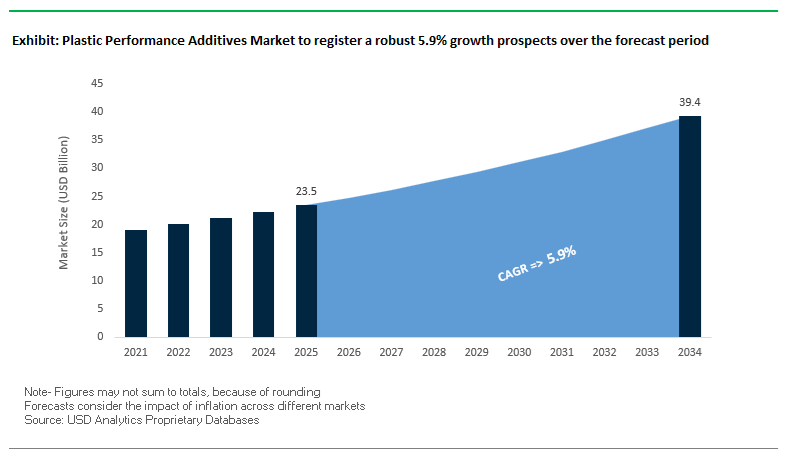

The Global Plastic Performance Additives Market is projected to grow from USD 23.5 billion in 2025 to USD 39.4 billion by 2034, registering a robust CAGR of 5.9%. The market’s steady expansion is driven by rising polymer consumption, sustainability mandates, and the transition toward high-performance, specialty-grade additives that enable recyclability, heat resistance, and material circularity across industries such as automotive, electronics, packaging, and construction.

A defining market force is the shift toward circular economy compliance, with global recyclability mandates reshaping additive development strategies. As only 10% of plastic waste is effectively recycled worldwide, the industry faces mounting regulatory pressure to reduce virgin polymer usage. This has triggered a surge in demand for compatibilizers, chain extenders, and stabilizers that restore mechanical strength and durability in post-consumer recycled (PCR) polymers.

Simultaneously, EV and high-temperature electronics are driving additive innovation. Modern engineering plastics used in EV battery casings, wire insulation, and thermal housings must sustain temperatures up to 200°C while meeting UL94 V-0 fire retardancy standards. This necessitates advanced formulations incorporating flame retardants, antioxidants, and hydrolysis stabilizers tailored for next-generation materials.

Meanwhile, the phaseout of PFAS-based additives by companies like BASF and Clariant (2024) marks a major industry milestone. The transition toward fluoro-free chemistries is reshaping performance additive portfolios, especially in films, cables, and coatings applications. Complementing this, the integration of digital passports and additive tracers—in alignment with EU Packaging and Packaging Waste Regulation (PPWR) effective 2030—is set to revolutionize traceability, compliance, and lifecycle transparency within plastic supply chains.

The Plastic Performance Additives Market is undergoing a phase of rapid regulatory evolution and strategic consolidation, as producers race to achieve circularity and secure high-value application segments.

In February 2025, M&A activity in the global plastics sector surged by 34.4% over the previous quarter, emphasizing the sector’s strategic realignment toward sustainable packaging, flame retardancy innovation, and recyclability enhancement. This momentum coincides with EU regulatory shifts, such as the Packaging and Packaging Waste Regulation (PPWR), effective February 2025, which mandates full recyclability by 2030. The regulation has already triggered new investment in compatibilizers, deinking additives, and stabilizer technologies to ensure compliance across polymer packaging chains.

BASF SE, in August 2025, unveiled its VALERAS® portfolio expansion at K 2025, focusing on “Extend the Loop” and “Close the Loop” frameworks—introducing new products like Tinuvin® NOR 112 HALS for agricultural films and advanced weatherable polymers. Meanwhile, Clariant AG, in November 2024, finalized its complete PFAS-free transition, debuting its AddWorks® PPA processing aid series to preempt regulatory bans in Europe and North America. This move positioned Clariant as one of the first companies globally to provide a fully fluorine-free additive line, aligning with long-term sustainability and compliance strategies.

