Market Overview: Growing Demand for Sustainable and High-Performance Adhesives

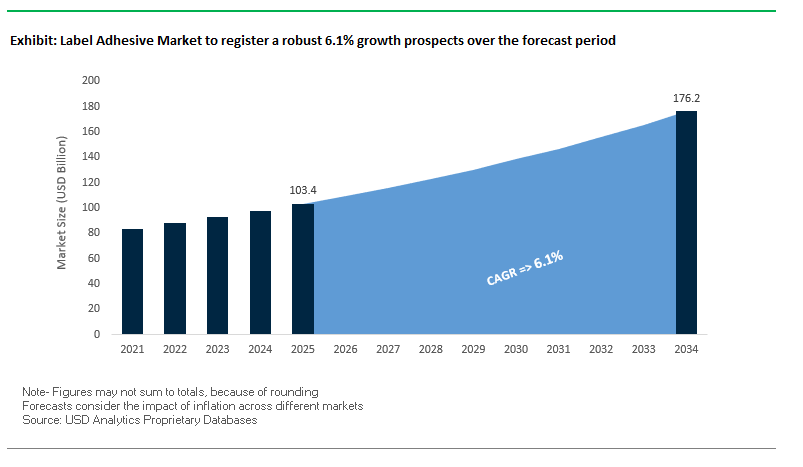

The Label Adhesive Market is projected to grow from USD 103.4 billion in 2025 to USD 176.2 billion by 2034, expanding at a CAGR of 6.1%. The market plays a pivotal role in enabling product branding, logistics, compliance, and smart packaging integration across industries such as food & beverages, pharmaceuticals, personal care, and e-commerce. As labeling regulations tighten and sustainability demands accelerate, the adhesive segment is undergoing significant transformation to meet performance and recyclability requirements.

Key Insights for Industry Professionals

- Sustainability Imperative: Brands demand wash-off and repulpable adhesives to enable recycling, aligning with EU PPWR and circular economy goals.

- Digital Printing Push: Growth of on-demand digital printing requires adhesives compatible with high-speed production, ensuring flexibility and reduced waste.

- E-commerce Boom: Expansion of global e-commerce fuels demand for durable, tamper-evident shipping labels that withstand harsh transit conditions.

- Smart Label Growth: Integration of RFID and QR codes into packaging is creating demand for adhesives that securely bond electronic components without impairing performance.

- Material Diversification: Rising use of bio-based adhesives and low-VOC chemistries highlights the industry’s commitment to eco-friendly solutions.

Market Analysis: Recent Industry Developments Driving Innovation

The global label adhesive market is witnessing a wave of acquisitions, product launches, and sustainability-driven strategies. In August 2025, Avery Dennison expanded its portfolio by acquiring the U.S.-based flooring adhesives business of Meridian Adhesives Group, strengthening its position in specialty adhesives beyond labels. The same month, Siegwerk acquired Dutch coating specialist Allinova, furthering its presence in packaging coatings, while Covestro agreed to acquire two HDI derivative production sites from Vencorex, critical for adhesive formulations.

M&A activity continued in July 2025, when Henkel acquired Nordbak of South Africa, a strong player in MRO solutions, widening its reach into mining and infrastructure markets. Earlier in May 2025, SCHÜTZ entered a partnership with a Saudi Arabian company to produce ECOBULK IBCs for the food industry, indirectly influencing adhesive consumption through value chain integration. Reports from March 2025 emphasized sustainable packaging and automation, with label adhesives highlighted as central to this transition.

Consumer-facing innovation is also gaining traction. In June 2024, Beontag launched self-adhesive labels for the Latin America wine market, incorporating 40% grass fiber with FSC-certified cellulose, highlighting material innovation. The market also saw major consolidation in October 2024, when Smurfit Kappa and WestRock merged, reshaping the paper packaging ecosystem that directly influences label adhesives.

