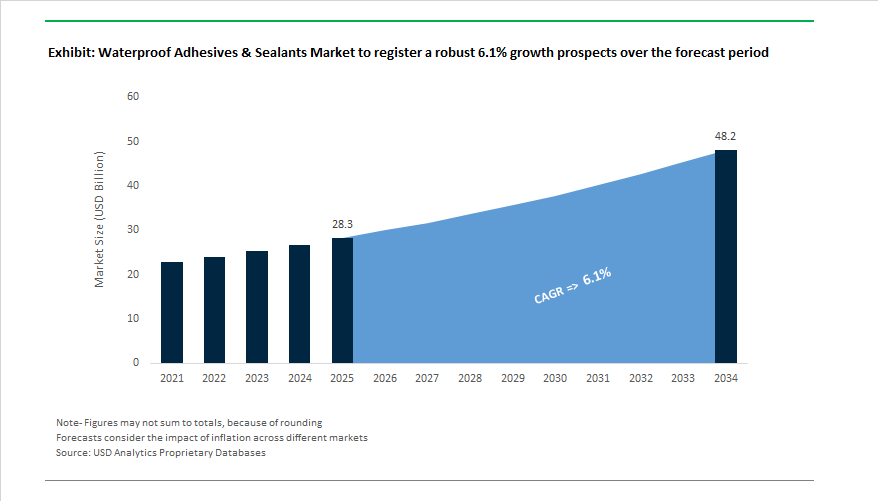

The Global Waterproof Adhesives and Sealants Market is projected to expand from USD 28.3 billion in 2025 to USD 48.2 billion by 2034, advancing at a CAGR of 6.1%, as waterproofing solutions move decisively into the core performance layer of buildings, mobility platforms, and public infrastructure. Market growth is being shaped by specification tightening, lifecycle durability requirements, and regulatory scrutiny around emissions, safety, and resilience. Across regions, waterproof adhesives and sealants are increasingly selected early in design phases, reflecting their direct impact on asset longevity, maintenance cycles, and total cost of ownership.

A central structural shift is the reformulation of chemistries toward solvent-free, water-based, and bio-attributed systems without compromising mechanical or environmental resistance. Major manufacturers such as Sika, Henkel, Arkema (Bostik), Tremco, and Dow have re-engineered polyurethane, silicone, and hybrid sealant platforms to meet stringent VOC thresholds while retaining elasticity, adhesion to difficult substrates, and long-term weathering stability. In façade, glazing, and expansion-joint applications, next-generation silicones and hybrid SMP systems are now routinely specified with ±25% to ±50% movement capability, UV stability exceeding two decades, and compatibility with high-rise curtain wall systems exposed to extreme wind loads and temperature cycling.

Electromobility and energy infrastructure are materially raising performance expectations. Waterproof adhesives and sealants used in EV battery packs, power electronics, and charging systems must now combine moisture ingress protection, dielectric integrity, vibration resistance, and thermal stability—a convergence that is accelerating demand for structural silicones and advanced polyurethanes. Manufacturers are responding with formulations qualified for IP67–IP68 sealing, low ionic contamination, and compatibility with automated dispensing in battery assembly lines. This shift is elevating waterproofing materials from secondary sealing products to safety-critical components within electric mobility architectures.

Public infrastructure and megaprojects are reinforcing the market’s durability bias. Transportation authorities and asset owners are increasingly specifying reactive polyurea and polyurethane waterproofing systems with 20–25 year certified service lives for bridges, tunnels, podium decks, and transit systems. These systems are favored for their rapid cure, crack-bridging capability, and resistance to standing water, de-icing salts, fuels, and aggressive chemicals. As infrastructure investment cycles accelerate across Asia-Pacific, the Middle East, and parts of Europe, waterproof adhesives and sealants are becoming integral to resilience strategies, particularly in flood-prone, coastal, and high-temperature environments.

Waterproof adhesives and sealants advanced on sustainability, capacity, and application breadth through 2026. In October 2025, Henkel deepened transparency by publishing 50+ Environmental Product Declarations (EPDs) for construction lines (Ceresit, Fester), positioning portfolios for EU CPR readiness and enabling project teams to earn LEED/BREEAM credits while benchmarking embodied carbon. The same month (October 2025), a major silicone producer raised prices on select siloxane intermediates due to persistent energy and feedstock pressures across Europe/North America, stressing the need for cost pass-through models, spec flexibility, and dual-chemistry alternates in strategic sourcing.

