Alcohol Packaging Market Overview: Premiumization, Sustainability, and E-commerce Transforming a $136.9 Billion Industry

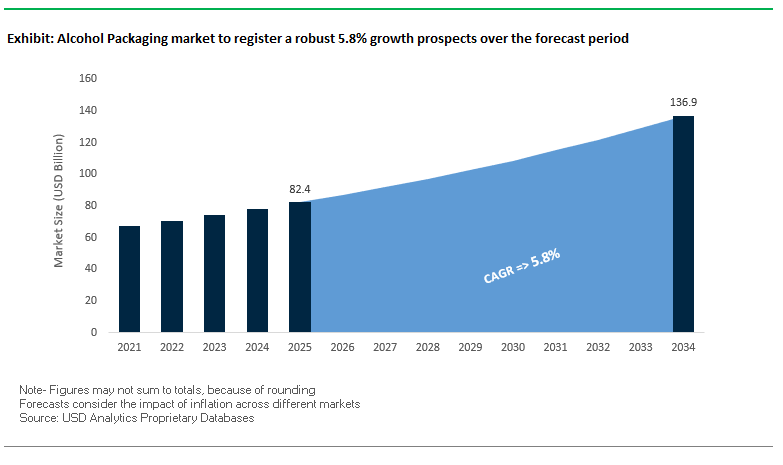

The global alcohol packaging market is projected to grow from USD 82.4 billion in 2025 to USD 136.9 billion by 2034, expanding at a CAGR of 5.8%. For industry professionals and brand owners, packaging is no longer a passive container it has become a strategic lever for differentiation, sustainability, and omnichannel growth. As premium spirits, craft beverages, and direct-to-consumer alcohol sales surge, the demand for packaging that balances luxury aesthetics, environmental performance, and protective functionality has never been greater.

Packaging executives and procurement specialists are now addressing three fundamental questions:

- How can packaging amplify brand storytelling and premium positioning while remaining cost-efficient?

- What sustainable solutions are available to reduce carbon footprints without compromising durability?

- How can packaging adapt to the growth of e-commerce channels, where transit protection and consumer experience are critical?

Key Insights for Industry Stakeholders

- Premiumization accelerates demand for custom-designed glass, embossed labels, and advanced closures in super-premium spirits, craft beer, and fine wine.

- Sustainability matters to 50%+ of consumers, driving adoption of lightweight glass, aluminum cans, and paper-based designs.

- E-commerce reshapes packaging requirements, fueling demand for robust secondary packaging and protective inserts to reduce breakage.

- Craft and artisanal expansion boosts niche demand for scalable, flexible, and creative packaging solutions that support limited runs and unique designs.

Market Analysis: Strategic Developments Redefining Global Alcohol Packaging

The past year has highlighted a wave of strategic acquisitions, sustainability milestones, and regulatory shifts that are reshaping the global alcohol packaging market. In January 2025, United Breweries launched Kingfisher Flavors, marking its entry into flavored beer and sparking demand for distinctive packaging tailored to youthful consumer segments. By April 2025, India’s DeVANS Modern Breweries introduced a new craft gin, underscoring the premiumization of local markets and the corresponding need for high-quality glass and decorative packaging.

In May 2025, Smurfit Kappa unveiled its Bag-in-Box wine solution, catering to sustainability-conscious consumers and the growing e-commerce wine segment. This was followed in June 2025 by the UK government’s proposal for mandatory recycling information and updated health warnings on alcohol bottles and cans, forcing packaging producers to upgrade labeling technologies and design systems.

In July 2025, O-I Glass reported early achievement of its 2030 sustainability goals achieving 51% renewable electricity use and reducing GHG emissions by 30% a milestone that will strengthen its credibility with sustainability-driven brands. During the same month, Quadpack invested in PET dip-in capacity in Germany, expanding its portfolio with potential applications in ready-to-drink (RTD) alcoholic beverages.

By August 2025, consolidation and supply chain optimization defined industry headlines. Amcor and Berry Global finalized their $24 billion merger, creating a global packaging powerhouse with strong leverage in beverage packaging. Simultaneously, Diageo announced a restructuring of its North American supply chain, including a bottling plant closure in Ontario, signaling a sharper focus on agility and cost efficiency. These moves, combined with long-term investments in sustainability and premiumization, are transforming the alcohol packaging ecosystem.