Emerging Trends and Opportunities Shaping the Label Adhesive Market

Accelerated Demand for Recyclable PSA Constructions Driven by EPR Legislation

The label adhesive market is experiencing a surge in demand for recyclable pressure-sensitive adhesive (PSA) constructions due to the rapid implementation of Extended Producer Responsibility (EPR) laws across packaging sectors. Brands are increasingly prioritizing packaging recyclability, creating a direct need for PSA technologies compatible with polyolefin and PET recycling streams. Avery Dennison’s CleanFlake™ technology, for instance, “switches off” during the caustic wash in PET recycling, enabling clean label separation and earning accreditation from the Association of Plastic Recyclers (APR). Dow’s RecycleReady Technology™ portfolio provides solvent-free, water-borne adhesives and resins compatible with mechanical recycling for multi-layer PE-based packaging, approved by RecyClass. Regulatory mandates like the EU Packaging and Packaging Waste Regulation (PPWR), which requires full recyclability by 2030, are acting as catalysts, forcing adhesive manufacturers to innovate proactively. Financial incentives, such as eco-modulated fees under EPR laws in states like California and Minnesota, further drive the adoption of recyclable adhesives, offering brands cost advantages and reinforcing a circular economy model.

Strategic M&A and Capital Investment in Sustainable & Functional Adhesive Technologies

Leading adhesive manufacturers are pursuing mergers, acquisitions, and capital investments to strengthen their positions in high-growth, sustainable, and functional adhesive segments. H.B. Fuller’s acquisitions of GEM S.r.l., Medifill Ltd., and Adhezion Biomedical between 2023–2024 exemplify a strategy focused on specialized, high-margin solutions, particularly in medical and industrial adhesives. Bostik is investing in production capacity to support water-based and circular adhesives, aligning 80% of its new patents with sustainability and circular economy objectives in 2023. Hybrid adhesive technologies, such as UV-curable hot melts developed by artimelt, are gaining traction due to their high transparency, chemical resistance, and suitability for outdoor applications. These strategic investments enable companies to meet evolving regulatory requirements, offer eco-friendly alternatives, and provide high-performance solutions that cater to the increasing demand for functional and sustainable labeling solutions.

Development of Adhesives for Reusable Packaging and Circular Economy Models

The growth of reusable packaging in e-commerce, grocery, and consumer goods markets creates a niche for durable, clean-release adhesives that can endure multiple wash cycles. Bekuplast highlights reusable containers where labels “adhere optimally and can still be removed very well in the washing process,” demonstrating the feasibility of multi-trip adhesive solutions. UPM Raflatac’s wash-off label technology ensures labels separate cleanly from glass containers, leaving no residue and facilitating repeated reuse. Standardization efforts, referencing cyclos-HTP and APR guidelines, are critical for establishing industry-wide frameworks for reusable adhesive systems. These innovations enable efficient reverse logistics, reduce material waste, and reinforce circular economy principles, presenting a significant opportunity for adhesive manufacturers to provide sustainable, durable labeling solutions.

Advanced Adhesives for Smart and Intelligent Label Integration

The rise of smart labeling technologies, including RFID, NFC, and sensor-enabled labels, drives demand for adhesives that maintain stability while supporting electronic components. Specialized adhesives are required to securely bond RFID chips and NFC tags without chemical or thermal damage. Conductive adhesive inks, like Saralon’s silver-based screen-printable solutions, allow efficient integration of surface-mount devices on flexible substrates, enabling hybrid printed electronics at low temperatures. High-temperature-resistant adhesives, such as smart-TEC’s “smart-LABEL HIGH TEMPERATURE,” ensure reliable performance in industrial or harsh environmental applications. These advanced adhesive solutions are pivotal for smart supply chain monitoring, enhancing traceability, security, and functionality across multiple industries, establishing a high-value growth avenue within the label adhesive market.

Competitive Landscape: Leading Companies in Global Label Adhesive Industry

The label adhesive market is led by multinational corporations with deep expertise in adhesive chemistries, sustainable innovations, and global distribution networks. These companies are shaping the industry through acquisitions, technology advancements, and circular economy initiatives.

Henkel AG & Co. KGaA: Expanding portfolio through global acquisitions

Henkel is a global leader in adhesives with flagship brands such as Loctite and Technomelt. In July 2025, it acquired Nordbak, strengthening its industrial adhesives portfolio in Africa. Its strategy focuses on sustainability and digital transformation, with a strong pipeline of low-carbon and circular economy-oriented adhesives. Henkel’s wide expertise in hot melts and water-based emulsions makes it a dominant force in label adhesives across packaging, industrial, and consumer applications.

