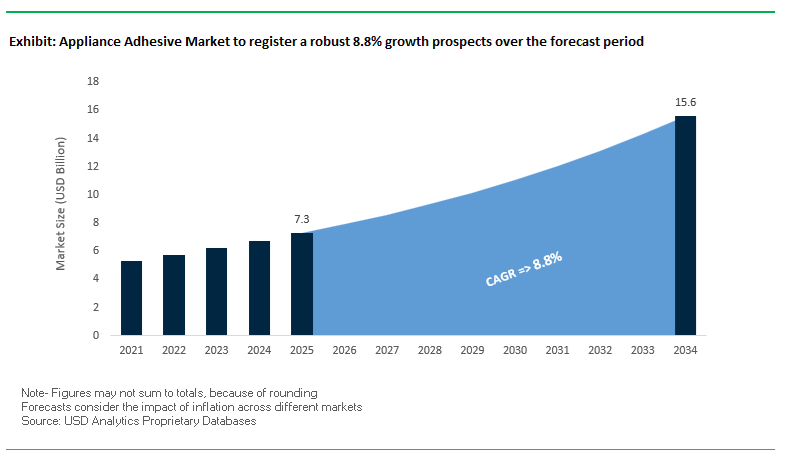

The global appliance adhesive market is projected to expand from USD 7.3 billion in 2025 to USD 15.6 billion by 2034, registering a strong 8.8% CAGR, as appliance OEMs transition away from mechanical fastening toward structural bonding, sealing, and encapsulation technologies that support lightweighting, energy efficiency, and automated high-volume manufacturing. Adhesives have become integral to appliance design, enabling thinner housings, mixed-material assemblies, and improved noise, vibration, and durability performance across refrigeration, laundry, cooking, HVAC, and smart home appliances.

Manufacturers such as Henkel, Sika, H.B. Fuller, Dow, Wacker, and 3M position appliance adhesives as process enablers, not just joining materials. UV-curable acrylic adhesives are widely deployed on automated assembly lines for display bonding, plastic housings, touch panels, and decorative trims, delivering fixture strength in <15 seconds and enabling inline optical inspection and immediate downstream handling. This rapid cure capability directly supports higher line speeds and reduced work-in-process inventory in appliance electronics and user-interface modules.

Thermal durability remains a defining performance criterion, particularly in cooking appliances and heat-generating systems. High-temperature silicone sealants specified by appliance OEMs retain elasticity and adhesion across −65 °C to +315 °C, maintaining seal integrity under repeated thermal cycling, vibration, and long service life expectations. These materials are critical in ovens, cooktops, exhaust paths, and heat-shielding interfaces, where conventional organic adhesives fail. At the same time, regulatory compliance and indoor air-quality standards are reshaping adhesive selection.

Appliance manufacturers are accelerating the adoption of low-VOC polyurethane systems and water-based adhesives, particularly in Europe and North America, where compliance with REACH, RoHS, and consumer exposure limits is mandatory. OEM procurement data indicates double-digit growth in low-VOC formulations, driven by sustainability mandates and corporate decarbonization targets.

The Appliance Adhesive Industry is undergoing rapid technological transformation, with major adhesive manufacturers investing in high-performance formulations, automation-ready solutions, and eco-compliant systems to meet the growing complexity of modern appliance manufacturing. In October 2025, H.B. Fuller announced a US$50 million investment to expand Reactive Hot Melt (RHM) production capacity across Asia-Pacific, a move aimed at supporting the region’s electronics and smart appliance manufacturing hubs. These RHMs offer exceptional flexibility, heat resistance, and curing speed, perfectly aligning with the shift toward connected home appliances and automated production lines.

