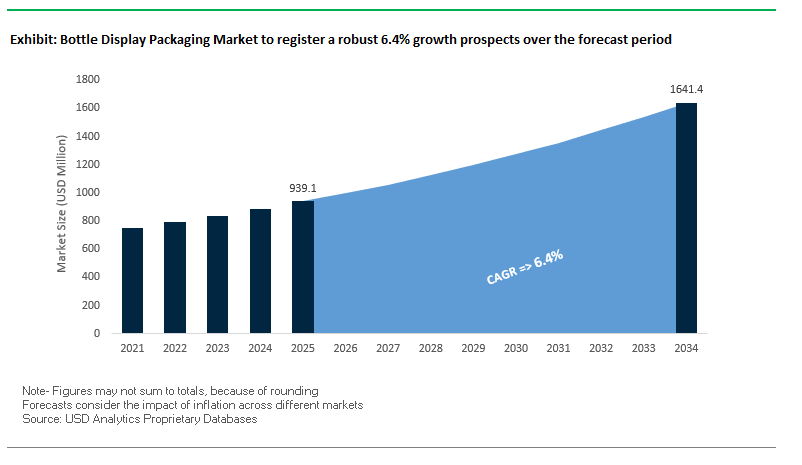

Bottle Display Packaging Market to Reach USD 1.64 Billion by 2034, Expanding at 6.4% CAGR

The global bottle display packaging market is projected to grow from USD 939.1 million in 2025 to USD 1.64 billion by 2034, registering a steady CAGR of 6.4%. This growth is underpinned by rising consumer demand for visually appealing and sustainable packaging solutions across beverages, cosmetics, and premium personal care. With over 70% of purchase decisions made at the point of sale, shelf-ready and display-focused packaging formats are proving critical in influencing consumer choice and driving brand loyalty.

Key industry trends include the premiumization of packaging, where brands use textured finishes, unique designs, and luxury elements to differentiate products, as well as digital printing advancements that allow for rapid customization and short-run promotional campaigns. Sustainability remains central to the market’s evolution, with a growing transition toward recycled fiberboard, bioplastics, and compostable coatings in line with retailer requirements and consumer eco-consciousness.

Key Insights for Industry Leaders

- Market size: USD 939.1M (2025) → USD 1.64B (2034) at 6.4% CAGR.

- Purchase influence: 70%+ of buying decisions made at point of sale.

- Sustainability driver: High adoption of recycled paper, corrugated board, and biodegradable coatings.

- Premium branding: Luxury finishes and unique shapes driving consumer engagement.

- Digital printing: Enables faster turnaround, personalization, and targeted promotions.

Recent Regulatory Shifts and Corporate Expansions Shape Bottle Display Packaging Market

The competitive and regulatory landscape is rapidly reshaping the bottle display packaging industry, creating fresh opportunities for paperboard and corrugated solutions. In August 2025, the newly formed Smurfit WestRock debuted in New York and London following the Smurfit Kappa–WestRock merger, instantly becoming a global leader in sustainable display-ready packaging. That same month, Mondi showcased its e-commerce packaging portfolio at eCommerce EXPO UK, a milestone signaling how bottle display packaging is being adapted for the fast-growing online retail sector.

In July 2025, International Paper divested five European corrugated plants to finalize its acquisition of DS Smith, consolidating its footprint as a global leader in corrugated bottle displays. Mondi, in June 2025, unveiled recyclable packaging with bio-based coatings, highlighting innovation in protective yet compostable materials. Similarly, Billerud’s October 2024 launch of ConFlex CoatBase Met provided a recyclable alternative for previously non-recyclable displays, enhancing circular economy potential in the bottle packaging sector.

Corporate anniversaries and expansions also play a role in strengthening supply networks. Smurfit WestRock’s Três Barras mill in Brazil celebrated 50 years of sustainable production in December 2024, cementing its strategic role in the global supply of display-ready materials. Meanwhile, the Mitsubishi Chemical–ALBION collaboration (Feb 2025) focused on circular cosmetic container solutions signals the wider crossover of bottle display packaging innovations into adjacent consumer goods.

