Global Ambient Food Packaging Market Overview: Market Size, Growth, and Industry Insights

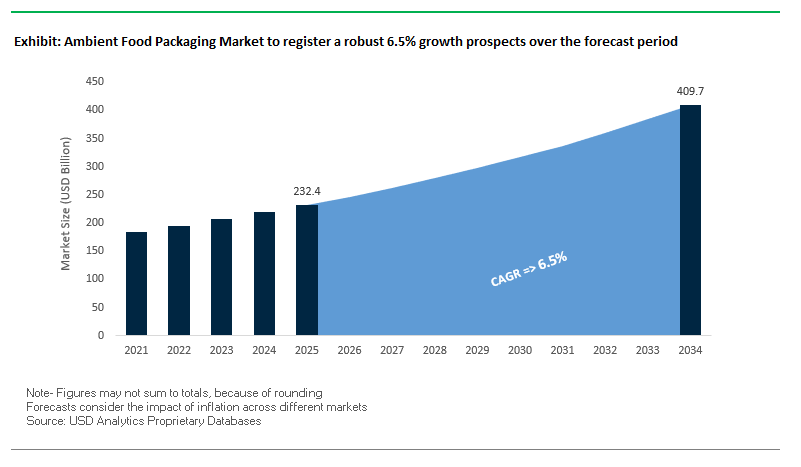

The Global Ambient Food Packaging Market is projected to grow from $232.4 billion in 2025 to $409.6 billion by 2034, expanding at a strong CAGR of 6.5%. As the food industry prioritizes shelf-life extension, waste reduction, and sustainable packaging, ambient packaging has emerged as a vital enabler of global supply chains. This category eliminates the need for refrigeration while ensuring product safety, convenience, and sustainability, positioning it at the core of the packaged food ecosystem.

The market’s growth is driven by three major forces: food waste reduction, the rise of aseptic and retort packaging, and consumer demand for single-serve convenience formats. Packaging technologies such as aseptic cartons and retort pouches sterilize and seal products in a way that guarantees longevity and safety without cold-chain dependency. At the same time, paperboard packaging is seeing widespread adoption as brands and regulators push toward eco-friendly alternatives to plastic.

The evolving consumer lifestyle dominated by ready-to-eat meals, snacking, and on-the-go consumption is accelerating adoption of resealable pouches, portion packs, and sustainable containers. This combination of sustainability, innovation, and lifestyle-driven consumption will continue to fuel the ambient food packaging market’s expansion.

Key Insights for Industry Professionals

- Food Waste Reduction: Packaging barriers against oxygen, light, and moisture extend shelf life, reducing food loss globally.

- Aseptic & Retort Packaging: Critical for eliminating refrigeration needs, reducing energy consumption, and ensuring safety.

- Paperboard Demand: Paper and paperboard cartons are rising as eco-friendly packaging alternatives to plastics.

- Convenience Growth: Single-serve formats and resealable pouches are meeting urban consumers’ fast-paced, mobile lifestyles.

Market Analysis: Recent Industry Developments and Strategic Moves

The ambient food packaging market has experienced significant momentum fueled by mergers, acquisitions, and product innovations. In August 2025, Amcor upgraded its Heanor recycling facility in the UK, expanding its capacity to produce recyclate from flexible plastic waste used extensively in ambient packaging. In the same month, Constantia Flexibles invested more than €100 million in its global network to strengthen flexible packaging solutions for food and pharma.

Also in July 2025, Huhtamaki expanded its sustainable portfolio with compostable and recyclable ice cream cups, while in May 2025, Pregis increased capacity for EVOH barrier films, boosting high-performance options for the food industry. Meanwhile, Amcor finalized its acquisition of Berry Global in April 2025, creating a packaging powerhouse with approximately $24 billion in annual revenue.

Earlier developments also reshaped the sector. In July 2024, Smurfit Kappa completed its merger with WestRock, creating Smurfit WestRock, a global leader in paper-based ambient packaging with unmatched global reach. In June 2024, Mondi and Saga Nutrition collaborated to launch sustainable pet food packaging, while Saica Group and Mondelez co-developed recyclable paper multipacks for confectionery. These initiatives reflect a dual strategy: investing in sustainable innovation while consolidating market power through large-scale acquisitions.