In September 2025, 3M launched a single-part structural acrylic adhesive line designed to bond low surface energy plastics like polypropylene — common in refrigeration components and HVAC drain pans — eliminating the need for surface primers. This primer-less bonding technology significantly enhances process efficiency and reduces material waste. Meanwhile, in August 2025, the U.S. Environmental Protection Agency (EPA) issued updated regulations on solvent-based adhesive systems, propelling manufacturers toward moisture-curing and 100% solids formulations, especially in industrial and heavy-duty appliances where regulatory compliance and sustainability have become critical competitive differentiators.

In July 2025, Sika AG completed the acquisition of a German adhesives dispensing equipment manufacturer, strengthening its offering in automated adhesive application systems for dishwasher and laundry assembly lines. Similarly, in June 2025, Dow (Dowsil) introduced a thermally conductive silicone gap filler for inverter-driven air conditioners, engineered for efficient heat dissipation in power modules and circuit boards. These innovations are crucial for enhancing energy efficiency and reliability in high-performance home appliances.

Henkel, in May 2025, launched a patented instant adhesive system under its Loctite brand, engineered for metal-to-glass bonding in premium kitchen ranges and cooktops, offering superior moisture and thermal resistance. Earlier, in April 2025, Covestro, in collaboration with Asian OEMs, validated the long-term energy-saving performance of polyurethane foam-in-place gaskets (FIPG) for freezer and refrigerator lids, reinforcing the market shift toward airtight sealing and energy efficiency. Finally, in March 2025, PPG Industries began pilot production in Mexico for corrosion-resistant waterborne coatings and sealants, targeting outdoor HVAC units and industrial appliances — a strategic move supporting global supply chain localization.

The industry is undergoing a decisive transition toward low-VOC (volatile organic compound) and solvent-free adhesive systems in response to tightening global indoor air quality regulations. Agencies such as the U.S. Environmental Protection Agency (EPA) have established stringent VOC thresholds, requiring adhesives to contain less than 20 g/L of VOCs (excluding water and exempt compounds). The benchmark is reshaping adhesive manufacturing practices, especially for indoor appliance assembly, where compliance with LEED and Greenguard certification standards is increasingly mandatory.

Leading adhesive producers are replacing traditional solvent-based formulations with waterborne and 100% solids technologies, designed to meet both environmental and occupational safety objectives. A prominent example is the adoption of Polyurethane Reactive (PUR) hot-melt adhesives, which offer zero VOC emissions, rapid curing, and exceptional mechanical strength—critical for applications such as panel lamination, motor assembly, and frame bonding in refrigerators, washing machines, and dishwashers.

These new PUR adhesive systems not only eliminate volatile solvents but also enhance thermal resistance, durability, and productivity, offering superior bonding performance in high-speed manufacturing lines. The chemical shift toward reactive hot melts marks a pivotal advancement, allowing appliance OEMs to maintain high structural integrity while adhering to sustainable manufacturing principles.

As consumers and regulatory agencies place a premium on health and sustainability, the widespread use of low-emission adhesives positions manufacturers favorably in both consumer and B2B markets. In addition, the aligns with the appliance sector’s growing emphasis on eco-label certification and lifecycle sustainability, ensuring long-term competitiveness across global markets.

The appliance industry is witnessing a structural transformation in assembly design—driven by lightweighting imperatives, noise reduction goals, and aesthetic flexibility. Modern OEMs are adopting structural adhesives to replace traditional fastening techniques such as screws, rivets, and welds, optimizing both performance and design freedom.

Advanced two-part epoxy and acrylic adhesives are enabling the construction of modular and hybrid assemblies, helping appliance manufacturers achieve notable weight savings. Similar to innovations observed in automotive assembly, structural bonding in appliance modules has demonstrated weight reductions of 3–10 kg per unit, leading to improved energy efficiency and operational performance.

In addition to mechanical benefits, these adhesives offer superior NVH (Noise, Vibration, and Harshness) characteristics—critical for enhancing the consumer experience in high-end home appliances. Flexible polyurethane and epoxy-based structural adhesives effectively dampen vibrations and reduce noise output, ensuring quieter operation in premium washing machines, dishwashers, and refrigeration units.