H.B. Fuller Company: Driving linerless and residue-free label adhesives

H.B. Fuller has carved a niche in pressure-sensitive adhesives (PSAs) and specialty chemistries for packaging. Its innovation in microsphere adhesive technology allows linerless labels that peel without residue, supporting efficiency and recyclability. The company’s portfolio spans bio-based hot melts, hygiene adhesives, and food packaging adhesives, ensuring reliability across industries. Its strategic focus remains on sustainable innovation and high-performance bonding solutions.

Avery Dennison Corporation: Strengthening global position through acquisitions

Avery Dennison continues to expand its adhesive technologies through strategic moves, including the August 2025 acquisition of Meridian Adhesives’ flooring business. A global leader in pressure-sensitive labels, Avery Dennison emphasizes linerless formats, recycled-content adhesives, and RFID-enabled smart labels. Its global presence and integration capabilities position it as a key enabler of traceable, sustainable, and intelligent labeling systems.

3M Company: Leveraging global R&D for advanced adhesive solutions

3M’s adhesive portfolio includes tapes, films, and label adhesives tailored for extreme conditions. The company is renowned for high-performance PSAs used across logistics, industrial, and consumer markets. 3M’s innovation strategy centers on recyclable, durable adhesives that minimize environmental impact while ensuring performance. With a broad global footprint and R&D network, 3M remains a critical player in next-gen label adhesive solutions.

Arkema Group (Bostik): Innovating with hot melt and sustainable chemistries

Arkema’s subsidiary Bostik specializes in smart adhesives with a strong presence in tapes, labels, and FMCG packaging. In November 2022, it launched HM2060 and HM2070 hot-melt PSAs in India, targeting high-speed FMCG label applications and e-commerce packaging. Bostik’s strategy is to deliver biodegradable and compostable adhesives without compromising performance. Its growing portfolio reflects Arkema’s broader sustainability-driven roadmap for the adhesives sector.

Label Adhesive Market Share Insights

Plastic Substrates Lead Market Share in the Label Adhesive Industry

Plastic substrates command 45% of the label adhesive industry in 2025, reflecting their dominance as the primary material for packaging in food, beverage, personal care, and household chemicals. Adhesives engineered for plastic must overcome low-surface-energy challenges associated with substrates like PET, PP, and PE, which has spurred innovation in acrylic- and hot-melt-based solutions that deliver strong, long-lasting bonds. Paper substrates also play a vital role, particularly in corrugated boxes, cartons, and paper-based retail packaging, where quick tack and fiber tear resistance are critical. Glass and metal substrates, though smaller, carry high-value applications in beverage bottles, jars, and canned goods, where adhesives must endure refrigeration, sterilization, and humidity exposure. Together, this segmentation illustrates how plastic drives adhesive innovation and revenue, while paper, glass, and metal ensure diversification across regulated and specialized packaging markets.

Food & Beverages Continue to Drive Market Share by Application in the Label Adhesive Industry

Food and beverages remain the largest application segment for label adhesives in 2025, accounting for 40% of demand. This leadership is driven by the sheer diversity and volume of products requiring adhesive labels across bottles, cans, jars, and flexible packaging. Adhesives in this sector must meet stringent safety standards (e.g., FDA compliance), resist moisture and condensation, and perform reliably under refrigeration or immersion, ensuring product integrity and regulatory compliance. Pharmaceuticals & healthcare represent a premium, specification-driven segment, where adhesives must withstand sterilization processes, freeze-thaw conditions, and chemical exposure while maintaining permanent labeling for traceability. Consumer goods including cosmetics and cleaning products demand adhesives that balance chemical resistance with brand aesthetics, while industrial and automotive applications require highly durable formulations capable of withstanding abrasion, UV exposure, and extreme temperatures. This segmentation highlights how food and beverages secure volume leadership, while regulated healthcare and automotive sectors push adhesive innovation for performance-critical environments.

