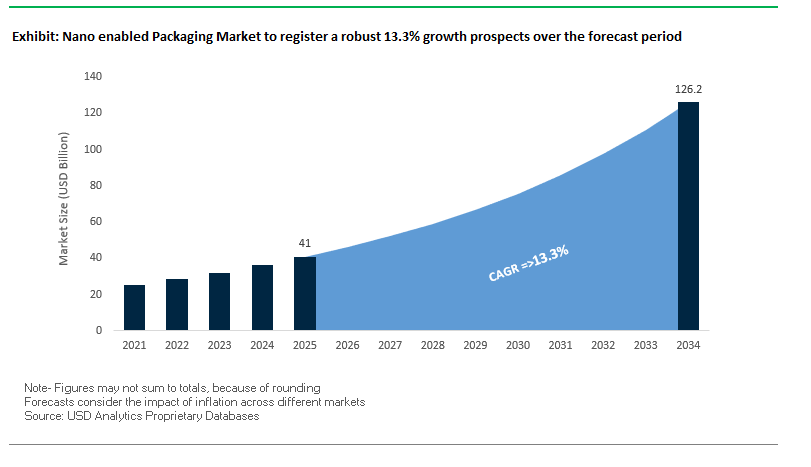

Nano-Enabled Packaging Market to Surge to $126.1 Billion by 2034 at 13.3% CAGR

The global nano-enabled packaging market is projected to grow from $41 billion in 2025 to $126.1 billion by 2034, achieving a CAGR of 13.3%. The market is driven by the rapid adoption of nanotechnology in food, beverage, and pharmaceutical packaging, the rise of intelligent packaging solutions, and a growing emphasis on sustainable and high-barrier materials. Nano-enabled packaging enhances food preservation, reduces spoilage, and provides advanced barrier and antimicrobial properties, making it a critical innovation for manufacturers and brands seeking to extend product shelf life and ensure safety.

Key Insights for Industry Professionals:

- Enhanced food preservation: Nanotechnology extends shelf life and reduces spoilage for perishable products like meat, dairy, and fresh produce.

- Intelligent packaging adoption: Over 40% of intelligent packaging solutions now integrate nanosensors and indicators for real-time monitoring of temperature, humidity, and product quality.

- Advanced barrier performance: Nanoclays, metal oxides, and nanocoatings improve protection against oxygen, moisture, and UV light, reducing food waste.

- Sustainable packaging innovation: Nearly 30% of new sustainable solutions incorporate nanotechnology to enhance biodegradability, recyclability, and material efficiency.

- Cross-industry relevance: Applications extend across food, beverage, pharmaceuticals, and personal care, offering opportunities for high-performance and intelligent packaging solutions.

Recent Developments Driving the Global Nano-Enabled Packaging Industry

The nano-enabled packaging sector has seen significant advancements through technological innovation, strategic partnerships, and sustainability initiatives. In August 2025, a Nano Letters study introduced an inhibitor-modified atomic layer deposition (ALD) strategy for ultrathin iridium and platinum films, a potential breakthrough for high-barrier nanocoatings. In July 2025, metallized film converters invested in wider, faster coating lines to meet growing demand for high-barrier nano-enabled packaging.

In June 2025, Amcor and Cofigeo collaborated to produce a polypropylene-based monomaterial ready meal tray with NIR-detectable masterbatch, demonstrating nanoparticle-enabled sorting and barrier technologies. Harpak’s automated modified atmosphere packaging equipment launched in May 2025, supporting high-volume production of nano-enabled films and trays. In April 2025, Nfinite Nanotechnology and Amcor initiated a joint research project to validate nanocoating technology for improved oxygen barrier performance in recyclable and compostable packaging.

Earlier in February 2025, Packaging Digest reported a surge in demand for sustainable, protective packaging enhancing shelf life, driving adoption of metallized and nano-enabled films. Cirkla’s molded fiber MAP trays launched in January 2025 exemplify the broader trend toward lightweight, high-performance packaging solutions. Finally, in November 2024, Sonoco Products Company announced its acquisition of Eviosys, expanding its packaging capabilities and potential for nano-enabled applications in the food and aerosol sectors.

