Advanced Ceramic Additives Market Overview: MV Growth, Energy-Efficient Sintering, and Toughening Performance

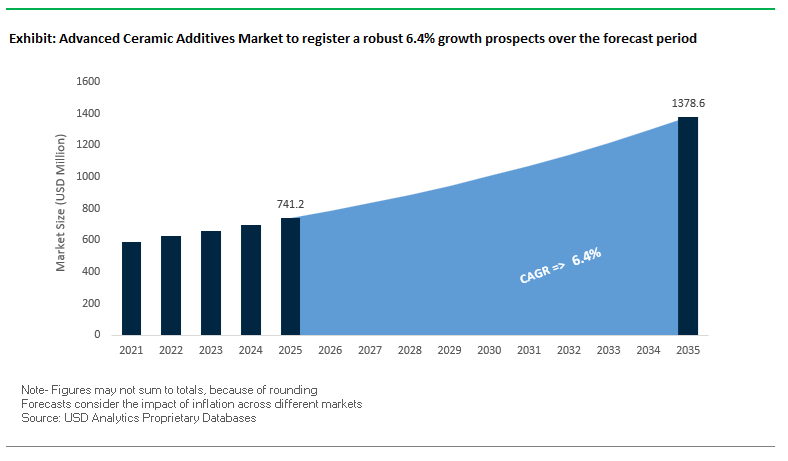

The Advanced Ceramic Additives Market is projected to grow from USD 741.2 million in 2025 to around USD 1,378.3 million by 2035, registering a robust CAGR of 6.4% (2025–2035). This growth is underpinned by the need for energy-efficient sintering, high-purity ceramic bodies, and reliable mechanical performance across technical ceramics, electronic ceramics, and advanced structural components. For manufacturers and vendors, additives such as sintering aids, binders, dispersants, toughening agents, and cold-sintering aids are becoming strategic value levers that directly influence yield, cycle times, and performance in end-use applications ranging from automotive catalysts and filters to solid-state batteries and semiconductor ceramics.

Advanced ceramic additive suppliers are increasingly tailoring their portfolios to support lower-temperature densification, higher solids loading, and improved fracture toughness, enabling customers to cut energy costs and improve throughput. Sintering aids now routinely cut sintering temperatures by up to 200°C versus traditional ~1,600°C alumina/zirconia firing, while Cold Sintering Process (CSP) routes demonstrate more than 90% energy savings by achieving densification below 300°C. At the same time, high-performance organic binders are formulated to leave less than 0.05% residual carbon after burnout, ensuring the color stability and purity demanded by high-value technical ceramics. Dispersant systems can lower slurry viscosity by up to 50% at 70 wt% solids, and transformation-toughening additives such as yttria-stabilized zirconia can double fracture toughness (from ~3 to ≥6 MPa·m½), making ceramic components more reliable under shock and cyclic loads.

Key insights for advanced ceramic additive manufacturers and vendors:

- Sintering aids that reduce firing temperature by up to 200°C are central to OEMs’ decarbonization and energy cost-reduction roadmaps in advanced ceramics manufacturing.

- Binder systems are being optimized to deliver <0.05% residual carbon post-burnout, minimizing defects, discoloration, and scrap in high-purity alumina, zirconia, and electronic ceramics.

- High-efficiency dispersants capable of cutting slurry viscosity by around 50% at 70 wt% solids loading are enabling more uniform tape casting, slip casting, and high-precision green shaping.

- Toughening additives such as YSZ are boosting alumina’s fracture toughness to ≥6 MPa·m½, significantly improving shock resistance and reliability in demanding mechanical and structural applications.

- Cold Sintering Process (CSP) using transient solvents as sintering aids is emerging as a disruptive low-temperature route, achieving densification below 300°C and offering >90% thermal energy savings versus conventional >1,000°C firing.

