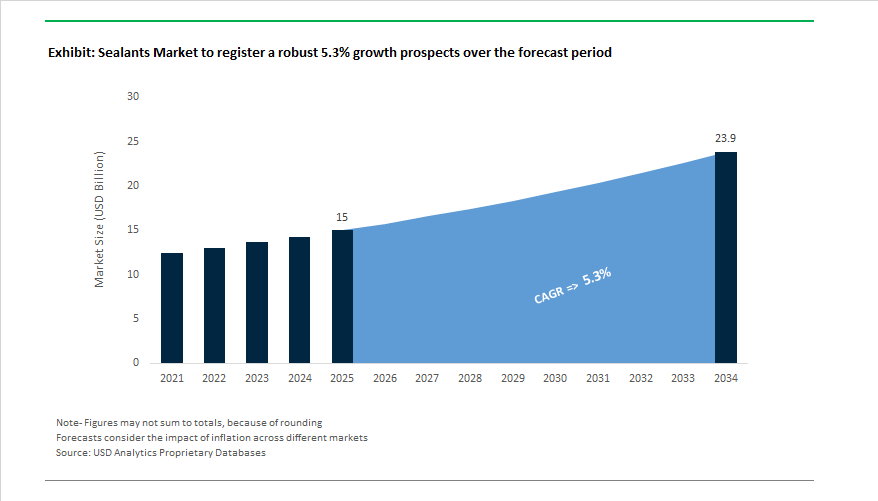

The Global Sealants Market is projected to expand from USD 15.0 billion in 2025 to USD 23.9 billion by 2034, at a CAGR of 5.3%, as sealants become structurally embedded in energy efficiency, durability, and safety outcomes across buildings, vehicles, and industrial assets. Growth reflects a shift in how architects, OEMs, and regulators treat sealants—as functional materials that directly influence airtightness, weather resistance, vibration control, and lifecycle performance, rather than cosmetic finishing products.

Silicone sealants remain the performance benchmark, particularly in façade glazing, curtain walls, and expansion joints, where long-term UV stability, elastic recovery, and temperature resistance are non-negotiable. Manufacturers such as Dow, Wacker Chemie, Shin-Etsu, and Momentive continue to refine neutral-cure and low-modulus silicone systems designed to maintain elasticity for decades under constant thermal cycling and solar exposure. These properties are central to high-rise and infrastructure projects, where sealant failure directly compromises water ingress protection and energy efficiency. In parallel, building envelopes are being designed around airtight and watertight continuity, elevating sealant specification as a prerequisite for meeting modern thermal performance targets rather than a downstream detail.

At the same time, silyl-modified polymers (SMPs) and hybrid sealants are emerging as the fastest-growing chemistry class, particularly in construction, modular assembly, and industrial applications. Suppliers such as Sika, Henkel, Bostik (Arkema), and Tremco are positioning hybrid systems as a strategic alternative to traditional silicones and polyurethanes by combining primerless adhesion, paintability, and low-VOC profiles with elastic movement capability. These hybrids are increasingly specified in LEED-aligned and low-emission projects, where contractors require fast skin-over times, reduced odor, and broad substrate compatibility without sacrificing durability.

Automotive and electric vehicle manufacturing represents a structurally important demand vector. Silicone and polyurethane sealants are increasingly used in battery enclosures, windshield bonding, body seams, and NVH isolation, where resistance to heat, vibration, and chemical exposure is critical. As EV architectures reduce powertrain noise, sealants play a more visible role in acoustic comfort and long-term joint integrity, shifting procurement focus toward elastic recovery, aging resistance, and compatibility with mixed material stacks. Major OEM programs increasingly qualify sealants alongside structural adhesives rather than treating them as secondary consumables.

Minimum Energy Performance Standards (MEPS) in the U.S. and the EU Energy Performance of Buildings Directive (EPBD) are pushing airtightness, moisture control, and low-emission materials to the forefront of design. In this environment, sealants are evolving into energy-management components—integral to controlling air leakage, thermal bridging, and moisture ingress across windows, doors, façades, and service penetrations.

