chemicals & Petrochemicals

- Textile & Pulp & Paper

- Power Generation

- Other Industrial Applications

By Filtration Mode

- Aerobic MBR Systems

- Anaerobic MBR Systems

By End-User

- Municipal Authorities

- Industrial Facilities

- Commercial Establishments

By Capacity

- Small-Scale (Below 1 MLD)

- Medium-Scale (1–20 MLD)

- Large-Scale (Above 20 MLD)

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Immersed Membrane Bioreactor Systems Industry include-

- SUEZ

- Veolia

- Kubota Corporation

- Toray Industries, Inc.

- Pentair plc

- Xylem Inc.

- Asahi Kasei Corporation

- Mitsubishi Chemical Corporation

- Evoqua Water Technologies

- The Dow Chemical Company

- MANN+HUMMEL

- Koch Industries

- V.A. TECH WABAG Ltd.

- Alfa Laval

- DuPont de Nemours, Inc.

*- List not Exhaustive

Research Coverage

Produced by USDAnalytics, this report investigates the global Immersed Membrane Bioreactor (iMBR) Systems opportunity from demand drivers to bankability, integrating market sizing, performance benchmarking, and policy catalysts; the analysis reviews configuration choices (internal vs. external submerged), membrane form factors (hollow fiber, flat sheet, multi-tubular), and OPEX levers (aeration, CIP, solids management), and highlights recent breakthroughs in anti-fouling materials, digital monitoring, and hybrid integrations (e.g., FO-iMBR, anaerobic MBR). Leveraging vendor scorecards, deployment evidence, and sensitivity testing on energy and sludge costs, this report is an essential resource for utilities, EPCs, industrial owners, and investors seeking defensible forecasts to 2034, comparative TCO, and practical procurement guidance across municipal and high-strength industrial reuse applications. Scope Includes-

- Segmentation: By Membrane Type (Hollow Fiber Membranes, Flat Sheet Membranes, Multi-Tubular Membranes); By System Configuration (Internal Submerged Systems, External Submerged Systems); By Application (Municipal Wastewater Treatment, Industrial Wastewater Treatment Food & Beverage, Pharmaceutical & Biotechnology, Chemicals & Petrochemicals, Textile & Pulp & Paper, Power Generation, Other Industrial Applications); By Filtration Mode (Aerobic MBR Systems, Anaerobic MBR Systems); By End-User (Municipal Authorities, Industrial Facilities, Commercial Establishments); By Capacity (Small-Scale (Below 1 MLD), Medium-Scale (1–20 MLD), Large-Scale (Above 20 MLD)).

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Companies (Profiles of 15+ companies): SUEZ; Veolia; Kubota Corporation; Toray Industries, Inc.; Pentair plc; Xylem Inc.; Asahi Kasei Corporation; Mitsubishi Chemical Corporation; Evoqua Water Technologies; The Dow Chemical Company; MANN+HUMMEL; Koch Industries; V.A. TECH WABAG Ltd.; Alfa Laval; DuPont de Nemours, Inc.

Methodology

USDAnalytics applied a mixed top-down/bottom-up approach: we built demand trees by end-market and capacity band, reconciled with country-level project trackers and awards, and validated with 40+ stakeholder interviews (utilities, EPCs, OEMs, operators). Techno-economic models normalize flux, SRT/MLSS, aeration set-points, cleaning frequency, energy (kWh/m³), chemicals, and sludge hauling to derive TCO and LCOwater across aerobic and anaerobic iMBR. Vendor benchmarking scores membranes on packing density, fouling rebound, permeability at temperature, and mechanical robustness; scenario analysis stress-tests energy inflation, effluent-limit tightening, and hybrid add-ons (e.g., RO/FO polishing). Forecasts use cohort adoption curves, replacement cycles, and sensitivity bands, with consistency checks against historic spend and policy pipelines.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Immersed Membrane Bioreactor (iMBR) Systems Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Insights for Buyers and Industry Stakeholders