Emerging Trends and Opportunities Redefining the Alcohol Packaging Market

Strategic Lightweighting and Investment in Recycled Glass Content

Sustainability has become a defining focus for the alcohol packaging market, with leading players investing heavily in lightweighting and the incorporation of recycled glass (cullet). Glass bottles, while iconic in alcohol branding, carry a significant environmental footprint due to their weight and reliance on virgin raw materials. Companies such as Diageo are taking bold steps, with its 2025 Annual Report outlining a revised target to increase recycled content to 50% by 2030. Notably, Diageo has already surpassed its interim goals in plastics, achieving 43% recycled content by 2025, proving the scalability of circular packaging strategies. Lightweighting projects across flagship brands such as Baileys, Cîroc, and Johnnie Walker are designed to cut carbon emissions and reduce logistics costs without compromising durability. Regulatory frameworks are accelerating this shift. The European Union’s Packaging and Packaging Waste Regulation (PPWR) mandates full recyclability by 2030, while the UK’s Extended Producer Responsibility (EPR) tax which can reach £330 per tonne for unrecycled glass creates a direct financial burden for non-compliance. Together, ESG commitments, capital investments, and regulatory pressures are driving the alcohol industry toward a circular packaging economy that reduces costs while meeting global sustainability goals.

Premiumization through Secondary Packaging and Limited-Edition Designs

As competition in the alcohol sector intensifies, secondary packaging is becoming a crucial tool for premiumization, differentiation, and consumer engagement. Brands are leveraging high-value paperboard packaging, bespoke designs, and limited-edition collections to elevate perception and justify higher price points. The consumer “unboxing experience” has grown in significance, especially for luxury spirits, where intricate detailing, magnetic closures, and embossed finishes transform packaging into a ceremonial ritual. Beyond aesthetics, secondary packaging is being weaponized against counterfeiting. Features such as holograms, unique QR codes, and tamper-evident seals are now integrated into outer boxes, enabling consumers to instantly verify authenticity. A 2024 spirits packaging report also highlighted the increasing adoption of smart packaging technologies including QR codes and NFC chips that unlock interactive brand experiences. These allow consumers to access origin stories, exclusive digital content, or loyalty programs, building deeper brand relationships. The fusion of luxury design with digital engagement illustrates how packaging is no longer simply functional but central to storytelling, brand protection, and premium value creation.

Development of Mono-Material and Recyclable Flexible Pouches for Ready-to-Drink (RTD) Beverages

The explosive rise of the RTD cocktails market is creating significant opportunities for innovative alcohol packaging formats beyond traditional cans and glass bottles. Flexible pouches are emerging as a disruptive solution, offering portability, lightweight logistics, and reduced environmental impact. The challenge has historically been recyclability due to multi-layer constructions, but companies such as TOPPAN are pioneering mono-material pouches made entirely from polypropylene (PP) or polyethylene (PE). These solutions provide high-barrier protection against oxygen ingress, ensuring flavor and shelf-life integrity while being recyclable in existing plastic waste streams. For alcohol brands, adopting recyclable mono-material pouches provides a way to enter the high-growth RTD category with a sustainable alternative that resonates with eco-conscious consumers. Beyond convenience, these pouches also enable differentiation in crowded retail shelves and digital marketplaces, offering a canvas for bold designs and new branding opportunities. As RTDs continue to gain global momentum, recyclable pouch technology is set to become one of the most transformative innovations in alcohol packaging.