The Global Sealants Industry is witnessing accelerated transformation fueled by strategic acquisitions, sustainability-focused R&D, and regulatory compliance. In October 2025, Sika AG expanded its footprint in Northern Europe by acquiring a mortar and construction chemical company in Denmark, consolidating its presence in the Nordic region—a market known for advanced insulation and sealant requirements in cold climates. Similarly, in June 2025, Sika further strengthened its Middle Eastern operations with the acquisition of Gulf Additive Factory LLC in Qatar, reinforcing its portfolio of waterproofing and joint sealants for infrastructure projects aligned with regional urbanization initiatives.

Henkel AG & Co. KGaA, under its Loctite brand, launched an innovative line of LED-curable adhesives and sealants in September 2025, addressing the growing medical device manufacturing sector. These products are biocompatibility-certified and enable faster, safer curing processes, particularly for wearable and implantable devices—a testament to how traditional sealant technology is evolving toward precision-engineered, high-performance bonding systems.

The global policy landscape also continues to shape the sealants market. The European Union’s Energy Performance of Buildings Directive (EPBD), revised in August 2025, mandates all new buildings to be Zero-Emission Buildings (ZEBs) by 2030, amplifying demand for airtight silicone and hybrid sealants in façades, joints, and glazing systems. In parallel, the U.S. Department of Energy (DOE) issued new rules in May 2025 for federal buildings, requiring a 90% reduction in fossil fuel usage by 2029. This has led to increased adoption of thermal-bridge-breaking sealants and high-insulation materials that directly contribute to building decarbonization targets.

Bostik (Arkema) continues to advance the smart adhesives and sealants category, unveiling low-VOC and recyclable formulations (March 2025) targeting flexible packaging and sustainable construction applications. These innovations align with Arkema’s broader circular economy goals and reflect an industry-wide commitment to reducing solvent use. Meanwhile, Dow Inc., the undisputed leader in silicone technology, launched its DOWSIL™ 991 Silicone High-Performance Sealant in January 2025, formulated for non-staining performance on natural stone and metal façades—an aesthetic and technical advantage sought after by premium façade contractors.

Strategically, Sika AG’s continued acquisition wave (including HPS North America in Q4 2024 and Cromar Building Products in April 2025) positions it as the most integrated global construction solutions provider. The company’s AI-driven partnership with Giatec™ Scientific (June 2025) underlines the increasing importance of digitalization in construction chemistry, merging data analytics, predictive curing, and sustainability within sealant applications.

Market Trend 1: Accelerated Reformulation to Eliminate PFAS and Restricted Substances Across Global Sealant Supply Chains

The accelerated elimination of PFAS and plasticizers from commercial sealants is reshaping the formulation landscape. In April 2024, the U.S. Environmental Protection Agency (EPA) officially designated PFOA and PFOS—two of the most prevalent PFAS compounds—as hazardous substances under CERCLA (Superfund). The landmark regulation immediately raised potential liabilities for manufacturers using PFAS in sealant production, with remediation and cleanup costs legally enforceable. As a result, adhesive and sealant producers are aggressively shifting toward PFAS-free sealants and non-hazardous polymer systems to mitigate legal and environmental risk while maintaining high adhesion and flexibility standards.

In parallel, the European Union’s REACH and POPs Regulations have progressively restricted long-chain fluorinated compounds, banning PFOA, PFOS, and C9–C14 perfluorinated carboxylic acids (PFCAs). These cumulative bans are forcing the replacement of traditional fluorinated surfactants and plasticizers in high-performance sealants with safer, silane-modified or bio-based alternatives. Further, the U.S. EPA’s TSCA rule, requiring manufacturers to report all PFAS-containing materials produced or imported since 2011, has increased transparency and intensified supply chain accountability.

The convergence of regulatory enforcement, corporate ESG goals, and consumer scrutiny is reshaping competitive differentiation. Major global players are investing in green chemistry innovation, developing non-fluorinated polymer sealants, and adopting biodegradable crosslinkers to replace persistent organic pollutants. The reformulation race is not only about compliance but about capturing the fast-growing demand for sustainable construction and automotive sealants that meet modern environmental and performance benchmarks.