Further, the ability of these adhesives to bond dissimilar materials (e.g., metals, composites, and thermoplastics) allows manufacturers to pursue innovative designs without compromising on strength or durability. Structural adhesives thus enable appliance OEMs to meet multiple objectives—reducing assembly complexity, improving aesthetics, and enhancing product longevity—positioning them as an essential enabler of the modern appliance production ecosystem.

The rapid adoption of energy-efficient heat pump systems in HVAC and appliance applications is creating a high-value segment for high-temperature, chemically resistant adhesive systems. As global energy policies prioritize decarbonization, demand for heat pumps and hybrid HVAC systems is surging—requiring adhesives that perform reliably under extreme thermal cycles and chemical exposure.

In the domain, epoxy and anaerobic adhesives have become indispensable for bonding and sealing heat exchangers, copper tubing, and compressor housings. Certain aerospace-grade epoxy systems used in heat pump manufacturing demonstrate continuous operational stability at temperatures up to 180°C (350°F) while maintaining resistance to refrigerants, coolants, and oils—capabilities that conventional mechanical fasteners cannot achieve in thin-walled or pressure-sensitive assemblies.

A critical engineering challenge lies in bonding dissimilar materials, such as aluminum fins to copper tubing, without galvanic corrosion. Adhesives uniquely provide non-conductive, corrosion-resistant interfaces, enhancing thermal performance while maintaining mechanical integrity. Modern formulations achieve shear strengths exceeding 40 MPa (6,000 psi) on steel substrates, supporting the miniaturization and performance optimization of next-generation thermal appliances.

With global markets investing heavily in heat pump installations, particularly in Europe and North America, adhesive suppliers have a unique opportunity to penetrate the fast-growing segment by developing thermally conductive, chemically resilient, and VOC-compliant formulations specifically tailored for thermal management systems.

The digital transformation of the appliance sector—marked by IoT connectivity, smart sensors, and AI-driven control systems—is creating robust growth potential for functional adhesives designed for electronics assembly, thermal management, and structural integrity in compact devices.

Modern appliances integrate an increasing number of sensors for temperature, motion, and load control, each requiring precise bonding and heat dissipation mechanisms. The has led to a rising demand for Electrically Conductive Adhesives (ECAs) and Thermally Conductive Adhesives (TCAs) that ensure reliable signal transmission, electrical insulation, and efficient heat dissipation in confined spaces. Nano-enhanced conductive adhesives are emerging as lead-free alternatives to solder, providing superior thermal and electrical properties while enabling flexible bonding between substrates with different coefficients of thermal expansion.

In addition, leading adhesive manufacturers are investing in smart manufacturing technologies that integrate mix-ratio monitoring sensors and real-time curing diagnostics into adhesive dispensing systems. These innovations provide time-stamped traceability and ensure process reliability, a crucial advantage in high-volume smart appliance production where every assembly unit demands quality verification and consistent performance.

With IoT and AI-enabled appliances becoming mainstream, the need for precision bonding, vibration stability, and electronic safety compliance is expanding rapidly. The positions functional adhesives as a cornerstone technology in the next phase of smart home innovation—blending electronic reliability, miniaturization, and environmental sustainability.