Advanced Ceramic Additives Market Analysis: Additive Manufacturing, SiC Value Chain, and Cold Sintering Momentum

The Advanced Ceramic Additives Market is being reshaped by the rapid industrialization of ceramic additive manufacturing (AM) and the shift from pilot to full-scale production. In October 2025, Bosch Advanced Ceramics forecast a 115% revenue increase for full-year 2025, explicitly linked to industrial adoption of AM technical ceramics, which depend on highly engineered binder and powder additive systems to control rheology, green strength, and burnout behavior. The AM Ceramics 2025 Conference (October 2025) further highlighted the transition from pilot to production in ceramic AM, with strong emphasis on robust binders, dispersants, and stabilizers as critical enablers of repeatable, high-volume manufacturing. In parallel, ongoing Desktop Metal–Nano Dimension merger discussions in 2025 signal strategic consolidation across the ceramic AM materials ecosystem, underscoring the importance of differentiated additive technologies.

Beyond AM, the market is seeing structural changes in Silicon Carbide (SiC) and lithium-related ceramic systems, both of which heavily rely on high-purity additives. The Linde–BASF collaboration (ongoing in 2025) aims to improve the purity and supply chain of precursors for SiC production, where dispersants, surfactants, and sintering aids directly influence defect levels in SiC powders and components. In November 2025, Saint-Gobain Ceramics and Eurodia Industrie announced a strategic partnership focused on direct lithium extraction (DLE), which is expected to boost demand for ceramic membranes and porous supports using tailored pore-forming and permeability-modifying additives. Additionally, Schunk’s acquisition of ESK-SIC (2024/2025) has strengthened the upstream SiC supply chain, where sintering additives such as carbon or boron remain critical to achieving the target density and microstructure in refractory, filtration, and high-temperature ceramics.

The third structural driver is the push towards next-generation ultra-high-temperature ceramics (UHTCs) and energy-saving processing technologies. In 2025, industry specialists reported growing activity around UHTC composite systems with fiber-reinforced matrices, designed to address the intrinsic brittleness of UHTCs in aerospace and hypersonic applications; this trend is increasing demand for wetting and sintering additives that ensure proper matrix infiltration and interfacial bonding. At the process level, Cold Sintering Process (CSP) is gaining traction as a viable industrial technology by late 2025, with academic and industrial research showing that transient solution additives can consolidate oxide ceramics at sub-300°C conditions. This is particularly attractive for solid-state battery electrolytes and other temperature-sensitive systems where conventional >1,000°C firing is incompatible with embedded components or cost targets. Collectively, these developments position advanced ceramic additives as a strategic enabler of both performance-critical applications and low-carbon manufacturing routes across the global advanced ceramics value chain.

Breakthroughs in Additive Formulations and Functional Nano-Modifiers Driving the Advanced Ceramic Additives Landscape

Market Trend 1: Engineering Ultra-Efficient Dispersants and Binders to Enable High-Solid-Loading Ceramic Additive Manufacturing

A defining trend in the Advanced Ceramic Additives Market is the rapid advancement of specialized dispersants and binders tailored for high-resolution ceramic additive manufacturing processes, including stereolithography (SL), direct ink writing (DIW), and paste-based deposition systems. Achieving ≥50 vol% solid loading is essential to minimize shrinkage during sintering and to reach the high relative densities required for structural-grade ceramics, and this is only possible through optimized dispersant chemistry that reduces viscosity without destabilizing the slurry. For example, PMAA-NH₄ dispersant at optimized loading levels can reduce slurry viscosity by 7–8× (from 2257 mPa·s to nearly 300 mPa·s), enabling precision flow characteristics needed for complex geometries.

Equally critical are clean-burnout binders engineered to follow first-order degradation kinetics between 300°C and 600°C, leaving ≤0.05 wt% residual ash, which prevents pore formation, crystal growth inhibition, and structural defects in the final ceramic. In DIW, dispersants must also impart precise shear-thinning behavior, allowing the material to extrude under high shear but hold its shape immediately after deposition—an essential characteristic for large overhangs and unsupported structures. These advancements collectively establish high-performance dispersant–binder systems as core enablers of next-generation ceramic AM scaling, minimizing print failures, improving dimensional fidelity, and supporting industrial adoption.