LANXESS AG further advanced innovation by launching Levagard® 2100 in October 2025, a reactive phosphonate flame retardant offering low volatility and superior permanence in rigid polyurethane (PUR) and PIR foams, enhancing performance for insulation and construction applications. On the materials side, the ban on Bisphenol A (BPA) in food-contact plastics (EU, 2025) has accelerated R&D into antimicrobial stabilizers and BPA-free antioxidant systems.

Volatility in tin and phosphorous raw materials (2024–2025) has also influenced additive pricing and availability, prompting greater reliance on vertically integrated suppliers like SONGWON and Avient Corporation, which maintain captive intermediate production to ensure cost stability.

Across the global landscape, strategic initiatives like Sika’s collaboration with Sulzer (2025) and BASF’s ongoing partnerships with Security Matters to develop digital additive tracing for closed-loop recycling underline the industry’s pivot toward sustainability-driven digitalization—creating new standards for transparency and compliance in the plastics value chain.

Market Trend 1: Development of High-Efficiency, Non-Halogenated Flame Retardants for Electronics and Electric Vehicles

Global regulatory policies and environmental mandates are catalyzing the widespread substitution of halogenated flame retardants with non-halogenated, eco-compliant formulations in high-performance plastics. A defining driver of the trend is the European Union’s Ecodesign Regulation for Electronic Displays, which came into full effect in March 2021. The rule explicitly bans halogenated flame retardants in the casings and stands of electronic displays exceeding 100 cm², compelling manufacturers to adopt phosphorus-based, nitrogen-based, or mineral-based flame retardant systems.

In the wire and cable sector, halogen-free flame-retardant adoption exceeds 49% globally, reflecting mounting safety and environmental compliance pressures. These halogen-free systems are designed to minimize toxic smoke emission and corrosive gas release, aligning with low-smoke, zero-halogen (LSZH) specifications standard in European and Asian markets.

R&D investments are overwhelmingly concentrated in phosphorus-based chemistries, which account for roughly 46% of all new additive patents in the flame-retardant segment. These formulations are replacing legacy brominated compounds in polyolefins, polyamides, and high-performance thermoplastics, offering comparable flame retardancy with enhanced recyclability.

In the rapidly expanding electric vehicle (EV) industry, polymer flame retardants play a pivotal role in thermal protection. Advanced mineral-based flame-retardant additives have been launched to achieve the UL 94 V-0 flame rating for EV battery modules and connectors, ensuring effective containment against thermal runaway events. These developments position non-halogenated additives as a technological cornerstone in the electrification era, where fire safety, electrical insulation, and material circularity converge.

Market Trend 2: Proliferation of Advanced Nucleating and Clarifying Agents for High-Speed, Thin-Wall Processing

The second major trend shaping the plastic performance additives market is the accelerating use of nucleating and clarifying agents to enhance polymer crystallization kinetics, production efficiency, and mechanical performance in thin-wall applications. For industries like packaging, consumer electronics, and automotive, these agents enable faster production cycles and superior optical clarity—both vital to competitiveness.

Empirical studies demonstrate that advanced nucleating agents can reduce injection molding cycle times by up to 30% for polypropylene (PP) and other semi-crystalline polymers, a transformative productivity gain in large-scale operations. The adoption of nanofibrillar nucleating systems has also achieved simultaneous mechanical performance gains of 15% in tensile strength and 55% in elastic modulus, particularly in isotactic polypropylene used in lightweight structural components.

These additives also raise the onset crystallization temperature by approximately 11°C, effectively widening the processing window and shortening cooling cycles, thus improving throughput in high-speed production lines. Meanwhile, next-generation sorbitol-based clarifiers are being adopted to create ultra-transparent PP containers, enhancing brand visibility and consumer appeal—especially in premium food, personal care, and medical packaging markets.

Market Opportunity 1: Enabling the Circular Economy with Compatibilizers and Stabilizers for Plastic Recycling

One of the most transformative opportunities in the plastic performance additives industry lies in supporting the global shift toward circular economy models. With rising mandates for post-consumer recycled (PCR) content in packaging and industrial products, additive manufacturers are supplying specialized stabilizers, compatibilizers, and desiccants that address the inherent quality challenges of recycled polymers.