Appliance Adhesive Market Share Insights, 2025-2034

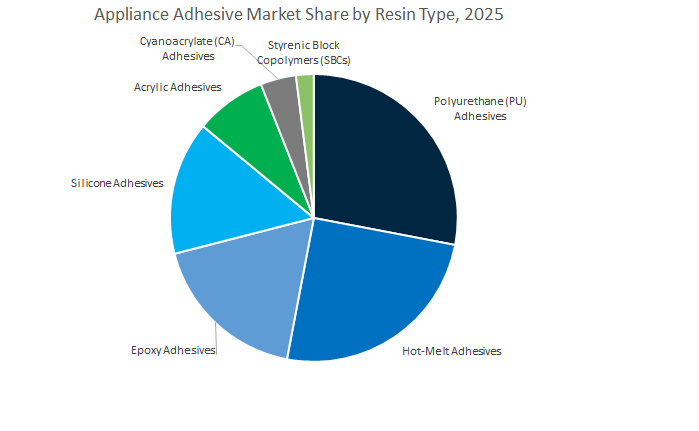

The polyurethane (PU) adhesives segment dominates the global appliance adhesive industry, commanding approximately 28% of the total market share in 2025. Polyurethane’s unmatched versatility, flexibility, and superior bonding performance across dissimilar substrates—such as metals, plastics, foams, and glass—make it indispensable in appliance manufacturing. PU adhesives are especially vital in refrigerators and freezers, where they are used in foam insulation panels, door seals, and structural bonding to ensure energy efficiency and long-term durability. Their gap-filling ability, chemical resistance, and excellent adhesion to coated metals make them the preferred choice for both structural and semi-structural bonding. Additionally, PU adhesives support low-VOC and solvent-free formulations, aligning with sustainability goals and regulatory compliance (such as REACH and EPA standards). The growing global emphasis on energy-efficient, lightweight, and quieter appliances continues to strengthen the dominance of polyurethane-based adhesives. Manufacturers favor PU chemistries for their ability to deliver shock absorption, flexibility, and long-term reliability—key attributes in extending appliance lifespans and minimizing field failures in both residential and commercial applications.

The hot-melt adhesives segment, accounting for around 25% of market share, represents the fastest-growing category within the appliance adhesives industry. Hot melts are the preferred choice for high-speed automated manufacturing, offering instant bonding, minimal waste, and strong adhesion to a variety of substrates. Their rapid setting time makes them ideal for non-structural assembly tasks such as wire harnessing, insulation placement, panel lamination, and trim attachment—critical processes on modern appliance production lines. Hot-melt technologies, particularly those based on ethylene-vinyl acetate (EVA), polyamide, and styrenic block copolymers (SBCs), provide an excellent balance of performance and cost-effectiveness. The growing adoption of reactive hot-melt adhesives (RHMAs) is further expanding this segment, as they offer enhanced temperature resistance and durability comparable to traditional liquid adhesives. Hot melts also support environmentally friendly and solvent-free processing, reducing production cycle times while improving worker safety. As appliance OEMs continue to pursue lean manufacturing and automation efficiency, hot-melt adhesives remain at the forefront of production optimization and lightweight material bonding innovations.

The epoxy and silicone adhesives segment is a technically critical pillar of the appliance adhesives market, with epoxies providing the high shear strength, chemical resistance, and thermal stability required for motor assembly, metal bonding, and component encapsulation in compressors, heating elements, and electrical housings, while silicone adhesives deliver superior elasticity, dielectric properties, and temperature resistance for sealing, gasketing, and vibration damping in ovens, dryers, and cooktops. Both chemistries are advancing through fast-curing, hybrid, and low-VOC innovations that support higher manufacturing throughput and improved energy efficiency. In parallel, acrylic, cyanoacrylate, and SBC-based adhesives form a specialized segment serving targeted, high-value applications such as decorative panel mounting, trim attachment, nameplate bonding, precision electrical assembly, and flexible bonding of plastics and rubbers. With attributes including moisture resistance, UV stability, rapid curing, and enhanced elasticity, these formulations, though lower in volume, remain essential to modern appliance design and performance.