United States Label Adhesive Market Strengthened by Regulatory Compliance and E-Commerce Growth

The U.S. label adhesive market is significantly shaped by a fragmented regulatory environment, with key oversight from the FDA and DOT ensuring the safety and integrity of pharmaceutical, food, and beverage packaging. The Drug Supply Chain Security Act (DSCSA), which mandates unique identifiers for pharmaceutical packaging, is accelerating the adoption of track-and-trace technologies relying on high-performance adhesives. Technological advancements are a major growth driver, with companies like UPM Raflatac pioneering pressure-sensitive adhesives compliant with FDA regulations and achieving ISO 22000:2018 Food Safety Management System certification across their U.S. facilities.

Corporate investments are further fueling market expansion, exemplified by Avery Dennison’s 2025 acquisition of a new Midwest facility to enhance sustainable label material production for the e-commerce and logistics sectors. Key applications driving demand include healthcare and e-commerce labeling, particularly for high-value biologics and mRNA vaccines, where adhesives must perform under ultra-low temperatures. The “Amazon Effect” has intensified demand for durable, versatile labels, while sustainability initiatives are fostering the use of adhesives with lower volatile organic compound (VOC) emissions, aligning with both regulatory requirements and consumer expectations.

Germany Emerges as a Leader in Sustainable and Wash-Off Label Adhesives

Germany’s label adhesive market operates under a stringent regulatory environment, with the EU Packaging and Packaging Waste Regulation (PPWR) effective February 2025, mandating fully recyclable or reusable packaging by 2030. This regulation has become a key driver for wash-off and removable adhesives that facilitate recycling and promote sustainable labeling practices.

Technological innovation is central to Germany’s market, with Industry 4.0 initiatives revolutionizing production processes. Herma, a German self-adhesive technology specialist, launched the 52W wash-off label adhesive for PET bottles, exemplifying the country’s focus on high-performance and environmentally friendly solutions. Germany’s Packaging Act (VerpackG) incentivizes recyclable packaging through modulated fees, favoring sustainable label adhesives. Major corporate investments, including Henkel’s expansion in sustainable adhesive solutions, underscore the market’s emphasis on innovation, regulatory compliance, and circular economy leadership.

China’s Label Adhesive Market Expands with Green Policies and Domestic Manufacturing Initiatives

China’s label adhesive industry is advancing under governmental initiatives aimed at sustainability and industrial transformation. The March 2024 “Action Plan for Promoting Large-Scale Equipment Updates and Consumer Goods Replacement” encourages recycling and the adoption of sustainable materials across all industries, including adhesives. Regulatory reforms, such as GB/T 31268 and the 2025 amendment to the Express Delivery Regulations, are reducing excessive packaging and promoting recyclable solutions, particularly in e-commerce, a major label adhesive application channel.

Technological advancements in automation, AI, and RFID-enabled real-time tracking are improving production efficiency and supply chain transparency. Domestic manufacturing is a strategic focus, with local companies expanding capacity to meet growing demand from sectors like e-commerce, electronics, and automotive. The integration of high-performance adhesives for specialized applications supports China’s broader circular economy goals and enhances the adoption of eco-friendly labeling solutions.

India’s Label Adhesive Market Strengthens with Circular Economy Policies and Domestic Manufacturing

India’s label adhesive market benefits from government initiatives such as the “Make in India” program and Production Linked Incentives (PLI) for Pharmaceuticals and Medical Devices, which support domestic manufacturing and technological advancement. Regulatory and sustainability efforts are accelerating the adoption of eco-friendly adhesive solutions in labeling, aligning with the country’s circular economy goals.

Technological adoption is rising, with companies like Pidilite Industries Ltd. introducing new water-based adhesives in September 2025 for packaging and labeling sectors. Corporate investments are increasing, driven by expanding e-commerce, food and beverage, and pharmaceutical industries. Key applications include high-performance labeling for pharmaceutical products, industrial goods, and consumer packaged goods, reinforcing the importance of durable, eco-conscious adhesive solutions that comply with global safety standards.

Japan Leads in High-Performance and Specialty Label Adhesives Through Advanced Manufacturing

Japan’s label adhesive market is a hub of innovation, supported by precision manufacturing and advanced materials expertise. Companies like LINTEC and Oji Holdings are recognized for their leadership in adhesive technology and next-generation label materials. Regulatory support, including the Plastic Resource Circulation Act (April 2022) and revised food contact material regulations effective June 2026, encourages sustainable labeling practices and reduces single-use plastics.