Market Trend 2: Integration of High-Aspect-Ratio Nano-Additives to Achieve Electrically and Thermally Conductive Ceramic Composites

A parallel trend reshaping the market is the integration of functional nano-additives, such as CNTs, graphene nanoplatelets (GNPs), boron nitride nanosheets, and metallic nanoparticles, to engineer ceramic composites with advanced electrical and thermal performance. Conductive nanomaterials exhibit a sharp jump in electrical conductivity at the percolation threshold, where increasing Ag nanoparticle loading from 0.01 to 0.05 vol% can elevate conductivity by 8–10 orders of magnitude (from 10⁻⁶ S/cm to hundreds of S/cm).

Thermal conductivity improvements are similarly impressive: graphene nanoplatelets at 30 wt% loading can yield 1,500% enhancement (from 0.5 W/m·K to 8.094 W/m·K). In materials like BN, anisotropic lamellar alignment can create 20× thermal conductivity differences depending on orientation—an effect controlled through additive morphology and slurry rheology.

High-aspect-ratio additives yield 100–1000× higher conductivity enhancement than spherical fillers due to their ability to form percolating networks at much lower loadings. This shift toward nanostructured conductive additives positions ceramics as viable materials for RF substrates, thermal management modules, EMI shielding components, and multifunctional structural systems.

Market Opportunity 1: Next-Generation Low-Temperature Sintering Aids for Co-Firing with Base Metals in MLCCs and Ceramic Capacitors

One of the highest-value opportunities in the Advanced Ceramic Additives Market is the development of low-temperature sintering aids that enable co-firing with base metals such as nickel and copper in multi-layer ceramic components (MLCCs). Additives like BaB₂O₄ or NiFe₂O₄ allow BaTiO₃ ceramics to achieve ≥94% relative density at temperatures 100–200°C lower than the traditional 1,250–1,350°C sintering range. Such reductions dramatically expand compatibility with low-melting metal electrodes, reducing component cost and improving electrical performance.

Furthermore, even at reduced temperatures, optimized additive loading (e.g., 0.1 mol% NiFe₂O₄) can retain a high dielectric constant (≈1,500), essential for capacitor miniaturization and energy storage efficiency. Emerging techniques like cold sintering enable densification at <250°C, cutting activation energy for densification by ≈10× versus conventional methods, opening a pathway to radically lower energy consumption.

Advanced BaTiO₃–Ni systems demonstrate dielectric constants of ≈11,000 at 1,200°C, with controlled grain sizes of 0.6–1.5 μm, reinforcing the opportunity for tailored microstructure control at sub-traditional temperatures. These advances align directly with electronics manufacturers’ shift toward energy-efficient, low-temperature ceramic processing for next-generation passive components.

Market Opportunity 2: Supply of Ultra-High-Purity, Phase-Stabilized Powders for Water-Based Tape Casting Applications

A second high-value opportunity lies in supplying high-purity, phase-stabilized ceramic powders optimized for aqueous tape casting—an increasingly preferred method for producing thin ceramic sheets for electronics, fuel cells, and substrates. By engineering surface-modified powders, manufacturers can achieve ≥60 wt% (≥40 vol%) solid loading while maintaining low viscosity (~100 mPa·s), enabling uniform tape flow and defect-free casting.

To meet semiconductor-grade requirements, powders must exhibit extremely low ionic contaminants, as even trace Na⁺ ions from binder systems can lead to conductivity failures. Dispersant-powder interactions must also achieve optimal Zeta potentials (e.g., −71 mV for Al₂O₃ slurries), enabling long-term slurry stability and preventing agglomeration in water-based systems.