Capacity localization and infrastructure alignment were clear as Sika opened a new plant in Xi’an, China (September 2025) to ramp waterproofing membranes, admixtures, specialty mortars for China’s western build-out—cutting lead times and supply risk for megaprojects. H.B. Fuller augmented specialty sealing breadth with its acquisition of HS Butyl (August 2025), sharpening its position in butyl tapes for building envelopes and renewables. At the product-innovation frontier, Henkel (July 2025) launched Loctite Liofol LA 7837/LA 6265, a solvent-free aliphatic adhesive system for retort packaging—proof that high-thermal, high-barrier performance can coincide with zero-solvent processing.

Sustainability leadership continued as Dow (June 2025) expanded low-embodied-carbon DOWSIL™ offerings for structural glazing/weatherproofing, pairing products with PAS 2060 carbon-neutrality certificates for marquee architectural projects. Bostik (May 2025) committed capital to SMP sealants capacity in Southeast Asia to support elastic bonding in transportation and general assembly, where lightweighting and NVH benefits accelerate the shift away from mechanical fasteners. 3M (February 2025) spotlighted 3M™ Industrial Sealing Tape IS1—a high-tack acrylic that achieves instant, water-tight seals down to −18 °C, popular in HVAC, specialty vehicles, and wind where cold-start productivity is critical.

At the electrification interface, a global Tier-1 (January 2025) partnered with a leading sealant maker to co-develop a fire-retardant epoxy for mass-production EV battery modules, optimizing thermal management and structural integrity in fire scenarios. Policy also nudged specifications upward as India (December 2024) issued national standards for public-infrastructure waterproofing, mandating Type A (integral) and Type C (cementitious) compliance to boost lifecycle performance in tropical conditions. The through-line: sustainability data, localized supply, cold-weather productivity, and EV-grade reliability are defining purchase criteria and pricing power.

Market Trend 1: Rapid Adoption of Silane-Terminated Polymer (STP) Technologies for Sustainable Construction and Infrastructure

The waterproof adhesives market is undergoing a structural shift toward silane-terminated polymer (STP) sealants, a new generation of hybrid polymer technologies designed to meet both environmental and performance standards. These advanced formulations, often described as the next evolution beyond polyurethane (PU) and silicone sealants, combine the elasticity of PU with the weathering resistance of silicone, making them ideal for construction, façade sealing, and infrastructure waterproofing.

One of the major drivers for STP technology is occupational safety and health compliance. Traditional PU sealants contain isocyanates, which pose inhalation and sensitization risks to workers. In contrast, STP-based waterproof sealants are 100% isocyanate-free, removing a key health hazard while maintaining superior mechanical performance—achieving tensile strengths exceeding 1.8 MPa and elongation at break above 400%.

Environmental regulations are also accelerating adoption. Regions like California (SCAQMD Rule 1168) and the EU VOC Directive (2004/42/EC) restrict volatile organic compounds (VOCs) in sealants, prompting a widespread transition to solvent-free, low-VOC formulations. STP sealants naturally comply, ensuring compatibility with LEED and BREEAM green building certifications.

A defining advantage of hybrid STP polymers is their primerless adhesion across substrates such as concrete, aluminum, glass, and natural stone, reducing installation time and total cost. These properties make STP sealants indispensable in bridge expansion joints, roof flashing, and tunnel waterproofing, where adhesion reliability is critical for long-term performance.

Market Trend 2: Proliferation of Rapid-Cure, Underwater-Setting Formulations for Marine and Civil Engineering

The marine infrastructure and underwater construction sectors are adopting rapid-curing waterproof adhesives capable of bonding in fully submerged conditions, marking a significant evolution in civil engineering repair solutions. These epoxy-based and polyurethane underwater adhesives are enabling in-situ repairs on dams, bridges, docks, and offshore platforms without the costly need for dewatering.

Laboratory evaluations demonstrate that modern submerged-application epoxies achieve bond strengths exceeding 2 MPa when applied to steel plates underwater—performance nearly equivalent to dry bonding conditions. The level of adhesion ensures structural reinforcement even in high-pressure aquatic environments, preventing catastrophic failures in aging civil assets and marine structures.