Emerging Trends and Strategic Opportunities Shaping the Ambient Food Packaging Market

Accelerated Shift to Mono-Material Polyolefin Structures for Recyclability

The ambient food packaging market is undergoing a significant transformation as global food brands and converters respond to Extended Producer Responsibility (EPR) regulations and ambitious corporate sustainability goals. The transition from multi-material laminates to mono-material polypropylene (PP) and polyethylene (PE) structures is gaining traction, driven by the need to align packaging with existing polyolefin recycling streams. Companies like Nestlé, Danone, Kraft Heinz, Mars, PepsiCo, and Unilever have pledged to achieve 100% recyclable, reusable, or compostable packaging by 2025, directly fueling demand for high-performance mono-material solutions. Regulatory pressures further accelerate this trend; for instance, California’s SB54 mandates 65% recycling of single-use plastics by 2032, compelling brands to adopt recyclable packaging formats. Advances in engineered polyolefin films now allow mono-material structures to deliver sufficient oxygen and moisture barrier properties, ensuring freshness and extended shelf-life for dry ambient foods such as snacks, nuts, cereals, and powdered products.

Integration of Digital Watermarks for High-Speed Sorting and Consumer Engagement

Digital watermarking technology, exemplified by HolyGrail 2.0, is being deployed to improve sorting accuracy of flexible packaging in recycling facilities while enabling enhanced consumer engagement. Industrial-scale trials at German facilities have achieved up to 93.8% detection accuracy for rigid plastics, demonstrating the technology’s potential to create high-purity recycling streams for previously unrecyclable flexible packaging. Embedded digital watermarks carry detailed SKU-level information, including product type and brand, providing traceability at a granular level unachievable with traditional near-infrared (NIR) sorting systems. The HolyGrail initiative is moving towards “HolyGrail 2030,” focusing on proving economic feasibility and creating high-quality recyclates suitable for food-grade packaging, a critical step toward a truly circular economy.

Development of High-Barrier, Compostable Films for Dry Foods

There is a substantial opportunity to commercialize compostable films that meet the stringent oxygen and moisture barrier requirements for dry ambient foods such as pasta, grains, snacks, and powdered products. Firms like Futamura and TIPA have introduced compostable films from renewable resources like wood pulp and cornstarch, certified for both industrial and home composting. These films offer excellent barrier protection, making them suitable for coffee pouches, snack bags, and other dry food applications. Unlike mono-material recyclable packaging, compostable films address the end-of-life issue of food-contaminated packaging, allowing the product to be composted along with food scraps, aligning with zero-waste initiatives and consumer demand for sustainable solutions.

Strategic Lightweighting of Metal Cans Through Advanced Alloys and Engineering

The ambient food packaging market is also exploring further reductions in the weight of steel and aluminum cans through advanced metallurgy and design engineering. Strategic lightweighting has already achieved a 40% reduction in steel can weight since 1970, and a 26% reduction in aluminum cans, increasing production efficiency (34 cans from the material previously yielding 27). High-strength, thin-walled alloys are being developed for can bodies, ends, and pull-tabs, maintaining mechanical integrity while simplifying recycling. Beyond material savings, lightweighting also reduces transportation emissions, lowering the carbon footprint of packaged food products, while mitigating raw material cost volatility, making it a compelling opportunity for sustainable packaging innovation.

Competitive Landscape: Leading Companies in Global Ambient Food Packaging

The competitive environment of the ambient food packaging industry is shaped by large multinational players and innovators that combine sustainability, global reach, and advanced barrier technologies to serve food manufacturers worldwide.

Smurfit WestRock: Global Leader in Paper-Based Ambient Packaging

Formed by the merger of Smurfit Kappa and WestRock in July 2024, Smurfit WestRock is now one of the world’s largest providers of paper-based packaging. With a presence in 42 countries and over 500 operations, the company delivers corrugated packaging and specialized solutions for bulk transport of produce and grains. Its EnduraGrip and EverGrow solutions offer moisture-resistant and ergonomic features, reflecting its strategic focus on eco-friendly, paper-based innovations.

Constantia Flexibles: Driving Innovation in High-Barrier Flexible Packaging

Constantia Flexibles leads in flexible packaging solutions with a diverse portfolio of aluminum foils, laminates, and pouches. In April 2025, its ComforLid won the Global Packaging Award, reinforcing its commitment to high-performance sustainable solutions. It also launched a mono-PP spouted pouch designed for recyclability without aluminum. With its February 2024 acquisition of Aluflexpack AG, Constantia has strengthened its European market presence while advancing its “People Passion Packaging” sustainability vision.

