Market Overview: Industry Statistics

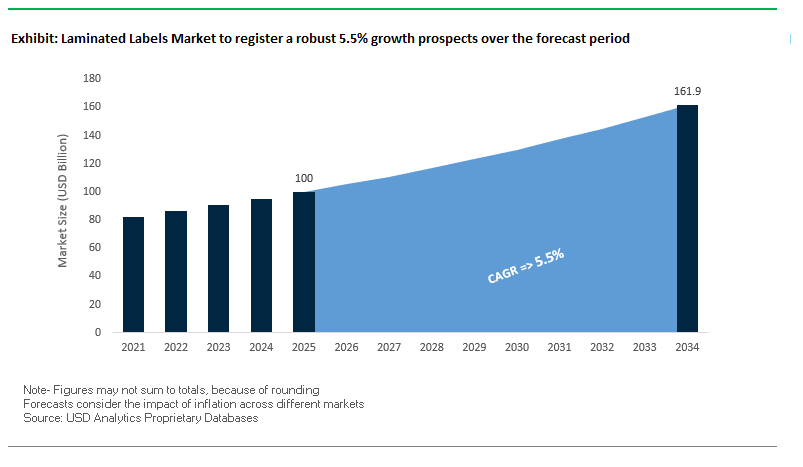

The Global Laminated Labels Market is projected to grow from USD 100.0 billion in 2025 to USD 161.9 billion by 2034, registering a CAGR of 5.5%. Laminated labels are gaining prominence across food and beverages, pharmaceuticals, healthcare, personal care, and e-commerce packaging due to their durability, resistance to moisture, UV, and chemicals, and ability to enhance product branding. As global supply chains expand and regulatory compliance becomes more stringent, laminated labels are viewed as indispensable for ensuring product integrity, traceability, and consumer engagement.

Key Insights for Industry Professionals

- Durability Imperative: Laminated labels are preferred for long shelf-life products requiring resistance to harsh storage and transit conditions.

- E-Commerce Growth Driver: Major e-commerce retailers rely on laminated labels for logistics durability and tamper-evidence, ensuring product safety during shipping.

- Material Trends: Polyester is driving premium print quality and tensile strength, while polypropylene dominates as a cost-effective and durable option.

- Sustainability Push: Manufacturers are investing in PCR-based laminated films and recyclable constructions, aligning with global ESG and regulatory requirements.

- Smart Packaging Integration: Increasing use of RFID and QR-enabled laminated labels supports traceability and digital supply chain management.

Market Analysis: Recent Developments in Laminated Labels

The laminated labels industry has entered a transformative growth phase, driven by digitalization, sustainability, and consolidation. In September 2025, Domino Printing Sciences launched the N410 digital LED inkjet label press at Labelexpo Europe, making high-speed, digital label printing more accessible and enabling converters to deliver on-demand, customized laminated labels.

M&A activity remains a cornerstone of the industry. In August 2025, Avery Dennison acquired the U.S.-based flooring adhesives business of Meridian Adhesives Group, expanding its materials portfolio. The same month, Siegwerk strengthened its coatings business with the acquisition of Dutch coating specialist Allinova, a strategic move supporting innovations in protective and laminated label coatings. Additionally, Comexi showcased new digital and flexographic presses in July 2025, reinforcing the role of advanced printing technology in scaling sustainable laminated labels.

Structural rebranding and strategic positioning are shaping competition. In June 2025, UPM Raflatac rebranded as UPM Adhesive Materials, signaling diversification into specialty tapes and graphics beyond label substrates. Earlier, in January 2025, the company announced that all North American direct thermal laminates are now BPA- and BPS-free, highlighting its compliance with global health and safety standards. On the consolidation front, the Smurfit Kappa–WestRock merger in October 2024 created a new heavyweight in paper-based packaging, which also influences laminated label raw material supply chains.

