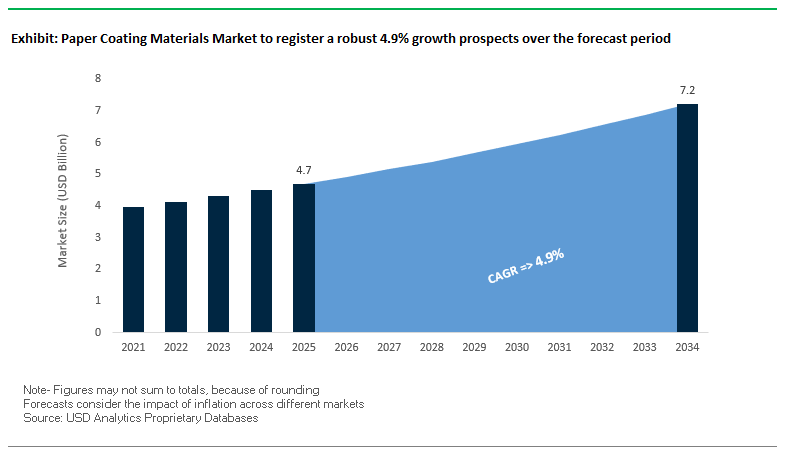

Paper Coating Materials Market to Expand from $4.7 Billion in 2025 to $7.2 Billion by 2034 Fueled by Printability and Sustainability Demands

The Global Paper Coating Materials Market is projected to grow from $4.7 billion in 2025 to $7.2 billion by 2034, at a CAGR of 4.9%, driven by increasing demand for high-performance coatings in printing and packaging applications. These materials enhance print quality, gloss, brightness, and barrier properties, making them essential for food packaging, e-commerce, and premium printed materials.

Key Insights for Industry Professionals:

- High-Quality Printability Remains a Core Demand: Coatings enable smooth, bright surfaces that allow for vibrant graphics and high-resolution text, crucial for brand differentiation.

- Sustainability Drives Formulation Innovation: Transition from petroleum-based coatings to bio-based, water-based, and recyclable alternatives is aligning the industry with corporate and regulatory sustainability goals.

- Barrier Properties Are Increasingly Critical: Enhanced resistance to moisture, grease, and oxygen extends shelf life and protects e-commerce shipments.

- Compatibility with Digital Printing Technologies: Rise of short-run and personalized printing requires coatings suitable for inkjet and toner-based processes.

- Strategic Role in Packaging and Printing Supply Chains: Coatings are central to product quality, brand experience, and operational efficiency, making them a strategic investment for manufacturers and converters.

Recent Strategic Moves Highlighting Innovation and Global Expansion in Paper Coating Materials

The Global Paper Coating Materials Industry has witnessed dynamic strategic developments that underscore technology adoption, sustainability focus, and market consolidation. In August 2025, Mondi plc launched FunctionalBarrier Paper Ultimate, a high-performance paper-based barrier material for food packaging, offering superior protection against oxygen, moisture, and grease. The same month, LINTEC invested approximately 4.8 billion yen in state-of-the-art coating equipment at its Komatsushima Plant to increase production of casting papers for synthetic leather applications.

July 2025 saw BASF Coatings, in collaboration with Renault Group and Dürr, awarded for a sustainable application technology, demonstrating its commitment to eco-friendly coatings, while BASF India Ltd. released its Q2 2025 financial results, providing insights into its regional performance and strategic initiatives. Earlier, in April 2025, Hubergroup Chemicals showcased its modern portfolio of chemicals and resins at the American Coatings Show, reinforcing a commitment to efficient and sustainable coating solutions.

Key consolidation moves include Omya’s acquisition of Distrupol in February 2025, creating a global polymers distribution network supporting coating applications, and the November 2024 completion of WestRock’s acquisition by Smurfit Kappa, establishing Smurfit WestRock as a dominant player in paperboard—a key end-use market for coating materials. In September 2024, Donaldson Company expanded into life sciences with its Isolere Bio IsoTag™ AAV reagent, illustrating diversification into high-value specialty applications.