Amcor plc: Expanding Market Dominance with Berry Global Acquisition

Amcor strengthened its leadership by finalizing the Berry Global acquisition in April 2025, significantly enhancing its integrated solutions portfolio. Its investments in recycling capacity, such as the August 2025 Heanor facility upgrade, underline its focus on closing the loop on flexible packaging. With flagship products like AmLite Recyclable and its proprietary Amcor 360 service, the company is steering the market toward packaging that is recyclable, reusable, or compostable by 2025.

Huhtamaki Oyj: Innovating Fiber-Based Alternatives and Compostable Solutions

Huhtamaki continues to lead with innovations in fiber-based packaging and compostable solutions. Its July 2025 compostable ice cream cups and FunctionalBarrier Paper range show its capability in offering recyclable, fiber-based barrier packaging. With strong vertical integration and R&D, Huhtamaki leverages global resources to expand sustainable alternatives to plastics, making it a competitive force in flexible and paper-based ambient packaging.

Ambient Food Packaging Market Share Insights

Flexible Packaging Holds the Largest Share by Product Type in the Ambient Food Packaging Industry

Flexible packaging commands 45% of the ambient food packaging market, reflecting its unmatched efficiency in material use, logistics, and adaptability. Stand-up pouches, laminated films, and bags dominate this category, offering lightweight protection and extended shelf stability for products such as soups, dried meals, and confectionery. Advanced barrier laminates incorporating aluminum foil layers or metallized films enable long-term preservation without refrigeration, aligning with rising global demand for ambient storage formats. Rigid packaging cans, jars, and rigid plastics retains a strong presence due to its superior protection and consumer familiarity. Metal cans, in particular, remain the gold standard for shelf life in vegetables, seafood, and meats, supported by retort processing. Semi-rigid packaging occupies a balanced middle ground, with trays and composite tubs serving ready meals and condiments. This segment benefits from its ability to offer structure and convenience while being lighter than traditional rigid containers, making it well-suited to modern on-the-go consumption patterns.

Ready-to-Eat Meals Drive Market Share by End-Use Application in the Ambient Food Packaging Industry

Ready-to-eat (RTE) meals represent the leading application at 25%, driven by accelerating urbanization, evolving dietary habits, and the demand for quick, shelf-stable meal solutions. Retort pouches, foil trays, and aseptic cartons dominate this segment, offering easy-open functionality, microwave compatibility, and long-term storage without refrigeration. Bakery and confectionery packaging is the second-largest driver, where metallized films and laminates extend shelf life by protecting against staleness and moisture ingress. Sauces, dressings, and condiments rely on a combination of glass jars, barrier-layer bottles, and flexible sachets to maintain freshness and brand differentiation. Fruits and vegetables continue as a core segment, largely supplied in cans and jars, where hermetic sealing guarantees multi-year shelf life. Meat, poultry, and seafood packaging requires the most robust preservation technologies, with high-barrier retort pouches and cans ensuring product safety under extreme processing conditions. Dairy products represent an innovation-led niche, with aseptic cartons and flexible formats enabling shelf-stable milk, creamers, and condensed milk, particularly in emerging markets where refrigeration access is limited.

United States: EPR Regulations and Sustainable Innovations Driving Ambient Food Packaging

The U.S. ambient food packaging market is increasingly shaped by state-level Extended Producer Responsibility (EPR) laws, which place the responsibility and cost of packaging waste management on producers. This regulatory push is driving the adoption of sustainable and easily recyclable materials such as paperboard and high-recycled-content plastics. Technological advancements are also transforming the sector, with innovations like modified atmosphere packaging (MAP), high-barrier films, and retort pouches extending the shelf life of ambient products without refrigeration.

Corporate initiatives underscore the market’s sustainability focus. Mondi Group launched its EcoVantage™ recyclable packaging solution in December 2023, while Smurfit Kappa Group introduced its Bag-in-Box solution in March 2020, providing cost-effective and convenient ambient food packaging options. Rising consumer demand for eco-friendly solutions is pushing companies to incorporate higher percentages of post-consumer recycled (PCR) content and mono-material designs that simplify recycling. Key applications include ready-to-eat meals, soups, and sauces, particularly fueled by e-commerce growth and the preference for convenience foods. Premiumization trends are driving demand for high-barrier packaging that maintains product quality and supports clean-label formulations, offering protection against oxygen and moisture.