Trends and Opportunities in the Nano-Enabled Packaging Market

Development of High-Barrier Nanoclay and Nanooxide Coatings for Food Preservation

The nano-enabled packaging market is being propelled by the global need to reduce food waste and extend shelf life in perishable categories. Nanoclay and nanooxide coatings, such as montmorillonite nanoclay and silicon dioxide (SiO₂) nanoparticles, are at the forefront of this transformation. These materials create a “tortuous path” barrier, drastically slowing the diffusion of oxygen and water vapor molecules through packaging films. Academic reviews highlight that even small additions of nanoclay can significantly improve the oxygen transmission rate (OTR) and water vapor transmission rate (WVTR) of polymers, outperforming traditional laminates.

The global urgency for high-barrier packaging is underscored by the UN Environment Programme’s 2024 Food Waste Index Report, which revealed that 19% of food is wasted at the consumer level, while the FAO noted another 13.2% is lost between harvest and retail. By integrating nano-enabled barriers, fresh produce, dairy, and meat packaging can extend shelf life, reduce microbial spoilage, and decrease the carbon footprint tied to food loss.

Beyond preservation, nanoclay-based films improve mechanical strength and thermal resistance, making them more durable for hot-fill applications and high-performance logistics. Their use in frozen meals, ready-to-eat categories, and export-oriented perishable supply chains highlights the rising adoption of nano-enhanced packaging solutions for food security and sustainability.

Strategic Focus on Bio-Based and Biodegradable Nanomaterials

The second major trend shaping the market is the pivot toward sustainable nano-reinforcements such as nanocellulose, nanochitin, and starch-based nanoparticles. Unlike synthetic nanoparticles, these bio-based alternatives offer biodegradability and reduced ecotoxicity while maintaining exceptional strength and barrier properties.

For instance, nanocellulose, derived from agricultural and forestry residues, is reported to be eight times stronger than steel by weight while remaining fully compostable. Coatings made with nanocellulose deliver excellent grease, oxygen, and oil resistance, enabling replacement of non-recyclable plastic linings in foodservice and consumer packaging. Similarly, nanochitin, sourced from the 10+ million tons of annual crustacean shell waste, transforms fisheries byproducts into high-value inputs for packaging films, aligning with circular economy models.

This trend is reinforced by regulatory and consumer demand for eco-friendly nanotechnology that reduces fossil-fuel dependency. The rise of biodegradable nano-enhanced coatings addresses both performance and sustainability, positioning them as a critical growth driver in next-generation packaging solutions.

Nano-Enabled Active Packaging with Controlled Release of Antimicrobials

A major opportunity lies in advancing packaging beyond passive barriers into active food preservation systems. Nano-carriers embedded with antimicrobial agents such as silver nanoparticles, nisin, or essential oils are being engineered for controlled release in response to moisture or microbial activity. This approach directly combats pathogens like E. coli and Salmonella, extending the freshness of meat, seafood, and dairy products.

Research highlights the efficacy of silver nanoparticles in reducing microbial growth, while nano-encapsulation of GRAS-certified essential oils provides longer-lasting antimicrobial protection compared to free oil applications. These controlled-release systems also reduce reliance on synthetic preservatives, catering to the clean-label trend in food packaging.

By offering a dynamic defense mechanism against spoilage, nano-enabled active packaging addresses both safety concerns and consumer demand for minimally processed, preservative-free foods. This opportunity is particularly valuable in fresh produce, poultry, and ready-to-eat meals, where microbial contamination poses the greatest risk.

Integration of Nanosensors for Real-Time Freshness and Safety Monitoring

Another high-value opportunity is the integration of nanosensors into smart packaging for freshness and safety assurance. These nanosensors can detect spoilage gases like ammonia and hydrogen sulfide, or track volatile amines released by decaying seafood and meat, triggering a visible colorimetric change on the packaging surface.

Such visual freshness indicators empower consumers and retailers to make informed decisions, reducing unnecessary disposal of still-edible products and enhancing trust in packaged goods. Technical developments also extend to thermochromic nanosensors, which provide clear indicators of cold-chain breaches in dairy, meat, and pharmaceuticals, where even short temperature deviations can compromise product integrity.

The convergence of nano-diagnostics and packaging represents a major leap forward in food safety, supply chain transparency, and consumer engagement. As regulatory frameworks increasingly emphasize traceability and shelf-life management, nanosensor-enabled packaging is poised to become a defining feature of premium and high-risk food categories.