Market Trend 2: Hybrid Polymer Sealants Dominating Multi-Substrate and Extreme Climate Applications

The global construction sector is witnessing a widespread migration toward Hybrid Polymer Sealants, such as Modified Silane (MS) and Silyl-Terminated Polyurethane (SPUR) systems, which combine the flexibility of silicones with the durability of polyurethanes—minus their primary limitations. These high-performance formulations are rapidly replacing solvent-based systems in both new construction and infrastructure rehabilitation projects.

Manufacturers are heavily investing in blended polymer R&D, merging the mechanical robustness of polyurethane with the elasticity and weather resistance of silane-modified polymers. The result is a new generation of Hybrid Sealants capable of maintaining long-term adhesion to dissimilar substrates like glass, metal, wood, and concrete, even under extreme temperature and UV exposure.

The shift is particularly critical for large-scale infrastructure projects, such as bridges, tunnels, and transit systems, which require materials that can withstand mechanical stress and environmental cycling. With billions of dollars allocated through government infrastructure programs (e.g., the U.S. Infrastructure Investment and Jobs Act), demand for UV-stable, high-flexibility, solvent-free sealants continue to surge.

In addition, green building certification systems like LEED, BREEAM, and Green Star reward the use of Low-VOC, isocyanate-free products. As MS Polymer-based sealants naturally comply with these standards due to their solvent-free composition, they are emerging as the preferred specification choice for sustainable commercial and residential projects seeking indoor air quality credits and green compliance certifications.

Market Opportunity 1: Fire-Rated Acoustic Sealants Enabling Safer and Quieter Mass Timber Construction

The rapid rise of Mass Timber Construction, particularly Cross-Laminated Timber (CLT) and Glue-Laminated Timber (GLT) structures, is creating a significant opportunity for fire-rated acoustic sealants that ensure both life safety and occupant comfort. Although CLT naturally achieves excellent charring and load-bearing performance during fire events, studies show that joints and penetrations are the weakest points for smoke and gas leakage. Research indicates leakage rates of up to 8.27 m³/h at a 25 Pa pressure differential, emphasizing the urgent need for sealants that can maintain air-tightness and fire integrity under prolonged high-temperature exposure.

Recent code changes in North America and Europe permit tall timber buildings up to 18 stories, dramatically increasing the complexity of fire compartmentation and sound isolation requirements. The regulatory evolution is driving the demand for dual-function acoustic firestop sealants, capable of meeting UL- and EN-rated fire protection standards while also delivering superior sound transmission class (STC) ratings for high-rise timber buildings.

Manufacturers who develop elastomeric, non-shrinking, and intumescent sealants that maintain performance during both thermal and acoustic loading stand to gain a significant market advantage. These advanced sealants are expected to play a central role in achieving fire safety compliance, noise reduction, and LEED acoustic credits in next-generation sustainable architecture.

Market Opportunity 2: Conductive and EMI Shielding Sealants Powering 5G and Aerospace Electronics

The proliferation of 5G telecommunications, electric vehicles, and high-density electronics has unlocked new demand for conductive sealants capable of providing both environmental sealing and electromagnetic interference (EMI) protection. As 5G and mmWave technologies operate at ultra-high frequencies, electronic components are increasingly susceptible to interference, necessitating sealants with Shielding Effectiveness (SE) exceeding 60 dB, equivalent to a 99.9% EMI reduction.

In military, aerospace, and medical applications, requirements can exceed 120 dB, aligning with MIL-STD-285 specifications. These demanding environments are fueling the evolution of silver-, nickel-, and carbon nanotube-loaded sealants that combine conductivity, corrosion resistance, and mechanical durability. Such materials are critical for sealing electronic enclosures, sensor housings, and RF modules exposed to dynamic temperature and vibration conditions.

The trend toward lightweight conductive plastics in enclosures for 5G and IoT infrastructure further amplifies the opportunity. As polymer housings replace metal for cost and weight benefits, the need for conductive elastomer sealants becomes essential to ensure electromagnetic compatibility (EMC) across the system. Manufacturers developing hybrid conductive sealants with optimized filler dispersion and flexibility are poised to capture strong growth from both the telecommunications and defense electronics sectors.