Germany: Circular Economy Leadership and Innovative Paper-Based Packaging

Germany’s ambient food packaging market is guided by a stringent regulatory framework, including the EU Packaging and Packaging Waste Regulation (PPWR) effective February 2025. This legislation mandates fully recyclable or reusable packaging by 2030, prompting innovation in materials and design. The German Packaging Act (VerpackG) further enforces producer responsibility for the entire life cycle of packaging, benefiting the ambient food sector through widespread adoption of recycling and mono-material packaging systems.

Technological advancements are driving new product development, such as grass paper and high-strength recycled fibers for paper-based packaging. Governmental mandates under PPWR establish waste reduction targets, significantly influencing packaging design and sustainability initiatives. Key applications are particularly strong in confectionery and bakery sectors. Collaborations, like those between Syntegon and brands such as Ritter Sport and Mars Wrigley, have led to paper-based pouches and flow wraps for chocolate bars and snacks, replacing traditional plastic packaging while ensuring product safety and quality.

China: Dual Carbon Goals and E-Commerce Expansion Shape Ambient Food Packaging

China’s ambient food packaging market is being transformed by the government’s dual carbon goals and a focus on reducing delivery and packaging waste. A new packaging regulation, effective June 1, 2025, promotes recycled materials and reusable systems, particularly for the rapidly growing e-commerce and express delivery sectors. Manufacturers are integrating automation, AI, and “5G plus industrial internet” solutions to enhance production efficiency and flexible packaging capabilities.

Sustainability is a key driver, with policies restricting non-degradable plastics and spurring demand for paper-based and recyclable alternatives. Regulatory reforms in the food sector encourage the adoption of sustainable packaging, while domestic e-commerce growth fuels demand for customizable solutions for snacks, ready-to-eat meals, and other ambient foods. Leading delivery companies such as JDL Express and ZTO Express are implementing intelligent logistics systems and utilizing original manufacturer packaging to optimize material usage, reduce waste, and improve sustainability across the supply chain.

India: Government Incentives and Biodegradable Packaging Spur Market Growth

India’s ambient food packaging market is supported by governmental initiatives like the “National Strategy for Additive Manufacturing,” which aims to contribute nearly $1 billion to GDP by 2025, fostering startups and innovations in packaging machinery, materials, and software. Regulatory oversight by the Food Safety and Standards Authority of India (FSSAI) ensures compliance with the Food Safety and Standards (Packaging) Regulations, 2018, banning unsafe materials like newspapers for food wrapping and defining material and labeling standards.

Infrastructure investments, such as the Production Linked Incentive (PLI) Scheme for the food processing industry, enhance manufacturing capabilities and drive demand for standardized, high-quality packaging solutions. Technological adoption is rising, with QR codes and automated packaging systems improving traceability, product information, and shelf life. Focus on biodegradable and compostable materials is growing, exemplified by Mumbai-based WOL3D, which leverages advanced manufacturing to produce protective and sustainable packaging. Rising middle-class consumption and preference for convenience foods further boost the demand for ambient food packaging solutions in India.

Brazil: Regulatory Support and Strategic Investments Advance Sustainable Packaging

Brazil’s ambient food packaging market is strongly influenced by the National Solid Waste Policy, which promotes circular economy principles and encourages reusable, durable alternatives, including flexible packaging. Technological adoption, including robotics and AI, is enhancing operational efficiency and quality control, from automated sorting to defect detection. Corporate initiatives such as SIG’s partnership with DPA Brazil in March 2024 to produce spouted pouch packaging for the Chamyto yogurt line reflect a growing focus on convenience-driven packaging solutions.

Strategic investments totaling approximately R10.5 billion ($1.8 billion) per year over the next few years are expected to expand factories, advance sustainable packaging technologies, enhance recycling systems, and improve reverse logistics. Key applications are in the food and beverage sector, with expanding food processing driving demand for pouches, bags, and containers. The Brazilian market’s emphasis on sustainable practices and convenience-focused designs is fostering growth in ambient food packaging solutions that align with consumer and regulatory expectations.