Capitalizing on Regulatory Shifts for D2C Shipping and E-commerce Compliance

The permanent expansion of direct-to-consumer (D2C) alcohol shipping, accelerated by regulatory changes and consumer demand, is creating a new frontier for alcohol packaging. Unlike retail formats, D2C channels require packaging engineered to withstand the rigors of parcel logistics while complying with legal mandates. Breakage prevention is paramount, driving the adoption of custom corrugated inserts and molded fiber pulp trays that provide superior cushioning and structural integrity for glass bottles. Regulatory compliance adds another layer of complexity. Carriers like FedEx mandate adult signature verification, which has spurred the development of tamper-evident outer packaging and age-verification labels to combat diversion to underage buyers. Efficiency also matters: “right-sized packaging” is becoming a priority for e-commerce fulfillment, as oversized boxes drive up shipping costs and waste. Brands are now working with packaging engineers to create custom-fit solutions that minimize void space and optimize shipping efficiency while maintaining sustainability credentials. With e-commerce becoming a permanent sales channel for premium spirits and wine, compliant, durable, and sustainable packaging innovations are set to drive long-term growth in this segment.

Competitive Landscape: Global Leaders Driving Premium, Sustainable, and Omnichannel Packaging Solutions

The alcohol packaging market is highly competitive, with global leaders combining scale, innovation, and sustainability to meet the evolving needs of alcohol producers and consumers. Companies are focusing on glass purity, lightweighting, paper innovation, and premium aesthetics while navigating new regulatory and e-commerce challenges.

O-I Glass Inc. leads with recyclable glass and sustainability milestones

O-I Glass remains a global leader in premium glass bottles and jars for beer, wine, and spirits. In July 2025, it validated early completion of its 2030 goals, surpassing targets for renewable electricity and GHG reductions. Its investments in gas-oxygen furnaces and expanded use of recycled cullet reduce environmental impact while maintaining premium quality. With 69 plants across 19 countries, O-I combines local responsiveness with a strong premium brand image, making it a top partner for leading alcohol producers.

Smurfit Kappa advances e-commerce and paper-based alcohol packaging

Smurfit Kappa is spearheading sustainable secondary packaging solutions for e-commerce alcohol markets. Its Bag-in-Box wine solution (May 2025) and TopClip multipack bundling system highlight its leadership in plastic-free, recyclable alternatives. Its vertically integrated model from forestry to manufacturing ensures supply security and material consistency. The launch of its eBottle portfolio for online alcohol deliveries positions Smurfit Kappa as a preferred partner for brands prioritizing damage protection, consumer convenience, and sustainability.

Amcor plc scales presence through Berry Global merger

Amcor offers flexible pouches, PET bottles, and specialty cartons across traditional and emerging alcohol categories. Its April 2025 merger with Berry Global created a $24 billion global leader in consumer and healthcare packaging, strengthening its alcohol sector position. Its AmPrima™ recycle-ready materials and PCR integration strategy are central to helping alcohol brands meet sustainability targets. Amcor’s one-stop-shop solutions for bottles, closures, and labels, combined with its global scale, make it an indispensable packaging partner for multinational beverage companies.

Diageo plc integrates premiumization with packaging innovation

As one of the largest alcohol producers, Diageo directly influences packaging trends. Its August 2025 supply chain restructuring improved efficiency, while its expansion into non-alcoholic beverages (e.g., Seedlip, Guinness 0.0) requires packaging innovations for product integrity. With a $500 million tequila expansion in Mexico, Diageo is driving demand for specialized glass bottles and closures. Its premium brands like Johnnie Walker and Smirnoff rely on bespoke packaging for storytelling, authenticity, and luxury perception.

Pernod Ricard S.A. strengthens premium spirits packaging with “Growth Ambition” plan

Pernod Ricard is advancing its premiumization strategy under its “Growth Ambition” plan, consolidating its portfolio to focus on high-growth brands like Jameson, Absolut, and Chivas Regal. In August 2025, Pernod Ricard USA announced a new Route-to-Market strategy, enhancing distributor partnerships and requiring packaging innovation for improved logistics. Its collaborations with suppliers emphasize iconic designs, eye-catching decoration, and sustainable materials, reinforcing packaging as a key differentiator in global spirits branding.