The residential appliances segment is the undisputed leader in the global appliance adhesive market, accounting for a commanding 74.3% of total market share in 2025. This dominance is driven by the sheer volume of household appliances produced annually—ranging from refrigerators, washing machines, and microwaves to air conditioners, dishwashers, and water heaters. Adhesives in this segment must balance cost-effectiveness, process efficiency, and regulatory compliance, as they are extensively used in panel bonding, insulation foam lamination, motor assembly, vibration damping, and component sealing. Residential manufacturers prioritize adhesives that offer fast curing, strong adhesion to coated metals and plastics, and compatibility with automated dispensing systems, enabling efficient, high-throughput production. Furthermore, the global shift toward energy-efficient and environmentally friendly home appliances has accelerated demand for low-VOC, halogen-free, and recyclable adhesive systems. With appliance manufacturers investing heavily in smart home technologies and aesthetic design innovations, adhesives play an increasingly vital role in enabling seamless integration of sensors, displays, and composite materials, reinforcing this segment’s long-term market leadership.

The commercial appliances segment represents a high-performance, lower-volume but higher-value market, focused on professional-grade equipment such as industrial refrigerators, commercial ovens, dishwashers, and laundry systems. Adhesives in this segment are engineered for extended duty cycles, high thermal loads, and frequent mechanical stress, far exceeding residential requirements. Epoxy and silicone systems dominate this category due to their durability, temperature stability, and resistance to aggressive cleaning chemicals commonly used in food service and hospitality environments. The segment’s growth is being propelled by urbanization, rising foodservice establishments, and expansion of healthcare facilities, all of which require reliable, high-capacity appliances. Additionally, the move toward automated, energy-efficient commercial equipment—such as self-cleaning ovens and digital refrigeration systems—has intensified the need for electrically insulating and thermally stable adhesives. As OEMs prioritize downtime reduction and long-term operational reliability, adhesive formulations tailored for longevity, moisture resistance, and vibration control are becoming key differentiators in the commercial appliance market.

The industrial (OEM) assembly segment, though the smallest by volume, serves as a strategically specialized niche in the global appliance adhesives industry. This segment involves adhesives used in custom or integrated appliance components that are part of larger machinery or industrial systems—such as heat exchangers, process cooling systems, and industrial dryers. Adhesives deployed here must meet unique specifications for chemical resistance, high-pressure tolerance, and mechanical vibration damping. Epoxy, silicone, and polyurethane chemistries dominate this space, ensuring structural stability, corrosion resistance, and compatibility with diverse metals and composites. Unlike the high-volume residential sector, industrial OEM applications often demand custom-engineered solutions that comply with industry-specific performance standards and certifications (e.g., ISO 10993, UL 94, and ASTM D1002). The segment’s growth is supported by increasing industrial automation and the adoption of smart factory systems, where adhesives play a key role in motor sealing, electrical insulation, and structural bonding.

The Global Appliance Adhesive Market is characterized by high R&D intensity and vertically integrated innovation strategies from major players such as Henkel, 3M, H.B. Fuller, Sika AG, and Dow Inc. (Dowsil). Each company is advancing adhesive chemistry, sustainability standards, and automation technologies to deliver tailored bonding solutions for white goods, HVAC systems, and smart appliance assemblies.

Henkel dominates the appliance adhesive market through its Loctite and Bonderite brands, offering complete bonding and surface treatment solutions. Its Bonderite pretreatment coatings are applied to over 60% of appliance metal sheets processed in Europe and China. The company invests 30% of its Adhesive Technologies R&D budget into sustainable and bio-based formulations, with a strong emphasis on recyclable-at-end-of-life adhesives for durable goods. Henkel’s LOCTITE structural adhesives can replace up to eight spot welds per panel, enhancing assembly speed and product strength. The company’s robotic dispensing automation systems have demonstrated a 15% increase in application precision, optimizing both throughput and material efficiency in appliance production.

3M continues to lead the adhesive bonding segment with its VHB Tapes and polyurethane-based formulations, extensively used in induction cooktops and built-in ovens, accounting for over 45% of the premium market share in North America. Its adhesives deliver superior thermal expansion compensation and long-term durability, verified by 1,000-hour exposure at 85°C/85% humidity testing. The company’s hybrid adhesive sealants address common manufacturing challenges such as foaming during curing, ensuring cosmetic precision for refrigerator door seals. In addition, 3M’s acoustic dampening foams complement its acrylic adhesives to achieve significant NVH reduction, enabling quieter, vibration-resistant appliances.