The European Union’s revised Packaging and Packaging Waste Regulation (PPWR) is poised to establish mandatory recycled content targets across multiple packaging categories. The policy framework is creating a sustained demand surge for additives that enhance the mechanical and thermal stability of recycled plastics during high-heat reprocessing.

Leading chemical producers have commercialized antioxidant masterbatches designed specifically for PCR applications, preventing oxidative degradation and preserving tensile and impact strength. Similarly, reactive compatibilizers are bridging the gap between immiscible polymers—such as polyolefins (PE, PP) and polar materials (EVOH, PA)—found in multilayer packaging waste. These additives chemically link incompatible resins, improving homogeneity and enabling mechanical recycling of complex plastic scrap previously destined for landfill or incineration.

Desiccant additives, another essential innovation, are mitigating moisture-related defects in recycled plastics. During melt processing, these additives capture residual moisture, preventing outgassing, fish eyes, and void formation, thus improving surface quality and enabling the reuse of higher PCR content.

Market Opportunity 2: Servicing the Additive Manufacturing Market with Functional 3D Printing Additives

Another high-value growth segment is the additive manufacturing (AM) industry, where functional polymer additives are redefining the boundaries of 3D-printed component performance. As industries such as aerospace, automotive, and medical devices increasingly integrate AM into production, the need for specialized performance-enhancing additives—for flame retardancy, conductivity, antimicrobial function, and mechanical reinforcement—is growing exponentially.

Aerospace OEMs are already utilizing UL94 V-0 flame-retardant filaments with heat deflection temperatures exceeding 150°C, enabling 3D printing of safety-critical air duct and cabin components. These materials are lightweight, strong, and compliant with aviation fire safety regulations.

Simultaneously, R&D institutions such as Fraunhofer and AIMPLAS are engineering functionalized polymer additives to impart electrical conductivity and antimicrobial resistance, expanding the application range of AM materials in medical and electronics manufacturing. Reinforced composites are another focus area: the integration of carbon and glass fibers into PEEK and PEKK matrices has drastically improved stiffness-to-weight ratios, enabling polymer-based metal substitution in high-load structural applications.

Real-world aerospace case studies underscore the commercial value of these advancements. For example, French aircraft manufacturers have successfully replaced metal tooling and models with 3D-printed composite structures, achieving significant weight reductions and operational cost savings—key proof points for the scalability of AM-ready polymer additives.

The competitive landscape of the plastic performance additives industry is marked by technological leadership, sustainability-driven innovation, and strategic portfolio expansion. Key players—including BASF SE, LANXESS AG, Clariant AG, Avient Corporation, Baerlocher GmbH, and SONGWON Industrial Co.—are redefining market standards through low-toxicity, high-efficiency, and circularity-enhancing additive solutions.

BASF leads the global additives market through its Industrial Solutions segment, emphasizing sustainability through its VALERAS® platform, which integrates additives, digital services, and product carbon footprint tracking (PCF) for cradle-to-gate transparency. Its core additive lines, including Irganox® antioxidants and Tinuvin® light stabilizers, are widely used in automotive, E&E, and construction polymers. BASF’s Irganox® 1010 BMBcert (biomass-balanced) product exemplifies the company’s low-carbon material transformation, certified under ISCC PLUS. BASF’s deep R&D focus on weatherable polymer protection and circular feedstock traceability strengthens its dominance in both high-performance and sustainability-oriented markets.

LANXESS maintains a global leadership position in flame retardant additive systems, offering a diversified portfolio of phosphorus and brominated retardants tailored for E&E, automotive, and building materials. The company’s Levagard® 2100, launched in October 2025, represents a breakthrough in reactive phosphonate technology, ensuring chemical bonding with polymers for long-term stability and low migration. Its Emerald Innovation® 5000 polymeric retardant replaces DBDPE in engineering plastics, addressing environmental and safety concerns. The company’s Climate-Neutral 2040 strategy and elimination of critical substances reinforce its market leadership in sustainable additive chemistry.