Alcohol Packaging market Share Insights

Market Share by Product Type in Alcohol Packaging

Glass bottles dominate the global alcohol packaging market with a commanding 58% share in 2025, underscoring their entrenched role in the wine and spirits segments where tradition, brand identity, and consumer perception of quality remain paramount. Glass is valued for being chemically inert, providing a neutral taste profile while supporting premium branding with unique shapes, embossing, and labeling. Despite challenges around weight, transport costs, and environmental impact, innovation in lightweight glass and higher recycled cullet content ensures bottles maintain leadership. Cans, accounting for 23% of the market, are the fastest-growing format, propelled by the explosion of craft beer, hard seltzers, and ready-to-drink (RTD) cocktails. Aluminum cans offer lightweight portability, superior recyclability, rapid chilling, and excellent barriers against light and oxygen, which extend the shelf life of hop-sensitive beers. Kegs remain a vital bulk solution, particularly in the on-premise draught beer segment, serving both global beer giants and craft brewers that rely on smaller keg formats for taproom distribution. Their reusability also supports sustainability commitments within the brewing industry. Bag-in-Box and pouches serve as niche yet strategic formats in value-driven markets, especially for commercial wines and portable alcohol options. Bag-in-Box provides excellent oxygen barriers and post-opening shelf life, making it a practical solution for high-volume consumption, while pouches offer affordability and convenience but struggle with premium perception. These emerging alternatives highlight how packaging innovation continues to diversify beyond traditional dominance.

Market Share by Application in Alcohol Packaging

Beer leads the alcohol packaging market with 45% of the share in 2025, reflecting the sheer scale of global beer consumption and its reliance on both bottles and cans. This category is also the most dynamic in packaging trends, with aluminum cans gaining momentum due to the rise of craft brewers and hard seltzers that favor the portability, sustainability, and branding versatility of cans. Glass still holds ground in premium beer offerings but faces mounting competition. Spirits account for 30% of the market, serving as the stronghold of glass bottles. Spirits demand packaging that reinforces premiumness and authenticity, with brands investing heavily in customized glass bottle shapes, embossing, and closures to differentiate in a crowded market. While the bulk of spirits remain glass-bound, RTD cocktails have started introducing cans as a disruptive alternative within this traditionally glass-dominated category. Wine represents a market in transition. While premium and luxury wine continues to rely on traditional glass bottles with cork closures, commercial wine segments are steadily adopting alternative packaging formats such as Bag-in-Box, aluminum cans, and premium pouches. These formats address consumer demand for affordability, lightweight transport, and single-serve convenience, slowly reshaping glass’s dominance in the category. Other alcoholic beverages, including cider, sake, and hard kombucha, represent the innovation hub of the market. With agile brands and experimental consumers, this segment often pioneers new packaging solutions, ranging from recyclable pouches to sustainable hybrid designs, before they scale into mainstream categories. This demonstrates how smaller beverage categories act as testbeds for the future of alcohol packaging innovation.

United States: Lightweighting, Smart Packaging, and E-Commerce Fuel Innovation in Alcohol Packaging

The United States alcohol packaging market is undergoing rapid transformation, driven by a dual focus on sustainability and consumer engagement. Leading companies like O-I Glass are investing heavily in lightweight glass manufacturing to meet the surging demand for recyclable bottles while reducing the carbon footprint associated with logistics and production. At the same time, the market has witnessed explosive growth in aluminum cans for wine, cocktails, and ready-to-drink (RTD) beverages, with players like Ball Corporation scaling up new production facilities to capture this demand. Beyond sustainability, smart packaging technologies are reshaping consumer engagement, with QR codes and digital-enabled labels providing recipes, authenticity checks, and brand stories directly to consumers. The U.S. alcohol e-commerce boom has also accelerated demand for durable, protective, and visually appealing secondary packaging designed to minimize breakage during shipping while reinforcing premium brand identity. Meanwhile, technological advancements in digital printing and direct-to-can labeling are enabling cost-efficient, personalized, and limited-edition packaging runs that resonate strongly with U.S. consumers’ preference for customization.

China: Premiumization of Spirits and High-Speed Production Reshaping Alcohol Packaging Demand

China’s alcohol packaging market is heavily influenced by the premiumization of traditional spirits such as baijiu and rice wine, with manufacturers investing in high-end packaging solutions like decorative glass bottles, ornate closures, and luxury presentation boxes. This focus on elevating perceived value aligns with the growing demand for premium and luxury alcohol segments across China’s middle and upper classes. Younger consumers are also shifting preference toward recyclable metal cans for beer and RTD beverages, signaling a transition away from traditional glass in mass-market categories. On the production side, Chinese packaging manufacturers are deploying high-speed automated lines for both glass and metal formats to cater to the massive domestic consumption volumes. Furthermore, the rise of e-commerce platforms such as Alibaba and JD.com has redefined packaging priorities, with durability, tamper resistance, and digital-first branding becoming essential for attracting online shoppers. This mix of premiumization, convenience-driven packaging, and digital retail influence makes China a focal point for global alcohol packaging innovation.

