Market Overview: Platform-Level Substitution and Electrification Redefine the Role of Plastic Adhesives

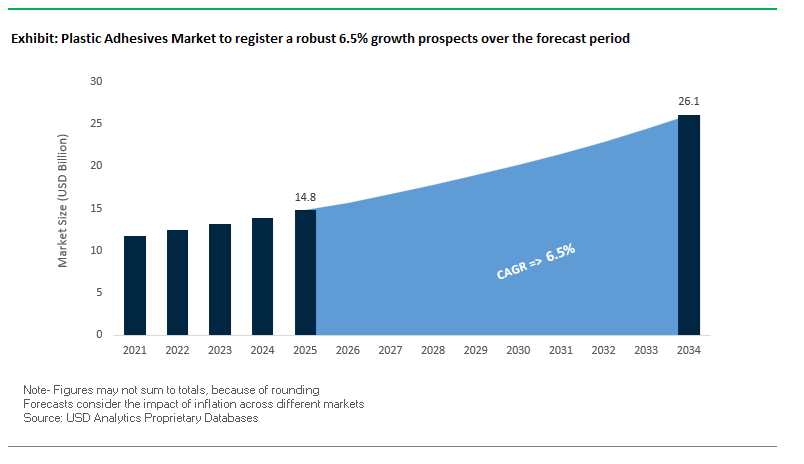

The Global Plastic Adhesives Market is projected to expand from USD 14.8 billion in 2025 to USD 26.1 billion by 2034, advancing at a CAGR of 6.5%, as adhesive bonding becomes structurally embedded in how products are designed, assembled, and regulated across automotive, electronics, construction, and medical sectors. Growth is increasingly driven by platform-level substitution of welding and mechanical fastening, rather than incremental volume expansion, as manufacturers prioritize lightweighting, electrification, and energy-efficient production architectures.

In automotive manufacturing, plastic adhesives are now specified as load-bearing elements rather than auxiliary joining materials. Electric vehicle platforms, in particular, rely heavily on structural adhesive bonding to manage mixed-material architectures and crash energy paths. Leading OEMs—including Tesla, Ford, and Volkswagen—have integrated adhesive bonding into nearly 80% of vehicle chassis assembly, reflecting a shift toward adhesive-centric body-in-white and battery pack designs. High-strength plastic adhesives enable reliable bonding between aluminum, composites, and thermoplastics, while reducing part count, mitigating galvanic corrosion, and contributing to overall vehicle weight reduction and energy efficiency.

Electronics and semiconductor manufacturing are reinforcing demand through a different performance lens. The rapid proliferation of ADAS modules, PCBs, and LiDAR sensors is driving adoption of thermally conductive and dual-curing plastic adhesives capable of managing heat while maintaining dimensional stability in compact, high-density assemblies. Suppliers such as Henkel and 3M continue to expand portfolios of thermally conductive epoxies and acrylics to support sensor fusion, camera modules, and power electronics, where adhesive failure directly affects signal accuracy and device reliability. At the same time, dual-curing systems that combine UV fixation with moisture or thermal cure are gaining importance in automated lines, allowing rapid handling strength without compromising deep-section cure in complex geometries.

The plastic adhesives industry is characterized by strategic consolidation, sustainability milestones, and R&D breakthroughs in adhesive chemistry and polymer innovation.

In October 2025, Orlen announced plans to acquire Grupa Azoty Polyolefins, strengthening upstream control of polyolefin feedstocks vital to adhesive production. This vertical integration move aims to stabilize raw material costs and secure long-term polymer supply chains for adhesive manufacturers, particularly in Europe’s construction and automotive sectors. In the same month, Syensqo introduced a low-density High-Performance Polyamide (HPPA) tailored for consumer electronics, creating fresh demand for high-strength plastic adhesives optimized for thinner, lighter, and heat-resistant device assemblies.

In September 2025, Parker Hannifin’s LORD division completed the acquisition of a North American composite bonding specialist, expanding its portfolio of urethane and acrylic structural adhesives for heavy-duty applications such as truck chassis and construction machinery. Around the same period, Sika AG achieved a Silver Medal from EcoVadis in August 2025, marking its leadership in sustainable adhesive manufacturing, notably through eco-friendly tinplate cartridge systems that reduce environmental footprint across its packaging lines.