Clariant has successfully repositioned itself as a pioneer in halogen- and PFAS-free additive solutions, anchored by its Exolit® flame retardant and AddWorks® multifunctional additive product lines. In December 2023, Clariant achieved full PFAS elimination, launching new PPA processing aids that enhance polymer flow and extrusion efficiency without fluorinated compounds. Its AddWorks® ready-to-use packages reduce cost and complexity for compounders by integrating stabilizers and processing aids. Additionally, partnerships such as the Floreon biopolymer collaboration (2020) underline Clariant’s strategic push into bio-based plastics and sustainable material design.

Avient Corporation differentiates itself through its integration of additives into pre-formulated masterbatches, offering precision dosing and operational simplicity. Its Omnicolor® range features heavy-metal-free colorants compatible across multiple polymers, catering to sustainability-conscious brands. Avient’s additive systems are particularly strong in consumer goods, appliances, and medical devices, emphasizing clarity, safety, and antimicrobial performance. The company’s focus on portfolio optimization toward high-margin specialty applications—including lightweight automotive and recyclable packaging—aligns it with the industry's megatrends.

Baerlocher GmbH is a recognized leader in PVC and polyolefin stabilizers, offering long-term thermal and weathering resistance solutions for construction and infrastructure applications. The company pioneered calcium-based stabilizers, replacing heavy-metal formulations and ensuring compliance with EU REACH and global toxicological regulations. The launch of Baerolub® AID, a fluoro-free processing aid, reinforces Baerlocher’s proactive approach to sustainability amid tightening PFAS restrictions. Its expansive global manufacturing footprint across Europe, Asia, and the Americas ensures stable supply of metal stearates and additive blends, critical in polymer extrusion and compounding.

Country Analysis: Strategic Regional Developments in the Global Plastic Performance Additives Industry

China: Technological Self-Reliance and Packaging Expansion Driving High-Performance Additive Growth

China has firmly positioned itself as the global hub for plastic performance additives, driven by rapid industrial upgrades, technological self-reliance, and strong domestic consumption. The government’s strategic focus on petrochemical independence has accelerated investments in high-performance stabilizers, antioxidants, and specialty chemical capacity, reducing import dependence and strengthening China’s polymer additive ecosystem. The “Made in China 2025” initiative continues to support the local production of advanced materials, encouraging R&D in flame retardants, polymer stabilizers, and color concentrates designed for engineering plastics and electronics applications.

The nation’s e-commerce and packaging boom is significantly amplifying demand for barrier enhancers and food-grade antioxidants, particularly within the food, medical, and logistics packaging sectors. Local manufacturers are leveraging low-cost raw materials and labor advantages to expand production capacity and supply the growing domestic and export markets. Additionally, China’s electrical and electronics segment remains a major consumer, utilizing advanced flame retardants and thermal management additives to ensure product safety and performance in high-heat applications. The structural shifts—combined with expanding local R&D, global partnerships, and rising export competitiveness—are solidifying China’s role as the Asia-Pacific leader in next-generation plastic performance additive innovation.

United States: Advanced Manufacturing, Sustainable Chemistry, and Near-Shoring Catalyzing Market Momentum

The United States plastic performance additives market is undergoing a technological transformation anchored in automotive electrification, infrastructure modernization, and sustainable chemistry innovation. The U.S. automotive industry’s aggressive push toward electric vehicle (EV) adoption is fueling demand for specialized flame-retardant and high-flow additives critical for battery enclosures, connectors, and lightweight thermoplastic components. At the same time, infrastructure investments across housing and commercial construction have elevated the need for durable PVC stabilizers and impact modifiers that ensure long-lasting structural integrity.

An emerging near-shoring trend is reshaping supply chains, with domestic additive and compound manufacturers scaling up production to meet rising demand for locally sourced masterbatches and custom polymer compounds. The shift is particularly vital for the extrusion and molding sectors, which rely on short lead times and consistent additive supply. Concurrently, the U.S. is leading global efforts in non-phthalate plasticizers, bio-based stabilizers, and low-VOC additive formulations, aligning with evolving EPA and FDA regulations. As sustainability becomes a defining pillar of the industry, the U.S. remains a key innovation hub for green additive technologies, balancing performance with regulatory compliance and market resilience.