Transformative Trends and Emerging Opportunities in the Laminated Labels Market

Accelerated Adoption of Polyolefin-Based Films to Enhance Recyclability

The laminated labels market is witnessing a strategic shift toward polyolefin-based films, driven by stringent EPR regulations and growing consumer demand for sustainable packaging. Traditional PET and PVC films are being replaced by polypropylene (PP) and polyethylene (PE) films, which align with the dominant polyolefin recycling streams, ensuring circularity and minimizing contamination of recycled plastics. Avery Dennison’s CleanFlake™ adhesive technology exemplifies this innovation, allowing labels to cleanly separate from PET bottles during recycling, earning recognition from the Association of Plastic Recyclers (APR). Similarly, SmartCycle® PO polyolefin shrink sleeves are engineered to maintain compatibility with HDPE and PP containers, supporting mono-material packaging solutions in sectors like personal care and household cleaning. Industry collaborations, such as UPM Raflatac’s participation in RecyClass, are standardizing recyclable label protocols across Europe, while circular economy initiatives like RafCycle™ enable partners to return label liners for recycling. This trend underscores the market’s focus on sustainability, regulatory compliance, and circular material flows.

Integration of Functional and Smart Layers for Brand Protection & Engagement

Laminated labels are evolving beyond protective layers to become sophisticated platforms for brand engagement and anti-counterfeiting. The integration of tamper-evident features, RFID inlays, and NFC antennas enables security, direct digital marketing, and consumer interaction. Strategic acquisitions, such as Avery Dennison’s purchase of Smartrac’s RFID transponder business, bolster capabilities in smart labeling and digital identification. Companies like Veritech provide multi-layered security labels with overt features (microtext, guilloche patterns) and covert features (UV markings, encrypted patterns) to combat counterfeiting. NFC and QR codes integrated into laminated labels allow brands to communicate product authenticity, promotional content, and loyalty programs directly to consumers. High-value segments, including luxury goods and e-commerce products, increasingly use laminated labels with embedded “void effect” security, protecting against tampering and enhancing trust throughout the supply chain.

Development of High-Barrier, Compostable Laminates for Flexible Packaging

The rise of flexible plastic packaging in food and beverage sectors has created demand for labels that combine high-quality graphics, protective functions, and compostable properties. Compostable polymers such as PLA (polylactic acid) are being explored to create high-barrier laminates that resist moisture and oils while remaining compatible with industrial composting. Certification by bodies like SGS ensures compliance with standards such as BS EN 13432, enabling brands to credibly communicate sustainability claims and avoid greenwashing. Material innovations focus on bio-based coatings that provide functional barrier properties while fully degrading in compost streams. These developments are particularly relevant for companies with ambitious sustainability goals, such as Nestle’s target to make 95% of packaging recyclable or reusable by 2025. Compostable laminated labels thus represent a high-value opportunity to align product protection with environmental commitments.

Advanced Anti-Counterfeit Laminates for E-commerce and Luxury Goods

The growth of e-commerce has amplified the risk of counterfeit products, creating a strong market opportunity for laminated labels with multi-layered security features. Advanced labels integrate overt (holograms), semi-overt (magnifiable elements), and covert features (laser codes, encrypted patterns) that are extremely difficult to replicate. RFID and NFC integration enables real-time product tracking and supply chain visibility, providing brands with the ability to monitor distribution and identify diversion or counterfeit risks. E-commerce, with its lack of physical verification, has become a key driver for investment in robust anti-counterfeit solutions that can be verified by consumers and logistics partners via smartphones. Forensic-level security, including microscopic taggants or embedded DNA markers, delivers unparalleled brand protection, particularly for high-value or regulated goods, ensuring authenticity and trust across global supply chains.

Competitive Landscape: Top Companies in Laminated Labels Industry

The laminated labels industry is characterized by global material science leaders, adhesive innovators, and specialty converters, each driving sustainability, digital integration, and durability.

Avery Dennison Corporation: Expanding specialty adhesive portfolio

Avery Dennison combines expertise in pressure-sensitive adhesives (PSAs) with a strong materials science foundation. In August 2025, it acquired Meridian’s flooring adhesives business for USD 390 million, expanding into specialty adhesives. Its focus is on linerless and recyclable laminated labels, and it remains a leader in RFID-enabled smart labelling, ensuring compliance, traceability, and sustainability.