In July 2025, Sika also signed a joint venture agreement with Sulzer to develop new plastics recycling technologies for construction materials—an initiative that will support future adhesive formulations derived from recycled polymers. Earlier, in March 2025, Sika was recognized by the European Patent Office (EPO) as one of the top Swiss innovators for adhesive technology patents, particularly in polyurethane (PU) and silane-terminated polymer (STP) systems, underscoring its continuous innovation drive.

Other key milestones include 3M’s partnership with Nordson (August 2024) to deploy automated bonding systems integrating rapid-curing adhesives for industrial assembly, and Parker Lord’s release (February 2025) of advanced structural acrylic adhesives that enhance off-road vehicle durability by replacing welds and fasteners. Meanwhile, Sika’s acquisition of Marlon Tørmørtel A/S (October 2024) bolstered its Northern European footprint in building adhesives.

Market Trend 1: Development of Low-Surface-Energy (LSE) Compatible Structural Adhesives for Untreated Plastics

One of the most significant technological shifts in the plastic adhesives market is the development of LSE-compatible structural adhesives that eliminate the need for costly and time-sensitive surface pre-treatments such as plasma, flame, or corona discharge. Traditional thermoplastics like polypropylene (PP), polyethylene (PE), and thermoplastic polyolefins (TPOs) present inherent challenges to adhesion due to their low surface energy, typically below 40 mN/m.

Recent innovations in adhesive chemistry are enabling direct bonding to untreated LSE substrates, drastically improving production efficiency. A global adhesive leader has introduced a methyl methacrylate (MMA)-based adhesive capable of forming high-strength bonds on untreated PP and PE, achieving robust adhesion under demanding environmental conditions. The two-part acrylic system offers superior resistance to vibration, moisture, and temperature fluctuations—making it particularly valuable in automotive interiors, medical devices, and industrial plastic assemblies.

The removal of pre-treatment steps marks a pivotal breakthrough. Standard surface activation techniques often degrade quickly—losing effectiveness on silicone rubber within minutes and on polyethylene or polypropylene within weeks. By removing dependency on these time-sensitive processes, direct-to-substrate LSE adhesives deliver both cost and process efficiency advantages, while maintaining high structural integrity across large assemblies such as tanks, housings, and molded components.

In addition, the shift to low-energy bonding is facilitating the expanded use of commodity polyolefins in applications previously limited to higher-cost engineering plastics, offering both weight reduction and material cost savings in high-volume production lines. The represents a major leap forward for manufacturers seeking structural bonding solutions that deliver both durability and design freedom.

Market Trend 2: Accelerated Shift Toward Bio-Based Polyurethane and Polyolefin Hot-Melt Adhesives

Sustainability is a defining force within the plastic adhesives industry, driving the transition from petroleum-based to bio-based polyols and tackifiers. Brand owners’ carbon-reduction commitments and regulatory frameworks targeting Scope 3 emissions are compelling adhesive manufacturers to develop low-carbon, renewable formulations without sacrificing mechanical or chemical performance.

A standout innovation comes from a specialty chemicals company utilizing Cashew Nutshell Liquid (CNSL)—a non-food, annually renewable biomaterial—to create polyols for bio-based polyurethane adhesives. These formulations offer superior moisture resistance, thermal stability, and substrate compatibility, particularly for polymer bonding, automotive, and industrial coatings applications.

In high-value electronics manufacturing, one adhesives company has launched a bio-based polyurethane reactive (PUR) hot melt adhesive containing 40% renewable content. The new generation of sustainable PUR adhesives provides high adhesion strength across materials like ABS, PC, PMMA, stainless steel, and aluminum, proving that bio-based solutions serve precision assembly markets as well.

The larger market opportunity lies in the bio-polyolefin adhesives sector, where formulations derived from starch, lignin, and vegetable oils are being scaled up to replace conventional petroleum feedstocks. These systems not only lower lifecycle carbon footprints but also align with ESG-focused procurement strategies, cementing bio-based adhesives as a strategic pillar of the sustainable plastics ecosystem.