Effective additives can increase green density from ~37% to ~65% of theoretical density, reducing the required sintering temperature by ~100°C and improving the uniformity of shrinkage during firing. The demand for defect-free, phase-stable ceramic tapes is expanding rapidly in high-performance markets such as MLCCs, LTCC substrates, SOFC membranes, laser packaging, and microelectronics—making advanced precursor powders a cornerstone opportunity for additive suppliers.

Advanced Ceramic Additives Market Share Analysis

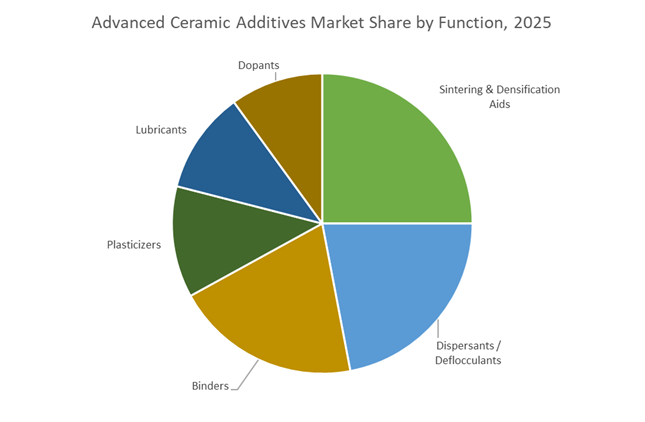

Market Share by Function: Sintering & Densification Aids Lead Due to Their Critical Role in Achieving High-Performance Ceramic Microstructures

Sintering & Densification Aids account for the largest share of the advanced ceramic additives market—approximately 25% in 2025—because they are indispensable for transforming ceramic powders into fully dense, high-performance materials that meet the demanding mechanical, electrical, and thermal requirements of advanced applications. These additives accelerate atomic diffusion during sintering, promoting grain boundary mobility and eliminating internal porosity—factors that directly determine the final ceramic’s strength, toughness, dielectric performance, and thermal reliability. Their ability to create a temporary liquid phase is particularly crucial for processing non-oxide ceramics like silicon carbide (SiC) and silicon nitride (Si₃N₄), materials that naturally require extremely high sintering temperatures. By lowering these temperatures by several hundred degrees, densification aids reduce energy consumption, extend furnace life, and significantly improve the cost-efficiency of high-volume ceramic manufacturing. Moreover, their role in microstructural control ensures uniform, fine-grained ceramics that deliver consistent performance in applications ranging from transparent armor to semiconductor wafer chucks. As industries push for higher reliability, tighter tolerances, and enhanced durability, densification aids remain the cornerstone additive category driving the adoption and scalability of next-generation advanced ceramics.

Market Share by End-Product Application: Electronics & Semiconductor Sector Dominates Due to High-Purity, High-Precision Material Requirements

The Electronics & Semiconductor industry accounts for roughly 35% of global advanced ceramic additive demand, driven by its dependence on precision-engineered ceramics with tightly controlled electrical, thermal, and structural properties. Advanced ceramics such as alumina, aluminum nitride, barium titanate, and silicon carbide are essential materials across the value chain—from substrates and insulators in power electronics to the MLCCs embedded in every smartphone, EV, and data center device. These components rely heavily on additives to optimize dielectric constant, thermal conductivity, grain uniformity, and sintering behavior, ensuring the reliability and miniaturization required in modern electronic architectures. In semiconductor fabrication, ceramic components used in etching tools, plasma chambers, deposition systems, and wafer handling equipment must withstand corrosive chemistries, high temperatures, and plasma environments without degrading—necessitating extremely pure and precisely tailored ceramic materials made possible by specialized additives. Rapid expansion of 5G networks, AI accelerators, IoT devices, advanced packaging technologies, and EV power modules further amplifies demand for high-performance ceramics, solidifying the Electronics & Semiconductor sector as the largest and most technologically intensive consumer of ceramic additives globally.