Trends and Opportunities Defining the Future of the Paper Coating Materials Market

Rapid Phase-Out of PFAS-Based Grease Barriers in Food Packaging

The global paper coating materials market is undergoing a dramatic shift as regulatory and voluntary actions accelerate the elimination of PFAS-based coatings in food packaging. In the United States, several states—including California, New York, and Colorado—have already banned food packaging containing intentionally added PFAS as of January 2024. This legal framework is creating an immediate gap for alternative grease-resistant coatings. Complementing state-level restrictions, the U.S. Food and Drug Administration (FDA) announced in February 2024 that it had secured voluntary agreements from manufacturers to phase out PFAS-based grease-proofing agents, effectively cutting off a major source of dietary PFAS exposure. Similar momentum is building in Europe, where the EU Packaging and Packaging Waste Regulation (PPWR) mandates a complete phase-out of PFAS in food packaging by August 12, 2026, with a threshold limit of 25 parts per billion (ppb). These combined legislative bans and voluntary corporate phase-outs highlight an irreversible transition toward safer, compliant alternatives. The pressure is reshaping global supply chains and compelling coating manufacturers to accelerate R&D into high-performance, non-toxic barrier solutions that can match or exceed PFAS functionality while meeting recyclability and compostability goals.

Strategic Shift to High-Performance Mineral and Bio-Based Coatings

With PFAS nearing extinction in packaging, the market is rapidly innovating to introduce advanced mineral and bio-based coatings that provide equivalent grease, moisture, and oxygen barrier performance. Bio-based alternatives leveraging starch, gelatin, and sodium alginate have demonstrated remarkable results, enhancing mechanical strength and biodegradability, with coated papers showing 100% weight loss after just three weeks of soil incubation. Companies are also introducing hybrid mineral-polymer coatings such as Smart Planet Technologies’ EarthCoating, which integrates up to 51% mineral content. This innovation enables compatibility with traditional paper recycling systems while serving as a drop-in replacement for petroleum-based plastic films. Additionally, leading suppliers such as Omya are advancing calcium carbonate mineral coatings, which enhance brightness, opacity, and recyclability while lowering the carbon footprint of coated substrates. These innovations not only improve product functionality but also align with sustainability mandates, ensuring that the industry transitions toward coatings that support a circular economy without sacrificing packaging performance.

Development of Recyclable Polymer Dispersion Barriers for Liquid Packaging

One of the most lucrative opportunities lies in creating recyclable barrier solutions for liquid packaging, where polyethylene (PE) extrusion has long hindered fiber recovery. Water-based polymer dispersion coatings are emerging as the frontrunner, offering easy separation during the repulping process and significantly improving fiber yield. These dispersions reduce overall plastic content, enable faster processing, and enhance fiber recovery compared to traditional PE layers. The 4evergreen Alliance is playing a critical role in this transition by establishing industry-wide recycling protocols that ensure new solutions are viable at scale. Importantly, these dispersions can be applied using existing coating equipment, eliminating the need for costly machinery upgrades. By enabling converters to replace PE layers with water-based barriers seamlessly, this opportunity offers both scalability and cost efficiency while positioning liquid cartons as a truly recyclable packaging format that aligns with EU PPWR and U.S. state-level recycling mandates.

Advanced Nanocellulose Coatings for High-Gas-Barrier Applications

Nanocellulose technology represents a breakthrough opportunity for applications requiring superior gas barrier performance. Derived from wood pulp, nanocellulose offers oxygen barrier properties that outperform traditional petrochemical-based materials. Academic studies show anisotropic nanocellulose films can cut oxygen transmission rates by up to 75% compared to uncoated paper, while some tests report barrier improvements up to 900 times greater than conventional materials like BoPET and EVOH. The exceptional crystallinity and tortuous structure of nanocellulose allow for ultra-thin coatings that provide protection without increasing weight or material usage. Beyond performance, nanocellulose is compostable, renewable, and food-safe, making it particularly appealing to brands with aggressive sustainability and circularity commitments. Its ability to replace synthetic barrier layers while meeting compostability and biodegradability targets positions it as a game-changing solution for sensitive applications such as snack packaging, dairy products, and ready-to-eat meals.

Leading Companies Are Driving Innovation and Sustainability in Paper Coating Materials

The competitive landscape is dominated by companies leveraging materials expertise, R&D capabilities, and sustainable practices to deliver high-performance coating solutions for diverse paper and paperboard applications. Key players differentiate through strategic acquisitions, innovation in functional additives, and sustainability initiatives, enabling enhanced printability, barrier performance, and operational efficiency.