Market Opportunity 1: Enabling Multi-Material Lightweighting in Electric Vehicle Battery Systems and Interiors

The rise of electric vehicles (EVs) represents a transformative growth avenue for plastic adhesive manufacturers, particularly in the areas of battery assembly, thermal management, and lightweight structural bonding. As OEMs seek to reduce vehicle mass and increase range, the integration of plastics, composites, and aluminum in EV construction is accelerating, replacing mechanical fasteners with high-strength structural adhesives that provide superior stress distribution and thermal regulation.

In EV battery systems, thermally conductive adhesives are essential for bonding cells to cooling plates, allowing for efficient heat dissipation that extends battery life and supports rapid charging capabilities. Further, non-silicone sealants are used to ensure moisture and dust ingress protection within battery enclosures, meeting stringent durability standards in high-voltage environments.

Inside the cabin, lightweight polymer components and composite panels are increasingly joined using high-performance plastic adhesives, which reduce vibration, noise, and structural fatigue over time. These adhesives play a pivotal role in maintaining rigidity while accommodating expansion from temperature fluctuations—a key factor in meeting automotive reliability benchmarks such as 500-hour thermal cycling tests between -40°C and 120°C.

The evolution positions structural plastic adhesives as a core technology underpinning EV lightweighting, enabling the next generation of efficient, durable, and thermally stable electric vehicles.

Market Opportunity 2: Servicing the Advanced Recycling and Monomaterial Packaging Value Chain

A parallel growth opportunity lies in the recyclable packaging adhesives market, which is becoming indispensable to achieving global circular economy goals. As major consumer goods companies commit to 100% recyclable or compostable packaging by 2025–2030, the shift from multi-layer, multi-material films to monomaterial packaging (PE-to-PE or PP-to-PP) has become critical.

Advanced laminating adhesives enable the creation of single-polymer flexible packaging that can be efficiently processed in existing mechanical recycling streams. These adhesives maintain high green bond strength, optical clarity, and barrier performance, ensuring that the resulting films maintain both durability and recyclability.

Recent studies on polyolefin-based recyclable films coated with advanced barrier layers confirm that mechanical reprocessing via extrusion and compression molding preserves tensile strength and elongation comparable to virgin materials, provided that adhesive chemistries remain chemically compatible with the dominant polymer stream.

The emerging segment is expected to see widespread adoption across food, pharmaceutical, and personal care packaging, as it aligns with upcoming Extended Producer Responsibility (EPR) legislation and recycling infrastructure compatibility standards, such as APR’s Critical Guidance Protocols. Adhesive producers that develop recycling-neutral formulations will occupy a strategic advantage in supporting global packaging circularity.

Plastic Adhesives Market Share Insights, 2025-2034

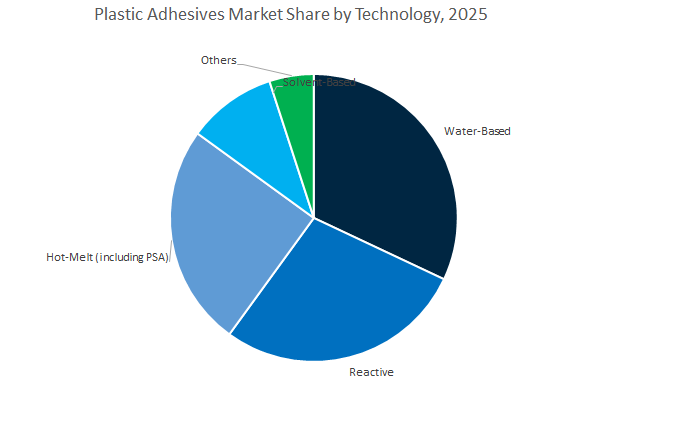

Market Share by Technology

The water-based plastic adhesives segment leads the global plastic adhesives market, accounting for an estimated 32.2% share in 2025. This dominance stems from the growing enforcement of VOC emission regulations and the shift toward eco-friendly adhesive technologies across industries. Water-based systems provide reliable adhesion on a variety of thermoplastics, including PVC, ABS, and polyethylene, making them ideal for packaging, construction, and consumer goods applications. Their superior workability, non-flammability, and compatibility with automated assembly lines contribute to their widespread adoption. Additionally, global sustainability initiatives and the rapid expansion of recyclable packaging materials have further accelerated the demand for low-toxicity, water-dispersed adhesive chemistries. In Europe and North America, the phaseout of solvent-based formulations has intensified the transition toward advanced aqueous acrylic and polyurethane-based systems, positioning water-based adhesives as the technology of choice for regulatory compliance and environmental performance.