Country Analysis: Global Advancement Drivers in the Advanced Ceramic Additives Market

United States: National Lab Leadership, Additive Manufacturing Expansion, and Defense-Grade UHTC Development

The United States remains a dominant innovation hub in the Advanced Ceramic Additives Market, supported by federal research programs, hypersonic defense initiatives, and rapid progress in ceramic additive manufacturing. Leading national laboratories—Oak Ridge National Laboratory (ORNL) and Lawrence Livermore National Laboratory (LLNL)—have intensified efforts to optimize binder jetting, multi-material AM, and vat-photopolymerization pathways, driving demand for ceramic additives that enhance green part strength, sintering density, and microstructural uniformity. From 2021 to 2025, these labs have accelerated R&D into specialized additives for Silicon Carbide (SiC)-based embedded sensor architectures and next-generation structural ceramics, establishing the U.S. as a global leader in ceramic AM research.

The scaling of SiC power electronics manufacturing for EVs further amplifies demand for advanced sintering aids, grain growth modifiers, and dopants that enable defect-free ceramic substrates with high conductivity and high thermal stability. In defense, U.S. government agencies continue to increase funding for Ultra-High Temperature Ceramics (UHTCs) designed for hypersonic vehicles, propulsion systems, and thermal protection structures. These programs rely on precision-controlled precursor chemistries and specialized ceramic additives capable of withstanding environments up to 3,000°C, reinforcing the U.S. strategic position in high-temperature ceramics. Commercial AM suppliers like Tethon 3D are also expanding proprietary resins and ceramic slurry systems for Zirconia, Alumina, and Si3N4, enabling broader commercialization of advanced ceramic components across aerospace, industrial, and medical sectors.

China: Solid-State Battery Investment, Electronics Miniaturization, and High-Volume Structural Ceramic Production

China continues to scale rapidly in the Advanced Ceramic Additives Market, leveraging its massive manufacturing ecosystem and state-backed research initiatives. A major technological focus centers on solid-state EV batteries, where Chinese institutions are developing oxide and sulfide ceramic electrolytes—including LLZO (Lithium Lanthanum Zirconium Oxide)—that require specialized ceramic additives to enhance ionic conductivity, co-firing compatibility, and densification behavior. These additives are essential for producing next-generation solid-state electrolytes with consistent performance and manufacturability at gigafactory scale.

China’s global dominance in electrical and electronics manufacturing also drives significant demand for high-purity binders, dispersants, and anti-agglomeration additives used in Multi-Layer Ceramic Capacitors (MLCCs). As MLCC feature sizes shrink, additives play a critical role in maintaining slurry homogeneity, particle dispersion, and dielectric performance. Meanwhile, structural ceramics production—including SiC armor plates and high-strength industrial ceramics—continues to expand through companies such as Shenzhen Sinoma Advanced Materials, which rely on high-performance processing aids, grain modifiers, and ceramic powder conditioning agents to support volume manufacturing. Together, solid-state battery development and electronics miniaturization position China as one of the fastest-growing markets for advanced ceramic additives.

European Union (Germany & Austria): High-Precision Ceramic AM Leadership and Energy Technology Additive Optimization

Europe’s Advanced Ceramic Additives market is defined by innovation in precision ceramic additive manufacturing and high-performance energy systems. Lithoz GmbH (Austria) remains the global leader in Lithography-based Ceramic Manufacturing (LCM), developing proprietary high-resolution ceramic slurry systems for Zirconia, Alumina, Hydroxyapatite, and custom technical ceramics. These formulations depend heavily on advanced additives—photoinitiators, dispersants, stabilizers, polymer networks—to achieve exceptional surface quality, microstructural precision, and reliability in aerospace, medical, and micro-engineering applications. Europe’s leadership in LCM is transforming how high-value ceramic components are designed and manufactured.