CCL Industries Inc.: Strong digital and RFID innovation pipeline

CCL Industries is a global leader in specialty packaging and laminated labelling. Its Q2 2025 financials highlighted strong growth from its CCL, Checkpoint, and Innovia divisions, reinforcing profitability. CCL’s competitive edge lies in intelligent laminated labels with RFID and anti-theft technologies, which support supply chain security and product authentication.

UPM Adhesive Materials: Diversifying beyond labels

Rebranded in June 2025, UPM Adhesive Materials has expanded beyond conventional label substrates into graphics solutions and tapes. It is a pioneer in sustainable laminated materials, offering innovations such as Ocean Action labels made from ocean-bound plastics and Forest Film the first wood-based plastic label material. UPM’s strategy is aligned with a fossil-free future and closed-loop material flows.

3M Company: R&D powerhouse in durable laminated solutions

3M maintains a broad portfolio of industrial adhesives and laminated label materials. Its Versatile Print Label Material supports compatibility with diverse inks and printing methods. With a focus on sustainable, recycled-content formulations, 3M leverages its global R&D network to continuously introduce high-performance laminated label solutions that withstand extreme temperatures, UV, and chemicals.

Lintec Corporation: Developing eco-friendly labelstocks

Lintec specializes in pressure-sensitive label materials and specialty papers. The company is actively developing eco-friendly labelstocks compatible with digital printers to enhance recyclability and facilitate circularity in packaging. Its strategy emphasizes sustainability, continuous improvement, and technical support services, ensuring global competitiveness in laminated labels.

Flexcon Company Inc.: Partnering with digital press OEMs

Flexcon is a global leader in pressure-sensitive films and laminated label constructions. It partners with digital press manufacturers to develop certified substrates and advanced adhesives, ensuring compatibility with next-gen digital presses. Flexcon’s laminated labels are designed for harsh environments, including industrial chemicals, outdoor exposure, and high UV conditions, making it a preferred supplier for durable goods manufacturers.

Laminated Labels Market Share Insights

Permanent Adhesives Dominate Market Share by Adhesive Type in the Laminated Labels Industry

Permanent adhesives account for the largest share of the laminated labels market, holding nearly 60% of demand in 2025, as they remain the default solution for most product packaging applications. Their dominance stems from the non-negotiable need for labels to remain intact throughout a product’s lifecycle whether in food, beverages, pharmaceuticals, or consumer goods ensuring brand integrity, regulatory compliance, and supply chain traceability. These adhesives are engineered to resist moisture, friction, refrigeration, and handling, making them indispensable across industries where reliability is paramount. While removable adhesives support promotional and short-term labeling, and freezer or high-temperature adhesives address niche requirements, it is the universal application and durability of permanent adhesives that firmly establish them as the market leader.

Food and Beverages Secure the Largest Share by Application in the Laminated Labels Industry

The food and beverages sector holds the largest application share at 30%, reflecting the enormous global volume of packaged food and drink products. Laminated labels in this segment must meet rigorous standards, combining durability with compliance to FDA and EU food contact regulations while withstanding moisture, refrigeration, freezing, and condensation. Beyond functionality, laminated labels are a critical tool for consumer engagement, displaying nutritional information, barcodes, and branding that directly influence purchasing decisions. Pharmaceuticals and healthcare form another high-value application, where laminated labels are mandated to endure sterilization, chemical exposure, and long-term storage while preserving serialization and traceability data. Industrial, automotive, and cosmetics sectors contribute with specialized needs, but the scale, compliance pressure, and branding value in F&B firmly secure its market leadership.

United States Laminated Labels Market Driven by FDA Regulations and Smart Packaging Innovations

The U.S. laminated labels market is strongly influenced by a fragmented regulatory environment, with FDA and DOT regulations ensuring safety and compliance for pharmaceuticals, food, and beverages. The Drug Supply Chain Security Act (DSCSA) mandates unique identifiers on pharmaceutical packaging, accelerating adoption of track-and-trace technologies and high-performance laminated labels.