In the water and wastewater infrastructure segment, rapid-setting hydraulic cement adhesives can achieve water-tight sealing in as little as 3–6 minutes, effectively stopping leaks and joint failures under active water flow. Such rapid-cure formulations drastically reduce downtime, enabling emergency repairs in critical systems like storm drains and desalination facilities.

The industry is also drawing inspiration from bio-adhesive systems found in nature. Recent research on mussel-inspired polyurethane underwater adhesives has demonstrated burst pressure resistance up to 394 mmHg, reflecting how biological adhesion mechanisms can be replicated for next-generation marine-grade, rapid-bonding polymers. These biomimetic adhesives hold promise for future use in medical sealing, offshore wind structures, and ship maintenance applications.

Market Opportunity 1: Development of Spray-Applied, Crack-Bridging Membranes for Below-Grade and Tunnel Waterproofing

The rising adoption of spray-applied waterproofing membranes is revolutionizing the below-grade waterproofing segment, replacing slow, labor-intensive methods like torch-applied or sheet membranes. These liquid-applied rubber and polyurea systems deliver seamless, high-performance waterproofing barriers with exceptional crack-bridging and elongation properties.

Modern liquid spray-applied rubber membranes can cover concrete foundations four times faster than traditional peel-and-stick systems. The speed advantage is vital in large-scale projects such as subway tunnels, basements, and retaining walls, where fast application translates into substantial labor cost savings and accelerated project delivery.

Hot-spray polyurea and polyurethane hybrid systems further enhance efficiency by providing gel times as short as 10–20 seconds, allowing for immediate thickness build and early overcoating. Their monolithic structure eliminates seams and potential failure points, ensuring long-term durability against hydrostatic pressure and dynamic soil movement.

Such systems are rapidly gaining ground in underground infrastructure waterproofing, offering the dual advantage of fast application and superior mechanical elasticity—essential for accommodating substrate shifts and microcracks in deep foundation environments.

Market Opportunity 2: Formulation of Thermally Conductive and Electrically Insulating Sealants for EV Battery Encapsulation

The rapid electrification of mobility is creating an entirely new class of dual-function waterproof adhesives and sealants for EV battery pack protection, combining moisture resistance with advanced thermal management capabilities. These materials ensure battery safety, heat dissipation, and electrical insulation, all of which are vital for long-term EV performance and regulatory compliance.

Silicone and polyurethane-based thermally conductive gap fillers are emerging as the leading solutions for EV battery systems, offering thermal conductivities between 1 and 5 W/m·K while maintaining complete electrical insulation. The enables efficient heat transfer from lithium-ion cells to cooling plates, preventing hotspots and enhancing battery longevity within high-voltage ePowertrain systems.

Advanced formulations also incorporate ceramification technology, allowing the adhesive to transform into a protective ceramic layer under thermal runaway conditions. The feature provides critical flame resistance and particle containment, preventing fire propagation between cells. Such ceramifying encapsulants are considered essential for compliance with UN ECE R100 and ISO 6469-1 EV safety standards.

As EV platforms evolve toward higher power densities and faster charging, thermally conductive, waterproof sealants will play a pivotal role in battery pack design, electronics encapsulation, and power module bonding, bridging the gap between mechanical protection and heat management.