Sealants Market Share Insights, 2025-2034

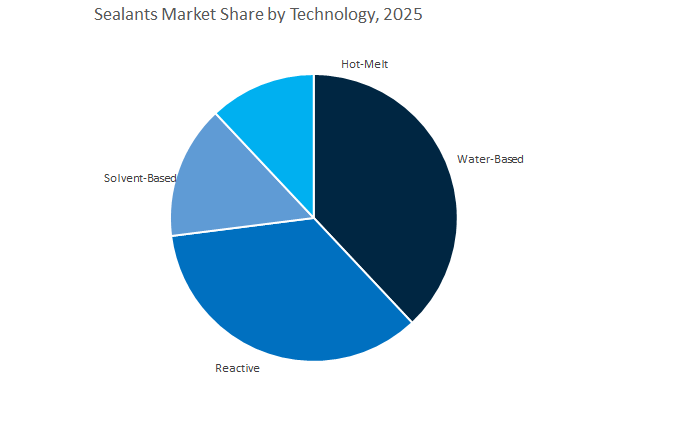

Market Share by Technology

Water-Based Sealants lead the global sealants market, accounting for an estimated 38.6% share in 2025, reflecting the industry’s shift toward sustainable, low-VOC, and environmentally friendly formulations. The dominance of water-based technologies is underpinned by stringent environmental regulations in North America, Europe, and parts of Asia-Pacific, which have accelerated the transition away from solvent-based systems. These sealants are widely adopted in building and construction, packaging, and consumer applications, owing to their ease of application, low odor, and compatibility with diverse substrates such as wood, concrete, and glass. The rise in green building certifications (LEED, BREEAM) and the increasing emphasis on eco-friendly construction chemicals have further reinforced this segment’s leadership.

Reactive Sealants represent the fastest-growing segment, driven by their high mechanical strength, superior chemical resistance, and long-term durability, making them ideal for automotive, aerospace, and industrial sealing applications. Polyurethane, silicone, and silyl-modified polymer-based reactive systems are increasingly favored for structural glazing, expansion joint sealing, and composite bonding, especially in modern architectural and mobility solutions. Solvent-Based Sealants, though declining in usage, retain relevance in industrial and heavy-duty maintenance applications, where their rapid curing, broad temperature resistance, and strong adhesion to metals and plastics are valued. Meanwhile, Hot-Melt Sealants cater to specialized applications in packaging, electronics, and assembly lines, offering instant bonding, reduced energy consumption, and clean processing.

Market Share by Application

Building & Construction is the leading application segment in the global sealants market, commanding approximately 45.4% share in 2025, driven by massive infrastructure investments, urbanization, and the expanding demand for weatherproofing, sealing, and glazing applications. Sealants play an indispensable role in modern construction for joint sealing, façade installation, flooring, and concrete repair, ensuring structural integrity, waterproofing, and thermal insulation. The surge in smart city projects, commercial real estate, and renovation activities in both developed and emerging economies has further amplified sealant consumption. Silicone and polyurethane-based products are particularly dominant in this segment, valued for their UV stability, flexibility, and long service life in dynamic building structures.

The Automotive & Transportation sector maintains a strong position, driven by sealant usage in windshield bonding, body seam sealing, and EV battery encapsulation. The ongoing transition to electric and lightweight vehicles has increased demand for advanced sealing materials that offer thermal resistance, acoustic insulation, and durability under extreme conditions. Industrial applications also represent a substantial share, spanning machinery assembly, maintenance, and equipment manufacturing, where chemical and oil resistance are critical. Meanwhile, Consumer and DIY sealants continue to grow in home improvement markets, propelled by online retail and demand for multi-purpose and easy-to-apply products. Electrical & Electronics and Packaging & Assembly form specialized yet expanding niches, where sealants enable component protection, moisture barriers, and clean adhesive performance.

The global sealants industry is led by a handful of multinational corporations—Sika AG, Dow Inc., Henkel AG & Co. KGaA, Arkema (Bostik), and Tremco CPG Inc.—each leveraging unique technological, regional, and sustainability strengths. Their strategies are increasingly defined by hybrid sealant innovation, low-VOC compliance, merger synergies, and digital integration for predictive performance.

Sika AG continues to dominate the global market through its "Roofing to Flooring" systems approach, offering end-to-end construction solutions. In 2024, Sika reported a 17.4% rise in net profit to CHF 1.25 billion, reflecting the successful integration of the MBCC Group. The company opened new plants in Singapore and Xi’an, China, focusing on mortars, waterproofing, and tile adhesive production. Sika’s investments in AI-driven construction technology (via Giatec Scientific) strengthen its leadership in smart sealant systems, optimizing product performance and sustainability across infrastructure applications.

Dow Inc. remains the market leader in silicone-based sealants, offering a comprehensive portfolio through its DOWSIL™ range, including structural glazing and weatherproofing solutions. Its DOWSIL™ 991 Silicone Sealant launched in January 2025, delivers non-staining, high-durability performance, catering to architectural projects demanding pristine aesthetics. Dow’s sealants, known for ±50% movement capability, are critical to high-rise construction under dynamic thermal conditions. The company complements its material offerings with structural design reviews and a 20-year adhesion warranty, reinforcing its position as the most technically integrated sealant provider globally.

Henkel, through its Loctite brand, combines industrial reliability with medical-grade innovation. The company’s LED-curable sealant series (September 2025) targets medical and wearable device manufacturing, meeting biocompatibility and safety standards. Henkel also offers Noise, Vibration, and Harshness (NVH) sealants for EVs, improving comfort and durability in next-generation vehicles. The company’s multi-sector portfolio—spanning MRO, automotive, and electronics—positions it as a leader in multi-performance sealant systems bridging industrial and consumer applications.

Arkema’s Bostik division emphasizes smart adhesive and sealant solutions across construction, packaging, and electronics. The company’s 2025 strategy focuses on low-VOC, solvent-free sealants that enable recyclable flexible packaging and eco-friendly construction bonding. Following its acquisition of Polytec PT (2023) and Permoseal (2024), Bostik expanded into battery assembly adhesives for EVs and high-performance SMP sealants for sustainable housing. Its Hot Melt Pressure Sensitive Adhesive (HMPAS) technology underpins Arkema’s position as a global circular economy pioneer.

Tremco CPG Inc., a subsidiary of RPM International, stands out for its holistic “Building Science” approach to commercial construction sealing systems. The company offers hybrid sealants combining silicone and polyurethane chemistries, balancing flexibility, adhesion, and paintability while maintaining compliance with stringent low-VOC regulations. Tremco’s expertise extends to infrastructure repair, supplying bridge deck and airfield sealants designed for extreme weather and chemical resistance. Its consulting-based model, offering system warranties and enclosure optimization, reinforces its role as a premium provider in durability-driven construction sealing solutions.

Country Analysis: Global Sealants Industry – Regional Innovation, Sustainability, and Growth Momentum

China: Infrastructure Expansion and EV-Driven Demand for High-Performance Silicone Sealants

China remains the largest and fastest-growing market for sealants globally, supported by massive infrastructure spending, advanced manufacturing growth, and electric vehicle (EV) adoption. The National Development and Reform Commission’s CNY 4 trillion (USD 0.56 trillion) allocation for “hidden infrastructure” upgrades through 2030—which includes over 200,000 km of new urban pipelines—is significantly driving the consumption of durable silicone sealants designed for waterproofing, insulation, and corrosion protection. As China aims to make 30% of new buildings prefabricated by 2025, demand for high-speed, structural polyurethane (PU) and silicone sealants is increasing across modular construction projects.

The nation’s EV and electronics industries are major contributors to sealant volume growth. With transportation equipment production rising 34.9% in 2024, the need for heat-cure and RTV (Room Temperature Vulcanizing) sealants in motor housings, battery modules, and lightweight body structures has surged. Domestic producers are investing in polymer innovation and RTV technology to serve growing requirements in automotive assembly and display manufacturing. Additionally, China’s 12% growth in secondary industry investments provides a strong supply base for precursors such as siloxanes and polyols, fortifying the regional ecosystem for silicone and polyurethane sealant production.

United States: Green Building Codes and Next-Generation Sealant Formulations for Sustainable Construction

The U.S. sealants industry is transitioning rapidly toward sustainability, energy efficiency, and long-term durability, driven by regulatory frameworks and changing consumer behavior. The U.S. Green Building Council’s LEED v5 framework (April 2025) has amplified emphasis on building envelope performance, with nearly 50% of points focusing on decarbonization and air-sealing systems, catalyzing the demand for low-VOC, neutral-cure silicone sealants in commercial and institutional buildings. The 2024 International Energy Conservation Code (IECC), mandating 7% higher energy efficiency for new housing, has intensified usage of high-performance building envelope and insulation sealants that minimize air leakage.

Home improvement trends reinforce steady market growth—67% of U.S. households prefer renovating rather than relocating, creating recurring demand for weather-resistant and UV-stable sealants used in roof repairs, siding, and window assemblies. Industry leaders are also expanding product portfolios into pressure-sensitive sealant tapes (PSAs) and metal bonding adhesives, optimized for high-performance environments like cold-weather installations and metal roofing systems. Backed by EPA low-VOC regulations and federal sustainability mandates, the United States is now a benchmark market for green sealant chemistry and next-generation moisture-curing technologies.

Germany: Advanced Polymer R&D and Sustainability Driving Premium Sealant Adoption

Germany continues to be Europe’s epicenter for specialty sealant innovation, supported by its advanced polymer chemistry capabilities, REACH compliance, and sustainable construction standards. German manufacturers are at the forefront of developing Low-Emission (EC1 PLUS-certified) sealant formulations to meet stringent EU indoor air quality and environmental performance regulations. The push for energy-efficient construction and climate-resilient building envelopes has made water-borne and hybrid polymer sealants increasingly dominant in the market.

The country’s automotive and renewable energy industries are also major consumers. Leading German OEMs are utilizing elastomeric sealants and adhesives for battery encapsulation and thermal management in next-generation EVs, while wind turbine blade manufacturers are adopting polyurethane and silicone sealants offering vibration damping and long-term UV resistance. R&D projects focused on lightweight, long-life, and recyclable sealant chemistries continue to shape the industry. Furthermore, large-scale investments by multinational players such as Henkel and BASF are expanding sealant capacity and supporting the transition toward bio-based, circular chemical systems, solidifying Germany’s role as a global leader in sustainable industrial sealant technology.

India: Infrastructure Expansion and Affordable Housing Driving High-Volume Sealant Demand

India’s sealants market is witnessing exponential growth, driven by urbanization, housing initiatives, and nationwide infrastructure modernization. Government-led programs such as Pradhan Mantri Awas Yojana (PMAY) and Smart Cities Mission are creating sustained demand for silicone and polysulfide sealants for waterproofing, glazing, and expansion joints in high-humidity environments. As India accelerates the construction of bridges, metro networks, and highway corridors, the use of high-modulus polyurethane and hybrid polymer sealants in expansion joints, precast structures, and tunnel linings is increasing sharply.

The government’s ‘Make in India’ policy has encouraged both domestic and international manufacturers to establish local production units, reducing reliance on imported materials and ensuring regional product availability. Multinational corporations are scaling their sealant manufacturing capabilities to cater to India’s rapidly expanding construction market, which is projected to account for over 13% of national GDP by 2026. Combined with rising awareness of energy-efficient and moisture-resistant building materials, India’s sealants market is evolving into one of the fastest-growing hubs in the Asia-Pacific region, emphasizing cost-effective, durable, and high-performance solutions for mass housing and infrastructure projects.

South Korea: Innovation in Thermal Management and High-Precision Electronic Sealants

South Korea’s sealants industry is advancing through technological innovation in electronics, EV manufacturing, and high-performance industrial applications. As a global leader in semiconductor, display, and EV battery production, South Korea drives significant demand for thermally conductive silicone and hybrid sealants that provide heat dissipation, vibration resistance, and long-term stability. Recent expansions by global silicone producers have strengthened the country’s capacity to meet surging domestic and export demand for advanced sealing compounds used in automotive electronics, display assembly, and power modules.

The push toward solid-state batteries and 6G communication devices is prompting R&D into high-purity, low-outgassing sealant formulations compatible with ultra-clean manufacturing environments. Additionally, automotive innovation—particularly in electric and hydrogen-powered vehicles—relies on high-temperature, flexible sealants for gasketing, thermal management, and NVH (Noise, Vibration, Harshness) control. With the government’s continued investment in advanced materials and green technology, South Korea is consolidating its position as a regional hub for next-generation electronic and industrial sealant solutions.