Germany & France: Sustainability and Refillable Packaging Driving European Alcohol Packaging Leadership

Germany and France are at the forefront of sustainable alcohol packaging innovation, driven by strict European Union regulations such as the Packaging and Packaging Waste Regulation (PPWR) and circular economy initiatives. European manufacturers are pioneers in lightweight glass technology, producing bottles up to 35% lighter than traditional formats, as seen with Champagne Telmont’s initiative. Luxury brands are also embracing refillable and reusable systems, with Rémy Martin introducing refillable glass for Club Cognac and The Macallan launching bottles crafted from recycled materials. Paper-based bottle innovation is another defining trend, with Johnnie Walker’s collaboration with Pulpex and Maison Ruinart’s “second skin” paper pulp casing reducing packaging-related carbon emissions by up to 60%. These initiatives highlight how Germany and France are not only meeting regulatory requirements but also setting global benchmarks for sustainable, luxury, and innovative alcohol packaging.

India: Young Consumer Base and Sustainability Campaigns Reshaping Alcohol Packaging Growth

India’s alcohol packaging market is expanding rapidly, powered by its young, urban, and aspirational consumer base seeking modern, convenient formats such as cans, pouches, and lightweight bottles. The industry is simultaneously embracing sustainability, with Pernod Ricard India eliminating mono-cartons and ITC collaborating with Frugalpac to introduce paper bottles made from 94% recycled material. Indian beverage companies are also committing to aggressive environmental targets, with Bira91 aiming for carbon neutrality by 2025 and pursuing zero-waste-to-landfill strategies. Local sourcing is another pillar of growth, as seen with Sula Vineyards sourcing 99% of its bottles from domestic vendors in Maharashtra to reduce transport emissions and strengthen supply chain resilience. Together, these initiatives showcase how India is balancing consumer-driven convenience with corporate sustainability and local manufacturing, making it one of the fastest-evolving alcohol packaging markets in Asia.

Brazil: Cans and RTDs Leading the Shift Toward Sustainable and Affordable Alcohol Packaging

Brazil’s alcohol packaging market is witnessing a strong consumer shift toward cans and RTD formats, with single-serve metal packaging becoming the dominant choice for beer, cocktails, and spirits. The country’s exceptionally high aluminum recycling rate makes cans an environmentally and economically attractive option, supporting the government and industry’s sustainability agendas. Companies like Crown Holdings are investing in new production facilities in Brazil to manufacture two-piece aluminum cans, underscoring the long-term growth potential of this packaging format. These investments align with the broader market’s preference for portable, cost-effective, and eco-friendly packaging solutions, positioning Brazil as a regional leader in sustainable alcohol packaging transformation.

Japan: Premium Craft Packaging and Recycling Laws Driving Market Evolution

Japan’s alcohol packaging market is shaped by two key forces premium craft positioning and strict recycling laws. Government initiatives such as the Containers and Packaging Recycling Law and the Act on Promotion of Resource Circulation for Plastics are compelling beverage manufacturers to prioritize lightweight, recyclable materials. At the same time, Japan’s vibrant craft spirits and beer industries are fueling demand for premium, artisanal glass bottles designed to highlight craftsmanship and luxury. Technological innovation plays a pivotal role, with manufacturers developing packaging solutions featuring advanced oxygen and UV barriers to preserve the integrity of high-value wines and aged spirits. Additionally, the rise of low- and no-alcohol beverages in Japan is spurring fresh demand for innovative, health-oriented packaging formats that appeal to younger and health-conscious consumers. These combined dynamics reinforce Japan’s reputation as a leader in premium, sustainable, and technologically advanced alcohol packaging solutions.