Omya AG’s Mineral-Based Solutions Enhance Paper Brightness and Printability

Omya AG is a leading global producer of essential minerals, including calcium carbonate used in paper coatings. In February 2025, Omya acquired Distrupol to create a global polymers distribution business, expanding its specialty materials portfolio. Omya offers precipitated and ground calcium carbonates that enhance brightness, opacity, and printability, supporting sustainable and high-quality paper products. Its strategy focuses on leveraging natural minerals to meet sustainability goals and improve end-product performance.

Kemira Oyj’s Bio-Based Coatings Position the Company for a Carbon-Neutral Future

Kemira Oyj specializes in sustainable chemical solutions for water-intensive industries, including pulp and paper. Its 2024 sustainability report emphasizes a bio-based product portfolio expansion by 2030 and carbon-neutral operations by 2045. Kemira provides binders and barrier coatings, such as the FennoBind portfolio, improving oil and grease resistance. Its strategy centers on innovative, sustainable solutions that enhance product quality and resource efficiency.

BASF SE Leads High-Performance Coatings with a Circular Economy Focus

BASF SE offers dispersion binders and specialty additives for paper coatings. In July 2025, it developed a sustainable two-tone painting process for automotive applications and released Q2 2025 financial results. Its Styronal, Acronal, and Acronal S binders improve binding strength, water resistance, and printability. BASF focuses on innovative, sustainable, high-performance solutions aligned with circular economy principles.

The Dow Chemical Company Develops Waterborne Solutions for High-Performance Paper Coatings

Dow Chemical supplies latex binders and specialty polymers for paper coatings, providing water-based solutions with low VOC emissions. Its PRIMAL and RHOPLEX brands enhance binding strength, printability, and water resistance. Dow promotes sustainable coatings for industrial applications, focusing on recyclability and circular economy integration.

J.M. Huber Corporation’s Specialty Minerals Enable Bright and Functional Paper Surfaces

J.M. Huber Corporation, through Hubergroup Chemicals, provides kaolin clay, calcium carbonate, and specialty pigments to improve brightness, opacity, and printability. In April 2024, it showcased its portfolio at the American Coatings Show, emphasizing high-performance, sustainable solutions. Huber focuses on custom-engineered materials that support sustainable and functional paper and paperboard coatings.

Paper Coating Materials Market Share Insights, 2025-2034

Packaging Paper & Paperboard Leads Market Share by Application in the Paper Coating Materials Industry

Packaging paper and paperboard dominate the paper coating materials market with nearly 65% share, cementing their role as the backbone of the industry. This dominance is directly linked to the e-commerce surge, premium consumer packaging, and the rising demand for food-grade functional barriers. Coatings are indispensable in this segment, not only for enhancing printability and shelf appeal but also for delivering critical performance attributes such as grease resistance, moisture protection, and extended shelf-life. The rapid substitution of plastics with fiber-based packaging has intensified the reliance on coated solutions that preserve recyclability while meeting stringent food safety and sustainability mandates. Labels further extend the performance-driven application of coatings, requiring formulations tailored for moisture stability and high-gloss finishes, while specialty papers like thermal, decorative, and release liners reflect a high-value niche where innovation in coatings is a differentiator. Although printing and writing paper has declined structurally due to digitalization, it continues to support a shrinking yet profitable demand for premium, high-gloss coated substrates in marketing and publishing. Together, these application trends underscore how coating materials are no longer just about enhancing print quality but are increasingly central to sustainable packaging transformation and high-performance specialty functions.