H.B. Fuller has cemented its role as a pioneer in high-performance hot melt adhesives for fast-cycle industrial applications. Its latest reactive hot melt (RHM) technologies enable bonding speeds exceeding 100 cycles per minute, dramatically improving line productivity for appliance and packaging OEMs. The company’s Silane Modified Polymer (SMP) sealants offer 500% elongation at break, crucial for water tank and drain assembly flexibility. Liquid Optical Clear Adhesives (LOCA), another growth segment, support the integration of touchscreen interfaces in smart home appliances. With 45 technology centers worldwide, H.B. Fuller provides custom formulation and technical support, ensuring local optimization for global manufacturers.

Sika AG specializes in polyurethane and silicone sealants designed for structural glazing and component sealing in commercial and domestic appliances. Its products are certified to withstand wind loads up to 2 kPa and meet the UL94 V-0 fire-retardancy standard, making them ideal for smart home electronic casings. The company’s automated robotic dispensing systems have demonstrated 10% material savings across major assembly operations. In July 2025, Sika expanded its R&D capacity in Switzerland to focus on energy-efficient bonding technologies for next-generation appliances.

Dow, through its DOWSIL brand, is a global leader in silicone-based adhesives and sealants for high-heat and moisture-sensitive applications. Its advanced grades retain elasticity above 280°C, making them indispensable in oven door and cooktop assembly. The company’s silicone encapsulants and RTV gap fillers provide IP-rated moisture protection for appliance electronic control units (ECUs). Dow recently launched fast-tack silicone RTVs with <10-minute skin-over times, streamlining dishwasher and washer sealing processes. Furthermore, its thermally conductive silicone range addresses heat dissipation challenges in EV chargers and battery storage systems, technologies increasingly overlapping with home energy appliances.

China remains the world’s largest producer and consumer of appliances, positioning itself as a dominant force in the global appliance adhesive market. Strategic capacity expansion and government-backed industrialization continue to strengthen its manufacturing ecosystem for high-performance adhesive technologies.

In January 2025, Sika AG opened a state-of-the-art manufacturing facility in Xi’an, Northwest China, producing a full range of products including tile adhesives, waterproofing systems, and appliance bonding materials. The expansion enhances supply chain responsiveness to China’s growing appliance, construction, and electronic assembly markets, underscoring Sika’s long-term commitment to the region’s industrial ecosystem.

China’s emphasis on high-performance polyurethane and silicone adhesives aligns with its push for durable, energy-efficient appliances that comply with green manufacturing standards. Domestic producers are scaling R&D in heat- and vibration-resistant adhesive systems designed for modern home appliances like refrigerators, air conditioners, and washing machines. The advancements ensure consistent bonding performance under high thermal stress and humidity — critical for both domestic appliances and global exports.

Germany continues to lead Europe’s appliance adhesive research and innovation landscape, emphasizing precision bonding technologies and automated production efficiency. Its manufacturers are investing heavily in light-curing adhesives, epoxies, and medical-grade formulations optimized for smart home and industrial appliance applications.

In February 2025, DELO Industrial Adhesives introduced the DELOLUX 30, an advanced small-area lamp designed for high-speed light curing — a breakthrough that significantly enhances fast-cycle adhesive applications in appliance assembly lines. The system enables rapid, consistent bonding of plastic, metal, and glass components, supporting automation-driven manufacturing in Germany’s globally recognized appliance sector.

German companies are pioneering in low-VOC adhesive formulations and energy-efficient curing systems, addressing EU sustainability mandates under REACH regulations. The growing use of robotic adhesive dispensing systems across Germany’s appliance and electronics industries highlights the transition toward Industry 4.0-ready manufacturing environments, where adhesives play a crucial role in ensuring material integrity and performance reliability.