Japan: Seismic Durability and Advanced Hybrid Sealants for Aging Infrastructure

Japan’s sealants market is centered on durability, resilience, and precision engineering, reflecting the nation’s emphasis on seismic safety and infrastructure longevity. Ongoing retrofitting of bridges, tunnels, and commercial buildings has intensified demand for structural silicone sealants that can withstand extreme joint movement, temperature fluctuations, and prolonged UV exposure. The advanced formulations ensure long-term sealing integrity, especially in earthquake-prone zones and coastal environments.

Japanese manufacturers are globally recognized for their R&D in hybrid polymer and acrylic sealants, engineered for rapid curing and high flexibility, catering to a construction market facing skilled labor shortages. The country’s aging infrastructure renewal initiatives, combined with the construction of resilient, energy-efficient urban buildings, are propelling investments in high-performance, weather-resistant sealing systems. Additionally, Japanese firms’ focus on innovation in lightweight, solvent-free technologies aligns with national decarbonization goals, positioning Japan as a global leader in structural and hybrid sealant technology for long-term sustainability.

Sealants Market Report Scope

Sealants Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$15 Billion

|

|

Market Size (2034)

|

$23.9 Billion

|

|

Market Growth Rate

|

5.3%

|

|

Segments

|

By Chemistry (Silicone, Polyurethane, Acrylic, Polysulfide, Butyl, MS Polymer, Epoxy, Others), By Technology (Water-Based, Solvent-Based, Reactive, Hot-Melt), By Application (Building & Construction, Automotive & Transportation, Industrial, Electrical & Electronics, Consumer/DIY, Packaging & Assembly), By Function (Bonding, Protection, Insulation/Soundproofing, Gap Filling/Joint Sealing

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, Dow Inc., Sika AG, Arkema Group (Bostik S.A.), H.B. Fuller Company, Wacker Chemie AG, 3M Company, BASF SE, RPM International Inc., MAPEI S.p.A., Soudal Group, PPG Industries, Inc., Evonik Industries AG, Illinois Tool Works Inc. (ITW), Shin-Etsu Chemical Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Chemistry

- Silicone

- Polyurethane

- Acrylic

- Polysulfide

- Butyl

- MS Polymer

- Epoxy

- Others

By Technology

- Water-Based

- Solvent-Based

- Reactive

- Hot-Melt

By Application

- Building & Construction

- Automotive & Transportation

- Industrial

- Electrical & Electronics

- Consumer/DIY

- Packaging & Assembly

By Function

- Bonding

- Protection

- Insulation/Soundproofing

- Gap Filling/Joint Sealing

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Sealants Market

- Henkel AG & Co. KGaA

- Dow Inc.

- Sika AG

- Arkema Group (Bostik S.A.)

- H.B. Fuller Company

- Wacker Chemie AG

- 3M Company

- BASF SE

- RPM International Inc.

- MAPEI S.p.A.

- Soudal Group

- PPG Industries, Inc.

- Evonik Industries AG

- Illinois Tool Works Inc. (ITW)

- Shin-Etsu Chemical Co., Ltd.

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the Global Sealants Market with decision-grade analysis reviews of demand, regulation, technology, and end-use adoption; it highlights breakthroughs in silicone science, hybrid/MS polymer platforms, and low-VOC reformulations that enable airtight façades, EV-ready assemblies, and long-life industrial joints—benchmarking performance, movement capability, and lifecycle cost under diverse climates and substrates; integrating policy signals and capex momentum across construction and mobility, we map competitive strategies, channels, and specification trends so stakeholders can act with confidence—this report is an essential resource for product leaders, estimators, procurement teams, and building envelope consultants who need timely, defensible insight for 2025–2034 planning.

Scope Highlights

Segmentation:

- By Chemistry: Silicone; Polyurethane; Acrylic; Polysulfide; Butyl; MS Polymer; Epoxy; Others.

- By Technology: Water-Based; Solvent-Based; Reactive; Hot-Melt.

- By Application: Building & Construction; Automotive & Transportation; Industrial; Electrical & Electronics; Consumer/DIY; Packaging & Assembly.

- By Function: Bonding; Protection; Insulation/Soundproofing; Gap Filling/Joint Sealing.

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa).

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Horizon: Historic data 2021–2024 and forecast data 2025–2034.

Companies Covered: Analysis / profiles of 15+ companies.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.