Emerging Trends and Strategic Opportunities Driving the Bottle Display Packaging Market

The Strategic Shift to Monomaterial Packaging for Recyclability

A defining trend in the bottle display packaging market is the shift toward monomaterial PET packaging, moving away from complex, multi-material constructions. This strategy aligns with sustainability goals, ESG mandates, and regulatory pressures, enabling brands to improve recyclability and enhance circularity. Key drivers include Extended Producer Responsibility (EPR) schemes and initiatives under the European Union Circular Economy Action Plan, which aims to make all packaging recyclable by 2030. Leading companies are actively adopting monomaterial solutions: Nestlé reported that 86.6% of its packaging is reusable, recyclable, or compostable, emphasizing monomaterial designs, while Coca-Cola has introduced monomaterial caps and labels to boost PET bottle recyclability. Monomaterial packaging also benefits from compatibility with existing recycling infrastructure, allowing brands to scale sustainability efforts without significant new investment. Advanced monomaterial films now incorporate barrier enhancements, antimicrobial properties, and oxygen-scavenging functionality, demonstrating that performance and sustainability can coexist in a single-material structure.

Integration of Digital and Connected Packaging Technologies

Digital and connected packaging is transforming static bottle displays into interactive consumer interfaces. Brands are embedding QR codes, NFC chips, and AR triggers to enhance supply chain transparency, combat counterfeiting, and engage directly with consumers. Growing consumer demand for transparency, as reported by digital marketing studies, shows that two-thirds of consumers may switch brands for more detailed product information. PepsiCo has leveraged QR codes on limited-edition bottles to provide promotional content, while Jameson Irish Whiskey uses NFC and QR technologies to offer personalized digital experiences. High-end spirits brands like Remy Martin and Johnnie Walker employ NFC chips to authenticate products and track them through the supply chain. This trend allows bottle packaging to serve as a dynamic marketing and engagement tool, providing brands with actionable consumer data and strengthening brand loyalty in a competitive marketplace.

Development of Advanced Bio-Based and Compostable Polymers

An important growth opportunity in the bottle display packaging market is the creation of high-performance bio-based and compostable polymers. Research highlights the need for materials with enhanced barrier properties and heat resistance to compete with conventional PET in premium beverages. Polymers like PLA and other bio-based alternatives face limitations in heat tolerance and moisture resistance, creating a white space for innovative solutions. The ISCC Plus certification allows brands to trace bio-based raw materials, building trust and enabling investment. Governments, such as India’s Ministry of Housing and Urban Development, are exploring industrial composting infrastructure, further supporting the adoption of sustainable polymers. By offering drop-in alternatives compatible with existing machinery, manufacturers can provide eco-friendly packaging without compromising product quality, unlocking a scalable and impactful growth avenue.

Adoption of Smart, On-Demand Manufacturing and Decoration

On-demand manufacturing and digital decoration technologies are enabling brands to achieve mass personalization in bottle display packaging. Advances in digital printing and additive manufacturing reduce costs for short runs, facilitate limited editions, and enable regionalized designs or targeted marketing campaigns. Brands leverage these capabilities to create exclusivity, boost engagement, and drive sales. Suntory Products has utilized 3D printing to create customized bottling parts, reducing downtime and improving flexibility for different designs. This approach transforms the value chain by allowing packaging providers to offer end-to-end services from design to production enabling brands to rapidly adapt to consumer preferences and Market Trends, reinforcing agility in the premium beverage packaging segment.

Competitive Landscape: Leading Companies in Bottle Display Packaging Market

The global bottle display packaging market is dominated by fiber-based packaging leaders, flexible packaging specialists, and sustainability-driven innovators, each pushing for differentiation through material innovation, premium design, and circular economy strategies.

Smurfit WestRock Emerges as a Global Leader in Paper-Based Bottle Displays

Smurfit WestRock, formed from the 2024 Smurfit Kappa–WestRock merger, debuted in August 2025 as a powerhouse in corrugated and display-ready packaging. Its portfolio spans retail-ready corrugated solutions and premium POS displays for beverages and consumer goods. Recent investments include a new corrugated hub in Wisconsin, aimed at boosting regional supply chain efficiency. With sustainability and premium branding at its core, the company sets the benchmark in eco-friendly bottle display packaging.