Japan: Precision Manufacturing and Innovative Sustainable Materials Define the Market

Japan’s ambient food packaging market leverages advanced technologies and precision manufacturing, with AI accelerating design processes and enhancing production accuracy. Regulatory updates by the Ministry of Health, Labour and Welfare (MHLW) in May 2025 revised requirements for food-contact packaging, ensuring safety, compliance, and alignment with international standards.

The market is shifting toward sustainable materials, with companies like Toyo Seikan Group innovating recyclable, lightweight packaging solutions. Functional innovations focus on high-barrier protection and resistance to deformation, enabling high-performance applications such as retort pouches for ready-to-eat meals. Demographic factors, including an aging population and the rise of single-person households, are driving demand for convenience foods and single-serving ambient meals. Japanese companies are responding with packaging designs that extend shelf life, reduce environmental impact, and meet evolving consumer needs.

Ambient Food Packaging Market Report Scope

Ambient Food Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$232.4 Billion

|

|

Market Size (2034)

|

$409.6 Billion

|

|

Market Growth Rate

|

6.5%

|

|

Segments

|

By Material (Plastic, Paper & Paperboard, Metal, Glass, Others), By Product Type (Rigid Packaging, Flexible Packaging, Semi-rigid Packaging), By Technology (MAP, Vacuum Packaging, Aseptic Packaging, Retort Packaging, Hot-fill Packaging), By End-Use Application (Fruits & Vegetables, Meat/Poultry/Seafood, Dairy Products, Bakery & Confectionery, Sauces/Dressings/Condiments, RTE Meals)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Mondi Group, Smurfit Kappa Group, DS Smith Plc, International Paper, Tetra Pak (Tetra Laval), Sonoco Products Company, Crown Holdings Inc., O-I Glass, Inc., Huhtamäki Oyj, Berry Global Group, Inc., Ball Corporation, Graphic Packaging International, Sealed Air Corporation, Greif, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Ambient Food Packaging Market Segmentation

By Material

- Plastic

- Paper & Paperboard

- Metal

- Glass

- Others

By Product Type

- Rigid Packaging

- Flexible Packaging

- Semi-rigid Packaging

By Technology

By End-Use Application

- Fruits & Vegetables

- Meat/Poultry/Seafood

- Dairy Products

- Bakery & Confectionery

- Sauces/Dressings/Condiments

- RTE Meals

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Ambient Food Packaging Market

- Amcor plc

- Mondi Group

- Smurfit Kappa Group

- DS Smith Plc

- International Paper

- Tetra Pak (Tetra Laval)

- Sonoco Products Company

- Crown Holdings Inc.

- O-I Glass, Inc.

- Huhtamäki Oyj

- Berry Global Group, Inc.

- Ball Corporation

- Graphic Packaging International

- Sealed Air Corporation

- Greif, Inc.

* List Not Exhaustive

Methodology

USDAnalytics employs a rigorous, multi-faceted research methodology to deliver comprehensive insights on the global Ambient Food Packaging Market. Our approach combines extensive primary research including interviews with packaging engineers, supply chain leaders, sustainability managers, and R&D heads with secondary research from corporate reports, trade journals, regulatory filings, and industry publications. Market sizing, projected to grow from $232.4 billion in 2025 to $409.6 billion by 2034 at a CAGR of 6.5%, is derived using both top-down and bottom-up analyses across materials (plastic, paper & paperboard, metal, glass), product types (rigid, flexible, semi-rigid), technologies (MAP, vacuum, aseptic, retort, hot-fill), and end-use applications (fruits & vegetables, meat/poultry/seafood, dairy, bakery & confectionery, sauces, RTE meals). USDAnalytics also evaluates key trends including mono-material polyolefin adoption for recyclability, high-barrier compostable films, digital watermarking for sorting and traceability, and lightweighting of metal cans. Regional analysis spans the U.S., Germany, China, India, Brazil, and Japan, integrating regulatory frameworks, Extended Producer Responsibility (EPR) laws, sustainability mandates, and e-commerce-driven packaging demands. Competitive benchmarking encompasses major players like Amcor, Smurfit WestRock, Constantia Flexibles, Huhtamaki, Mondi, and Tetra Pak, assessing capacity expansion, innovation, and sustainable packaging initiatives. This integrated methodology ensures actionable intelligence for strategic decisions, sustainability planning, and operational optimization in ambient food packaging.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.