Food & Beverage Packaging Commands Market Share by End-Use Industry in the Paper Coating Materials Industry

The food and beverage sector leads the end-use landscape with 35% share, underscoring the critical role of coatings in ensuring safety, durability, and compliance for consumable products. This segment relies heavily on barrier-coated paperboard for frozen foods, liquid packaging, bakery wraps, and takeaway formats, where coatings deliver grease, oil, and oxygen resistance while maintaining recyclability. Sustainability-driven innovation, such as water-based coatings and bio-based polymers, is accelerating adoption as brands pivot away from plastic laminates. The e-commerce and retail sector follows closely with 30% share, fueled by the need for scuff-resistant, graphically enhanced corrugated and folding cartons that withstand supply chain handling while supporting brand visibility. Healthcare and pharmaceuticals, though smaller in volume, are high-value niches requiring coatings that comply with strict regulatory standards, ensuring tamper evidence, sterility, and chemical resistance in medical and pharmaceutical packaging. Similarly, personal care and cosmetics depend on premium tactile finishes and high-gloss coatings to reinforce luxury positioning and sustainability credentials. Industrial manufacturing and publishing represent more functional niches, where coatings provide release properties, abrasion resistance, or legacy demand for coated print products. Collectively, end-use segmentation highlights how functional barriers for food and beverages, durability for e-commerce, and compliance-driven coatings for healthcare are shaping material innovation and driving growth across the paper coating materials market.

United States Paper Coating Materials Market Accelerates with FDA PFAS Ban and Bio-Based Innovation

The United States paper coating materials market is undergoing a significant transformation due to recent U.S. Food and Drug Administration (FDA) actions, including the ban on per- and polyfluoroalkyl substances (PFAS) in food contact materials. This regulatory shift has created strong momentum for fluorine-free alternatives and advanced barrier coatings that ensure food safety while maintaining durability. Companies like International Paper and Dow are at the forefront, investing heavily in sustainable and high-performance coatings tailored for the booming e-commerce and food packaging sectors.

The U.S. also benefits from a robust recycling infrastructure and rising consumer preference for eco-friendly and biodegradable solutions, driving innovations in repulpable coatings. Furthermore, the market is seeing rapid adoption of functional coatings with antimicrobial and UV-resistant properties, which add value in sectors like pharmaceuticals and healthcare packaging. U.S.-based manufacturers are increasingly shifting to bio-based binders derived from starch and cellulose, significantly reducing carbon footprints and aligning with broader circular economy goals.

China Paper Coating Materials Market Expands with E-Commerce Growth and Sustainability Regulations

The China paper coating materials market is rapidly expanding, propelled by strict plastic waste regulations and the government’s National Clean Air Programme. These policies are driving industries to shift away from plastics, boosting demand for advanced coated paperboard and fiber-based packaging. The explosive growth of e-commerce in China has intensified the need for lightweight, durable, and moisture-resistant packaging materials, where coatings play a critical role in ensuring performance.

Domestic paper companies are investing aggressively to increase production capacity and develop new coating technologies that address both strength and barrier properties. The food and beverage industry remains one of the largest application areas, requiring coatings with grease- and moisture-resistance to maintain safety and freshness. With its massive consumer base and expanding industrial capacity, China is positioning itself as a global hub for innovative and sustainable paper coating technologies.

Germany Paper Coating Materials Market Driven by EU Circular Economy and Premium Applications

The Germany paper coating materials market is heavily shaped by European Union directives, particularly the Packaging and Packaging Waste Directive, which mandates recyclable and biodegradable packaging solutions by 2030. This regulatory environment has accelerated adoption of eco-friendly and mono-material coatings. German companies such as BASF are pioneering in polymer dispersion technologies, with recent expansions to meet rising demand in both packaging and specialty paper markets.

Germany also has strong demand for high-performance coatings in luxury packaging, industrial uses, and electronics, reflecting its emphasis on precision manufacturing. Environmental certifications such as the Blue Angel ecolabel set stringent standards, pushing manufacturers to develop low-VOC, recyclable, and sustainable coatings. The combination of regulatory pressure, advanced R&D capabilities, and consumer preference for sustainable goods makes Germany a leading innovator in the global paper coating materials industry.

India Paper Coating Materials Market Grows with EPR Rules and Expanding Domestic Capacity

The India paper coating materials market is gaining momentum under the government’s Plastic Waste Management Rules and Extended Producer Responsibility (EPR) framework, both of which are encouraging industries to adopt paper-based alternatives over plastics. The food processing and e-commerce sectors are particularly influential, with rising demand for eco-friendly coatings that provide grease and moisture resistance.