The reactive adhesives segment is witnessing robust growth, driven by the need for high-strength, durable bonds in structural and performance-critical applications. Reactive systems—comprising epoxy, polyurethane, and methyl methacrylate-based chemistries—deliver superior resistance to heat, chemicals, and mechanical stress, making them indispensable in automotive, electronics, and medical device assembly. These adhesives have become pivotal in bonding dissimilar materials such as plastics to metals and composites, addressing the industry’s demand for lightweight hybrid assemblies. Meanwhile, hot-melt and pressure-sensitive adhesives (PSA) maintain a significant market presence due to their rapid curing and high processing efficiency, especially in packaging, labeling, and high-speed manufacturing lines. They are favored for their clean application, recyclability, and compatibility with automation, aligning with the industry’s shift toward high-output adhesive technologies. Solvent-based adhesives, once widely used for their strong initial tack and broad substrate compatibility, continue to decline as global regulations tighten on VOC and hazardous solvent emissions.

Market Share by Application

The packaging segment dominates the global plastic adhesives market, holding a projected 30.9% share in 2025, underscoring the central role of adhesives in the production of flexible packaging, labels, pouches, and cartons. The segment’s leadership is reinforced by the global rise of e-commerce, food delivery, and sustainable packaging trends, which demand adhesives that offer high bond strength, fast curing, and compatibility with recyclable films. Plastic adhesives are crucial in lamination processes, providing clarity, chemical resistance, and barrier performance while ensuring food safety and regulatory compliance. The increasing adoption of bio-based films and lightweight packaging structures is further driving demand for advanced adhesive formulations that balance strength with sustainability.

The automotive and transportation sector represents one of the fastest-growing applications for plastic adhesives. The surge in electric vehicle (EV) production, coupled with lightweighting initiatives, has led to a dramatic increase in the use of engineering plastics and composites, driving the need for adhesives that can bond dissimilar materials. Adhesives are replacing mechanical fasteners and welding in vehicle interiors, exterior panels, and battery assemblies, delivering weight reduction, design flexibility, and improved structural integrity. The assembly segment maintains substantial market importance across consumer goods, appliances, and furniture manufacturing, where adhesives enable aesthetic design, efficient assembly, and cost-effective production.

The Global Plastic Adhesives Market is dominated by innovation-oriented companies leveraging advanced polymer chemistry, automation, and sustainability-driven product lines. Henkel, 3M, Sika, Parker Hannifin (LORD Division), and Arkema Group (Bostik, Sartomer) are among the top players shaping the future of adhesives through strategic investments and breakthrough formulations.

Henkel’s Adhesive Technologies division continues to lead globally with its Loctite brand, providing polyurethane, epoxy, and structural adhesives for critical automotive bonding applications, including EV battery modules and Body-in-White (BiW) structures. In 2024, Henkel expanded its Asia-Pacific manufacturing facilities to meet growing regional demand for solvent-free and water-based laminating adhesives. Through its “Adhesives for Tomorrow” strategy, the company prioritizes low-VOC, bio-based, and recyclable formulations, ensuring compliance with REACH and other global regulations. Henkel also remains a leader in thermal management adhesives for EVs, offering flame-retardant gap fillers that enhance vehicle safety and energy efficiency.

3M remains a global leader in structural acrylic adhesives under its Scotch-Weld™ and VHB™ product lines. Its acrylic foam tape systems offer robust bonding on low surface energy (LSE) plastics like polypropylene (PP) and polyethylene (PE)—with minimal surface preparation required. In 2024, 3M expanded its VHB Tapes portfolio featuring viscoelastic cores that dampen vibration and absorb stress between dissimilar materials, a critical feature for high-stress automotive and industrial assemblies. With three global R&D hubs across the U.S., Germany, and China, 3M continues to support high-precision adhesive testing and application development for next-generation plastic substrates and modular assemblies.