Alcohol Packaging Market Report Scope

Alcohol Packaging market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$82.4 Billion

|

|

Market Size (2034)

|

$136.9 Billion

|

|

Market Growth Rate

|

5.8%

|

|

Segments

|

By Material (Glass, Metal, Plastic, Paper & Paperboard, Others), By Product Type (Bottles, Cans, Pouches, Bag-in-Box, Kegs, Other Packaging), By Application (Beer, Wine, Spirits, Other Alcoholic Beverages)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Ball Corporation, Ardagh Group S.A., Crown Holdings, Inc., Smurfit Kappa Group, Gerresheimer AG, Vidrala S.A., Verallia S.A., O-I Glass, Inc., Mondi plc, Graphic Packaging International, WestRock Company, CAN-PACK S.A., Bormioli Luigi S.p.A., Tetra Pak

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Alcohol Packaging market Segmentation

By Material

- Glass

- Metal

- Plastic

- Paper & Paperboard

- Others

By Product Type

- Bottles

- Cans

- Pouches

- Bag-in-Box

- Kegs

- Other Packaging

By Application

- Beer

- Wine

- Spirits

- Other Alcoholic Beverages

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Alcohol Packaging market

- Amcor plc

- Ball Corporation

- Ardagh Group S.A.

- Crown Holdings, Inc.

- Smurfit Kappa Group

- Gerresheimer AG

- Vidrala S.A.

- Verallia S.A.

- O-I Glass, Inc.

- Mondi plc

- Graphic Packaging International

- WestRock Company

- CAN-PACK S.A.

- Bormioli Luigi S.p.A.

- Tetra Pak

* List Not Exhaustive

Research Coverage

This report investigates the Alcohol Packaging market with a focused lens on premiumization, sustainability breakthroughs, e-commerce adaptation and format innovation; the study synthesizes recent commercial pilots, M&A activity, material technology breakthroughs and market-entry case studies, and analysis reviews of lightweighting, recycled-content strategies and D2C logistics all to reveal practical trade-offs between brand equity, cost-to-serve and environmental performance. The report highlights region-specific regulatory impacts, high-value format shifts (cans, glass, pouches, Bag-in-Box), and secondary-packaging innovations that materially affect shelf appeal and breakage rates, and this report is an essential resource for packaging strategists, procurement leaders, brand and sustainability teams, and investors seeking evidence-based recommendations. USDAnalytics combines proprietary modelling, primary interviews with brand and converter executives, and scenario testing to map priority investments, supplier capabilities and roadmaps that support premium launches, circularity targets and resilient omnichannel distribution.

Scope Highlights

- Segmentation: By Material (Glass, Metal, Plastic, Paper & Paperboard, Others); By Product Type (Bottles, Cans, Pouches, Bag-in-Box, Kegs, Other Packaging); By Application (Beer, Wine, Spirits, Other Alcoholic Beverages).

- Geographic Scope: “Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.”

- Timeframe: Historic data from 2021–2024 and forecast horizon 2025–2034.

- Companies: Market analysis and executive profiles of 15+ strategic players across glassmakers, canmakers, converters and paper/board specialists.

Methodology

The study uses a mixed-methods research design that blends structured primary interviews with procurement leads, brand marketing and R&D teams, converter operations managers and logistics specialists, together with secondary research drawn from corporate reports, regulatory texts, patent filings and trade-show disclosures; market sizing deployed hybrid bottom-up and top-down modelling that reconciles plant capacity, SKU penetration, channel shifts (retail vs D2C) and historical shipment trends, while scenario and sensitivity analyses quantify impacts from recycled-content targets, lightweighting initiatives, tariff shocks and e-commerce growth. Technology adoption curves and recyclability claims were validated via supplier pilot data, independent lab test summaries and LCA inputs where available; findings were stress-tested against breakage, cost-to-serve and regulatory permutations to generate pragmatic, procurement-grade recommendations.

Deliverables:

• Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

• Country-Specific Forecasts & Analysis.

• Segment-Wise Revenue Forecasts (2025–2034).

• Competitive Analysis, Benchmarking, and SWOT Profiles.

• Recent Developments & Innovation Tracker.

• Executive Summary & Analyst Commentary.

• Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.