In parallel, the Fraunhofer IKTS (Germany) is pioneering ceramic additive technologies for Solid Oxide Fuel Cells (SOFCs) and solid-state battery electrolytes, optimizing glass-ceramic additives such as NaYPSiO to improve ionic transport, mechanical integrity, and manufacturability. Europe’s emphasis on energy transition and hydrogen infrastructure further increases demand for specialized ceramic additives in high-temperature electrolyzers, membranes, and thermal barrier systems. Strategic acquisitions—such as Schunk’s acquisition of ESK-SIC in 2024—underscore Europe’s commitment to securing high-purity SiC powder supply for advanced ceramics and AM applications. This ecosystem positions Europe at the forefront of precision manufacturing, energy ceramics, and sustainable high-performance material innovation.

Japan: LTCC Additive Excellence, SiC Wafer Expansion, and High-Reliability Automotive Ceramics

Japan remains a global center for high-performance electronic ceramics, driven by its unmatched expertise in fine ceramic processing and strict material reliability standards. Japanese companies such as Murata Manufacturing lead innovation in Low-Temperature Co-fired Ceramic (LTCC) materials, where specialized glass-ceramic additives enable low sintering temperatures while maintaining high dielectric performance and multilayer circuit integrity. These additives are essential for RF modules, antenna components, and miniaturized electronic systems used across telecommunications, smartphones, and emerging IoT applications.

Japan’s surge in SiC semiconductor wafer production—supported by Kyocera’s new smart factory and wafer slicing investments (2024–2025)—creates substantial demand for sintering aids, dopants, and slurry additives that ensure crystal uniformity and defect minimization. In automotive applications, Japanese manufacturers are investing heavily in Silicon Nitride (Si3N4) components for turbocharger rotors, bearings, and engine thermal systems. Producing these parts requires advanced polymer binders, pressing additives, and sintering agents to achieve exceptional thermal shock resistance and strength-to-weight ratios. These competencies position Japan as a critical innovation hub for both electronic and automotive ceramic additive technologies.

Competitive Landscape in Advanced Ceramic Additives: Chemical Majors Enabling High-Purity Ceramic Processing

The competitive landscape of the Advanced Ceramic Additives Market is dominated by global chemical and materials majors that leverage deep expertise in colloid chemistry, polymers, nanomaterials, and high-purity powders. Players such as BASF, Dow, Solvay, Evonik, and Saint-Gobain supply the dispersants, binders, sintering aids, rheology modifiers, and specialty grains that determine yield, energy consumption, and final part performance in advanced ceramics. Their strategies span from high-solids-loading dispersant design and low-VOC binder systems to nanoparticle-based densification enhancers and functional additives for SiC, solid-state batteries, and filtration ceramics. Partnerships and M&A—such as Saint-Gobain’s collaboration in DLE and Schunk’s acquisition of ESK-SIC—are consolidating control over high-value ceramic raw materials and additive technologies, creating an increasingly integrated ecosystem that supports both traditional high-temperature firing and emerging CSP/AM processes.

BASF SE: Advanced Dispersants and Ceramic Slurry Additives Powering High-Solid Technical Ceramics

BASF is a leading global chemical company and a key supplier of dispersants, binders, defoamers, and precursor materials to the advanced ceramic additives market. Its portfolio includes polyacrylate and polycationic polymer dispersants, wax- and resin-based binders, and defoaming agents that enable stable, high-solids ceramic slurries for tape casting, slip casting, and other shaping routes. Leveraging strong know-how in colloid and surface chemistry, BASF designs polymer additives that fine-tune rheology and particle packing, thereby reducing porosity and improving densification. The company also provides catalyst washcoat additives to optimize dispersion and viscosity in slurries used for automotive catalytic converters and diesel particulate filters (DPF). Strategically, BASF is investing in high-purity additives and precursor materials for SiC production, aligning its advanced ceramic additives offering with growth in EV power electronics and high-efficiency DC chargers.