Waterproof Adhesives & Sealants Market Share Insights, 2025-2034

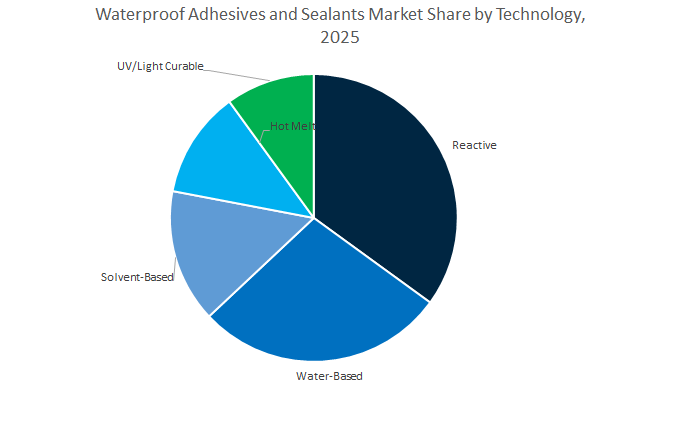

Market Share by Technology

The reactive adhesives and sealants segment dominates the global waterproof adhesives and sealants market, accounting for an estimated 37.1% share in 2025. Reactive systems—particularly polyurethanes, silicones, and silyl-modified polymers (SMP)—are preferred for their superior mechanical strength, flexibility, and long-term durability under exposure to moisture, chemicals, and fluctuating temperatures. Their ability to chemically cure into cross-linked structures creates waterproof bonds that maintain integrity in harsh conditions, making them essential in construction, automotive, marine, and industrial applications. Within the construction industry, reactive systems are integral to structural glazing, façade sealing, and concrete joint protection, where performance and longevity are paramount. In automotive and transportation, they are favored for vibration-resistant, flexible joints and windshield bonding. The growing focus on energy-efficient buildings and electric vehicle manufacturing further boosts demand for these systems due to their role in thermal management, sealing, and insulation.

Water-based technologies hold the second-largest share, reflecting the global shift toward low-VOC, environmentally sustainable formulations. They are primarily used in interior and non-structural applications where extreme durability is not required but ease of application, low odor, and cost-effectiveness are critical. As environmental regulations tighten across North America, Europe, and parts of Asia-Pacific, water-based adhesives and sealants are increasingly replacing solvent-based products in both residential and consumer DIY markets. Meanwhile, solvent-based systems continue to serve specialized markets requiring rapid drying and strong adhesion in low-temperature or high-humidity conditions, particularly in marine, industrial, and outdoor applications. Hot melt technologies are gaining steady traction due to their fast-setting nature and 100% solids composition, finding key applications in automated assembly and packaging sectors.

Market Share by End-Use Industry

The building and construction sector leads the global waterproof adhesives and sealants industry, commanding approximately 46.8% of the total market in 2025. This dominance is underpinned by the massive global demand for durable, moisture-resistant bonding and sealing solutions across infrastructure, residential, and commercial projects. Waterproof adhesives and sealants are indispensable in roofing systems, flooring, wet rooms, facades, expansion joints, and glazing applications, where long-term structural integrity depends on moisture exclusion and flexibility. The growing focus on green building certifications, energy-efficient structures, and sustainable urban development further accelerates the use of advanced waterproofing materials. Additionally, the renovation and retrofit segment—particularly in aging infrastructure in Europe and North America—represents a consistent and high-volume demand base. In emerging economies across Asia-Pacific and the Middle East, rapid urbanization and mega infrastructure projects continue to fuel construction-related consumption.

The automotive and transportation industry represents the second-largest and one of the fastest-growing application segments. Waterproof sealants and adhesives play a critical role in vehicle assembly, body panel bonding, weatherproofing, and underbody protection. With the rise of electric vehicles (EVs), demand has expanded further for applications such as battery pack encapsulation, thermal management, and moisture barrier protection in electrical components. These adhesives enhance vehicle safety, performance, and longevity by ensuring resistance to water ingress, corrosion, and vibration. Meanwhile, the consumer and DIY segment maintains a substantial share, driven by retail demand for home improvement, maintenance, and waterproof repair products. The electrical and electronics sector forms a high-value niche, utilizing waterproof adhesives and sealants for potting, encapsulation, and component protection in sensitive devices. This is increasingly vital for wearable electronics, 5G devices, and EV electronics, where reliability under humid and high-temperature conditions is critical. Packaging applications rely on water-resistant hot melt and water-based adhesives to ensure product protection and integrity in flexible packaging, corrugated boxes, and food-safe laminations.

The competitive field blends global chemical majors and specialized leaders; success hinges on sustainability credentials (EPDs, carbon neutrality), movement/adhesion validation for high-rise, and EV-ready thermal/dielectric performance. Integration of capacity expansions, targeted M&A, and application engineering is reshaping share capture in construction, transportation, and infrastructure.

Henkel couples scale (Loctite, Ceresit) with a pivot to solvent-free and bio-based systems aligned to 2030 sustainability goals. In 2025, it completed 50+ EPDs across construction, enabling specifiers to model embodied carbon and CPR compliance. The company spans retort-grade laminating adhesives and weatherproofing for building envelopes, with the Loctite Liofol LA 7837/LA 6265 (July 2025) system showcasing solvent-free, high-thermal packaging performance. Expect continued emphasis on regulatory readiness, EPD coverage, and high-stress sealing.