Sika AG holds a leading position in polyurethane and hybrid adhesive systems, serving industries ranging from automotive to construction. Its SikaPower® SmartFlow adhesives are optimized for bonding aluminum profiles and structural composites in lightweight EV assemblies. The company’s Purform® technology represents a breakthrough in low monomeric diisocyanate polyurethane adhesives, ensuring compliance with new EU safety standards while maintaining superior mechanical performance. Sika’s strategy also includes a circular economy focus, evidenced by its 2025 partnership with Sulzer to enhance plastics recycling in construction materials, and ongoing R&D efforts in AI-enabled concrete and adhesive formulation optimization.

Parker LORD, a division of Parker Hannifin, continues to dominate in urethane, epoxy, and acrylic adhesives for industrial, transportation, and heavy-equipment manufacturing. With over 40 years of expertise, LORD adhesives are engineered to bond composites, plastics, and foams under demanding environmental conditions. Its aggressive acrylic adhesives require minimal surface preparation, improving production efficiency and reducing VOC emissions on assembly lines. The company’s engineering partnership model assists manufacturers transitioning from mechanical fastening to structural adhesive bonding, providing cost modeling and process optimization for clients across North America and Europe.

Arkema’s Bostik and Sartomer divisions leverage deep expertise in specialty polymers like polyamide and PVDF to deliver advanced Cyanoacrylate and Methyl Methacrylate (MMA) adhesives for medical, automotive, and electronics applications. Through ongoing R&D in light-curing and 3D printing materials, Arkema supports the additive manufacturing of complex plastic parts requiring precision bonding. Its flame-retardant adhesive formulations meet stringent UL and FAR standards, ensuring compliance for aerospace and mass transit interiors. Further, Bostik’s Hot Melt Pressure-Sensitive Adhesives (HMPSA) enhance flexible packaging and nonwoven plastic film bonding, positioning Arkema as a key enabler of high-speed sustainable manufacturing.

Country Analysis: Regional Dynamics and Strategic Advancements in the Global Plastic Adhesives Industry

China: Expanding Asia-Pacific Leadership Through Technological Upgrades and Policy-Driven Innovation

China continues to dominate as the Asia-Pacific hub for plastic adhesives, supported by rapid industrialization, government incentives, and foreign direct investments. The acquisition of Crevo-Hengxin by Sika AG underscores China’s role as a manufacturing and R&D base for sealing and bonding technologies in the construction and automotive sectors. With the “Made in China 2025” initiative, the government is prioritizing the domestic production of high-end materials and specialty adhesives, accelerating the local innovation ecosystem for engineering plastics and high-performance bonding materials.

The nation’s growing electric vehicle (EV) and flexible packaging sectors are transforming adhesive consumption patterns. Rising adoption of polyurethane and epoxy adhesives for battery pack assembly, plastic-to-metal bonding, and chassis components aligns with China’s automotive lightweighting strategy. Moreover, environmental mandates are pushing adhesive producers toward solvent-free and water-based systems, minimizing volatile organic compound (VOC) emissions and supporting sustainable packaging solutions. China’s infrastructure expansion—including high-speed rail and urban megaprojects—continues to drive demand for PVC adhesives and high-performance bonding agents across construction plastics.

United States: Sustainability, R&D Collaboration, and Technological Leadership in Specialty Plastic Adhesives

The United States plastic adhesives industry remains at the forefront of sustainability innovation and high-performance bonding solutions, driven by cross-sector technological integration. Companies like 3M and H.B. Fuller are spearheading advancements in long-wear medical adhesives, structural bonding, and industrial assembly applications. For instance, 3M’s 28-day wear medical adhesive represents a major leap for extended-use devices, enhancing reliability and comfort in medical wearables. Meanwhile, collaborations between 3M and Nordson are streamlining manufacturing processes by integrating VHB tapes with liquid adhesives, offering automated, fast-curing bonding systems that improve production efficiency and sustainability.

Strategic acquisitions continue to shape market dominance, with H.B. Fuller’s acquisition of Beardow Adams expanding its global technology portfolio and customer reach. The focus on e-commerce and food-safe packaging adhesives is reinforcing the U.S.’s leadership in functional and regulatory-compliant adhesive solutions. Additionally, the aerospace and defense sectors rely on REACH-compliant epoxy structural adhesives, such as Henkel’s Loctite EA 9365FST, which meet stringent flame-retardancy and bonding requirements for aircraft interiors. On the domestic front, the construction and DIY markets are witnessing renewed adhesive demand, supported by Sika AG’s acquisition of DriTac’s flooring adhesives business, which strengthened its U.S. distribution footprint.