Dow Inc.: Binder and Rheology Solutions for Extruded, Pressed, and Porous Technical Ceramics

Dow is a major provider of specialty polymers and formulated solutions that serve as critical binders and dispersants in technical and refractory ceramics. Its portfolio features cellulose ether binders (e.g., Methocel and Walocel families) widely used in extrusion, pressing, and tape casting where they impart excellent green strength and plasticity to unfired ceramic bodies. Dow’s water-soluble binder systems are engineered to ensure dimensional stability and mechanical robustness during forming and handling. The company is also a key supplier of binder and stabilizer systems for the production of ceramic foams and porous structures used in industrial filtration and high-temperature insulation, where controlled pore structure is critical. With a growing focus on environmentally preferred polymers, including non-ionic surfactants that help cut VOC emissions during binder burnout, Dow positions itself as a sustainability-focused partner for ceramic manufacturers transitioning to greener processing routes.

Solvay S.A.: High-Performance Dispersants for Non-Oxide Ceramics and Additive Manufacturing

Solvay brings strong capabilities in high-performance polymers and functional additives to the advanced ceramic additives industry, particularly for demanding non-oxide systems. It supplies fluorinated and sulfonated polymers as specialty dispersants and wetting agents for challenging formulations involving non-oxide ceramics such as SiC and Si₃N₄ and nano-scale powders. Solvay’s core strength lies in highly efficient dispersants that support ultra-high solids loading in ceramic suspensions, which is key to achieving high final density and reduced shrinkage after sintering. The company is also a critical additive supplier for processing SiC and Si₃N₄ powders used in high-strength engine components and power electronics. Strategically, Solvay is investing in new polymer additives tailored for ceramic additive manufacturing (DLP, binder jetting, and related technologies), ensuring that ceramic slurries and binders exhibit the rheological stability and green strength required for industrial-scale 3D printing.

Evonik Industries AG: Nanoparticle-Based Ceramic Additives for Electronic and High-Density Ceramics

Evonik is a specialty chemicals leader with a strong portfolio of nanomaterials, additives, and functional materials targeted at ceramics, coatings, and adhesives. In advanced ceramics, it offers silica and alumina oxide nanoparticles (such as AEROSIL) used as rheology modifiers and sintering aids, as well as specialty binders and surfactants. Evonik’s core strength lies in producing high-purity nanoscale ceramic additives that help control grain growth and enhance densification at lower temperatures, enabling finer microstructures and improved mechanical and electrical properties. The company is a key additive supplier to electronic ceramics, including multilayer ceramic capacitors (MLCCs) and piezoelectric components, where subtle compositional changes can significantly impact electrical performance. Its strategic focus on sustainability and circularity has led to additive solutions that reduce energy consumption in ceramic processing, for example by supporting low-temperature sintering and more efficient firing cycles.

Saint-Gobain: Specialty Grains, Powders, and Additives for Thermal Management and Filtration Ceramics

Saint-Gobain, while renowned for finished ceramics and refractories, is also a significant player in specialty grains and powders that serve as functional additives and reinforcing agents in the advanced ceramic additives market. Through its specialty grains and powders unit, it supplies high-purity oxide and non-oxide powders, including boron nitride and zirconium oxide, which act as sintering aids, reinforcement phases, and thermal management fillers. The November 2025 partnership with Eurodia Industrie on direct lithium extraction (DLE) highlights Saint-Gobain’s focus on separation and filtration ceramics, which require tailored pore-forming and permeability-modifying additives to hit performance targets. Leveraging deep expertise in high-temperature processing, the company ensures high chemical and phase purity for its specialty grains and sintering aids used in refractory and metallurgical applications. In thermal management, boron nitride additives from Saint-Gobain are highly valued for combining high thermal conductivity with electrical insulation, making them key fillers in polymer/ceramic composites for heat sinks and EV-related applications.