1.3. Global Market Snapshot

2. Immersed Membrane Bioreactor Systems Market Outlook (2025–2034)

2.1. Market Overview: Rising Demand for iMBR Systems Driving Growth

2.2. Market Valuation and Growth Projections (2025–2034)

2.2.1. Current Market Size (2025): USD 3.7 Billion

2.2.2. Forecasted Market Size (2034): USD 7.7 Billion

2.2.3. Projected Compound Annual Growth Rate (CAGR): 8.5%

2.3. Key Trends and Opportunities

2.3.1. Stricter Regulations and Accelerating Push for Water Reuse

2.3.2. Breakthrough Innovations in Membrane Materials and Anti-Fouling Designs

2.3.3. Expansion of Decentralized and Modular Wastewater Treatment Systems

2.3.4. Rising Adoption in High-Strength Industrial Wastewater Treatment

3. Recent Developments: Technological Advancements and Strategic Developments

3.1. Market Analysis: Key Innovations and Strategic Activities

3.1.1. German Students Win Stockholm Junior Water Prize (August 2025)

3.1.2. Researchers Publish Findings on Nanofiltration Membranes (August 2025)

3.1.3. Acuriant Technologies Formed by Merger of Nanostone Water and Solecta (July 2025)

3.1.4. Veolia Unveils Memthane® Anaerobic MBR System (July 2025)

3.1.5. Meiden Singapore Demonstrates Ceramic Flat-Sheet Membranes (June 2025)

3.1.6. Toray Secures RO Membrane Order for Saudi Arabia Desalination Project (January 2025)

4. Competitive Landscape: Leading Players

4.1. Market Overview: From Technology Pioneers to Integrated Solution Providers

4.2. Key Competitive Factors

4.2.1. Membrane Innovation and System Integration

4.2.2. Focus on Energy Efficiency and Sustainability

4.2.3. Digital Monitoring and Smart Technologies

4.3. Profiles of Key Players

4.3.1. SUEZ Water Technologies & Solutions

4.3.2. Kubota Corporation

4.3.3. Toray Industries, Inc.

4.3.4. Xylem Inc.

4.3.5. Ovivo

4.3.6. Koch Separation Solutions (Kovalus)

5. Immersed Membrane Bioreactor Systems Market – Segmentation Insights

5.1. By Membrane Type

5.1.1. Hollow Fiber Membranes

5.1.2. Flat Sheet Membranes

5.1.3. Multi-Tubular Membranes

5.2. By System Configuration

5.2.1. Internal Submerged Systems

5.2.2. External Submerged Systems

5.3. By Application

5.3.1. Municipal Wastewater Treatment

5.3.2. Industrial Wastewater Treatment

5.4. By Filtration Mode

5.4.1. Aerobic MBR Systems

5.4.2. Anaerobic MBR Systems

5.5. By End-User

5.5.1. Municipal Authorities

5.5.2. Industrial Facilities

5.5.3. Commercial Establishments

5.6. By Capacity

5.6.1. Small-Scale (Below 1 MLD)

5.6.2. Medium-Scale (1–20 MLD)

5.6.3. Large-Scale (Above 20 MLD)

6. Country Analysis and Outlook: iMBR Systems Market

6.1. China: Regulatory Push and Advanced MBR Applications

6.2. United States: Federal Funding and Corporate Innovation

6.3. India: Government Missions and Green Bonds Supporting MBR Growth

6.4. Germany: Industrial MBR Leadership and Technological Expertise

6.5. Japan: Academic and Corporate R&D Pioneering MBR Innovations

6.6. Australia: Water Stress Driving Recycling and Advanced MBR Research

6.7. Other Key Countries Analyzed

6.7.1. North America (Canada, Mexico)

6.7.2. Europe (UK, France, Spain, Italy, Russia, Rest of Europe)

6.7.3. Asia Pacific (South Korea, South East Asia, Rest of Asia)

6.7.4. South America (Brazil, Argentina, Rest of South America)

6.7.5. Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

7. Immersed Membrane Bioreactor Systems Market Size Outlook by Region (2025-2034)

7.1. North America Market Size Outlook to 2034

7.1.1. By Membrane Type

7.1.2. By System Configuration

7.1.3. By Application

7.2. Europe Market Size Outlook to 2034

7.2.1. By Membrane Type

7.2.2. By System Configuration

7.2.3. By Application

7.3. Asia Pacific Market Size Outlook to 2034

7.3.1. By Membrane Type

7.3.2. By System Configuration

7.3.3. By Application

7.4. South America Market Size Outlook to 2034

7.4.1. By Membrane Type

7.4.2. By System Configuration

7.4.3. By Application

7.5. Middle East and Africa Market Size Outlook to 2034

7.5.1. By Membrane Type

7.5.2. By System Configuration

7.5.3. By Application

8. Company Profiles: Additional Leading Players

8.1. SUEZ

8.2. Veolia

8.3. Kubota Corporation

8.4. Toray Industries, Inc.

8.5. Pentair plc

8.6. Xylem Inc.

8.7. Asahi Kasei Corporation

8.8. Mitsubishi Chemical Corporation

8.9. Evoqua Water Technologies

8.10. The Dow Chemical Company

8.11. MANN+HUMMEL

8.12. Koch Industries

8.13. V.A. TECH WABAG Ltd.

8.14. Alfa Laval

8.15. DuPont de Nemours, Inc.

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures