Paint Packaging Market Set to Reach $42.2 Billion by 2034 Fueled by DIY and Sustainable Packaging Trends

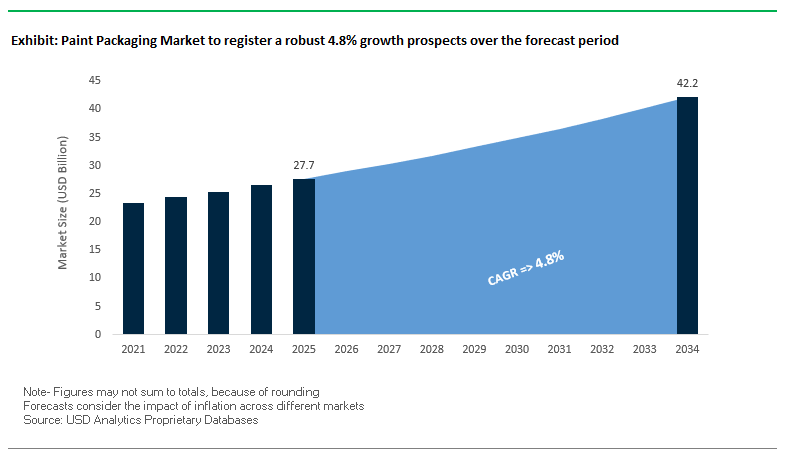

The Global Paint Packaging Market is projected to grow from $27.7 billion in 2025 to $42.2 billion by 2034, at a CAGR of 4.8%, driven by the expanding DIY and home renovation markets, rising sustainability mandates, and evolving consumer preferences for functional, user-friendly packaging. Paint packaging encompasses metal cans, plastic pails, and innovative pouches, ensuring product integrity, preventing spills, and enhancing brand visibility at the point of sale.

Key Insights for Industry Professionals:

- DIY and Home Renovation Surge: Smaller, easy-to-handle containers are increasingly preferred by individual consumers.

- Sustainability Push: Shift toward recycled steel cans and post-consumer recycled (PCR) plastic pails aligns with corporate and regulatory targets.

- Functional Innovation: Features such as easy-open lids, improved seals, and enhanced printability are crucial for brand differentiation.

- Lightweight Packaging Designs: Adoption of plastic pails, pouches, and bag-in-box systems reduces transport costs and overall carbon footprint.

- Regulatory Compliance and Consumer Safety: Packaging materials are evolving to meet environmental regulations and health-conscious consumer demands.

Industry Momentum Driven by Strategic Acquisitions, Eco-Friendly Innovations, and Technological Advancements

The Global Paint Packaging Industry has witnessed significant strategic developments, reflecting a commitment to sustainability, advanced packaging technologies, and market consolidation. In August 2025, Crown Holdings formalized its net-zero targets through validation by the Science Based Targets initiative (SBTi), reinforcing its dedication to low-carbon packaging solutions. July 2025 saw Crown release its Second Quarter results, highlighting operational and strategic progress, while PPG emphasized sustainability across its product lifecycle, including packaging.

May 2025 marked Sherwin-Williams releasing its 2024 Sustainability Report, detailing advancements in waste management and eco-friendly packaging adoption. In March 2025, Billerud introduced heat-sealable, recyclable paper alternatives, presenting new opportunities for paper-based paint containers. Major industry consolidations include Smurfit Kappa completing the acquisition of WestRock in November 2024, establishing a dominant paperboard supplier for paint packaging.

Innovation in eco-packaging and lightweight formats continues to shape the market. In October 2023, PPG’s DYRUP brand in Denmark launched a bag-in-box system composed of 75% recyclable and biodegradable materials. Earlier, in August 2022, BASF partnered with Nippon Paint China to implement industrial eco-packaging, building a sustainable supply chain in the Asia-Pacific region.

Trends and Opportunities Defining the Future of the Paint Packaging Market

Mandated Shift to Recycled Content and Recyclable Mono-Material Structures

The paint packaging market is undergoing a major structural transformation due to global regulatory mandates and corporate sustainability commitments. The European Union’s Packaging and Packaging Waste Regulation (PPWR), effective from February 2025, enforces strict recycled content targets—ranging from 10–35% by 2030 and rising to 25–65% by 2040, depending on packaging category. These targets are creating a legally binding demand for post-consumer recycled (PCR) plastics in paint pails, lids, and containers.

In the U.S., Extended Producer Responsibility (EPR) laws in seven states are reinforcing the same transition, making manufacturers financially accountable for the end-of-life management of their packaging. Paint majors like AkzoNobel are ahead of the curve, reporting 43% recycled content in 2024 in their European packaging, with a goal of 50% by 2025. To meet these evolving requirements, manufacturers are rapidly transitioning from multi-material designs to mono-material HDPE structures, which simplify recyclability and align with material recovery infrastructure. This shift represents not only regulatory compliance but also a redefinition of packaging performance, recyclability, and brand reputation.

Adoption of Bag-in-Box and Refillable Systems to Reduce Plastic Waste

The second defining trend is the adoption of bulk and reusable paint packaging formats that minimize single-use plastic. AkzoNobel’s Decorative Paints UK division piloted 170-liter reusable containers for large projects, reducing the number of single-use cans required. Meanwhile, bag-in-box systems, long established in food and beverage, are now entering the paint industry, offering logistical efficiency, extended shelf stability, and a lower carbon footprint.

These models align directly with circular economy goals, as they replace the need for continuous manufacturing of rigid plastic pails. The use of replaceable liners in durable outer containers or flexible inner bags that collapse during dispensing drastically cuts down material waste. For industrial and professional segments, where project scales are large, these systems deliver cost savings, sustainability compliance, and operational convenience—positioning refillable and bag-in-box solutions as the future backbone of sustainable paint packaging.

Development of Advanced PCR HDPE with Enhanced Performance Properties

A major opportunity lies in the upcycling of PCR resins to meet the demanding mechanical and chemical requirements of paint packaging. Research published in 2025 demonstrated that blending PCR-HDPE with engineering polymers like PBT and PA6 results in composites with superior impact toughness and durability. Such composites ensure that PCR-based paint pails can withstand chemical exposure, stacking loads, and handling stress, which were previously barriers to PCR adoption.

The Association of Plastic Recyclers (APR) PCR certification program, backed by U.S. legislation such as California SB54, provides brands with third-party assurance and full chain-of-custody traceability, making it easier to build consumer trust and regulatory compliance. At the same time, chemical recycling investments are scaling globally, with technologies that break down mixed plastic waste into virgin-quality feedstocks suitable for food-contact and high-performance applications. Together, these innovations create a clear path for a closed-loop system in paint packaging, where durable, high-barrier containers can be made from recycled material without performance trade-offs.

Integration of Smart Labels for Color Accuracy and Project Management

Another significant growth opportunity is the integration of smart labeling technologies that extend packaging utility beyond containment. X-Rite’s ColorDesigner PLUS workflow is a notable example, allowing retailers to achieve a first-hit color match 50% more often—a major improvement that reduces costly mis-tints and enhances consumer satisfaction.

Smart labels embedded with QR codes or NFC chips can unlock augmented reality (AR) features, enabling customers to visualize paint colors on walls, receive project-specific guidance, and manage inventory. For professionals, these labels can provide instant digital access to Safety Data Sheets (SDS) and Technical Data Sheets (TDS), streamlining compliance and improving job-site efficiency.

Competitive Landscape Reflects Innovation, Sustainability, and Custom Solutions in Paint Packaging

The Global Paint Packaging Industry is dominated by companies combining expertise in metal and plastic packaging, material science, and sustainability to deliver durable, high-performance containers for paints and coatings. Leading players focus on eco-friendly designs, lightweight formats, and brand differentiation.

Crown Holdings: Advancing Metal Packaging with Net-Zero Targets and Innovative Container Designs

Crown Holdings specializes in rigid metal packaging, offering steel and aluminum cans for paints and coatings. In August 2025, the company validated its net-zero targets with SBTi, reinforcing its low-carbon commitment. Crown’s offerings include customizable metal cans with high-quality printing, balancing durability, functionality, and sustainability. Its Twentyby30 program accelerates ESG initiatives, supporting brands in achieving sustainability goals.

Silgan Holdings: Providing Comprehensive Metal and Plastic Packaging Solutions for Paints

Silgan Holdings delivers steel and aluminum containers, as well as plastic closures and dispensing systems, for the paint industry. The company emphasizes custom designs for diverse applications, including industrial chemicals and household paints. Silgan focuses on lightweight, recyclable packaging, combining innovation and quality to help customers meet sustainability objectives.

Ardagh Group: Leveraging Sustainable Metal Expertise to Protect and Preserve Paint Quality

Ardagh Group provides metal packaging with superior barrier properties that protect paint from light and oxygen exposure. Through Ardagh Metal Packaging (AMP), the company promotes sustainable, infinitely recyclable containers. Its metal solutions cater to general line paint packaging, offering durability while enhancing brand appeal and eco-conscious messaging.

Mauser Packaging Solutions: Driving Circular Economy Through Plastic Paint Containers

Mauser Packaging Solutions offers industrial-grade plastic pails and tighthead drums, emphasizing reuse, reconditioning, and recycling services. The company focuses on PCR content and sustainable solutions, helping customers reduce environmental impact. Mauser’s containers are durable, versatile, and designed for circular industrial packaging.

Berry Global Group: Innovating Lightweight Plastic Packaging While Supporting Circular Economy

Berry Global delivers plastic pails, tubs, and bottles with a focus on lightweight, high-performance design. The July 2025 merger with Amcor strengthened its presence in industrial and consumer paint packaging. Berry prioritizes recycled content, product protection, and shelf appeal, aligning with the global transition toward sustainable plastics.

Paint Packaging Market Share Insights, 2025-2034

Cans & Pails Lead Market Share by Product Type in the Paint Packaging Industry

Cans and pails dominate the paint packaging industry with 45% market share, reflecting their central role in the architectural coatings segment, which accounts for the bulk of global paint demand. Metal cans (typically one-gallon or four-liter formats) remain the standard in consumer and DIY channels due to their cost-effectiveness, stackability, resealability, and robust barrier properties. Plastic pails are equally important for larger commercial volumes, offering durability and ease of handling for contractors and industrial buyers. Drums, with a 20% share, serve the bulk packaging needs of the industrial, protective, and automotive coatings markets, where large-volume delivery to OEMs and professional applicators is essential. Aerosol cans occupy a resilient niche, enabling precise application in automotive repair, industrial maintenance, and specialty coatings, though their growth is moderated by VOC regulations and shifts in propellant technology. Bottles are indispensable for packaging wood coatings, stains, and solvents, where controlled pouring and smaller volumes are required. Emerging formats such as pouches, tubes, and composite containers are gaining traction in sustainability-focused and premium branding strategies, offering lightweight alternatives that reduce material usage and transportation costs while appealing to eco-conscious consumers.

Architectural Coatings Drive the Largest Market Share by Application in the Paint Packaging Industry

Architectural coatings dominate paint packaging with 65% of application share, reflecting the massive scale of residential and commercial construction, renovation, and DIY projects worldwide. This segment’s packaging requirements prioritize convenience, affordability, and durability, with metal cans and plastic pails leading due to their user-friendly features like easy-open lids, resealability, and compatibility with labeling technologies. Industrial coatings hold the second-largest share, with packaging focused on bulk delivery formats such as drums and intermediate containers, designed to withstand aggressive chemical formulations while ensuring safe storage and application. Automotive coatings represent a diverse packaging profile, spanning drums for OEM plants, aerosol cans for aftermarket touch-ups, and smaller containers for workshops, underscoring the segment’s multifaceted needs. Wood coatings rely heavily on bottles and cans that provide precise dispensing and preserve product quality, with consumer preference for user-friendly packaging innovations like integrated applicators driving growth. Protective and marine coatings remain specialized but high-value niches, where packaging must deliver rugged performance, corrosion resistance, and perfect sealing integrity to prevent spoilage of products designed for extreme environments such as bridges, ships, and offshore structures. Collectively, application trends highlight that architectural coatings drive volume, while industrial, automotive, and protective coatings ensure technical diversification in the global paint packaging market.

China Paint Packaging Market Driven by Infrastructure Growth and Eco-Friendly Innovations

The China paint packaging market is expanding rapidly, driven by the country’s massive infrastructure and construction investments, projected to reach USD 13 trillion by 2030. This scale of development directly fuels demand for durable and versatile paint packaging solutions across residential, commercial, and industrial sectors. Nippon Paint China, with more than 70 production bases and 10,000 employees, highlights the country’s large-scale paint and packaging ecosystem, strengthening its position as a global hub.

Sustainability is a major driver. A strategic collaboration between Nippon Paint China and BASF introduced the first water-based barrier coating for industrial paint packaging in the country, signaling a shift toward eco-friendly and recyclable packaging materials. The government’s strict regulations on single-use plastics are accelerating this transformation, pushing manufacturers toward biodegradable packaging, advanced barrier coatings, and reusable container formats that align with both regulatory mandates and consumer environmental expectations.

United States Paint Packaging Market Supported by Industry Leaders and E-Commerce Growth

The United States paint packaging market is supported by global industry leaders such as PPG Industries and Sherwin-Williams, both headquartered in the U.S. These companies are continuously innovating packaging formats to improve safety, shelf life, and branding appeal. The U.S. construction sector, fueled by both residential and commercial projects, remains a dominant demand driver, ensuring steady growth in metal cans, pails, and advanced plastic containers for paints and coatings.

Corporate transformation is also influencing packaging development. Axalta Coating Systems’ February 2024 restructuring plan focused on streamlining operations and enhancing packaging solutions for better customer service. Meanwhile, Diamond Paints’ expansion into Asian manufacturing hubs underlines the U.S. role in global paint production and packaging innovation. Increasing emphasis on sustainable and smart packaging technologies, such as low-VOC containers and tamper-evident packaging, reflects broader regulatory pressure and consumer demand for eco-friendly solutions.

India Paint Packaging Market Fueled by Construction Boom and Smart Packaging Adoption

The India paint packaging market is thriving due to the country’s construction sector, which is poised to become the third-largest globally, with a surge in affordable housing projects by 2025. This rapid growth drives significant demand for bulk paint containers, automotive coating packaging, and eco-friendly solutions. The Ministry of Environment, Forest and Climate Change (MoEFCC) is promoting biodegradable and recyclable packaging materials, compelling manufacturers to embrace sustainable practices in paint packaging.

Technological modernization is another defining factor. The government’s Digital India initiative is accelerating the adoption of RFID-enabled paint containers, digital labeling, and smart tracking technologies for better inventory management and consumer engagement. Nippon Paint India’s strategy to double automotive refinish revenues and Asian Paints’ backward integration project in Gujarat to build a new VAE/VAM complex reflect strong investments in both raw materials and packaging innovation. These moves emphasize India’s growing role in automotive coatings packaging, e-commerce paint distribution, and eco-friendly consumer packaging solutions.

Germany Paint Packaging Market Led by Automotive Industry and EU Packaging Mandates

The Germany paint packaging market is strongly influenced by the country’s automotive sector, which demands specialized, durable, and chemical-resistant packaging solutions for high-performance coatings. Rising consumer and industrial awareness of sustainability is driving demand for biodegradable and recyclable packaging formats, particularly in the automotive and construction industries.

The EU Packaging and Packaging Waste Directive (PPWD), aiming for 100% recyclable or reusable packaging by 2030, is a central regulatory driver. German manufacturers are responding with circular economy packaging solutions, including metal packaging with improved recyclability and bio-based container coatings. BASF Coatings, headquartered in Germany, plays a leading role in advancing sustainable packaging coatings, positioning the country as a key European hub for eco-friendly paint packaging innovation.

Netherlands Paint Packaging Market Driven by AkzoNobel’s Global Innovation Strategy

The Netherlands paint packaging market is led by AkzoNobel, headquartered in the country and active in 150 markets worldwide. The company’s strategic focus on sustainable paint packaging solutions reflects both European consumer demand for eco-friendly packaging and compliance with EU environmental regulations.