Mondi Group Strengthens Position with Sustainable E-Commerce Displays

Mondi offers an extensive range of paper-based and flexible display packaging, widely used for bottle presentation in retail and online channels. In August 2025, Mondi unveiled a UK-focused e-commerce packaging lineup, reinforcing its edge in digital-first bottle displays. With a corporate pledge to make 100% of products recyclable or compostable by 2025, Mondi continues to expand through acquisitions such as Schumacher Packaging’s Western Europe operations, enabling customized, solid board solutions for brand-driven displays.

International Paper Expands North American Sustainable Packaging Capacity

International Paper remains a cornerstone in corrugated and fiber-based bottle display packaging. In June 2025, it announced plans for a sustainable packaging facility in Salt Lake City, underlining its North American growth strategy. The company’s July 2025 divestiture of European plants post-DS Smith acquisition highlights its commitment to regulatory compliance while expanding global presence. Its suite of corrugated display packaging for beverages and FMCG is recognized for efficiency and eco-design.

DS Smith Leverages Circular Economy Expertise Under International Paper

Following its 2025 acquisition by International Paper, DS Smith continues to supply innovative point-of-sale and retail-ready packaging with a circular economy focus. The brand is known for high-quality printing and design solutions that enhance consumer engagement at the shelf. Integrated under International Paper’s global structure, DS Smith now leverages broader resources while maintaining its edge in circular bottle display packaging innovation.

Constantia Flexibles Invests €100 Million in Sustainable Flexibles for Bottle Packaging

Constantia Flexibles is a key global supplier of flexible laminates, foils, and secondary packaging formats for bottles. In August 2025, the company announced a €100 million investment to modernize its production facilities, focusing on expanding aluminum foil capacity and sustainability. Its Ecolutions portfolio, complemented by a joint demo with Syntegon on mono-material pouches, demonstrates its push for a 360-degree sustainable packaging approach, supporting beverage, personal care, and specialty bottle displays.

Bottle Display Packaging Market Share Insights

Corrugated Boxes Dominate Bottle Display Packaging Market Share by Type

Corrugated boxes hold the leading share of the bottle display packaging market at 35% in 2025, driven by their superior strength, cost-effectiveness, and recyclability for transporting multi-bottle packs of beverages such as beer, water, and soda. Folding cartons and premium boxes follow with 25%, preferred in categories like wine, spirits, and cosmetics where brand image and tactile shelf appeal directly influence consumer choice. Retail-ready formats such as trays and stand-up displays collectively account for 35%, reflecting the growing demand for easy stocking, high-visibility merchandising, and impulse-driven promotions at retail. Sleeves and wraps represent a smaller yet vital 5% share, enabling cost-effective differentiation for limited-edition runs and multi-brand promotions. The balance across these types underscores the dual focus of bottle display packaging: meeting logistics needs while maximizing branding and retail impact.

Food & Beverages Anchor Market Share by End-Use in Bottle Display Packaging

Food and beverages account for 55% of the bottle display packaging market in 2025, cementing their position as the largest end-use segment due to the sheer volume of bottled water, soft drinks, juices, spirits, and edible oils requiring multi-pack formats for logistics and merchandising. Personal care and cosmetics follow with a 25% share, where display packaging plays a crucial role in brand identity and premium positioning for perfumes, shampoos, lotions, and serums. Pharmaceuticals and medical applications represent 12% of demand, focused on functionality, tamper evidence, and compliance-driven requirements for glass medicine bottles and liquid solutions. Industrial uses, at 5%, center on chemicals, lubricants, and cleaning products, where corrugated boxes dominate due to safety, durability, and hazard communication. Together, these industries highlight the versatility of bottle display packaging as both a functional logistics solution and a branding tool across diverse markets.

United States Bottle Display Packaging Market Boosted by Sustainability Regulations and E-Commerce Trends

The U.S. bottle display packaging market is being significantly shaped by regulatory developments and corporate sustainability initiatives. Federal and state regulations, including the FTC “Green Guides” and Extended Producer Responsibility (EPR) bills passed in Washington and Maryland in 2025, are compelling producers to design display packaging that is recyclable, reusable, and environmentally transparent. This regulatory framework encourages innovation in materials and structural design, ensuring compliance while enhancing product appeal.