The United States appliance adhesive industry is defined by consolidation, innovation, and sustainability investments. Manufacturers are diversifying product portfolios to meet the growing demand for high-performance adhesives in consumer appliances, electronics, and smart device assembly.

In May 2024, H.B. Fuller Company announced its acquisition of ND Industries, a U.S.-based leader in specialty adhesives and fastener locking technologies. The acquisition broadens H.B. Fuller’s adhesive portfolio, integrating epoxy, cyanoacrylate, and UV-curable systems — all critical to modern appliance assembly, electronics sealing, and metal bonding applications.

The U.S. market is also witnessing a surge in eco-friendly and solvent-free adhesive innovations, driven by the tightening of EPA VOC regulations. R&D investments are focused on developing high-strength, temperature-resistant adhesives to meet the technical requirements of energy-efficient and connected appliances. Concurrently, manufacturers are adopting AI-powered quality inspection and robotic adhesive application systems to enhance precision, reduce waste, and streamline assembly in large-scale production facilities.

India’s appliance adhesive industry is expanding rapidly, propelled by urbanization, infrastructure development, and the government’s ‘Make in India’ initiative. The surge in consumer durables and white goods production is creating strong demand for locally manufactured industrial adhesives and sealants that meet both cost and performance benchmarks.

Pidilite Industries Ltd., a dominant player in India’s adhesives sector, continues to leverage its dual expertise in consumer and industrial adhesives, with growing market penetration into construction, appliance assembly, and furniture manufacturing. Pidilite’s continued investment in industrial-grade adhesive technologies supports the rising domestic demand from appliance OEMs (Original Equipment Manufacturers) and contract assemblers.

India’s strategic shift toward domestic production of compressors, control panels, and structural components has accelerated the adoption of polyurethane and hot-melt adhesives for efficient assembly. Moreover, government incentives for electronics and appliance localization are encouraging multinationals to establish local adhesive manufacturing facilities, fostering long-term market self-reliance.

Singapore plays a pivotal role as Southeast Asia’s adhesive distribution and logistics hub, serving as a gateway for high-quality appliance adhesive products across the ASEAN region. The city-state’s strategic location, regulatory stability, and advanced infrastructure make it ideal for multinational chemical companies seeking regional reach.

In January 2025, Sika AG inaugurated a state-of-the-art facility in Singapore specializing in mortar and adhesive production, significantly strengthening its chemical supply chain presence in Southeast Asia. The facility supports rapid delivery of industrial adhesive materials to regional markets such as Malaysia, Indonesia, and Thailand, effectively reducing lead times and transportation costs.

Singapore’s continued investments in chemical manufacturing and distribution efficiency underscore its role in enabling smart manufacturing and appliance production across the ASEAN bloc. With growing demand for lightweight and thermally stable adhesives used in refrigeration and electronics appliances, Singapore remains a strategic pivot for industrial adhesive trade in Asia.

Malaysia has emerged as a strategic ASEAN production base for adhesive materials catering to the durable goods and consumer electronics sectors. The country’s favorable industrial policies and infrastructure have attracted major foreign investments in multi-capability adhesive manufacturing plants.

In August 2025, UPM Adhesive Materials announced a major investment in its Johor Bahru facility, introducing a new coating line and advanced manufacturing capabilities to enhance adhesive production for durables and electronic appliances. The expansion supports regional OEM supply chains, ensuring that appliance producers in Southeast Asia have reliable access to high-performance bonding solutions.

Malaysia’s emphasis on export-oriented manufacturing and technology-driven production is accelerating the adoption of environmentally compliant adhesives. With growing regional demand for energy-efficient home and kitchen appliances, Malaysia’s upgraded adhesive infrastructure strengthens its position as a critical contributor to ASEAN’s advanced materials ecosystem.