Germany: Electrification and Circular Economy Innovation Reshaping the Performance Additives Ecosystem

Germany remains at the forefront of Europe’s plastic performance additives innovation, underpinned by its strong industrial base, regulatory leadership, and high-value R&D ecosystem. The country’s automotive electrification agenda has intensified the use of halogen-free polyamides and polyphosphonate esters that enhance fire resistance and heat stability in EV battery housings and wiring components. The trend is complemented by Germany’s commitment to EU-wide fire-safety standards, particularly within the Renovation Wave initiative, which is driving large-scale adoption of non-halogenated flame retardants and phosphorus-based intumescent systems in insulation and construction materials.

Global chemical giants such as BASF and Lanxess are pioneering biomass-balanced plastic additives, including sustainable antioxidants like Irganox, designed to reduce fossil feedstock dependency. The nation’s additive research also focuses heavily on enhancing recyclability—developing new compatibilizers, stabilizers, and polymer processing aids that improve the mechanical properties of recycled plastics. Germany’s strategic integration of circular economy practices, combined with its technical expertise and stringent environmental regulations, continues to make it the European benchmark for advanced, sustainable polymer additive solutions.

India: Expanding Construction and FMCG Sectors Fueling Additive Consumption in Pipes and Packaging

India’s plastic performance additives industry is witnessing robust expansion, driven by construction, FMCG growth, and manufacturing modernization. The government’s infrastructure push—including initiatives for affordable housing and urban development—has sharply increased demand for PVC pipes, profiles, and sheets, all of which depend on heat stabilizers, impact modifiers, and processing aids for long-term performance. Rising disposable incomes and the proliferation of organized retail and FMCG packaging further bolster the demand for antioxidants and color masterbatches, particularly in flexible packaging films and rigid containers.

The nation’s rapidly expanding electronics manufacturing base also contributes to the demand for halogen-free flame retardants to ensure compliance with global safety and environmental standards. In parallel, India’s regulatory agencies are tightening building codes and fire-safety enforcement, prompting higher market penetration of performance-enhancing additives in construction polymers. Supported by low manufacturing costs, growing foreign investment, and accelerating urbanization, India is emerging as a key production and consumption hub for plastic performance additives in Asia.

Japan: Precision Additives and Eco-Friendly Formulations Powering High-Tech Polymer Applications

Japan’s plastic performance additives market continues to excel in precision engineering, eco-innovation, and high-performance polymer stabilization. Industry leaders such as Adeka Corporation are advancing comprehensive stabilizer portfolios tailored for automotive and electronics applications, focusing on UV resistance, oxidation stability, and long-term durability. Japan’s global leadership in automotive materials and microelectronics sustains strong demand for cyanoacrylate and polymer processing aids that deliver flawless, high-strength bonds essential for miniaturized and precision-engineered products.

The nation’s growing commitment to eco-friendly additive technologies is driving R&D investments into light-stabilizing and weather-resistant systems for outdoor and high-temperature applications. Advanced formulations enable lightweight, recyclable materials for next-generation transportation systems, aligning with Japan’s broader carbon-neutral targets. Combining precision manufacturing with continuous innovation in polymer chemistry, Japan remains a global frontrunner in the development of sustainable, high-performance additive technologies that support both quality and circularity in high-tech manufacturing.

Europe (Germany, France, United Kingdom): Regulatory-Driven Innovation Transforming Additive Chemistry and Market Direction

Across Europe, the plastic performance additives industry is undergoing a rapid transformation under the combined influence of REACH, the EU Green Deal, and Circular Economy Action Plan mandates. The frameworks are accelerating the transition toward bio-based, non-halogenated flame retardants, and low-VOC UV stabilizers, aligning the market with stringent environmental standards. The EU Chips Act and reshoring programs are reshaping the electronics and electricals sector, where halogen-free flame retardants are becoming essential for battery enclosures and 5G radio units.