Technological advancements are reshaping the market, with companies like The Packaging Company introducing eco-friendly, reusable insulated packaging solutions and smart packaging with IoT sensors for real-time temperature monitoring. UPM Raflatac has achieved ISO 22000:2018 FSMS certification for all U.S. factories, highlighting a commitment to food safety and innovation. Corporate investments, such as Avery Dennison’s acquisition of a Midwest facility in 2025, are expanding sustainable production capacity. Key applications are concentrated in the e-commerce and healthcare sectors, with strong demand for durable laminated labels for mRNA vaccines and fresh food delivery, driven by consumer expectations from the “Amazon Effect.” Sustainability remains a core focus, with the adoption of adhesives with low VOC emissions aligning with growing regulatory and consumer pressures.

Germany Laminated Labels Market Advances Through Regulatory Compliance and Circular Economy Leadership

Germany’s laminated label market operates under a stringent regulatory framework, including the EU Packaging and Packaging Waste Regulation (PPWR), effective February 2025, which mandates fully recyclable or reusable packaging by 2030. This regulation drives the adoption of wash-off and removable adhesives, enhancing recycling efficiency.

Technological innovation, powered by Industry 4.0 initiatives, is a hallmark of the market. Herma introduced 52W wash-off label adhesives for PET bottles, and companies are increasingly integrating digital technologies to enhance production efficiency. Germany’s Packaging Act (VerpackG) incentivizes eco-design and recycling, positioning the country as a leader in circular economy solutions. Key players like Henkel are investing strategically in high-performance and sustainable laminated labels to meet evolving regulatory and market demands.

China Laminated Labels Market Fueled by Governmental Initiatives and AI-Driven Technologies

China’s laminated labels market is being shaped by governmental policies targeting sustainability and digital innovation. The “dual carbon” goal and the Action Plan for Large-Scale Equipment Updates encourage recycling and adoption of eco-friendly materials. In September 2025, the rollout of a mandatory AI labeling law has opened new applications for digital laminated labels, especially in e-commerce and high-value goods.

Regulatory reforms, such as GB/T 31268 on excessive packaging, influence packaging design, particularly for consumer goods. Technological advancements in automation, RFID integration, and AI-driven logistics are improving production efficiency and supply chain transparency. Domestic manufacturing initiatives are expanding local capacity for high-quality, circular packaging, with booming e-commerce, electronics, and automotive sectors driving specialized laminated label demand.

India Laminated Labels Market Expands Through Circular Economy Initiatives and Growing Pharmaceutical Demand

India’s laminated labels market is experiencing robust growth, supported by government initiatives promoting a circular economy and domestic manufacturing. The Make in India initiative, alongside the Production Linked Incentive (PLI) for Pharmaceuticals and Medical Devices, has generated cumulative sales exceeding INR 2.66 lakh crore, fueling demand for durable, compliant laminated labels.

Technological advancements, including Pidilite Industries’ water-based adhesives, are enabling eco-friendly laminated label production. Rising corporate investments are expanding local manufacturing capacity to serve food and beverage, pharmaceutical, and e-commerce sectors. The export-oriented pharmaceutical sector further drives demand for high-performance laminated labels that meet international safety and regulatory standards, highlighting India’s growing role in the global laminated labels market.

Japan Laminated Labels Market Strengthened by High-Performance Adhesives and Regulatory Compliance

Japan’s laminated labels market is characterized by precision manufacturing and a focus on high-performance, value-added products. Companies such as LINTEC and Oji Holdings are leading in advanced label materials and adhesive technologies. LINTEC’s investment of approximately 4.8 billion yen in 2025 for new coating equipment highlights ongoing capacity expansion to meet demand for high-end laminated labels.