Corporate investments are increasingly focused on sustainable materials and advanced display aesthetics. Companies are redesigning cartons and boxes using recycled content paperboard and biodegradable films, with particular attention to premium spirits, wine, craft beer, cosmetics, and personal care sectors. Technological advancements, such as digital printing, holographic effects, and tactile finishes, are enabling intricate, short-run, and limited-edition designs. The growth of e-commerce is driving “DTC-ready” packaging solutions that combine durability for shipping with a premium unboxing experience. Governmental initiatives, including the EPA’s National Strategy to Prevent Plastic Pollution, provide further policy support, while 82% of U.S. suppliers prioritize recycled or biodegradable materials, highlighting a strong sustainability focus.

Germany Bottle Display Packaging Market Strengthened by Circular Economy Mandates and Hybrid Innovations

Germany’s bottle display packaging industry is guided by the stringent EU Packaging and Packaging Waste Regulation (PPWR), effective February 2025, which requires all packaging to be fully recyclable or reusable by 2030. Combined with Germany’s Packaging Act (VerpackG), producers are responsible for the entire lifecycle of packaging, ensuring compatibility with recycling streams and encouraging sustainable design.

Technological innovation is central to market growth. At FachPack 2025, Sappi Europe introduced high-barrier papers as recyclable alternatives to plastic, while Mondi Group developed FunctionalBarrier Paper suitable for bottle display applications. Hybrid packaging concepts combining corrugated board with transparent windows or foam inserts are gaining traction, optimizing protection, shelf appeal, and functionality. German R&D investments, demonstrated by Karl Knauer’s modular sleeve system for seasonal gift packaging, are advancing lightweight, strong, and sustainable solutions, aligning with regulatory mandates and consumer demand for premium yet eco-friendly packaging.

China Bottle Display Packaging Market Accelerates with Green Policies and Domestic Manufacturing Expansion

China’s bottle display packaging market is increasingly influenced by the government’s dual carbon goals and regulatory reforms. The five-year plan (2021-2025) aims to reduce single-use plastics and promote bio-based alternatives, while new national standards for recycled plastics (effective February 2026) require manufacturers to prioritize recyclability in packaging design. SAMR’s updates to GB standards ensure global-aligned safety and consumer protection, providing a clear framework for innovative bottle display packaging.

Technological adoption is rising, with AI and “5G plus industrial internet” integration optimizing production efficiency and flexible manufacturing. Domestic companies are replacing imported technology to meet growing local demand, particularly from the beverage, e-commerce, and food delivery sectors. Key applications focus on efficient, cost-effective, and sustainable packaging for domestic consumption and export. Despite lower direct R&D funding compared to the U.S., China ranks second in global packaging patents, reflecting strong innovation in bottle display solutions.

India Bottle Display Packaging Market Strengthened by Export-Oriented Sustainability and Advanced Machinery

India’s bottle display packaging market is shaped by government initiatives like “Make in India” and “Zero Effect Zero Defect,” which promote high-quality domestic production. The CSIR-led National Mission on Sustainable Packaging Solutions focuses on developing eco-friendly materials and recycling systems. Regulatory policies, including MoEFCC and FSSAI regulations along with the PWM Rules 2016 and 2023 amendment, provide a clear framework for biodegradable and compostable materials.

Technological advancements and corporate investments are driving market growth. Companies like UFlex Ltd. obtained USFDA approval for recycled material usage in 2025, and Siegwerk committed INR 350 crore to expand innovation, manufacturing, and sustainability initiatives. The focus on exports to Europe has prompted investments in Braille embossing machines and advanced printing technologies. Key applications include the expanding food processing sector for snacks, ready-to-eat meals, and dairy products, as well as high-end beverages, requiring innovative, premium, and sustainable bottle display packaging solutions.

Brazil Bottle Display Packaging Market Grows with Regulatory Push and Sustainable Material Adoption

Brazil’s bottle display packaging market is guided by the National Solid Waste Policy and a 2024 law mandating returnable, recyclable, or compostable packaging by 2030. ANVISA’s RDC 843/2024 streamlines regulatory approvals, facilitating market entry for compliant and innovative packaging solutions.