Recent developments, such as AkzoNobel’s 2022 acquisition of Lankwitzer Lackfabrik GmbH’s wheel liquid coatings business, underscore its expansion into specialized coatings and packaging systems. Dutch innovation is centered on lightweight, recyclable, and smart packaging solutions, enabling product traceability and reducing environmental impact. With its global footprint and R&D focus, the Netherlands is positioned as a leader in sustainable paint packaging within Europe and beyond.

Japan Paint Packaging Market Strengthened by Innovation in Green and High-Tech Solutions

The Japan paint packaging market is powered by global leaders like Nippon Paint, Kansai Paint, and Chugoku Marine Paints, each specializing in different coatings segments that require specialized, durable, and protective packaging. Nippon Paint’s emphasis on green formulations and Kansai Paint’s wide-ranging portfolio in automotive, industrial, and protective coatings drive demand for packaging that ensures chemical stability and extended shelf life.

Japan’s marine coatings sector, led by Chugoku Marine Paints, highlights the need for high-strength packaging solutions capable of withstanding harsh marine environments. The country is also at the forefront of developing self-healing paints and advanced materials, which require innovative, airtight, and functional packaging to maintain product integrity. Together, these dynamics make Japan a global hub for next-generation paint packaging solutions that balance sustainability, durability, and technological sophistication.

Paint Packaging Market Report Scope

Paint Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$27.7 Billion

|

|

Market Size (2034)

|

$42.2 Billion

|

|

Market Growth Rate

|

4.8%

|

|

Segments

|

By Material (Metal, Plastic, Paper & Paperboard, Glass, Other Materials), By Product Type (Cans & Pails, Bottles, Pouches & Tubes, Drums, Containers, Aerosol Cans), By Application (Architectural Coatings, Industrial Coatings, Automotive Coatings, Marine Coatings, Protective Coatings, Wood Coatings)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Sherwin-Williams Company, PPG Industries, AkzoNobel, Nippon Paint Holdings Co., Ltd., RPM International Inc., Axalta Coating Systems, BASF Coatings, Asian Paints Limited, Kansai Paint Co., Ltd., Jotun AS, Hempel A/S, Masco Corp, Berger Paints India Ltd., Benjamin Moore & Co., SKSHU (3trees)

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Paint Packaging Market Segmentation

By Material

- Metal

- Plastic

- Paper & Paperboard

- Glass

- Other Materials

By Product Type

- Cans & Pails

- Bottles

- Pouches & Tubes

- Drums

- Containers

- Aerosol Cans

By Application

- Architectural Coatings

- Industrial Coatings

- Automotive Coatings

- Marine Coatings

- Protective Coatings

- Wood Coatings

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Paint Packaging Market

- Sherwin-Williams Company

- PPG Industries

- AkzoNobel

- Nippon Paint Holdings Co., Ltd.

- RPM International Inc.

- Axalta Coating Systems

- BASF Coatings

- Asian Paints Limited

- Kansai Paint Co., Ltd.

- Jotun AS

- Hempel A/S

- Masco Corp

- Berger Paints India Ltd.

- Benjamin Moore & Co.

- SKSHU (3trees)

* List Not Exhaustive

Methodology

USDAnalytics utilizes a comprehensive and multi-layered research methodology to deliver accurate and actionable insights into the global Paint Packaging Market. Our approach integrates primary research, including interviews and surveys with key stakeholders such as packaging manufacturers, paint companies, regulatory authorities, and distributors, alongside secondary research from corporate filings, government publications, industry journals, and trade databases. We analyze material trends, product types, and applications—including metal cans, plastic pails, paperboard containers, drums, and innovative pouch solutions—while examining sustainability initiatives, regulatory compliance, and technological advancements such as smart labeling and digital tracking. USDAnalytics employs quantitative modeling to project market growth, assess competitive landscapes, and evaluate emerging opportunities in reusable, bag-in-box, and post-consumer recycled (PCR) packaging solutions. Regional insights cover major markets including the U.S., China, India, Germany, Netherlands, and Japan, accounting for local regulations, construction and DIY trends, and sustainability mandates. By combining qualitative and quantitative analysis, USDAnalytics ensures a holistic understanding of the market’s dynamics, competitive strategies, and innovation trajectories, empowering industry professionals to make informed decisions and capitalize on growth opportunities in eco-friendly, high-performance paint packaging solutions.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.