Competitive Landscape of Global Nano-Enabled Packaging Market

The nano-enabled packaging market is highly competitive, with leading players leveraging nanotechnology, materials science, and sustainable solutions to deliver advanced, high-barrier packaging. Companies focus on applications in food, beverages, pharmaceuticals, and consumer goods, combining intelligent packaging features with enhanced barrier performance.

Amcor plc: Advancing Sustainable High-Barrier Nano-Packaging

Amcor is a global leader in flexible and rigid packaging, offering nano-enabled films and laminates that enhance barrier properties for food, beverages, and pharmaceuticals. In April 2025, Amcor partnered with Nfinite Nanotechnology to validate nanocoating technology, improving oxygen barrier performance in recyclable and compostable packaging. Its Amcor Vento™ films and high-barrier packaging solutions extend shelf life and support sustainability initiatives, giving it a competitive edge in high-performance packaging.

BASF SE: Innovating Nanomaterials for Enhanced Packaging Performance

BASF is a global chemical company supplying nanoclays, titanium dioxide nanoparticles, and polymers for high-performance packaging. Its expertise in materials science enables improvements in barrier properties, antimicrobial activity, and lightweighting. BASF invests heavily in nanomaterial research and development, offering solutions for both flexible and rigid packaging that enhance food safety, shelf life, and packaging efficiency.

Sealed Air Corporation: Leading Nano-Coated Protective and Food Packaging

Sealed Air provides high-barrier nano-enabled films and trays under its CRYOVAC® brand, extending shelf life for perishable products. Its focus on nanocoatings improves barrier properties and supports a circular economy. Sealed Air’s solutions integrate seamlessly into existing production lines, optimizing operations while providing recyclable-ready, sustainable packaging options for food and consumer goods.

Sonoco Products Company: Expanding Global Packaging Capabilities with Nano Solutions

Sonoco offers a wide range of nano-enabled films, trays, and containers with advanced barrier properties. The November 2024 acquisition of Eviosys expanded its metal food can and aerosol packaging capabilities. Sonoco emphasizes lightweight, durable, and recyclable solutions, leveraging nanocoatings to improve oxygen and moisture protection across food and beverage applications.

Honeywell International Inc.: Integrating Nanotechnology into Intelligent Packaging

Honeywell provides high-performance films and additives for protective and intelligent packaging. Its Aclar® film, often combined with nanomaterials, offers superior barrier properties for moisture-sensitive products. Honeywell’s R&D focuses on developing innovative, sustainable, and high-performance nanomaterials, enabling applications across pharmaceutical, food, and consumer products while improving shelf life, safety, and operational efficiency.

Nano enabled Packaging Market Share Insights

Nano-Clays Dominate Market Share by Nanomaterial in the Nano-Enabled Packaging Industry

Nano-clays hold the leading 35% market share in 2025, cementing their role as the most commercially adopted nanomaterial in packaging. Their dominance is attributed to their ability to create a tortuous path within polymer matrices such as PET, PP, and Nylon, significantly reducing oxygen, carbon dioxide, and moisture permeation. This property directly addresses the food and beverage industry’s need to extend shelf life without resorting to complex multi-layer laminates or heavier packaging formats. Silver nanoparticles account for a substantial 25% share, primarily due to their antimicrobial properties that safeguard perishable goods and sterile medical products, though regulatory scrutiny and consumer concerns about nanoparticle migration temper growth. Titanium dioxide and zinc oxide nanoparticles collectively secure growing shares for their UV-blocking and antimicrobial dual functionality, particularly in pharmaceuticals, cosmetics, and personal care. Carbon nanotubes, while only 8% of the market, cater to high-value applications like electrostatic discharge (ESD) protection and smart sensor integration, making them indispensable in electronics and advanced intelligent packaging solutions. Emerging nanomaterials such as nano-cellulose and nano-silica represent 5% of the market, signaling the next frontier of innovation in biodegradable and functional coatings.