Germany: Sustainable Transformation and Advanced Plastic Bonding in Automotive and Industrial Applications

Germany’s plastic adhesives market is at the forefront of Europe’s green transformation, driven by the EU Circular Economy Action Plan and the Ecodesign for Sustainable Products Regulation (ESPR). German chemical manufacturers are pioneering bio-based and low-VOC polyurethane adhesives, designed for eco-friendly automotive and construction uses. The focus on sustainability is further amplified by corporate commitments from leading players like Henkel, which is investing in plastic-free and recyclable packaging adhesives to achieve its 2025 sustainability goals.

The automotive sector, Germany’s industrial backbone, is driving demand for thermal management adhesives critical to EV battery pack assembly. The materials provide high heat resistance and insulation, supporting vehicle safety and performance. German companies are also investing in chemical recycling-compatible adhesives, enabling full material recovery in polymer recycling systems. The integration of adhesive technology with circular economy practices demonstrates Germany’s strategic leadership in sustainable material design. Supported by a robust R&D ecosystem and advanced regulatory infrastructure, Germany remains the European benchmark for innovation in automotive, industrial, and eco-friendly plastic adhesives.

Japan: Precision Engineering and High-Performance Adhesives for Advanced Electronics and Packaging

Japan’s plastic adhesives industry is defined by precision engineering, miniaturization, and high-performance material science. As a global leader in consumer electronics, Japan drives demand for cyanoacrylate and UV-curing adhesives tailored for micro-components, sensors, and flexible displays. The formulations deliver instant bonding and high durability, essential for the country’s smartphone, robotics, and wearable device industries.

Under the philosophy of Monozukuri (craftsmanship innovation), Japanese companies continue to enhance adhesive technologies that enable strong, lightweight bonds between dissimilar materials such as metals, composites, and engineering plastics. The country’s growing focus on sustainable food packaging is also influencing adhesive design, with investments in high-barrier laminating adhesives capable of withstanding retort sterilization and high-temperature processes. The innovations cater to Japan’s thriving ready-to-eat food segment, where packaging performance and shelf-life stability are paramount. With continuous R&D in electronics adhesives and packaging materials, Japan remains a global pioneer in advanced and application-specific bonding technologies.

South Korea: Next-Generation Plastic Adhesives for Displays and Semiconductor Manufacturing

South Korea’s plastic adhesives market is rapidly expanding due to the country’s dominance in display and semiconductor manufacturing. The rise of foldable smartphones, OLED TVs, and flexible displays has created substantial demand for optically clear adhesives (OCA) and die attach adhesives engineered for plastic substrates. The advanced adhesives are designed to maintain optical transparency, flexibility, and durability in next-generation consumer electronics.

In parallel, the semiconductor and cleanroom adhesives segment is witnessing unprecedented growth. South Korean producers are developing ultra-pure epoxy adhesives with low outgassing properties that meet stringent cleanroom assembly standards. As domestic investment in semiconductor fabs continues, demand for precision bonding solutions for chip packaging and device encapsulation is accelerating. South Korea’s R&D intensity, combined with its technological ecosystem in display and electronics manufacturing, is solidifying its reputation as a global hub for high-purity and high-performance plastic adhesive innovation.

Brazil: Infrastructure and Packaging Growth Fueling Regional Adhesive Demand

Brazil represents the center of Latin America’s emerging plastic adhesives market, underpinned by rapid urbanization, infrastructure development, and retail modernization. The construction sector is witnessing a surge in PVC and PU adhesive consumption, particularly for pipe and fitting assembly, prefabricated components, and flooring applications. As large-scale residential and commercial projects proliferate, solvent-based and water-based adhesives are being widely adopted to enhance structural durability and reduce installation time.