Sika leverages deep construction-chemicals integration (Sikaflex) for roofing, basement waterproofing, tunnels/bridges, and rapid project service. The MBCC integration accelerates synergy in concrete/waterproofing, while new facilities in Xi’an (September 2025) and Belo Horizonte (2025) de-risk regional supply and shorten critical-path schedules. Sika’s playbook—spec-driven performance, on-site technical service, and robust logistics—drives share in APAC/LatAm infrastructure.

H.B. Fuller’s strength lies in engineering adhesives and specialty sealants for IG, transportation, and door/window lines. The HS Butyl acquisition (August 2025) expands butyl-based tapes for building envelopes and renewables, complementing PU/elastic sealants for durable assemblies. With a strategy centered on high-growth construction and energy, Fuller aligns portfolios to low-temperature flexibility, UV durability, and installation speed.

Dow’s DOWSIL™ platform sets benchmarks in UV resistance, flexibility, and longevity for structural glazing and weathersealing. In June 2025, Dow expanded low-embodied-carbon lines and offers PAS 2060 certification—helping developers hit LEED/BREEAM targets while maintaining performance. Differentiation stems from validated movement capability, adhesion to challenging substrates, and design-assist collaboration for high-rise envelopes.

Bostik leads in Silyl Modified Polymer (SMP) sealants and elastic bonding that replace mechanical fasteners in automotive, rail, and marine. A capacity expansion in Southeast Asia (May 2025) supports regional transportation growth and general assembly. With four global R&D centers and 2.7% of sales to R&D, Bostik advances bio-based/low-VOC chemistries for waterproof flooring, tile systems, glazing, and high-performance tapes.

3M brings PSA expertise (VHB™, Extreme Sealing) to instant, water-tight field applications in RVs/trailers, HVAC, metalworking. 3M™ Industrial Sealing Tape IS1 (February 2025) uses a conformable acrylic that seals around fasteners and performs from −40 °F to 240 °F (−40 °C to 116 °C)—ideal for cold-climate installs. Strategic focus remains on application speed, reliability, and MRO efficiency, with ongoing innovation to align with environmental goals.

Country Analysis: Global Waterproof Adhesives and Sealants Industry Developments

China – Expanding Infrastructure Projects Fuel Demand for Advanced Polyurethane and Elastomeric Waterproofing Systems

China represents the largest and fastest-growing market for waterproof adhesives and sealants, driven by the government’s aggressive infrastructure investment and construction modernization programs. The surge in large-scale residential complexes, metro systems, and high-speed rail tunnels has accelerated demand for high-performance Polyurethane (PU) Sealants and Elastomeric Waterproofing Membranes. In a major expansion move, Sika AG acquired Shenzhen Landun Holding, enhancing its domestic footprint and product portfolio in China’s booming construction waterproofing market. The acquisition supports local production of high-strength waterproof adhesives aligned with China's increasing use of solvent-free, reactive waterproofing systems.

Chinese manufacturers are also shifting from bitumen-based materials to high-solid modified asphalt waterproofing sheets, improving durability and environmental performance. Government policies enforcing longer waterproofing lifespans in public housing projects have pushed the adoption of premium silicone and hybrid sealants capable of long-term adhesion even under extreme humidity. The growing use of Polyurea Spray Coatings in tunnels and subway systems demonstrates the market’s focus on rapid-curing, corrosion-resistant waterproof systems. Simultaneously, major domestic producers are investing in polymer dispersion facilities to supply low-VOC, water-based waterproof adhesives, while R&D initiatives explore self-healing hybrid sealants and sustainable concrete additives that support China’s national green building objectives.

Germany – European Leader in Sustainable Waterproofing and Automotive Sealing Technologies

Germany continues to dominate the European waterproof adhesives and sealants industry, underpinned by its strong automotive sector, infrastructure upgrades, and green building mandates. Henkel AG & Co. KGaA is leading innovation through its recyclable pressure-sensitive adhesives (PSAs) and CO₂-reducing waterproof adhesive systems, directly supporting the EU’s Circular Economy and Green Deal goals. The revised EU Construction Products Regulation (CPR) has accelerated adoption of low-emission, polyurethane foams and high-performance waterborne acrylic sealants designed for both construction and industrial applications.

The German automotive industry, a major consumer of advanced waterproof adhesives, is increasingly using reactive structural sealants for EV battery assembly, requiring high heat and chemical resistance. Infrastructure projects across the country demand elastomeric overlays and injection grouts for bridge deck waterproofing and repair. Companies are establishing digital innovation labs to enhance moisture-curing waterproofing formulations, while the impending ECHA restrictions on PFAS compounds are forcing chemical firms to reformulate traditional fluorinated waterproofing agents. With its focus on sustainable innovation, safety compliance, and precision engineering, Germany sets the European benchmark for next-generation waterproof adhesives and sealants.