The market is increasingly focused on specialty and value-added products, including adhesives with superior barrier properties, self-sealing functionality, and durability in harsh environments. This emphasis on high-performance, functional adhesives caters to diverse industries, including healthcare, logistics, and consumer goods, positioning Japan as a global leader in technologically advanced and environmentally responsible labeling solutions.

Brazil’s Label Adhesive Market Advances with Sustainable Practices and Technological Investments

Brazil’s label adhesive market is guided by the National Solid Waste Policy, amended in April 2022, which promotes sustainable waste management over the next two decades. Technological innovation is accelerating market growth, with companies like Henkel establishing an Inspiration Center for Adhesive Technologies in São Paulo to enhance collaboration and drive sustainable solutions.

Key applications in Brazil include food and beverage and agricultural packaging, with growing demand for high-performance labels in processed and ready-to-eat products. Market expansion is fueled by both domestic and international investments, while initiatives like the EU-Mercosur trade agreement are expected to diversify and attract further investment. Companies such as Beontag are introducing self-adhesive wine labels to capitalize on emerging opportunities in Latin America’s food and beverage sector.

Label Adhesive Market Report Scope

Label Adhesive Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$103.4 Billion

|

|

Market Size (2034)

|

$176.2 Billion

|

|

Market Growth Rate

|

6.1%

|

|

Segments

|

By Technology (Water-based, Hot-melt-based, Solvent-based, Others), By Substrate (Paper, Plastic, Metal, Glass, Others), By Application (Food & Beverages, Pharmaceuticals & Healthcare, Consumer Goods, Automotive, Industrial, Others), By Adhesive Type (Permanent, Removable, Freezer, High-temperature, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Avery Dennison Corporation, Henkel AG & Co. KGaA, H.B. Fuller Company, 3M Company, Arkema SA (Bostik), The Dow Chemical Company, Sika AG, UPM Raflatac, Pidilite Industries Ltd., LINTEC Corporation, Illinois Tool Works Inc., Lord Corporation, Wacker Chemie AG, Jowat SE, Ashland Global Holdings Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Label Adhesive Market Segmentation

By Technology

- Water-based

- Hot-melt-based

- Solvent-based

- Others

By Substrate

- Paper

- Plastic

- Metal

- Glass

- Others

By Application

- Food & Beverages

- Pharmaceuticals & Healthcare

- Consumer Goods

- Automotive

- Industrial

- Others

By Adhesive Type

- Permanent

- Removable

- Freezer

- High-temperature

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Label Adhesive Market

- Avery Dennison Corporation

- Henkel AG & Co. KGaA

- H.B. Fuller Company

- 3M Company

- Arkema SA (Bostik)

- The Dow Chemical Company

- Sika AG

- UPM Raflatac

- Pidilite Industries Ltd.

- LINTEC Corporation

- Illinois Tool Works Inc.

- Lord Corporation

- Wacker Chemie AG

- Jowat SE

- Ashland Global Holdings Inc.

* List Not Exhaustive

Methodology

USDAnalytics applies a rigorous, multi-method research framework to develop the Label Adhesive Market analysis, combining primary interviews with R&D leaders, product managers, and supply-chain executives across adhesives, label converters, and brand owners, with exhaustive secondary research that includes company filings, patent databases, industry standards (APR, RecyClass), regulatory texts (PPWR, EPR frameworks), and trade data; market sizing and forecasts are derived through a blended bottom-up (plant/technology capacity, substrate demand by end-use) and top-down (historical spend and macro demand drivers) approach, while technology and product roadmaps are validated with laboratory performance benchmarks and supplier capability mapping to capture trends such as wash-off PSA, water-based chemistries, UV-curable hot melts, and smart-label adhesives; competitive positioning uses M&A tracking, patent citation analysis, and pricing elasticity models, and scenario modelling tests regulatory shocks (EPR rollouts, recyclability mandates) and commercial shifts (digital printing, e-commerce growth) to deliver actionable, risk-aware insight for procurement, product development, and sustainability strategy teams.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.