The Plastic Resource Circulation Act (2022) and revised food contact material regulations (effective June 2026) promote eco-friendly designs and reduce single-use plastics, driving innovation in laminated label functionality. The market is emphasizing self-sealing labels, superior barrier properties, and durability, serving diverse sectors including pharmaceuticals, food, and industrial products.

Brazil Laminated Labels Market Grows Through Sustainability Initiatives and Strategic Corporate Investments

Brazil’s laminated labels market is shaped by sustainable waste management policies and expanding corporate investment. The National Solid Waste Policy and 2024 Senate ban on imported solid waste promote local recycling and circular packaging solutions, creating opportunities for laminated labels produced from recycled content.

Technological advancements are evident as companies like Beontag launch self-adhesive wine labels with premium lamination. The market is particularly strong in the food, beverage, and agricultural sectors, and the EU-Mercosur trade agreement is expected to drive further diversification and investment. The combined focus on sustainability, premium aesthetics, and regulatory compliance positions Brazil as a growing hub for laminated label innovations in Latin America.

Laminated Labels Market Report Scope

Laminated Labels Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$100 Billion

|

|

Market Size (2034)

|

$161.9 Billion

|

|

Market Growth Rate

|

5.5%

|

|

Segments

|

By Facestock Material (Paper, Plastic Films, Others), By Adhesive Type (Permanent, Removable, Freezer, High-temperature, Others), By Application (Food & Beverages, Pharmaceuticals & Healthcare, Cosmetics & Personal Care, Consumer Goods, Automotive, Industrial, Others), By Printing Technology (Digital Printing, Flexography, Lithography, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Avery Dennison Corporation, CCL Industries Inc., 3M Company, UPM Raflatac, LINTEC Corporation, Fuji Seal International, Inc., Mondi Group, Konica Minolta, Inc., Nippon Paper Industries Co., Ltd., SATO Holdings Corporation, Toray Industries, Inc., H.B. Fuller Company, Beontag, Henkel AG & Co. KGaA, Cenveo Worldwide Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Laminated Labels Market Segmentation

By Facestock Material

- Paper

- Plastic Films

- Others

By Adhesive Type

- Permanent

- Removable

- Freezer

- High-temperature

- Others

By Application

- Food & Beverages

- Pharmaceuticals & Healthcare

- Cosmetics & Personal Care

- Consumer Goods

- Automotive

- Industrial

- Others

By Printing Technology

- Digital Printing

- Flexography

- Lithography

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Laminated Labels Market

- Avery Dennison Corporation

- CCL Industries Inc.

- 3M Company

- UPM Raflatac

- LINTEC Corporation

- Fuji Seal International, Inc.

- Mondi Group

- Konica Minolta, Inc.

- Nippon Paper Industries Co., Ltd.

- SATO Holdings Corporation

- Toray Industries, Inc.

- H.B. Fuller Company

- Beontag

- Henkel AG & Co. KGaA

- Cenveo Worldwide Limited

* List Not Exhaustive

Methodology

USDAnalytics applies a rigorous, multi-source research methodology to the Laminated Labels Market that blends targeted primary research (in-depth interviews with label converters, C-suite packaging buyers, sustainability leads, brand protection specialists and OEM printer partners) with exhaustive secondary analysis of company filings, patent activity, trade and import/export flows, regulatory texts (EPR/PPWR), and technical whitepapers; market sizing and the 2025–2034 CAGR are produced via a hybrid bottom-up/top-down approach (converter capacity, laminated film consumption by end-use, digital press deployments, and SKU proliferation in F&B and pharma) and validated with vendor shipment statistics and field-level pilot data; technology validation uses laboratory performance benchmarks (UV/chemical resistance, peel/tack, CleanFlake®-style wash-off trials, and polyolefin vs. polyester recyclability tests), while competitive positioning combines M&A tracking, supply-chain concentration analysis, and price-elasticity models scenario stress tests quantify impacts from accelerated EPR rollouts, mono-material mandates, and digital decentralization (on-demand laminated label production) to deliver actionable guidance for procurement, R&D, sustainability and brand-protection teams.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.