Technological advancements, including AI and robotics, are enhancing operational efficiency, quality control, and product protection. Sustainability is a key driver, with companies like Klabin introducing recyclable Wicket Paper Bags applicable to bottle display packaging. Key applications include food, beverage, and cosmetics sectors, supported by government-led recycling targets of 30% in 2025 and 50% by 2040. Corporate initiatives, such as Qualy’s reinsertion of recycled polypropylene, further reflect a commitment to circular economy practices in display packaging.

Japan Bottle Display Packaging Market Transformed by Advanced Materials and Smart Packaging

Japan’s bottle display packaging market is leading in precision manufacturing and circular economy adoption. Companies like Kirin are deploying lightweight returnable glass bottles and chemically recycled PET for beverages, demonstrating advanced, sustainable solutions. The Plastic Resource Circulation Act (2022) enforces design for environmental sustainability and reduction of single-use plastics, guiding the industry’s innovation efforts.

Smart packaging integration is gaining momentum, with sensors and digital monitoring tools enhancing product safety, shelf life, and functionality. Constant innovation focuses on materials with high dimensional stability and resistance to deformation for premium applications. Major corporations like Toppan are pioneering recyclable, biodegradable, and high-barrier paper-based solutions, while academic research supports novel biopolymer and natural-agent-based packaging. Japanese innovations in corrugated cardboard cases optimize both structural strength and bottle protection, setting a benchmark for high-performance display packaging.

Bottle Display Packaging Market Report Scope

Bottle Display Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$939.1 Million

|

|

Market Size (2034)

|

$1641.3 Million

|

|

Market Growth Rate

|

6.4%

|

|

Segments

|

By Material Type (Paper & Paperboard, Plastics, Glass, Metal, Other Materials), By Packaging Type (Boxes & Cartons, Trays, Stand-up Displays, Corrugated Boxes, Sleeves & Wraps), By End-Use Industry (Food & Beverages, Pharmaceuticals & Medical, Personal Care & Cosmetics, Industrial, Others), By Distribution Channel (Offline, Online)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, WestRock Company, DS Smith Plc, Smurfit Kappa Group, International Paper Company, Mondi Group, Sonoco Products Company, Graphic Packaging Holding Company, Huhtamäki Oyj, AR Packaging Group AB (part of Graphic Packaging), Billerud AB, Oji Holdings Corporation, MeadWestvaco Corporation (part of WestRock), Crown Holdings Inc., Ball Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Bottle Display Packaging Market Segmentation

By Material Type

- Paper & Paperboard

- Plastics

- Glass

- Metal

- Other Materials

By Packaging Type

- Boxes & Cartons

- Trays

- Stand-up Displays

- Corrugated Boxes

- Sleeves & Wraps

By End-Use Industry

- Food & Beverages

- Pharmaceuticals & Medical

- Personal Care & Cosmetics

- Industrial

- Others

By Distribution Channel

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Bottle Display Packaging Market

- Amcor plc

- WestRock Company

- DS Smith Plc

- Smurfit Kappa Group

- International Paper Company

- Mondi Group

- Sonoco Products Company

- Graphic Packaging Holding Company

- Huhtamäki Oyj

- AR Packaging Group AB (part of Graphic Packaging)

- Billerud AB

- Oji Holdings Corporation

- MeadWestvaco Corporation (part of WestRock)

- Crown Holdings Inc.

- Ball Corporation

* List Not Exhaustive

Methodology

USDAnalytics employs a rigorous, multi-faceted research methodology to provide a comprehensive assessment of the global bottle display packaging market. Our approach combines primary research, including interviews with packaging manufacturers, brand managers, regulatory authorities, and end-users, with extensive secondary research from corporate reports, trade journals, patent filings, and sustainability initiatives. Market sizing and CAGR forecasts are derived by analyzing technological innovations, including corrugated, folding carton, and monomaterial PET displays, alongside advanced digital printing and connected packaging systems. The study evaluates market trends such as premiumization, on-demand decoration, sustainability transitions toward bio-based and compostable polymers, and regulatory compliance across key geographies including the U.S., EU, China, India, and Brazil. USDAnalytics also assesses corporate strategies, mergers and acquisitions, and capital investments by leading players such as Smurfit WestRock, Mondi, International Paper, DS Smith, and Constantia Flexibles to provide industry professionals with actionable insights into growth drivers, emerging opportunities, and competitive dynamics shaping the bottle display packaging market.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.