United States – Growth Driven by Modular Building, Weatherproofing, and Green Construction Standards

The United States waterproof adhesives and sealants market is expanding rapidly due to strong residential construction, modular building adoption, and sustainability mandates. H.B. Fuller Company has announced major investment plans to strengthen its North American production capacity for hot melt and reactive polyurethane sealants, targeting the high-value construction and industrial assembly sectors. Similarly, Avery Dennison Performance Tapes introduced pressure-sensitive waterproof tapes engineered for metal building assemblies, capable of withstanding extreme weather fluctuations.

Innovation in Hybrid Silicone-Polyurethane (SPUR) and Silane Modified Polymer (SMP) formulations has positioned U.S. manufacturers at the forefront of UV-resistant and long-life waterproofing technologies. The country’s growing use of Liquid-Applied Waterproofing (LAW) systems in roofing and commercial construction reflects a shift toward seamless, rapid-curing membranes that reduce labor costs. In addition, EPA and LEED certification frameworks continue to influence adhesive chemistry, ensuring that new product lines are low-VOC and environmentally compliant. Beyond construction, UV-curable waterproof adhesives are increasingly used in electronic assemblies and displays, supporting waterproof device manufacturing and next-gen consumer electronics.

India – Infrastructure Expansion and Affordable Housing Accelerate Demand for Cost-Effective Waterproofing Solutions

India’s waterproof adhesives and sealants market is growing rapidly, driven by urbanization, infrastructure expansion, and affordable housing development. The government’s Smart Cities Mission and Housing for All initiatives have triggered extensive consumption of cementitious waterproofing slurries and polymer-modified mortars for basements, bathrooms, and rooftop applications. Pidilite Industries Ltd., a leading domestic player, continues to expand its nationwide distribution network, introducing DIY-friendly waterproofing solutions alongside professional-grade polyurethane and epoxy sealants.

The rapid rollout of metro rail and highway infrastructure projects has intensified demand for elastomeric joint sealants that maintain flexibility and watertight performance under dynamic structural movement. Additionally, the emphasis on cost-effective construction in affordable housing projects has prompted the development of water-based, synthetic rubber adhesives tailored for diverse substrates. Local R&D initiatives are strengthening India’s domestic manufacturing capabilities, reducing dependency on imported waterproofing materials. The growing presence of low-VOC and polymer-based formulations also aligns with India’s focus on sustainable construction practices and long-term building durability.

Japan – Advanced Seismic-Resistant Waterproofing and High-Tech Automotive Applications

Japan’s waterproof adhesives and sealants industry is characterized by its focus on precision, performance, and seismic resilience. The country’s stringent building codes and aging infrastructure necessitate the use of rapid-curing MS polymer sealants and acrylic-silicone hybrids for structural glazing and waterproofing joints in earthquake-prone regions. Japanese automotive manufacturers are heavy users of thermally conductive silicone sealants for electric vehicle (EV) battery sealing, ensuring both moisture and vibration resistance under extreme operating conditions.

In infrastructure repair, reactive epoxy injection resins are increasingly used for bridge and water tunnel restoration, enabling structural waterproofing with minimal downtime. Additionally, Japan’s focus on design aesthetics drives demand for translucent, weather-stable sealants suitable for exterior facades and glass applications. Through advanced material science and precision manufacturing, Japan remains a leader in high-durability waterproof adhesives that cater to both industrial and consumer sectors.

Switzerland – Global R&D Center for High-End Liquid Applied Membranes and Self-Healing Waterproofing Technologies

Switzerland, home to Sika AG, remains the innovation hub for high-end waterproof adhesives and sealants globally. Sika AG’s ongoing investments in self-healing elastomeric membranes and liquid-applied membrane (LAM) technologies have set international benchmarks for durability and long-term water resistance in both civil and commercial construction. The systems offer crack-bridging capabilities and superior UV stability, making them preferred solutions for tunnels, bridges, and industrial facilities.

Strategically, Sika’s global acquisitions — including firms in China and the United States — demonstrate its intent to localize production and technical expertise across key markets while maintaining its R&D leadership in Switzerland. With strong focus on performance innovation, sustainability, and scalability, the country continues to influence global standards for premium waterproof adhesives and sealants used in construction, transportation, and marine sectors.