Advanced Ceramic Additives Market Report Scope

Advanced Ceramic Additives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$741.2 Million

|

|

Market Size (2035)

|

$1378.3 Million

|

|

Market Growth Rate

|

6.4%

|

|

Segments

|

By Function (Binders, Dispersants/Deflocculants, Sintering & Densification Aids, Lubricants, Plasticizers, Dopants), By Ceramic Manufacturing Process (Dry Pressing/Isostatic Pressing, Tape Casting, Slip Casting/Extrusion, Additive Manufacturing, Gel Casting), By End-Product Application (Electronics & Semiconductor, Energy Storage, Aerospace & Defense, Medical & Dental Ceramics, Industrial & Chemical Components)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Dow, Evonik, Solvay, Ashland, Kyocera, CeramTec, Sanyo Chemical, Bozzetto Group, Brenntag (Univar), Morgan Advanced Materials, Lithoz, 3M, Bentonite Performance Minerals, Wacker Chemie

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Advanced Ceramic Additives Market Segmentation

By Function

- Binders

- Dispersants / Deflocculants

- Sintering & Densification Aids

- Lubricants

- Plasticizers

- Dopants

By Ceramic Manufacturing Process

- Dry Pressing / Isostatic Pressing

- Tape Casting

- Slip Casting / Extrusion

- Additive Manufacturing

- Gel Casting

By End-Product Application

- Electronics & Semiconductor

- Energy Storage

- Aerospace & Defense

- Medical & Dental Ceramics

- Industrial & Chemical Components

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Advanced Ceramic Additives Market

- BASF SE

- Dow

- Evonik

- Solvay

- Ashland

- Kyocera

- CeramTec

- Sanyo Chemical

- BOZZETTO Group

- Brenntag (Univar)

- Morgan Advanced Materials

- Lithoz

- 3M

- Bentonite Performance Minerals

- Wacker Chemie.

*- List not Exhaustive

Research Coverage: Advanced Ceramic Additives Market

This USDAnalytics report investigates the global Advanced Ceramic Additives Market in depth, providing quantitative and qualitative analysis reviews of demand for sintering aids, binders, dispersants, toughening agents, dopants, and cold-sintering additives across electronics, energy storage, aerospace, medical, and industrial applications. It highlights how breakthroughs in low-temperature densification, high-solid-loading slurries, and nano-modified formulations are reshaping ceramic manufacturing economics, enabling energy-efficient firing, improved microstructural control, and higher yield in technical ceramics and semiconductor-grade components. The study examines value chain shifts linked to ceramic additive manufacturing, SiC and solid-state battery ecosystems, and ultra-high-purity additive requirements for advanced electronic ceramics, while mapping regulatory, sustainability, and decarbonization drivers that are pushing OEMs toward next-generation additive chemistries. It further evaluates competitive strategies of leading chemical majors and specialist ceramics companies, including product portfolio evolution, partnership models, and technology roadmaps, and benchmarks their positioning by function, process route, and end-use sector. With comprehensive market sizing, price and margin commentary, technology benchmarking, and regional adoption patterns, this report highlights critical growth pockets, risk factors, and strategic opportunities, making it an essential resource for business leaders, R&D heads, and investment stakeholders seeking to understand where value will accrue in advanced ceramic additives over 2026–2034.

Scope Highlights

- Segmentation

By Function – Binders; Dispersants / Deflocculants; Sintering & Densification Aids; Lubricants; Plasticizers; Dopants

By Ceramic Manufacturing Process – Dry Pressing / Isostatic Pressing; Tape Casting; Slip Casting / Extrusion; Additive Manufacturing; Gel Casting

By End-Product Application – Electronics & Semiconductor; Energy Storage; Aerospace & Defense; Medical & Dental Ceramics; Industrial & Chemical Components

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

- Time Horizon: Historic data from 2021 to 2025 and forecast data from 2026 to 2034.

- Company Coverage: Analysis and profiles of 15+ key participants across the global Advanced Ceramic Additives value chain.