European chemical manufacturers are actively introducing sustainable additive innovations, such as Clariant’s anti-scratch and high-durability additives for polypropylene (PP) and thermoplastic olefins (TPO), which improve the recyclability, mechanical performance, and aesthetic life of automotive and consumer products. Meanwhile, upcoming microplastic restrictions are compelling companies to reformulate masterbatches and adopt compliant dispersant and liquid additive systems. The evolution underscores Europe’s status as a regulatory and technological pioneer in the field of sustainable polymer performance additives, emphasizing recyclability, product longevity, and compliance-driven material reformulation.

Plastic Performance Additives Market Report Scope

Plastic Performance Additives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$23.5 Billion

|

|

Market Size (2034)

|

$39.4 Billion

|

|

Market Growth Rate

|

5.9%

|

|

Segments

|

By Function (Plasticizers, Stabilizers, Flame Retardants, Impact Modifiers, Processing Aids and Lubricants, Colorants and Pigments, Blowing Agents, Antimicrobials and Antistatic Agents, Nucleating and Clarifying Agents, Coupling Agents and Fillers), By Plastic Type (Commodity Plastics, Engineering Plastics, High-Performance Plastics), By End-User (Packaging, Building & Construction, Automotive, Electrical & Electronics, Consumer Goods, Agriculture, Medical & Healthcare, Textiles

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, The Dow Chemical Company, Evonik Industries AG, Clariant International Ltd., Lanxess AG, Songwon Industrial Co. Ltd., Adeka Corporation, Baerlocher Group, Eastman Chemical Company, Avient Corporation, DuPont de Nemours, Inc., Sakai Chemical Industry Co., Ltd., Albemarle Corporation, Nouryon, Huntsman Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Function/Type

- Plasticizers

- Stabilizers

- Flame Retardants

- Impact Modifiers

- Processing Aids and Lubricants

- Colorants and Pigments

- Blowing Agents

- Antimicrobials and Antistatic Agents

- Nucleating and Clarifying Agents

- Coupling Agents and Fillers

By Plastic Type

- Commodity Plastics

- Engineering Plastics

- High-Performance Plastics

By End-Use Industry

- Packaging

- Building & Construction

- Automotive

- Electrical & Electronics

- Consumer Goods

- Agriculture

- Medical & Healthcare

- Textiles

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Plastic Performance Additives Market

- BASF SE

- The Dow Chemical Company

- Evonik Industries AG

- Clariant International Ltd.

- Lanxess AG

- Songwon Industrial Co. Ltd.

- Adeka Corporation

- Baerlocher Group

- Eastman Chemical Company

- Avient Corporation

- DuPont de Nemours, Inc.

- Sakai Chemical Industry Co., Ltd.

- Albemarle Corporation

- Nouryon

- Huntsman Corporation

*- List not Exhaustive

Research Coverage

This report investigates the Global Plastic Performance Additives Market with rigorous analysis reviews of demand drivers, compliance levers, and cost-in-use dynamics across packaging, automotive, E&E, construction, and healthcare, and it highlights technology breakthroughs in non-halogenated flame retardants, PCR-enabling stabilizers/compatibilizers, high-temperature antioxidant systems, and digital traceability that future-proof polymer value chains; built by USDAnalytics, the study benchmarks specifications (UL94, weatherability, hydrolysis/oxidation resistance), compares circularity pathways (biomass balance, mass-balance certification, fluoro-free reformulation), and stress-tests scenarios under policy shifts and raw-material volatility—making this report an essential resource for executives and engineers who need clear segment sizing, competitive positioning, and strategy-ready insights through 2034.

Scope Highlights

Segmentation:

- By Function/Type: Plasticizers; Stabilizers; Flame Retardants; Impact Modifiers; Processing Aids and Lubricants; Colorants and Pigments; Blowing Agents; Antimicrobials and Antistatic Agents; Nucleating and Clarifying Agents; Coupling Agents and Fillers.

- By Plastic Type: Commodity Plastics; Engineering Plastics; High-Performance Plastics.

- By End-Use Industry: Packaging; Building & Construction; Automotive; Electrical & Electronics; Consumer Goods; Agriculture; Medical & Healthcare; Textiles.

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa).

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Timeframe: Historic data 2021–2024 and forecast data 2025–2034.

Companies: Analysis/profiles of 15+ companies.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.