Waterproof Adhesives & Sealants Market Report Scope

Waterproof Adhesives & Sealants Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$28.3 Billion

|

|

Market Size (2034)

|

$48.2 Billion

|

|

Market Growth Rate

|

6.1%

|

|

Segments

|

By Product Type (Adhesives, Sealants), By Chemistry - Adhesives (Epoxy, Polyurethane, Acrylic, PVA, SBC, EVA, Cyanoacrylate), By Chemistry - Sealants (Silicone, Polyurethane, Acrylic, Polysulfide, Butyl, SBC), By Technology (Water-Based, Solvent-Based, Hot Melt, Reactive, UV/Light Curable), By End-Use Industry (Building & Construction, Automotive, Electrical, Packaging, Consumer/DIY), By Application (Roofing, Flooring, Wall & Facade, Window & Door, Windshield, Battery, Pipe, Tunnel

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, Sika AG, H.B. Fuller Company, Arkema S.A., 3M Company, Dow Inc., Wacker Chemie AG, Huntsman Corporation, RPM International Inc., BASF SE, DuPont de Nemours, Inc., Mapei S.p.A., Pidilite Industries Ltd., Illinois Tool Works Inc., Avery Dennison Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Product Type

By Chemistry - Adhesives

- Epoxy

- Polyurethane

- Acrylic

- PVA

- SBC

- EVA

- Cyanoacrylate

By Chemistry - Sealants

- Silicone

- Polyurethane

- Acrylic

- Polysulfide

- Butyl

- SBC

By Technology

- Water-Based

- Solvent-Based

- Hot Melt

- Reactive

- UV/Light Curable

By End-Use Industry

- Building & Construction

- Automotive

- Electrical

- Packaging

- Consumer/DIY

By Application

- Roofing

- Flooring

- Wall & Facade

- Window & Door

- Windshield

- Battery

- Pipe

- Tunnel

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Waterproof Adhesives and Sealants Market-

- Henkel AG & Co. KGaA

- Sika AG

- H.B. Fuller Company

- Arkema S.A.

- 3M Company

- Dow Inc.

- Wacker Chemie AG

- Huntsman Corporation

- RPM International Inc.

- BASF SE

- DuPont de Nemours, Inc.

- Mapei S.p.A.

- Pidilite Industries Ltd.

- Illinois Tool Works Inc.

- Avery Dennison Corporation

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the global Waterproof Adhesives and Sealants Market with a decision-useful lens on sustainability pivots, EV-ready materials, and high-movement building envelopes; our analysis reviews technology performance under moisture, heat, and chemical stress, benchmarks embodied-carbon transparency, and maps sourcing risk to raw-material volatility; it also highlights application-specific requirements from roof and tunnel waterproofing to battery encapsulation and facade IG units, distilling breakthroughs in silane-terminated hybrids, underwater repair chemistries, and thermally conductive, electrically insulating sealants—making this report an essential resource for product managers, specifiers, and procurement leaders seeking validated performance metrics, regulatory alignment, and margin-safe adoption playbooks, etc……

Scope Highlights

Segmentation:

- By Product Type: Adhesives; Sealants

- By Chemistry – Adhesives: Epoxy; Polyurethane; Acrylic; PVA; SBC; EVA; Cyanoacrylate

- By Chemistry – Sealants: Silicone; Polyurethane; Acrylic; Polysulfide; Butyl; SBC

- By Technology: Water-Based; Solvent-Based; Hot Melt; Reactive; UV/Light Curable

- By End-Use Industry: Building & Construction; Automotive; Electrical; Packaging; Consumer/DIY

- By Application: Roofing; Flooring; Wall & Facade; Window & Door; Windshield; Battery; Pipe; Tunnel

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Horizon: Historic data 2021–2024 and forecasts 2025–2034.

Companies Covered (analysis/profiles of 15+): Henkel AG & Co. KGaA; Sika AG; H.B. Fuller Company; Arkema S.A.; 3M Company; Dow Inc.; Wacker Chemie AG; Huntsman Corporation; RPM International Inc.; BASF SE; DuPont de Nemours, Inc.; Mapei S.p.A.; Pidilite Industries Ltd.; Illinois Tool Works Inc.; Avery Dennison Corporation.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.