Domestic paper producers such as Kuantum Papers are investing heavily in modernizing facilities and expanding production capacity, enabling the supply of sustainable and high-quality paper coatings. The National Clean Air Programme (NCAP) also indirectly supports this shift by promoting cleaner materials and industrial processes. Additionally, India’s abundant reserves of Ground Calcium Carbonate (GCC) give domestic manufacturers a cost advantage in producing coating-grade materials. Combined with the Make in India initiative, the market is moving toward self-reliance and innovation in eco-friendly coatings.

Japan Paper Coating Materials Market Strengthened by Green Innovation and High-Quality Standards

The Japan paper coating materials market is led by major players such as Nippon Paper Industries and Oji Holdings, both global leaders in sustainable forestry management and fiber-based material innovation. Japan’s packaging industry emphasizes precision, printability, and superior barrier properties, with coatings designed to meet the needs of magazines, food packaging, and high-end retail products.

With the rise of digital printing applications, demand for coatings that can handle high-resolution, fast-processing formats is growing across both commercial printing and packaging sectors. The government’s Green Innovation policies are further accelerating the development of biodegradable and compostable coating technologies, aligning with the nation’s climate goals. Japan’s strategic focus on exporting advanced coated paper solutions also underscores its position as a global leader in high-performance, sustainable paper coatings.

Paper Coating Materials Market Report Scope

Paper Coating Materials Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.7 Billion

|

|

Market Size (2034)

|

$7.2 Billion

|

|

Market Growth Rate

|

4.9%

|

|

Segments

|

By Material Type (Kaolin Clay, Calcium Carbonate, Titanium Dioxide, Starch, Binders, Wax & Wax Blends, Other Specialty Additives), By Application (Printing & Writing Paper, Packaging Paper & Paperboard, Specialty Papers, Labels), By End-Use Industry (Printing & Publishing, Food & Beverage, E-commerce & Retail, Personal Care & Cosmetics, Industrial Manufacturing, Healthcare & Pharmaceuticals)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Dow Inc., Imerys S.A., Michelman, Inc., International Paper Company, Sappi Limited, Nippon Paper Industries Co., Ltd., Oji Holdings Corporation, Stora Enso Oyj, Mondi Group, WestRock Company, Huber Engineered Materials, BillerudKorsnäs AB, DIC Corporation, IFF (International Flavors & Fragrances)

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Paper Coating Materials Market Segmentation

By Material Type

- Kaolin Clay

- Calcium Carbonate

- Titanium Dioxide

- Starch

- Binders

- Wax & Wax Blends

- Other Specialty Additives

By Application

By End-Use Industry

- Printing & Publishing

- Food & Beverage

- E-commerce & Retail

- Personal Care & Cosmetics

- Industrial Manufacturing

- Healthcare & Pharmaceuticals

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Paper Coating Materials Market

- BASF SE

- Dow Inc.

- Imerys S.A.

- Michelman, Inc.

- International Paper Company

- Sappi Limited

- Nippon Paper Industries Co., Ltd.

- Oji Holdings Corporation

- Stora Enso Oyj

- Mondi Group

- WestRock Company

- Huber Engineered Materials

- BillerudKorsnäs AB

- DIC Corporation

- IFF (International Flavors & Fragrances)

* List Not Exhaustive

Methodology

The research methodology integrates both primary and secondary approaches to provide a comprehensive, accurate analysis of the Paper Coating Materials Market. Primary research involved detailed interviews with industry executives, coating formulators, sustainability experts, and supply chain professionals across key global regions to capture insights on technological innovations, regulatory compliance, and operational strategies. Secondary research included examination of annual reports, regulatory databases, patents, sustainability disclosures, verified industry publications, and market intelligence reports. Advanced data triangulation validated market sizing, growth projections, and adoption trends for bio-based, mineral, and polymer coatings, incorporating macroeconomic indicators, raw material pricing, e-commerce expansion, and technological adoption such as nanocellulose and water-based polymer dispersions. Forecasting utilized both top-down and bottom-up approaches, while regional insights were contextualized against policy frameworks like EU PPWR, U.S. FDA regulations, and national EPR mandates, as well as trends in sustainability, digital printing, and e-commerce packaging. This rigorous, multi-layered methodology by USDAnalytics ensures reliable, fact-based insights for industry professionals navigating a rapidly evolving, high-performance, and sustainability-driven paper coating materials landscape.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.