Food & Beverages Hold the Largest Share by Application in the Nano-Enabled Packaging Industry

The food and beverages sector commands 50% of global nano-enabled packaging demand, making it the undisputed leader in application share. The sector’s dominance is linked to the urgent need for shelf-life extension, food safety, and waste reduction, areas where nano-clay composites and silver- or zinc-based antimicrobials deliver significant value. Modified atmosphere systems incorporating nano-barrier films are increasingly deployed across dairy, meat, and fresh produce to delay spoilage and maintain product integrity. Pharmaceuticals and healthcare represent 25% of the market, driven by stringent regulatory requirements for sterility, UV protection, and intelligent monitoring, with nanomaterials integrated into bottles, blister packs, and advanced drug-delivery systems. Electronics packaging holds a vital 10% share, where carbon nanotube-infused ESD protective packaging is essential to safeguard sensitive microchips and circuit boards during global logistics. Cosmetics and personal care secure 8%, leveraging nanomaterials for both aesthetic differentiation and product preservation, while automotive and other industrial applications collectively account for the remaining 7%, focusing on protective and specialty packaging requirements.

United States: Regulatory Compliance and Smart Nano-Enabled Packaging Drive Market Expansion

The United States nano-enabled packaging market is governed by a complex regulatory landscape, with oversight from the FDA and EPA. The Toxic Substances Control Act (TSCA) and product-specific, science-based guidance from the FDA ensure the safety of nanomaterials used in food and consumer products. These regulations encourage the development of compliant, high-performance nano-enabled packaging solutions that protect products and extend shelf life.

Technological advancements are transforming the market, with companies incorporating nano-clays, carbon nanotubes, and nanosensors into packaging materials to enhance barrier properties and enable real-time monitoring of food safety and quality. Corporate investments, such as Sonoco’s acquisition of Eviosys and Amcor’s partnership with Nfinite Nanotechnology, highlight strategic expansion in metal food cans, aerosol packaging, and compostable nano-coatings. Key applications include the food and beverage sector for shelf-life extension and the pharmaceutical and healthcare sectors for drug delivery and medical device sterilization, emphasizing the critical role of advanced nano-enabled packaging in product protection and consumer safety.

Germany: Stringent EU Regulations and Resource-Efficient Packaging Innovations Lead Market Growth

Germany operates under some of the world’s strictest regulations for nanomaterials in packaging, driven by the European Union’s focus on food safety and material compliance. Manufacturers are producing nano-enabled films and composites that meet stringent safety standards while providing enhanced protection against moisture and gases.

German companies are pioneers in advanced film extrusion and ultra-thin resource-saving materials, including SML’s 15-micron mono-oriented MDO-PE film for stand-up pouches. There is also a strong focus on recycled content and sustainable packaging solutions, aligning with circular economy principles. Market demand is particularly strong in the food and beverage industry, preserving fresh produce and ready-to-eat meals, as well as in the building and construction sector for insulation and other applications requiring high-performance plastics.

China: Government Support and Automation Propel Nano-Enabled Packaging Adoption

China’s nano-enabled packaging market benefits from robust governmental initiatives supporting high-performance plastics and advanced manufacturing. Policies that fast-track technology standards and simplify approvals are enabling rapid innovation. China now leads globally in nanotechnology patents, accounting for nearly 40% of the total in 2024, reflecting strong R&D momentum.

Chinese manufacturers are adopting automation and AI-driven production systems to enhance quality control and efficiency. Facilities like Amcor’s Huizhou plant showcase intelligent production capabilities, meeting rising demand from e-commerce, food processing, consumer goods, and electronics sectors. Focus on sustainable materials and recycling regulations further encourages the adoption of lightweight, nano-enabled packaging solutions, making them a critical component of China’s growing high-quality packaging industry.

India: Policy Support and Innovative Barrier Packaging Boost Nano-Enabled Market

India’s nano-enabled packaging industry is driven by government initiatives such as Make in India and the Production Linked Incentive (PLI) scheme, which promote domestic manufacturing and circular economy principles. Policies favoring infinitely recyclable materials are encouraging the adoption of sustainable nano-enabled packaging.

Technological advancements are evident in barrier-coated, micro-perforated packaging developed by companies like Uflex Ltd., reducing plastic usage while maintaining functionality for single-serve food and beverage sachets. Corporate investments, including the Huhtamaki Foundation’s CloseTheLoop recycling facility, support sustainability and innovation. The market is particularly strong in the food and beverage sector, driven by supermarkets and online retail, where nano-enabled packaging ensures product protection, shelf-life extension, and premium brand presentation.