Appliance Adhesive Market Report Scope

Appliance Adhesive Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$7.3 Billion

|

|

Market Size (2034)

|

$15.6 Billion

|

|

Market Growth Rate

|

8.8%

|

|

Segments

|

By Resin Type (Epoxy Adhesives, Polyurethane Adhesives, Acrylic Adhesives, Silicone Adhesives, Cyanoacrylate Adhesives, Hot-Melt Adhesives, Styrenic Block Copolymers), By Technology/Formulation (Water-Based Adhesives, Solvent-Based Adhesives, Hot-Melt Adhesives, Reactive Adhesives, UV/Light-Curable Adhesives, Pressure Sensitive Adhesives), By End-Use Appliance Application (Refrigerators and Freezers, Washing Machines and Dryers, Air Conditioners, Cooking Appliances, Dishwashers, Small Household Appliances), By End-User (Residential Appliances, Commercial Appliances, Industrial Assembly

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, H.B. Fuller Company, Sika AG, Arkema Group, 3M Company, Dow Inc., Ashland Global Holdings Inc., Wacker Chemie AG, DELO Industrial Adhesives, Huntsman Corporation, Lohmann GmbH & Co. KG, Pidilite Industries Ltd., Mapei S.p.A., Avery Dennison Corporation, Adhex Technologies

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Resin Type

- Epoxy Adhesives

- Polyurethane Adhesives

- Acrylic Adhesives

- Silicone Adhesives

- Cyanoacrylate Adhesives

- Hot-Melt Adhesives

- Styrenic Block Copolymers

By Technology/Formulation

- Water-Based Adhesives

- Solvent-Based Adhesives

- Hot-Melt Adhesives

- Reactive Adhesives

- UV/Light-Curable Adhesives

- Pressure Sensitive Adhesives

By End-Use Appliance Application

- Refrigerators and Freezers

- Washing Machines and Dryers

- Air Conditioners

- Cooking Appliances

- Dishwashers

- Small Household Appliances

By End-User Segment

- Residential Appliances

- Commercial Appliances

- Industrial Assembly

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- Henkel AG & Co. KGaA

- H.B. Fuller Company

- Sika AG

- Arkema Group

- 3M Company

- Dow Inc.

- Ashland Global Holdings Inc.

- Wacker Chemie AG

- DELO Industrial Adhesives

- Huntsman Corporation

- Lohmann GmbH & Co. KG

- Pidilite Industries Ltd.

- Mapei S.p.A.

- Avery Dennison Corporation

- Adhex Technologies

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the fast-evolving Appliance Adhesive Market, translating regulatory shifts, line-speed demands, and material choices into quantified impacts on takt time, scrap, and warranty risk. Our analysis reviews cure-on-demand UV systems, moisture-reactive PUR/RHM platforms, and heat-stable silicones alongside automation-ready dispensing and in-line QC. It highlights performance envelopes (temperature, chemical, NVH), LSE plastic bonding without primers, and design-for-disassembly considerations for circularity. We benchmark chemistries on throughput, VOC compliance, and lifetime durability, map end-user buying criteria, and size profit pools across residential, commercial, and industrial assemblies. Incorporating technology breakthroughs—from <15-second UV fixture to +315 °C silicone seals—this report is an essential resource for product engineering, sourcing, operations, and ESG teams seeking cost, speed, and reliability advantages.

Scope Includes

- By Resin Type: Epoxy; Polyurethane; Acrylic; Silicone; Cyanoacrylate; Hot-Melt; Styrenic Block Copolymers

- By Technology/Formulation: Water-Based; Solvent-Based; Hot-Melt; Reactive; UV/Light-Curable; Pressure Sensitive

- By End-Use Appliance Application: Refrigerators & Freezers; Washing Machines & Dryers; Air Conditioners; Cooking Appliances; Dishwashers; Small Household Appliances

- By End-User Segment: Residential Appliances; Commercial Appliances; Industrial Assembly

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Time Horizon: Historic 2021–2024; Forecast 2025–2034.

- Companies: 15+ company analysis/profiles.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.