Simultaneously, Brazil’s flexible packaging industry is growing rapidly, driven by rising middle-class consumption and expansion in modern retail and food processing sectors. Local adhesive manufacturers are scaling up production of high-tack lamination adhesives to cater to increasing demand from snack foods, personal care, and processed foods. Supported by an improving industrial base and regional integration initiatives, Brazil is positioning itself as Latin America’s strategic hub for packaging and construction-grade adhesive production.

Plastic Adhesives Market Report Scope

Plastic Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$14.8 Billion

|

|

Market Size (2034)

|

$26.1 Billion

|

|

Market Growth Rate

|

6.5%

|

|

Segments

|

By Resin Type (Epoxy, Polyurethane, Acrylic, Cyanoacrylate, Silicone, Polyvinyl Acetate, Polyolefin, Others), By Technology (Water-Based, Solvent-Based, Hot-Melt, Reactive, Others), By Substrate (Polyethylene, Polypropylene, Polyvinyl Chloride, Polystyrene, Polycarbonate, Acrylonitrile Butadiene Styrene, Polyethylene Terephthalate, Composite Plastics, Dissimilar Substrates), By Application (Packaging, Automotive & Transportation, Building & Construction, Assembly, Electrical & Electronics, Medical, Others

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, H.B. Fuller Company, 3M Company, Arkema S.A. (Bostik), Sika AG, The Dow Chemical Company, BASF SE, Huntsman Corporation, Dymax Corporation, Ashland Global Holdings Inc., Wacker Chemie AG, Covestro AG, Mapei S.p.A., Permabond LLC, Pidilite Industries Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Resin Type

- Epoxy

- Polyurethane

- Acrylic

- Cyanoacrylate

- Silicone

- Polyvinyl Acetate

- Polyolefin

- Others

By Technology

- Water-Based

- Solvent-Based

- Hot-Melt

- Reactive

- Others

By Substrate

- Polyethylene

- Polypropylene

- Polyvinyl Chloride

- Polystyrene

- Polycarbonate

- Acrylonitrile Butadiene Styrene

- Polyethylene Terephthalate

- Composite Plastics

- Dissimilar Substrates

By Application

- Packaging

- Automotive & Transportation

- Building & Construction

- Assembly

- Electrical & Electronics

- Medical

- Others

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Plastic Adhesives Market

- Henkel AG & Co. KGaA

- H.B. Fuller Company

- 3M Company

- Arkema S.A. (Bostik)

- Sika AG

- The Dow Chemical Company

- BASF SE

- Huntsman Corporation

- Dymax Corporation

- Ashland Global Holdings Inc.

- Wacker Chemie AG

- Covestro AG

- Mapei S.p.A.

- Permabond LLC

- Pidilite Industries Ltd.

*- List not Exhaustive

Research Coverage

This report investigates the Plastic Adhesives Market, delivering analysis reviews on demand shifts, qualification criteria, and cost-in-use levers as plastics replace welds and fasteners across mobility, electronics, construction, packaging, and medical; it highlights technology breakthroughs in structural bonding for EV lightweighting, LSE-compatible acrylics, dual-curing workflows for automated assembly, and next-gen water-based/bio-derived chemistries aligned to REACH and low-VOC operations; it maps supplier strategies, end-use adoption curves, and regulatory gating factors (thermal management, migration limits, recyclability interfaces) with defensible benchmarks on performance, reliability, and TCO. Built by USDAnalytics, this report is an essential resource for converters, OEMs, brand owners, and investors seeking clear positioning, materials roadmaps, and scenario-tested forecasts through 2034.

Scope Highlights

Segmentation:

- By Resin Type: Epoxy; Polyurethane; Acrylic; Cyanoacrylate; Silicone; Polyvinyl Acetate; Polyolefin; Others.

- By Technology: Water-Based; Solvent-Based; Hot-Melt; Reactive; Others.

- By Substrate: Polyethylene; Polypropylene; Polyvinyl Chloride; Polystyrene; Polycarbonate; Acrylonitrile Butadiene Styrene; Polyethylene Terephthalate; Composite Plastics; Dissimilar Substrates.

- By Application: Packaging; Automotive & Transportation; Building & Construction; Assembly; Electrical & Electronics; Medical; Others.

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa).

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Timeframe: Historic data 2021–2024 and forecast data 2025–2034.

Companies: Analysis/profiles of 15+ companies.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.