Japan: Innovative Materials and Sustainability Initiatives Strengthen Market Position

Japan has implemented new food container and packaging regulations, effective June 2025, introducing a positive list of permissible synthetic materials. These regulations drive the development of safe and compliant nano-enabled packaging for food, beverages, and electronics.

Japanese innovations include plastics that dissolve in seawater, providing eco-friendly alternatives to traditional packaging and addressing ocean pollution. The government actively promotes recycled plastics in the automotive and packaging sectors, supported by the Industry-Government-Academia Consortium. Key applications span the food and beverage industry and consumer electronics, where high-quality nano-enabled packaging enhances product safety, durability, and consumer appeal, reinforcing Japan’s leadership in sustainable packaging solutions.

Nano enabled Packaging Market Report Scope

Nano enabled Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$41 Billion

|

|

Market Size (2034)

|

$126.1 Billion

|

|

Market Growth Rate

|

13.3%

|

|

Segments

|

By Technology (Active Packaging, Intelligent Packaging, Controlled Release Packaging), By Nanomaterial (Nano-clays, Silver Nanoparticles, Titanium Dioxide Nanoparticles, Carbon Nanotubes, Nano-zinc Oxide, Others), By Application (Food & Beverages, Pharmaceuticals & Healthcare, Cosmetics & Personal Care, Automotive, Electronics, Others), By End-User (Food Manufacturers, Pharmaceutical Companies, Cosmetics & Personal Care Brands, Electronics Manufacturers, Automotive Components Manufacturers)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Sonoco Products Company, BASF SE, Honeywell International Inc., Nouryon Chemicals Holding B.V., Trelleborg AB, SABIC, Tetra Pak International S.A., Nfinite Nanotechnology, Metalchemy, Chase Corporation, Nanopack S.A., Nano Pack Ltd., Nanocore Inc., Sphere One, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Nano enabled Packaging Market Segmentation

By Technology

- Active Packaging

- Intelligent Packaging

- Controlled Release Packaging

By Nanomaterial

- Nano-clays

- Silver Nanoparticles

- Titanium Dioxide Nanoparticles

- Carbon Nanotubes

- Nano-zinc Oxide

- Others

By Application

- Food & Beverages

- Pharmaceuticals & Healthcare

- Cosmetics & Personal Care

- Automotive

- Electronics

- Others

By End-User

- Food Manufacturers

- Pharmaceutical Companies

- Cosmetics & Personal Care Brands

- Electronics Manufacturers

- Automotive Components Manufacturers

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Nano enabled Packaging Market

- Amcor plc

- Sonoco Products Company

- BASF SE

- Honeywell International Inc.

- Nouryon Chemicals Holding B.V.

- Trelleborg AB

- SABIC

- Tetra Pak International S.A.

- Nfinite Nanotechnology

- Metalchemy

- Chase Corporation

- Nanopack S.A.

- Nano Pack Ltd.

- Nanocore Inc.

- Sphere One, Inc.

* List Not Exhaustive

Methodology

USDAnalytics employs a robust, multi-dimensional research methodology to provide comprehensive insights into the global Nano-Enabled Packaging market. Our approach integrates primary research, including interviews with packaging engineers, R&D specialists, and supply chain executives, alongside secondary research from regulatory filings, industry reports, company disclosures, and academic studies. Market sizing and forecasting combine historical trends, CAGR projections, adoption of nanomaterials (nano-clays, silver nanoparticles, titanium dioxide, carbon nanotubes, and emerging bio-based nanoparticles), and application-specific growth drivers across food & beverages, pharmaceuticals, and consumer goods. We assess technological innovations such as active packaging, intelligent nanosensor integration, and controlled-release systems, alongside sustainability initiatives incorporating biodegradable nanomaterials and eco-friendly coatings. Regulatory impacts from agencies like the FDA, EPA, and EU authorities, coupled with global policies promoting safe nanomaterials and recyclable packaging, are thoroughly evaluated. Competitive intelligence examines strategic collaborations, acquisitions, and product launches by key players like Amcor, BASF, Sonoco, Honeywell, and Nfinite Nanotechnology, highlighting their approaches to high-barrier performance, antimicrobial protection, intelligent monitoring, and sustainable packaging. This methodology ensures USDAnalytics delivers actionable, data-driven insights that empower industry professionals to make informed strategic, operational, and innovation-focused decisions in the rapidly evolving nano-enabled packaging market.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.